HIGHLIGHTS

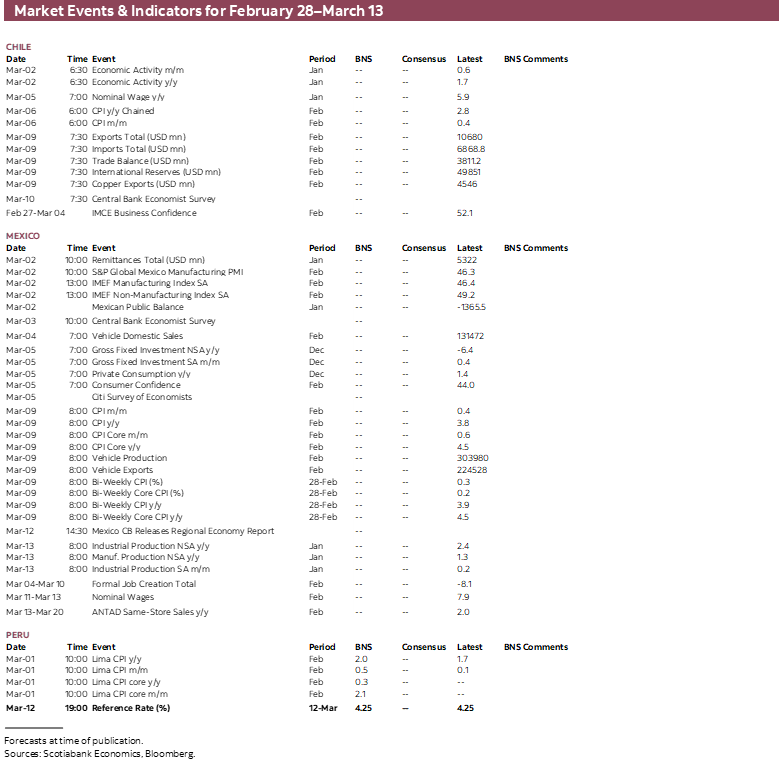

- Chilean, Peruvian, and Colombian inflation prints are the Latam data highlight over the coming week, with economic activity readings in Chile and Brazil, and Mexican investment data also on tap.

- Global markets will focus on a flood of U.S. data that include employment readings on Friday, with traders also keeping a close eye on U.S.-Iran nuclear deal talks and the AI anxiety hanging over U.S. equity markets.

- In today’s report, the team in Peru discuss their projection for local inflation to accelerate to 2% in February and also highlight the performance of January economic indicators that point to a 3% expansion to start out the year.

- Our economists in Mexico go over the latest foreign direct investment data that showed a 7.7% rise in 2025, though with a weak performance in the 4Q. Meanwhile, domestic investment data continue to underperform.

- We forecast that Chilean inflation slowed to 2.5% in February from 2.8% y/y, while economic activity likely decelerated further at the start of the year, with energy bills pulling headline inflation lower.

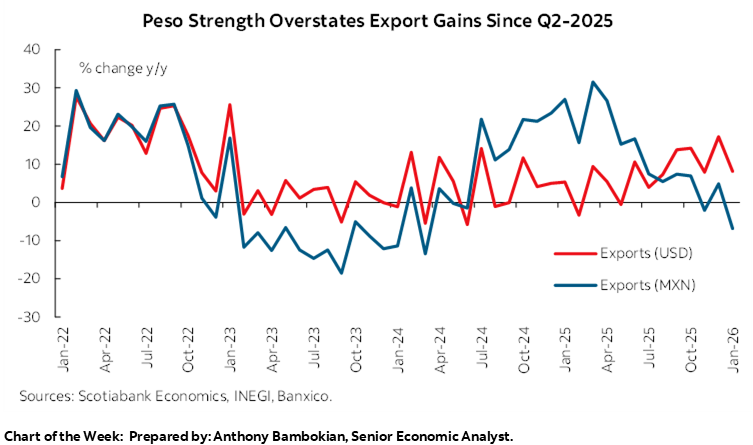

Chart of the Week

REGIONAL CPI, BRAZIL GDP, AND MEXICO INVESTMENT

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Chilean, Peruvian, and Colombian inflation prints are the Latam data highlight over the coming week, with economic activity readings in Chile and Brazil, and Mexican investment data also on tap.

- Global markets will focus on a flood of U.S. data that include employment readings on Friday, with traders also keeping a close eye on U.S.-Iran nuclear deal talks and the AI anxiety hanging over U.S. equity markets.

- In today’s report, the team in Peru discuss their projection for local inflation to accelerate to 2% in February and also highlight the performance of January economic indicators that point to a 3% expansion to start out the year.

- Our economists in Mexico go over the latest foreign direct investment data that showed a 7.7% rise in 2025, though with a weak performance in the 4Q. Meanwhile, domestic investment data continue to underperform.

- We forecast that Chilean inflation slowed to 2.5% in February from 2.8% y/y, while economic activity likely decelerated further at the start of the year, with energy bills pulling headline inflation lower.

Chilean, Peruvian, and Colombian inflation prints are the Latam data highlight over the coming week, with economic activity readings in Chile and Brazil, and Mexican investment data rounding out the data calendar in the region. The U.S. calendar is packed with key data, including ISM services and manufacturing, ADP employment, and ending the week with the all-important nonfarm payrolls report. The rest of the G10 has mostly second-tier data on tap, with the exception of Eurozone CPI on Tuesday. Elsewhere, Chinese official and private PMIs are on offer.

Beyond the busy U.S. data calendar, global markets will also be shaped by U.S.-Iran nuclear negotiations, with tensions lifting Brent crude oil prices 20% higher in the year-to-date while keeping equity markets on edge. So far, it would also seem that fixed income markets are being more responsive to risk-off trading rather than inflationary risks. On that note, equities also remain on uneasy footing amid AI disturbance risks and traders possibly worrying about the sustainability of large capex plans by the hyperscalers, with these factors standing as much bigger sentiment negatives than U.S. tariffs uncertainty.

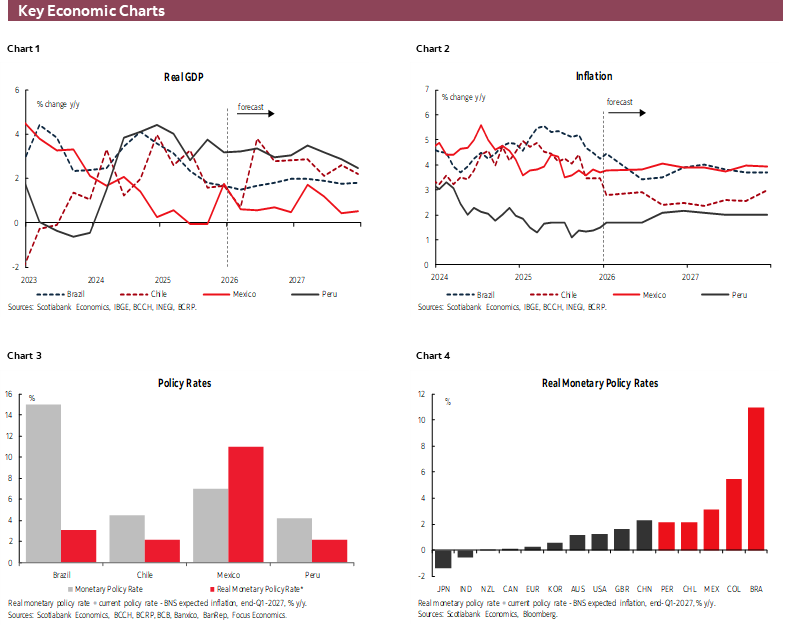

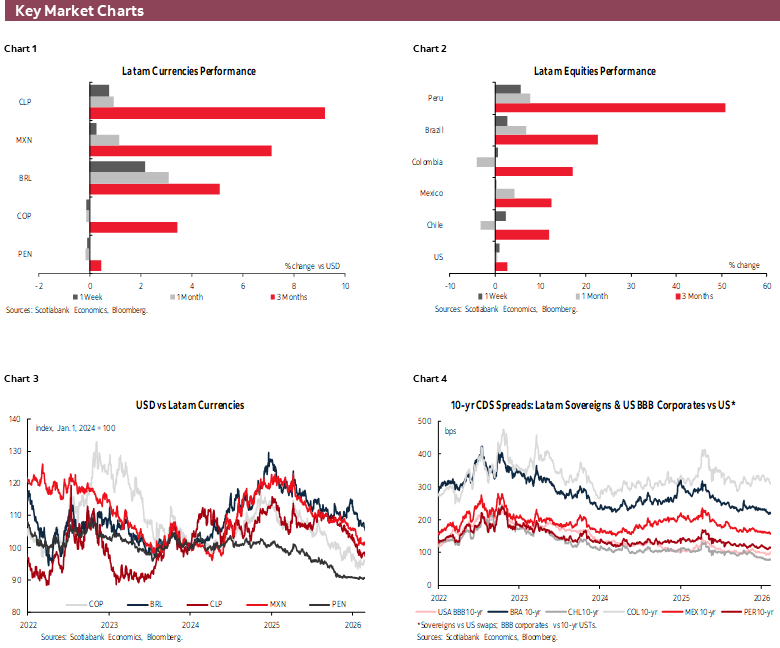

The U.S.’s tech supremacy advantage has been turned into a headwind this year, with the Nasdaq 100 down ~2–3% and the S&P 500 flat in the year-to-date, compared to 8% gains in Canada’s TSX, or ~11% and 18% rallies, respectively, in Mexico’s IPC and Brazil’s Ibovespa (all in local currency terms). In line with equity underperformance, and rates traders still expecting 2–3 Fed cuts this year (where next week’s NFP print will be key), the USD has weakened against all major currencies in 2026, from the BRL’s and MXN’s 9% and 6% gains to the more muted 0.5% appreciation in the JPY and GBP; the CLP, COP, and PEN sit somewhere in the middle of the leaderboard with ~4%, ~3%, and ~1% moves, in that order.

Domestic uncertainty in Mexico following last weekend’s military operation in Jalisco and its aftermath, as well as President Sheinbaum unveiling an electoral reform proposal were modest negatives for the Mexican peso, which is ending the week among the few currencies that lost ground against the USD since last Friday. However, its 0.4% loss falls short of the 0.6% decline in the JPY and 1% losses in the COP and CLP, reflecting some confidence in markets that recent events will have limited long-lasting impact on Mexican assets. The IPC is also roughly unchanged on the week, making it among the better performing Latam equity indices over the period, and its price action was more closely tied to the global equities mood. Whether the market’s muted read of these developments is correct remains to be seen.

Mexican financial market resilience aside, domestic investment trends suggest that local firms remain highly cautious. Past (e.g. judicial) and upcoming reforms as well as crime-related insecurity and issues in utilities supply (electricity and water) continue to weigh on sentiment—and developments in recent days likely reinforced their caution. Next Thursday, INEGI publishes fixed investment figures for December, coming off a 6.4% y/y contraction in November, to round out data for calendar 2025 which was tracking a 7.3% year-to-November decline. Across the main categories, machinery and investment neared a 10% ytd drop and public investment tracked a 30% drop, with a 1.4% ytd rise in private construction the only small positive thanks to greater residential building.

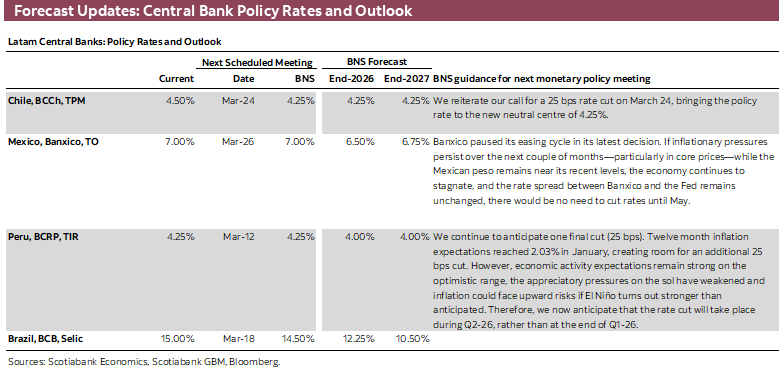

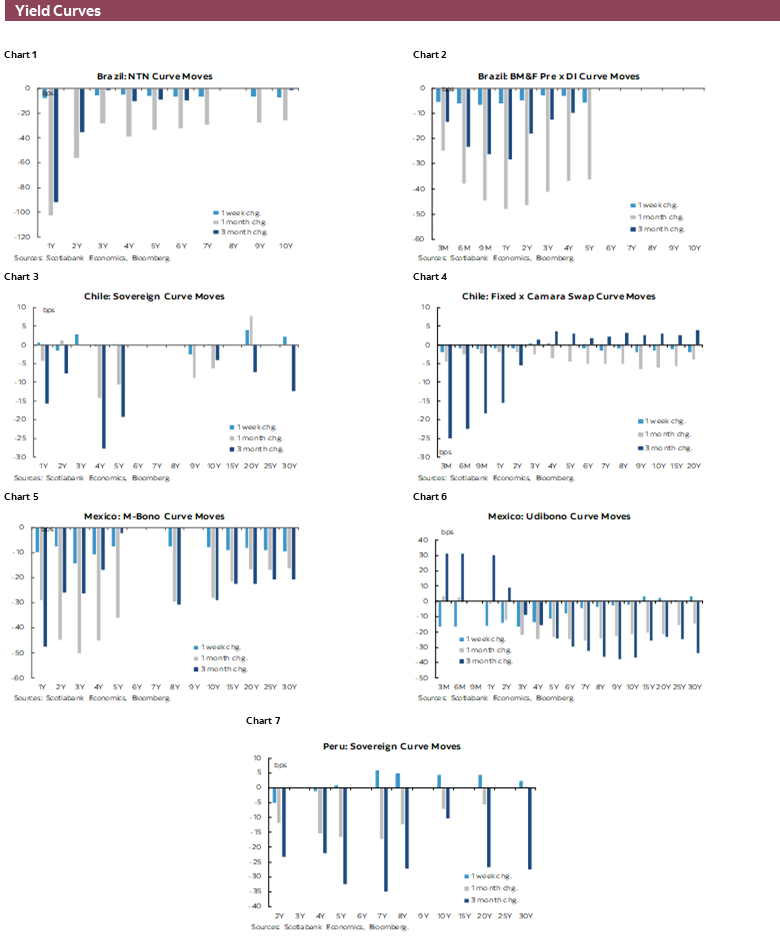

The soft economic backdrop at home and mostly as-expected inflation data earlier this week (see here) as well as dovish comments from Banxico Governor Rodriguez and board member Borja in recent days point to higher odds of the central bank rolling out a 25bps rate cut to 6.75% at its late-March decision (we believe they will wait until May). We’ll see what the median view of economists is in the results to the Citi survey out on Thursday. Meanwhile, markets are pricing in an 80% chance of a rate cut next month, with another quarter-point reduction priced in for one of the June or August decisions to a 6.50% terminal rate (in line with our forecast for end-2026).

Chile’s week is bookended by January economic activity on Monday and February CPI on Friday. This morning, the country released sectoral activity figures for the month that were generally disappointing, with retail sales slowing to 3.7% from 4.4% y/y, while industrial production contracted by 1.6% after a 1.8% y/y drop, where manufacturing output slid close to 4% after a muted 0.3% rise in December. The unemployment rate also rose more than expected at the start of the year (see here). Based on sectoral data for January, it is then possible that Chile posts a sub-1% rise in economic activity which marks a worrying trend after small increases of 1.7% and 1.2% y/y in December and November, respectively.

On the inflation front, the team estimates that prices growth slowed to 2.5% in February, from 2.8%, on the back of a 0.1% monthly rise driven by gains in services prices against downward pressure from volatile items (energy and food) and a minor rise in goods prices. The headline reading will be weighed by the implementation of new power bills prices that leaked into February instead of being captured in January data. If realised, next week’s inflation level, coupled with recent weakness in labour market and economic indicators support a 25bps rate cut by the BCCh at the March 24th announcement (~80% priced in by markets).

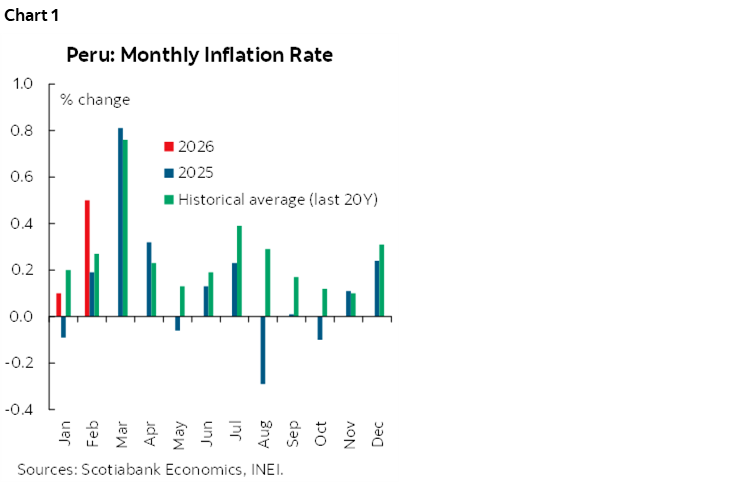

Turning to Peru, the local stats agency releases February CPI data on Sunday, with our economists eyeing 2% headline and 2.1% core inflation readings, up from 1.7% and 2%, respectively. Although these would represent their highest prints since late-2024/early-2025, it only marks a normalization of the disinflationary process to sit closer to the 2% BCRP goal after headline inflation reached a low of 1.1% in August 2025. As the team highlights in today’s report, they anticipate a higher than seasonally normal rise in prices in February due to large increases in chicken and egg prices with high temperatures impacting farms. In today’s note, they also discuss economic indicators for January that point to a solid 3% y/y rise in GDP for the month, with renewed strength in domestic demand.

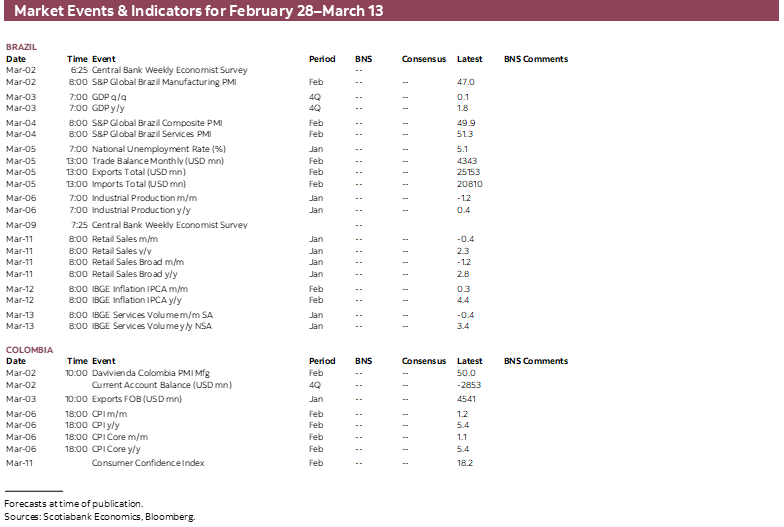

GDP data for 4Q is the highlight in Brazil, with growth seen in the high 1s, little changed from the 1.8% y/y registered in 3Q25 on the back of a 0.1–0.2% q/q expansion. This would take full year growth to around 2.2–2.3%, slowing considerably from 3.4% in 2024 on the weight of highly restrictive BCB policy rates, with government stimulus and subsidies now accounting for a key engine of domestic growth—and remaining this way for the remainder of the year.

Rate cut bets got a wake up call this morning, with IPCA-15 inflation coming in at 4.1% y/y versus the 3.8% median, further complicating expectations for the size of the first BCB rate cut at its March 19th decision. Markets are still betting on a 50bps cut, but there may be some anxiety that builds in the coming weeks that officials could begin easing with a 25bps move (more so if economic data surprise higher). Against rate cuts anxiety, markets and businesses may be back to feeling a bit optimistic about the October elections, with Flavio Bolsonaro neck-and-neck with Lula in a would-be second round vote according to a poll carried out by AtlasIntel published on Wednesday.

COUNTRY UPDATES

Mexico—Positive FDI, Weakening Fixed Investment: A Mixed Outlook for the Mexican Economy

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

During the week, Banco de México published Foreign Direct Investment (FDI) data for the fourth quarter of 2025 as part of the balance of payments release. FDI totaled USD 40.9bn in 2025, equivalent to a 7.7% annual increase. Within the components, new investments rose to USD 7.4bn (vs. USD 4.1 bn in the previous year), and intercompany accounts increased to USD 5.8 bn (vs. USD 5.1 bn). This contrasted with a decline in reinvested earnings to USD 27.7 bn (vs. USD 28.7 bn), which nevertheless represented 67.7% of total FDI. However, focusing solely on fourth‑quarter figures, FDI showed a disinvestment of USD 5 bn due to outflows of USD 4.1 bn in reinvested earnings and USD 1.1 bn in intercompany accounts, partially offset by only USD 138 million in new investments.

In this context, although the annual figures were interpreted as positive for the investment landscape, the drop in reinvested earnings—and the fourth‑quarter disinvestment in particular—raises concerns regarding the sentiment of foreign firms operating in Mexico. It is also important to recall that FDI figures are subject to continuous revisions, meaning that the data for the same period could be adjusted in upcoming quarters.

Beyond the FDI numbers, it is worth noting that domestic investment indicators remain markedly weak. Gross Fixed Investment (GFI) recorded fifteen consecutive months of declines through November, with new data to be released this week; we do not expect a substantial change, and the trend is likely to remain negative. This persistent weakness across components—machinery and equipment, as well as construction—reflects the effects of political and regulatory uncertainty and the slowdown in public spending, which have constrained the start of new projects. This prolonged contraction contrasts with the annual increase in FDI, suggesting that despite relatively stable foreign inflows, domestic productive investment continues to face structural obstacles that limit its recovery.

In parallel, business confidence has shown a steady deterioration—remaining below the 50‑point threshold throughout 2025—which may have contributed to the fourth‑quarter disinvestment within FDI, particularly in reinvested earnings. Additionally, the narrowing interest‑rate differential between Mexico and the United States has reduced the incentive for firms to retain liquidity or financial surpluses in Mexico, making the repatriation of earnings to the U.S. more attractive. The combination of a more uncertain environment, reduced appetite for expanding operations, and a relatively less favourable financial return supports the view that companies adopted a more defensive stance at year‑end. Finally, the decline in the number of registered employers with the IMSS—falling since mid‑2024—confirms a slowdown in business creation, adding further pressure to the investment outlook.

Taken together, both foreign and domestic investment indicators, along with confidence and labour‑market metrics, signal growing caution among investors amid an increasingly uncertain environment and a lack of clear recovery signals. Even so, a positive development is that Mexico’s share of global FDI flows to emerging markets appears to have increased slightly in 2025, suggesting that despite domestic challenges, the country maintained some relative attractiveness compared with other developing economies.

Looking ahead, investment risks are likely to remain tilted to the downside this year. Externally, the outlook will continue to be shaped by uncertainty surrounding trade negotiations with the United States and Canada, as well as the impact of new global tariff measures. Domestically, proposed reforms and the challenges associated with their implementation could continue to weigh on firms’ willingness to commit capital to new projects.

Peru—Mixed Signals: Higher Inflation in February, Yet Domestic Demand Shows a Solid Start in 2026

Ricardo Avila, Senior Analyst

ricardo.avila@scotiabank.com.pe

February’s inflation rate will be released on March 1st. We expect monthly inflation to exceed both the figure recorded in the same month of 2025 (0.19%) and the 20‑year historical average for February (0.27%) (chart 1). February’s inflation would come in at around 0.5%, which would push the annual rate up from 1.7% to 2.0%—the midpoint of the Central Bank’s target range.

This anticipated increase in inflation is not yet attributable to the impact of El Niño. Instead, it is driven by two specific products with significant weight in the consumer basket: chicken meat and hen eggs. Chicken prices appear to have risen by approximately 8%, while egg prices may have increased by around 20%. These price pressures have been evident since the final weeks of 2025 and are mainly explained by high temperatures affecting poultry production.

According to ENFEN, there is a heightened probability that a weak El Niño will be present in March. Such an event would not be expected to generate significant macroeconomic impacts. However, if El Niño were to reach moderate intensity, sector‑level effects would likely emerge—particularly in agriculture and fisheries—potentially leading to further price increases in products from these sectors. It is also worth noting that March is seasonally high for education‑related prices due to the start of the school year.

Previously, we expected the final policy rate cut to occur at the end of the first quarter of 2026. We now revise our outlook and believe the cut is more likely to take place during the second quarter. Twelve‑month inflation expectations reached 2.03% in January—right at the midpoint of the inflation target (2.0%). As a result, the real policy rate increased to 2.22% (22bps above the neutral rate), creating room for an additional 25 bp cut. However, we highlight three considerations:

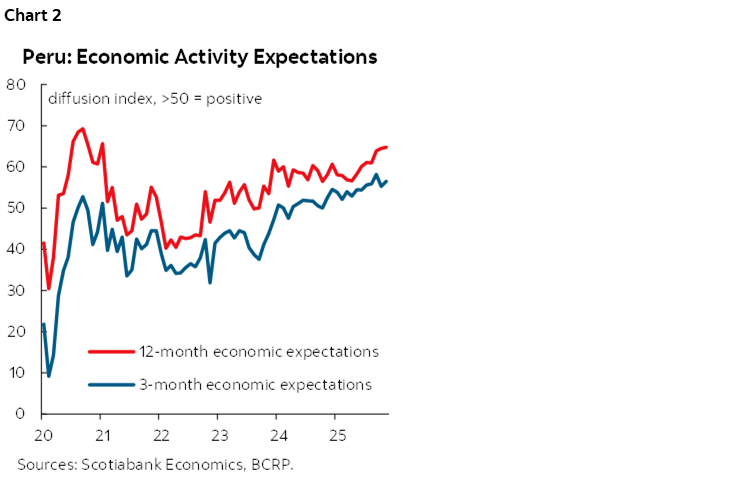

- Economic activity expectations remain strong on the optimistic range, continuing their uptrend for 12‑month horizons (chart 2).

- Appreciatory pressures on the sol have weakened.

- Inflation could face upward risks if El Niño turns out stronger than anticipated.

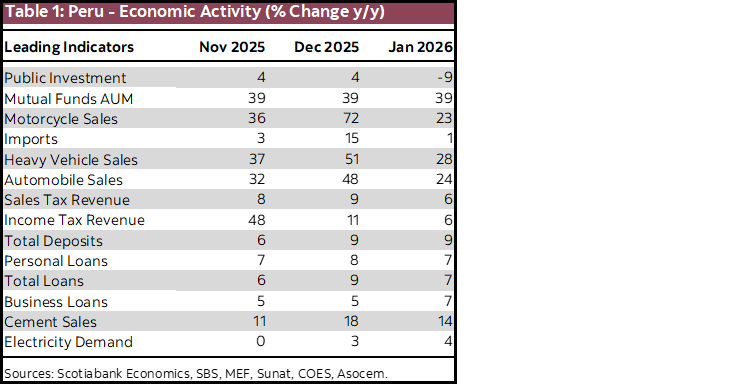

On the economic activity side, we updated our leading indicators (table 1), related to domestic demand. Overall, the environment remains favourable, suggesting a solid start to 2026. In terms of private investment, cement sales and heavy‑vehicle sales continue to grow at double‑digit rates, while electricity demand and business lending also show accelerating trends. Regarding private consumption, mutual fund holdings and vehicle sales are likewise expanding at double digits, and both tax revenues and personal loans continue to rise, albeit at a slower pace.

Taken together, these factors support our view that GDP dynamics will resemble those observed in the fourth quarter of 2025. We estimate that January’s economic growth reached approximately 3.0% and the domestic demand would gain renewed momentum.

| LOCAL MARKET COVERAGE | ||

| CHILE | ||

| Website: | Click here to be redirected | |

| Subscribe: | anibal.alarcon@scotiabank.cl | |

| Coverage: | Spanish and English | |

| MEXICO | ||

| Website: | Click here to be redirected | |

| Subscribe: | estudeco@scotiacb.com.mx | |

| Coverage: | Spanish | |

| PERU | ||

| Website: | Click here to be redirected | |

| Subscribe: | siee@scotiabank.com.pe | |

| Coverage: | Spanish | |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.