HIGHLIGHTS

- Key monetary policy decisions await from across the globe next week, but there may be little that officials can do or signal in the face of the conflict in the Middle East, with its conclusion being anyone’s guess, while Brent and WTI oil prices track about a 70% rise year-to-date.

- Next week, we have rate decisions from the BCB, Fed, BoC, ECB, BoE, BoJ, RBA, SNB, Riksbank and a handful of other global central banks. Across those mentioned, only the BCB is expected to roll out a rate cut, its first in the cycle, while one of them, the RBA, is expected to hike.

- In today’s note, our economists look at what the recent global energy shock could mean for Mexican inflation, with the government likely to keep pass-through in check. Mexican markets are closed on Monday.

- The team in Peru discusses the possible impacts of the local energy crisis and the Middle East conflict, which according to their estimates would lift annual inflation to 2.5–2.6% in March, up from 2.2% last month.

- Chilean 4Q GDP, and Brazilian, Chilean, and Colombian January economic activity are next week’s main Latam data releases, while China publishes retail sales and investment data on Monday, with Canadian CPI out that same day. U.S. PPI on Wednesday will be no challenge to the Fed’s meeting in the afternoon, nor will Thursday’s U.K. jobs report for the BoE’s announcement a few hours later.

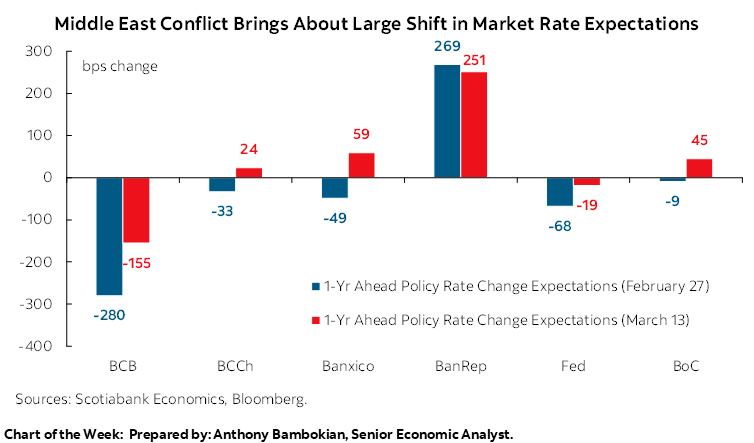

Chart of the Week

GLOBAL RATE DECISIONS, LATAM ECONOMIC ACTIVITY

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Key monetary policy decisions await from across the globe next week, but there may be little that officials can do or signal in the face of the conflict in the Middle East, with its conclusion being anyone’s guess, while Brent and WTI oil prices track about a 70% rise year-to-date.

- Next week, we have rate decisions from the BCB, Fed, BoC, ECB, BoE, BoJ, RBA, SNB, Riksbank and a handful of other global central banks. Across those mentioned, only the BCB is expected to roll out a rate cut, its first in the cycle, while one of them, the RBA, is expected to hike.

- In today’s note, our economists look at what the recent global energy shock could mean for Mexican inflation, with the government likely to keep pass-through in check. Mexican markets are closed on Monday.

- The team in Peru discusses the possible impacts of the local energy crisis and the Middle East conflict, which according to their estimates would lift annual inflation to 2.5–2.6% in March, up from 2.2% last month.

- Chilean 4Q GDP, and Brazilian, Chilean, and Colombian January economic activity are next week’s main Latam data releases, while China publishes retail sales and investment data on Monday, with Canadian CPI out that same day. U.S. PPI on Wednesday will be no challenge to the Fed’s meeting in the afternoon, nor will Thursday’s U.K. jobs report for the BoE’s announcement a few hours later.

Key monetary policy decisions await from across the globe next week, but there may be little that officials can do or signal in the face of the conflict in the Middle East. The ~70% jump in crude oil prices in the year-to-date, and no clarity on whether this rise may be short-lived or possibly extend, favours a cautious stance by policymakers. It is in the length of the conflict—and how long an eventual return to ‘normality’ would take—where the impact on inflation, and thus on policy goals, lies.

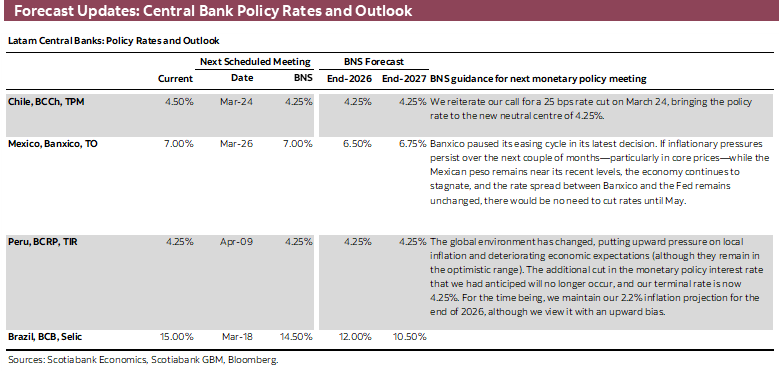

A short-lived conflict would mean the likes of the Fed, BoE, and Banxico could resume their easing cycles soon, while others like the BoC and the ECB can more comfortably keep rates on hold. A longer period of sizeable disruptions to transit through the straight of Hormuz (about a fifth of global oil and gas) could mean indefinite rate holds for some and possible rate hikes for others. For some, most notably the BCB, the policy path remains one of easing although the magnitude of cumulative cuts may be significantly reduced.

Next week, we have rate decisions from the BCB, Fed, BoC, ECB, BoE, BoJ, RBA, SNB, Riksbank and a handful of others global central banks. Across those mentioned, only the BCB is expected to roll out a rate cut, its first in the cycle (more later), while one of them, the RBA, is even expected to increase its cash rate by 25bps. We are a long way from the market pricing in a couple of weeks ago an 80–90% chance of a BoE on the 19th, shifting all the way to seeing about an 80% of a 25bps hike by year-end.

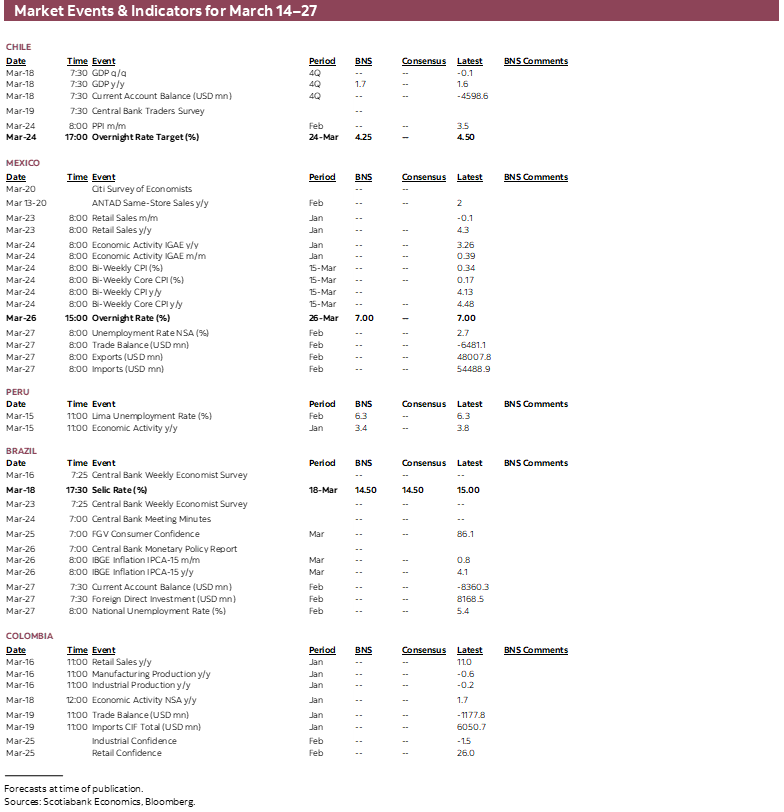

On the ex-Latam data front, Chinese retail trade, investment, and industrial production figures kick off the week alongside Canadian CPI, with U.S. PPI on Wednesday, and U.K. employment on Thursday. Colombia releases retail sales, and industrial output data on Monday, followed by economic activity on Wednesday, all for January, with the latter expected around 2% y/y, accelerating from the 1.7% rise in December. Local markets will keep a closer eye on international developments as well as the outlook for the late-May first round presidential vote, with the left’s Cepeda leading first-round polls but lagging in hypothetical head-to-head contests in a would-be second round.

Banxico will be among the last of the majors to announce a policy decision in the current cycle, on the 27th, with traders leaning towards no rate cut this month with odds at a 20% chance of a 25bps reduction compared to an 80% implied probability in late-February. Traders have also gone as far as expecting about two hikes (on net) a year from now, flipping from two cuts expected over the same period just a few weeks ago. Mexico’s calendar is quiet next week—with holidays on Monday, to boot—as the only relevant release will be Friday’s Citi survey of economists where we’ll see how expectations changed from last week’s poll, where the median still saw a quarter-point cut in late-March. In today’s note, our economists look at what the recent global energy shock could mean for Mexican inflation, with the government likely to keep pass-through in check.

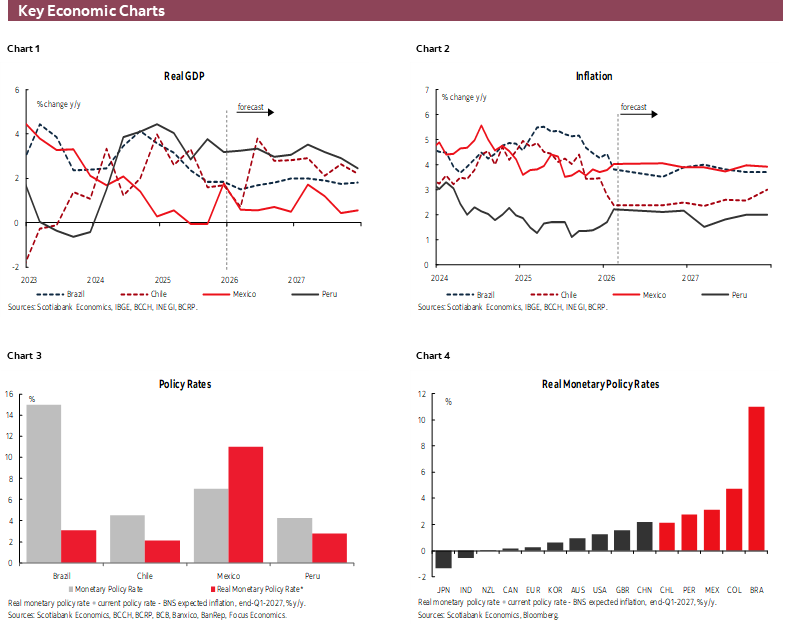

The BCB will certainly have to reassess its policy path over the next few quarters were the conflict to have longer lasting impacts on inflation. However, with Brazil’s Selic rate currently at 15% (against headline inflation at 3.8%), the BCB’s deliberations will likely centre not on whether to hold steady (and far from hiking) but on how long they will go once cuts start. Even a 50bps cut next week would keep policy highly restrictive—and even if we see inflationary pressures from global energy prices. Economists polled by Bloomberg have turned a bit more indecisive about next week’s announcement with an even split across those expecting a 25bps cut and those eyeing a 50bps move.

While our latest official forecast is that the BCB will begin the easing cycle with a half-point reduction, recent price action in global markets tees up the smaller-sized cut. Were crude oil prices to continue their ascent in the coming days, the BCB will probably opt for caution. Markets are pricing in only 20bps for next week, thus suggesting that officials led by Galipolo could even choose to delay the rate cutting cycle until the energy horizon clears up. We’ve seen a large move in Brazilian short-term yields in recent months, as traders now currently see about 150bps in total BCB easing by end-2026 compared to ~250bps by end-2026 at the close of last year. On Monday, Brazilian economic activity data for January is expected to show a material slowdown from 3% in December to ~1% at the start of the year with very soft services activity offset by a firmer performance in the industrial sector. As far as economic figures go, the BCB would be justified in announcing large rate cuts, but times are tricky.

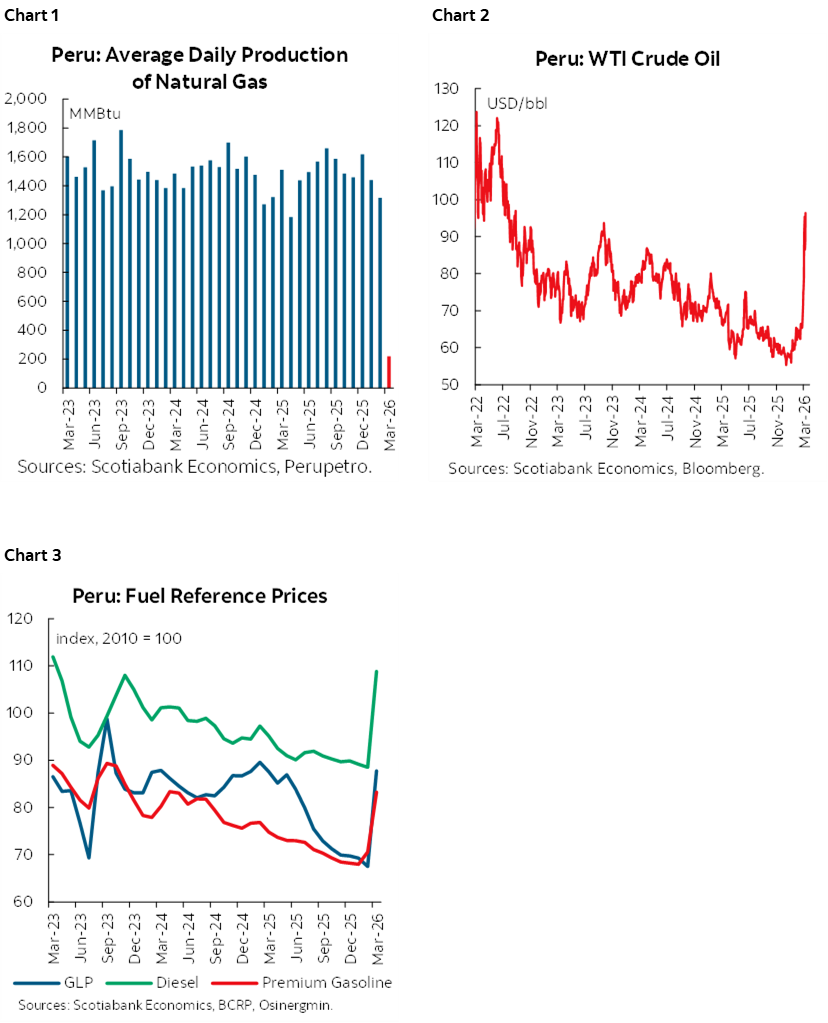

On Sunday, Peru releases January GDP and February unemployment rate data. The country’s economy likely held to a strong pace at the start of the year based on a series of activity indicators for the month that point to an expansion in the high-3s (close to December’s 3.8% rise). Robust household spending supported by low inflation and solid labour markets (and pension withdrawals, more recently) has combined for several months with strong investment spending (mining and infrastructure) that should remain important growth tailwinds. Yet, energy supply issues in recent weeks (now mostly resolved) due to a key gas pipeline leak and its suspension dented Peru’s upward momentum, and a rebound in inflation (mainly due to poultry prices) and now the risk of higher international energy prices could also act as a drag on domestic demand. In today’s Weekly, the team discusses the possible impacts of the local energy crisis and the Middle East conflict, which according to their estimates would lift annual inflation to 2.5–2.6% in March, up from 2.2% last month.

INE releases Chilean 4Q GDP data on Wednesday, but with monthly IMACEC data showing that the country expanded by 1.6% y/y in the quarter it will be the expenditure details of the release that will grab our attention. In the first three quarters of 2025, Chilean household spending averaged a strong 2.7% y/y pace, while investment averaged 5.8% y/y for its best ex-pandemic pace since 2018. Considering a deceleration in services activity for the quarter according to monthly GDP data (and roughly steady wholesale/retail trade), it’s likely that we see a slowdown in household spending in the quarterly figures. Meanwhile, investment may have also slowed a touch based on a deceleration in capital goods imports in 4Q—which nevertheless remained very strong at 20% y/y. On Thursday, the BCCh publishes the results to its traders survey which, based on market pricing, will likely show that market participants expect no more rate cuts from Chile’s central bank over the next 18 months or so—after which point traders are eyeing a small tightening cycle.

Mexico—The Global Inflation Shock After the War in Ukraine and Its Impact on Mexico

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

Russia’s invasion of Ukraine in early 2022 triggered one of the sharpest global increases in energy and food prices in decades, and Mexico—an open economy highly exposed to imported shocks—felt the impact almost immediately. Annual inflation, which stood at 7.07% in January 2022, accelerated as rising international prices of oil, natural gas, grains, and fertilizers filtered into the domestic economy. Inflation peaked at 8.70% in September 2022, the highest level in twenty years. The transmission channels were clear: higher fuel and transportation costs, more expensive imported basic grains, and rising agricultural input prices.

Mexico’s energy inflation reflected the global turmoil but also exhibited a distinctive feature: direct government intervention. To shield consumers from soaring fuel prices, the Ministry of Finance deployed substantial gasoline subsidies. By May 2022, these subsidies had reached an estimated 2.39 billion dollars—more than double the additional revenues generated by higher oil prices. As a result, energy inflation peaked at a relatively moderate 8.14% in August 2022 and even turned negative in 2023. Although the subsidies imposed a significant fiscal cost and added pressure on Pemex, they helped maintain budget stability and prevented a more pronounced inflationary pass-through.

As global markets gradually stabilized, inflation in Mexico began to ease. By December 2023, headline inflation had declined to 4.66%, nearly three percentage points below its peak. However, the episode highlighted Mexico’s vulnerability to geopolitical disruptions, given its dependence on imported strategic inputs such as energy, grains, and fertilizers.

Today, with conflict in the Middle East, Mexico once again faces upward-tilted inflation risks. In February (prior to the start of the conflict), headline inflation rose to 4.02%, up from 3.79% the previous month and above market expectations. Core inflation remained elevated at 4.50%, driven by increases in goods prices. Meanwhile, non-core inflation—more sensitive to swings in energy and agricultural commodity prices—climbed to 2.44%.

In this context, a potential reactivation of the IEPS-based gasoline subsidy could temporarily soften pressures on the energy component. However, its effectiveness would depend on the duration and magnitude of disruptions in international energy markets. Additional pressures could also emerge in other commodities and agricultural products in the short term. Private-sector analysts have already revised their year-end inflation expectations upward, now projecting 4.00% for headline inflation and 4.17% for core inflation. Supply-chain disruptions related to the Middle East conflict could prompt further upward adjustments.

For monetary policy, the market remains split on whether Banco de México will deliver its next rate cut in March or May. However, the intensity of the conflict abroad and Mexico’s early-March inflation reading will be crucial for Banxico’s decision this month, as well as for analysts’ expectations regarding the interest rate path for the rest of the year.

Peru—Local Energy Crisis May Be Nearing Its End

Katherine Salazar, Senior Analyst

katherine.salazar@scotiabank.com.pe

- Repair work on the Camisea gas pipeline shows 74% progress

- Government takes emergency measures to ration natural gas

- Incident on the pipeline, and the rise in oil, affected local fuel prices

On Sunday, March 1st, a gas leak with deflagration was detected at kilometre 43 (Megantoni, Cusco) on the gas pipeline operated by Transportadora de Gas del Perú (TGP). Immediate safety protocols were activated, transport of natural gas liquids was temporarily suspended, and injection of natural gas was interrupted as a preventive measure.

After the incident, the Ministry of Energy and Mines declared an emergency for the natural gas supply until March 14th with the objective of maintaining continuity of supply while repairs are carried out. Households (residential) and essential services (hospitals and commerce) are being prioritized, in addition to mass public transport that uses vehicular natural gas (VNG).

Additionally, the Government ordered telework for public employees and mandatory virtual classes for private schools in Lima and Callao between March 9th and 14th due to the energy crisis the country is going through. These measures seek to reduce traffic in the capital so that there is less fuel consumption.

The Camisea system has two pipelines. One for Natural Gas Liquids (NGL) that supplies a fractionation plant in Pisco (Ica) and produces LPG and other derivatives, and another for Natural Gas (NG) that reaches Lima and is used for the domestic market—households, industries and transport—and for export. After the deflagration, gas transport was suspended in both pipelines. The NG pipeline usually transports around 600 million cubic feet per day, so, once injection of gas in Camisea was suspended, only about 70 million cubic feet per day—stored in the pipeline—remained available, with which prioritized users are being supplied.

It should be noted that, as of Wednesday, March 11th, repair work on the Camisea gas pipeline had 74% progress, according to the Minister of Energy and Mines. Likewise, it is likely that restoration of natural gas service will occur on the scheduled date of March 14th.

Impact

The Peruvian electrical system is supplied by hydroelectric plants with a 49% share, thermal plants with around 36%, and the remaining 15% by non‑renewable energies—mainly solar and wind. The emergency declaration means that thermal generators will not have natural gas supply for 14 days, and in some cases are replacing this input with diesel. In addition, our country has a backup system called “cold reserve”, consisting of diesel‑fired thermal plants, which have an approximate autonomy of 45 days. With this backup, there should not be a problem with the electricity supply.

Regarding costs, in the case of regulated users (households and commerce) there would be no tariff increases in the short term since they have long‑term supply contracts, unlike free users—large energy consumers—who buy energy on the spot market and whose price has risen due to the higher cost of diesel compared to natural gas.

Another sector that was affected was Industry—around 1,000 companies use NG as an energy source.

Likewise, the restrictions reach vehicular natural gas (VNG) consumers, both private individuals and drivers who provide taxi services. Both groups have been temporarily using gasoline—most light vehicles are dual‑fuel—a fuel significantly more expensive than VNG—the latter is about 70% cheaper than gasoline.

Unfortunately, the local situation coincides with a phase of heightened tension in global energy markets due to the outbreak of a conflict in the Middle East between the U.S. and Israel versus Iran, which has led to the closure of the Strait of Hormuz—a strategic point through which about 20% of global oil and gas supply moves—and to a rise of around 40% in oil prices since late February—when the conflict began.

The impact of the higher prices of gasoline, diesel and LPG associated with the increase in international prices, together with the increase in the price of taxi service—due to the replacement of VNG with gasoline—will have an initial impact of around 0.35 percentage points on March inflation. Assuming the historical monthly rate for March of 0.8%, and considering the additional impact of fuels, the monthly inflation rate for March could be around 1.15%, bringing the annual rate to around 2.55% (2.2% in February). Nevertheless, we foresee a rapid reversal in the increase in taxi prices—assuming that GNV supply is restored starting mid‑March—but the impact on the price of imported fuels—gasoline, diesel, LPG—would continue, at least, until April.

Finally, the temporary suspension of NG and NGL transport from Camisea will have a significant impact on hydrocarbons production. It should be noted that both products contribute about 70% of the volume produced of hydrocarbons, with the remaining 30% coming from oil. Thus, assuming 15 days without NG and NGL production, it would generate a drop close to 35% in hydrocarbons production, ceteris paribus. Considering that hydrocarbons production represents about 2% of GDP, a 35% decline in March could subtract a little over 0.5 percentage points from March GDP, ceteris paribus.

| LOCAL MARKET COVERAGE | ||

| CHILE | ||

| Website: | Click here to be redirected | |

| Subscribe: | anibal.alarcon@scotiabank.cl | |

| Coverage: | Spanish and English | |

| MEXICO | ||

| Website: | Click here to be redirected | |

| Subscribe: | estudeco@scotiacb.com.mx | |

| Coverage: | Spanish | |

| PERU | ||

| Website: | Click here to be redirected | |

| Subscribe: | siee@scotiabank.com.pe | |

| Coverage: | Spanish | |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.