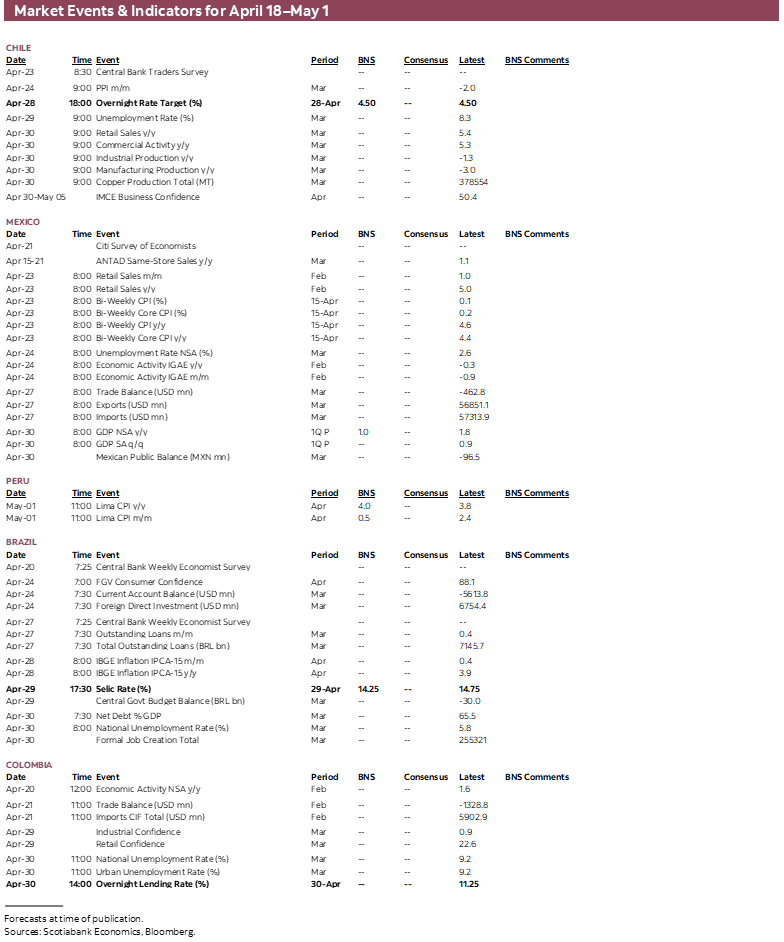

HIGHLIGHTS

- Once again, news out of the Middle East should remain the main driver of sentiment, with markets trading on an upbeat mood into the weekend. April PMIs from around the world are next week’s data highlight while traders await the next round of central bank decisions in late-April.

- The Latam calendar has a few bits and pieces on offer but none of them of major market relevance outside of H1-April CPI out of Mexico that should continue to reflect elevated fruits and vegetables prices due to adverse weather and a limited impact of higher global energy prices. Our colleagues in Mexico go over the IMF’s latest forecast update.

- Chilean markets will focus on the government’s planned submission to Congress of a reconstruction and economic package next week, which our local team discusses in today’s report.

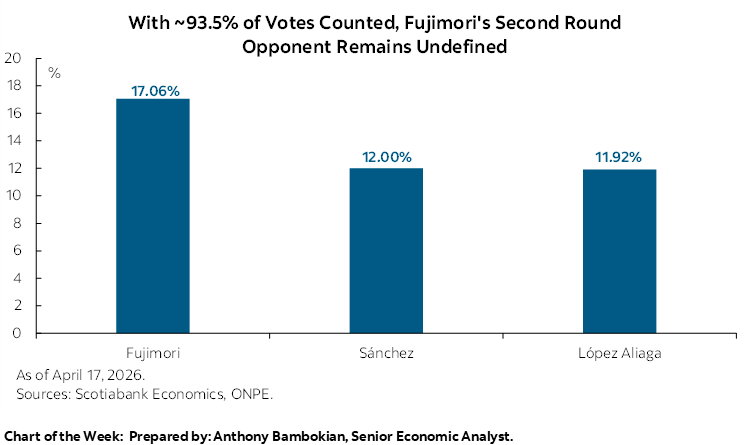

- In Peru, we’re waiting for who will face Fujimori at the June 7th presidential runoff, with the second-placed candidates neck-and-neck with 93.5% of votes counted so far. In today’s edition, the team in Peru highlight the country’s economic strength, and firm business confidence, contrasting with building inflationary risks.

Chart of the Week

MEXICAN CPI, CHILE’S ECONOMIC PLAN, AND PERU’S RESILIENCE VS. MIDDLE EAST NEWS

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Once again, news out of the Middle East should remain the main driver of sentiment, with markets trading on an upbeat mood into the weekend. April PMIs from around the world are next week’s data highlight while traders await the next round of central bank decisions in late-April.

- The Latam calendar has a few bits and pieces on offer but none of them of major market relevance outside of H1-April CPI out of Mexico that should continue to reflect elevated fruits and vegetables prices due to adverse weather and a limited impact of higher global energy prices. Our colleagues in Mexico go over the IMF’s latest forecast update.

- Chilean markets will focus on the government’s planned submission to Congress of a reconstruction and economic package next week, which our local team discusses in today’s report.

- In Peru, we’re waiting for who will face Fujimori at the June 7th presidential runoff, with the second-placed candidates neck-and-neck with 93.5% of votes counted so far. In today’s edition, the team in Peru highlight the country’s economic strength, and firm business confidence, contrasting with building inflationary risks.

Fast-paced Middle East developments over the past week have drastically shifted the near-term outlook for inflation and economic growth. This is, at least, as far as markets are concerned, taking Iranian, Israeli, and U.S. leaders to their word on the reopening of the Strait and the prospect of a longer-lasting end to military hostilities. Another round of negotiations over the coming days could strengthen or weaken the market’s conviction, although it may be a while before energy prices and fixed income markets price out crude oil and gas supply and inflation risks, respectively.

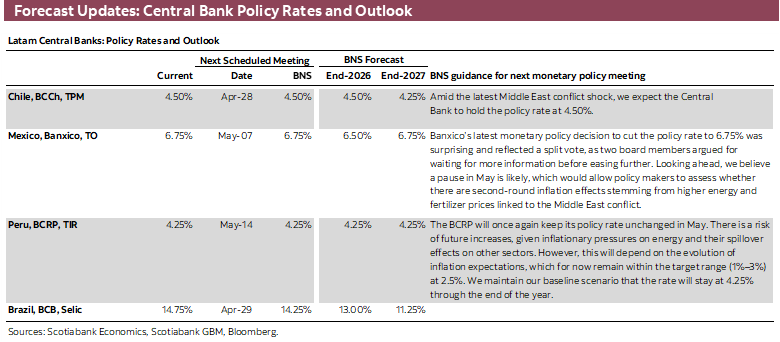

Once again, news out of the Middle East should remain the main driver of sentiment with traders paying particular attention to moves in commodity markets as we look ahead to the restart of central bank decisions on the week of the 27th. Were conditions to continue to improve, policymakers could soon return to baselines that are closer to pre-conflict settings although the unpredictability of geopolitics will likely see them maintain a cautious stance at their late-April/early-May announcements—where we see minimal odds of policy rate shifts.

On the data front, figures will continue to be generally backward-looking (pre-conflict) and one could argue that the period of staleness for data could extend until we get May prints at some point in June or July. Economic readings for March and April that would incorporate the negative impact of the conflict would offer few insights into the state of activity under would-be ceasefire conditions with lower energy prices and rebuilt sentiment in markets and among firms. Next Thursday’s April PMIs are the global highlight, but they may mix up pre- and post-ceasefire/Hormuz reopening opinions. Outside of Latam, Canadian, Japanese, and U.K. CPI, U.K. employment, and U.S. retail sales are the main (stale?) data to watch.

The Latam calendar has a few bits and pieces on offer but nothing that should be all that impactful outside of H1-April CPI out of Mexico, whose calendar also includes February economic activity and retail sales, March unemployment rate, and the results of Citi’s economists survey. The other countries in the region have much quieter weeks from a data standpoint, with nothing out of Brazil and Peru, only March PPI data in Chile, and Colombia’s February economic activity which—as in the case of Mexico—will speak to a different economic situation than at present.

Chilean markets will focus on the government’s planned submission to Congress of a reconstruction and economic package next week, which our local team discusses in today’s report. Meanwhile, in Peru, there is still not a clear second-placed candidate from last Sunday’s presidential vote that would face Fujimori at the June 7th runoff, with the left’s Sánchez and the right’s López Aliaga virtually tied with 93.5% of votes counted. Taking a step back from political developments, the economists in Peru highlight the country’s economic strength, and firm business confidence, contrasting with building inflationary risks—though these may perhaps be easing now.

Mexican inflation surged to 4.6% in March from 4% in February, all while reflecting only a marginal impact of the surge in global energy prices. The country’s cap on standard-grade (Magna) gasoline prices, which represents ~80% of total gasoline sales, and subsidies and measures to rein in higher-grade (Premium, ~20%) fuel prices has helped limit the inflation hit from the recent rise in crude oil prices. Last month, low-octane gasoline prices rose by 0.3% m/m compared to the 3.5% m/m increase in high-octane prices. In March, the clearest direct hit came from a 26.3% m/m rise in airfares (compared to +10.9% m/m in March 2025) as airlines quickly passed on higher jet fuel costs.

A steep rise in fruits and vegetables prices was an important contributor to last month’s jump in headline inflation, and should remain an upside factor in next week’s reading for 1H-Apr. Adverse weather conditions have impacted the supply of key agricultural products, such as tomatoes and potatoes, with the GCMA reporting that these rose 22% and 12% week-over-week, respectively, at the start of April, thus likely to keep inflation in the mid-4s in the near term before conditions normalize. As with the Middle East conflict, Banxico sees this as a transitory shock that will not see inflation deviate significantly from its convergence to the 3% target, which means officials could consider another rate cut at the April 7th decision.

In today’s Weekly, the team in Mexico go over the IMF’s latest forecast revisions published earlier this week, with the global body seeing Mexican GDP growth of 1.5% and 2.1% in 2026 and 2027—well below the 1% that we project for both years. While Mexico closed 2025 strongly, it started 2026 on the wrong foot with a 0.3% y/y contraction in economic activity (IGAE) in January. We’ll see what next week’s IGAE figures for February show, with industrial production, the only hard data at hand for the month, falling by 1.3% y/y, worse than its 1.1% y/y decline in January.

COUNTRY UPDATES

Chile—Government to Send Bill to Congress with Tax and Economic Reactivation Measures

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

On Wednesday, April 15th, the government announced a reconstruction and economic package combining fiscal mobilization, targeted stimulus, and regulatory reforms. The bill aims to restore fiscal balance, re-anchor medium-term growth toward a 4% trend, and scale up formal job creation. While the overall fiscal cost of the package remains undisclosed, the government has indicated that financing would rely primarily on higher revenues from an investment-led growth recovery, temporary revenue-raising measures, and fiscal spending cuts. It is expected to be sent to Congress on Tuesday, April 21st, with approval targeted for late August, ahead of the preparation of the 2027 budget.

The package is anchored by a gradual reduction in the corporate income tax rate, lowering the headline rate from 27% to 23% over the medium term to restore competitiveness and align Chile more closely with OECD benchmarks. This is complemented by a phased-in reintegration of the corporate-personal income tax system, culminating in full creditability of corporate taxes against personal taxes, thereby reducing distortions to profit distribution and investment decisions. To facilitate the transition from the semi-integrated regime, a temporary substitute tax allows firms to voluntarily convert existing corporate tax credits subject to restitution into fully usable credits through an upfront payment, advancing fiscal revenues while reducing future tax friction.

In parallel, the package introduces a time-limited foreign asset declaration and capital repatriation regime, aimed at mobilizing liquidity and generating immediate revenues, alongside a temporary reduction in the inheritance and donation tax to accelerate tax payments that would otherwise be deferred. On the social side, the package establishes a permanent exemption from property taxes on primary residences owned by individuals aged 65 and over, with full compensation to municipalities through transfers to the Municipal Common Fund, explicitly shifting the fiscal cost to the central government while preserving subnational revenue neutrality.

The second pillar of the package focuses on near-term demand support, employment protection, and regulatory certainty. A temporary VAT exemption on new housing sales seeks to accelerate the absorption of existing inventories and reactivate construction activity, while a payroll-based tax credit for formal employment directly reduces labour costs and improves firm liquidity, particularly for small- and medium-sized enterprises. These measures are complemented by the expansion of the Emergency Reconstruction Fund, providing immediate fiscal resources for post-disaster rebuilding.

On the regulatory and investment side, uncertainty is addressed through a permanent reduction in the administrative invalidation period for sectoral permits, limiting the window during which the granting authority itself may revoke previously issued permits, and through the creation of a targeted reimbursement mechanism for expenses incurred after a valid environmental approval (RCA) that is subsequently revoked or annulled by a final judicial ruling.

Finally, the package incorporates expenditure restraint through a four-year moratorium on the entry of new institutions into the tuition-free higher education system, curbing the structural growth of higher-education spending while preserving benefits for currently participating institutions and students.

Mexico—Global Growth Risks According to the IMF

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

The International Monetary Fund’s World Economic Outlook April 2026 Update describes a global macroeconomic environment that, while appearing broadly stable, remains highly vulnerable to adverse shocks. These vulnerabilities stem from the concentration of growth drivers in specific regions and sectors, as well as from a particularly fragile and volatile geopolitical context.

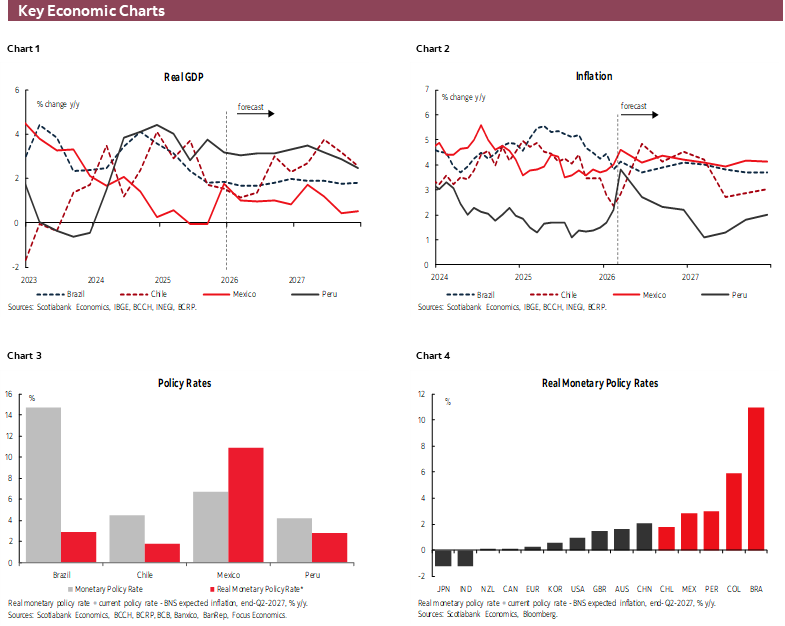

Global growth is projected at 3.3% in 2026 and 3.2% in 2027, figures that are broadly unchanged from 2025 and represent a slight upward revision relative to the October 2025 report. Meanwhile, the global inflation forecast continues to decline gradually, reaching 3.8% in 2026 and 3.4% in 2027, down from 4.1% in 2025. This growth outlook is underpinned primarily by factors that the IMF itself characterizes as fragile, including still-accommodative financial conditions, some fiscal impulse in advanced economies, and significant investment in high-technology sectors, particularly artificial intelligence. At the same time, elevated economic policy uncertainty persists, alongside the gradual tightening of certain trade restrictions, which has led to weaker momentum in international trade. Global trade growth is therefore projected to moderate to 2.6% in 2026 from 4.1% in 2025. The IMF emphasizes that this baseline scenario relies on relatively benign assumptions in an environment where the balance of risks remains clearly tilted to the downside.

Among the most relevant risks, the IMF explicitly highlights the potential escalation of geopolitical tensions, with particular emphasis on the conflict in the Middle East, as one of the main sources of systemic vulnerability. In an adverse scenario in which the conflict becomes prolonged and intensifies, the macroeconomic implications would be significant, affecting strategic shipping routes, critical infrastructure, and the production and transportation of oil and gas, thereby generating negative global supply shocks.

The primary transmission channel would be a renewed increase in energy prices, reversing the recent disinflationary trend. A sustained rise in oil and natural gas prices would raise production and transportation costs globally, exert upward pressure on inflation and erode households’ real incomes. This would force central banks to confront a difficult trade-off between containing inflation and supporting economic activity, potentially delaying or even halting the monetary easing cycles anticipated or already initiated by some central banks. This is particularly relevant given that monetary policy is effective in responding to demand-side shocks, but not to supply-side shocks such as higher energy prices driven by the Middle East conflict. The most likely outcome would be weaker global growth accompanied by more persistent inflation—an especially adverse environment for macroeconomic stability.

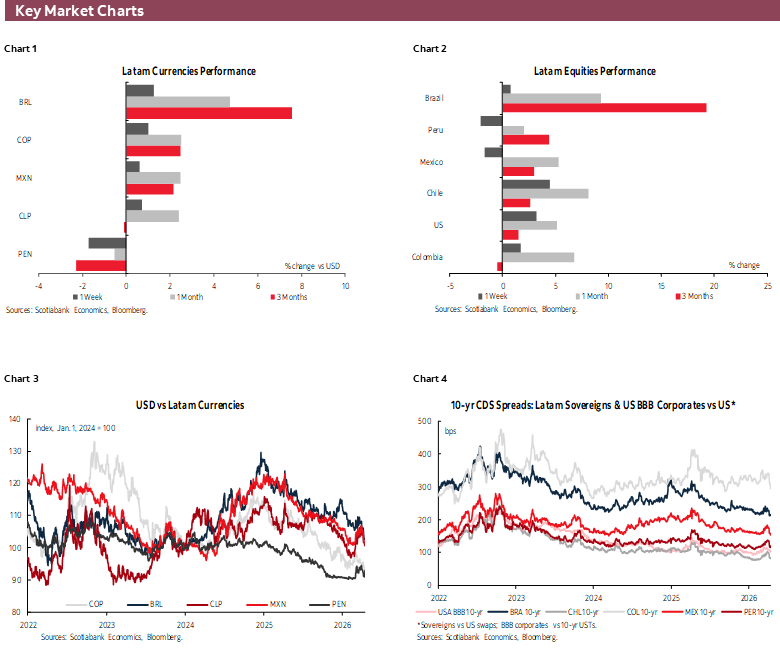

Similarly, an escalation of the Middle East conflict could exacerbate financial market volatility, increase risk premiums, and tighten global financial conditions. Economies with high public debt levels or heavy reliance on external financing would be particularly vulnerable. The combination of higher commodity prices, tighter financial conditions, and weaker international trade could amplify the initial negative effects, transforming a regional shock into an event of global scope.

For Mexico, this context entails significant risks. The IMF projects moderate economic growth of 1.5% in 2026 and 2.1% in 2027 (above our forecasts of 1.0% in each year). However, under a scenario of heightened conflict in the Middle East, Mexico would face inflationary pressures, particularly in energy and fertilizer prices, as well as a potential negative impact on external demand if global growth were to slow. These conditions would reduce the policy space for both monetary and fiscal policy, reinforcing the importance of preserving macroeconomic credibility, anchoring inflation expectations, and maintaining financial resilience.

Peru—Between the Strength of Economic Activity and Inflationary Risks

Ricardo Avila, Senior Analyst

ricardo.avila@scotiabank.com.pe

Economic growth in February reached 3.7% year-on-year, exceeding the consensus of analysts surveyed by Bloomberg and slightly accelerating compared to January (3.5%). As a result, GDP accumulated a 3.6% increase in the first two months of the year, above the estimated potential level of 3.0%. February’s acceleration was mainly driven by private investment dynamics and the strength of the labour market. In March, however, a significant slowdown is expected due to the temporary interruption of natural gas and Natural Gas Liquids (NGL) supply during the first half of the month.

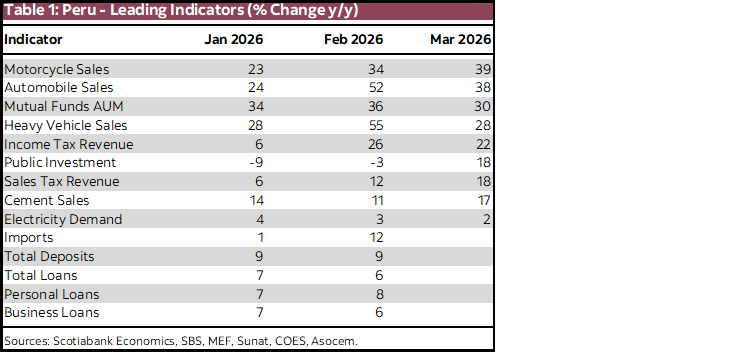

However, leading indicators and business expectations remain optimistic. Leading indicators (table 1) show that domestic demand continues to be solid, pointing to a strong first quarter (1Q26). On the side of private investment, cement demand and heavy vehicle sales continue to grow at double-digit rates, while electricity demand and business loans are also accelerating (the latter with data up to February). Regarding private consumption, mutual funds and vehicle sales maintained double-digit growth, and personal loans is expected to expand in March at levels close to 8%. Finally, tax revenues (from both companies and individuals) returned to double-digit growth.Economic growth in February reached 3.7% year-on-year, exceeding the consensus of analysts surveyed by Bloomberg and slightly accelerating compared to January (3.5%). As a result, GDP accumulated a 3.6% increase in the first two months of the year, above the estimated potential level of 3.0%. February’s acceleration was mainly driven by private investment dynamics and the strength of the labour market. In March, however, a significant slowdown is expected due to the temporary interruption of natural gas and Natural Gas Liquids (NGL) supply during the first half of the month.

However, leading indicators and business expectations remain optimistic. Leading indicators (table 1) show that domestic demand continues to be solid, pointing to a strong first quarter (1Q26). On the side of private investment, cement demand and heavy vehicle sales continue to grow at double-digit rates, while electricity demand and business loans are also accelerating (the latter with data up to February). Regarding private consumption, mutual funds and vehicle sales maintained double-digit growth, and personal loans is expected to expand in March at levels close to 8%. Finally, tax revenues (from both companies and individuals) returned to double-digit growth.

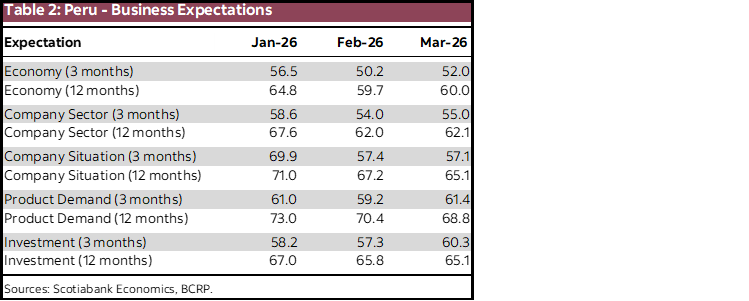

As for business expectations, on March 10th the Central Reserve Bank (BCRP) published the results of its Macroeconomic Expectations Survey, reaffirming economic agents’ perception of a solid economy. After a slight deterioration in February, short-term (three months) and medium-term (12 months) expectations recovered in March, with both indicators remaining in the optimistic range (above 50 points). Results for other indicators—such as sectoral expectations, company outlook, product demand, and investment demand—were mixed but still notably in the optimistic zone. The outcome of the presidential elections held on April 12th will influence business expectations depending on whether the two candidates advancing to the runoff support the current economic model or propose changes (table 2).

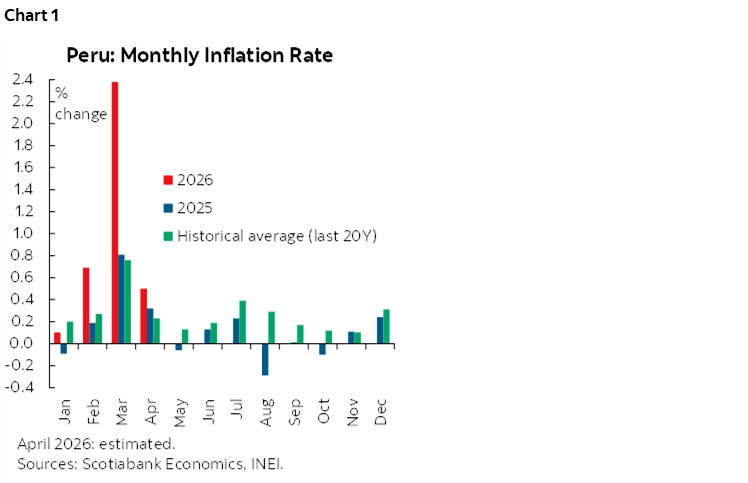

Regarding April inflation, to be published on May 1st, our preliminary estimates suggest it will remain above the historical average of the past 20 years (0.2%, chart 1). Oil-related energy prices remain elevated, and food prices continue to face upward pressures due to weather-related factors. Agricultural products such as tubers and fruits are registering increases; however, chicken prices—significant within the basic household basket—have begun to ease after rising since late 2025. Consequently, we preliminarily estimate April’s monthly inflation at around 0.5%, pushing annual inflation from 3.8% in March to nearly 4.0% in April. It is worth noting that prior to the Middle East conflict, year-end inflation was projected at 2.2%, slightly above the midpoint of the target range (2.0%). However, we now believe that while inflation will decelerate from current levels, it will remain slightly above the upper bound of the target range (3.0%).

Finally, 12-month inflation expectations rose from 2.1% to 2.5%, levels not seen in nearly two years (since June 2024). With the BCRP keeping its policy rate unchanged, the real interest rate (the difference between the policy rate and inflation expectations) fell from 2.1% to 1.7%, below the estimated neutral threshold (2.0%). This scenario has not been observed in approximately four years (since August 2022). If pressures on 12-month inflation expectations persist, the real rate would move further away from the neutral threshold, opening the possibility of new policy rate hikes. Considering that the rise in inflation is due to temporary shocks, we do not foresee rate increases in the short term, and our baseline scenario remains that the policy rate will hold at 4.25% toward year-end.

| LOCAL MARKET COVERAGE | ||

| CHILE | ||

| Website: | Click here to be redirected | |

| Subscribe: | anibal.alarcon@scotiabank.cl | |

| Coverage: | Spanish and English | |

| MEXICO | ||

| Website: | Click here to be redirected | |

| Subscribe: | estudeco@scotiacb.com.mx | |

| Coverage: | Spanish | |

| PERU | ||

| Website: | Click here to be redirected | |

| Subscribe: | siee@scotiabank.com.pe | |

| Coverage: | Spanish | |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.