HIGHLIGHTS

- Friday’s U.S. Supreme Court tariffs ruling is closing the week with some trade optimism but also some uncertainty on the future of the U.S.’s tariffs, coming ahead of what should be a relatively quiet week on the global data front. A bare U.S. data calendar contrasts with CPI releases from other major economies. Wednesday’s Nvidia results and Trump’s State of the Union address round out the calendar.

- In Latam, the spotlight will be on Mexican and Brazilian mid-month CPI, with the former expected to accelerate and the latter seen decelerating on base effects in food and energy, respectively.

- Banxico publishes updated economic forecasts in its quarterly report with economists paying attention to the reasoning behind its expectations for inflation convergence in 2Q27. In today’s note, the team goes over the mixed drivers behind Mexico’s economic weakness, pinning depressed industrial activity and investment against consumer resilience.

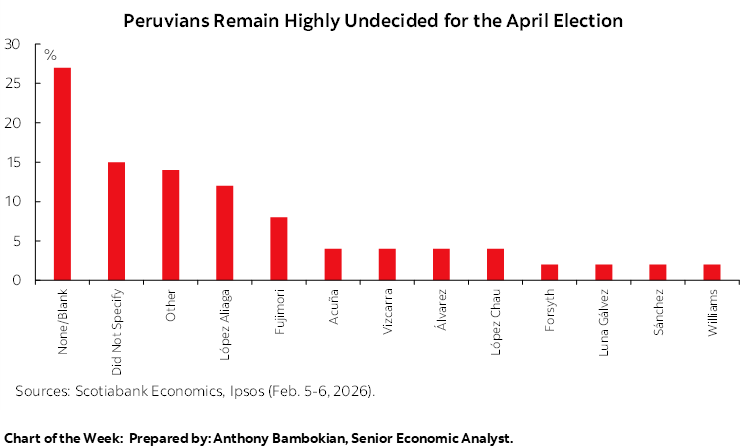

- Peru’s calendar is mostly empty with markets focused on events during the first few days of President Balcázar’s brief presidency ahead of the April election. Political noise aside, macro fundamentals are solid in the country, with our local team highlighting in today’s Weekly the strong growth of personal savings in 2025.

- Chile’s Friday macro flood will give us a good sense of how the country’s economy kicked off the year after a soft close to 2025 due to mining output disruptions.

Chart of the Week

MID-MONTH MEXICO AND BRAZIL CPI, BANXICO REPORT

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Friday’s U.S. Supreme Court tariffs ruling is closing the week with some trade optimism but also some uncertainty on the future of the U.S.’s tariffs, coming ahead of what should be a relatively quiet week on the global data front. A bare U.S. data calendar contrasts with CPI releases from other major economies. Wednesday’s Nvidia results and Trump’s State of the Union address round out the calendar.

- In Latam, the spotlight will be on Mexican and Brazilian mid-month CPI, with the former expected to accelerate and the latter seen decelerating on base effects in food and energy, respectively.

- Banxico publishes updated economic forecasts in its quarterly report with economists paying attention to the reasoning behind its expectations for inflation convergence in 2Q27. In today’s note, the team goes over the mixed drivers behind Mexico’s economic weakness, pinning depressed industrial activity and investment against consumer resilience.

- Peru’s calendar is mostly empty with markets focused on events during the first few days of President Balcázar’s brief presidency ahead of the April election. Political noise aside, macro fundamentals are solid in the country, with our local team highlighting in today’s Weekly the strong growth of personal savings in 2025.

- Chile’s Friday macro flood will give us a good sense of how the country’s economy kicked off the year after a soft close to 2025 due to mining output disruptions.

There are only a few bits and pieces in next week’s global calendar to keep markets occupied to close out the month on a relatively quiet note (at least as far as data are concerned). Friday’s U.S. Supreme Court ruling against the White House’s emergency powers tariffs has now opened the door of uncertainty to what tools the Trump administration may deploy to reimpose higher duties. The U.S. President has already announced a 10% global tariff, but he may soon launch unfair trade practices investigations (section 301) on certain countries to allow for higher duties.

Developments on the tariffs front may move global markets, as could news out of the Middle East with the U.S. building forces in the region with Iran under pressure to agree to a new nuclear deal. WTI/Brent crude oil prices have risen by 15–18% in the year-to-date in USD terms (practically equal to gold and silver gains) on risks of supply disruptions in the Persian Gulf. Were the conflict to escalate, extending the rise in energy prices, central bankers around the globe may have revisit their inflation forecasts for the coming months or take a more cautious stance to policymaking.

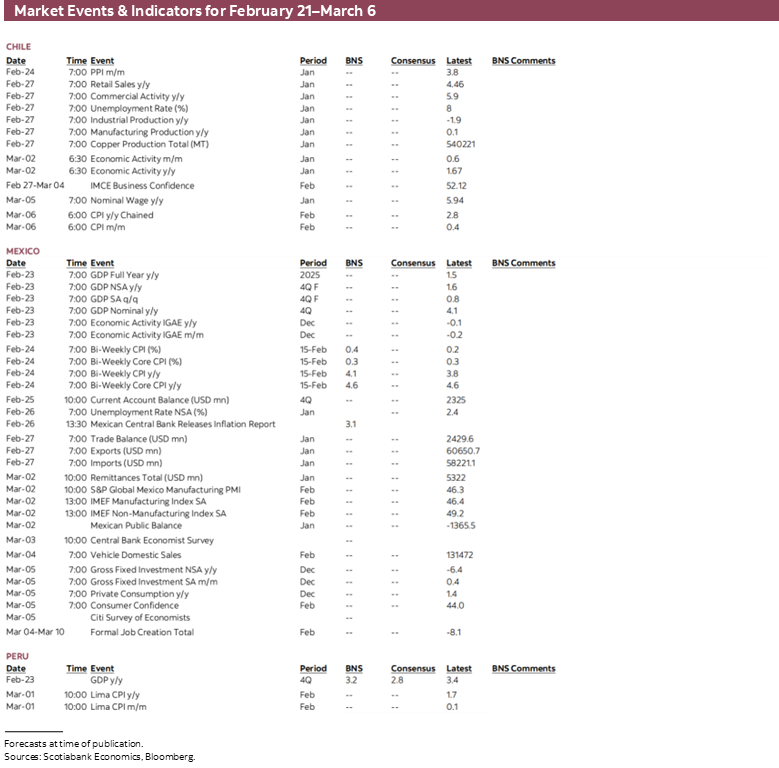

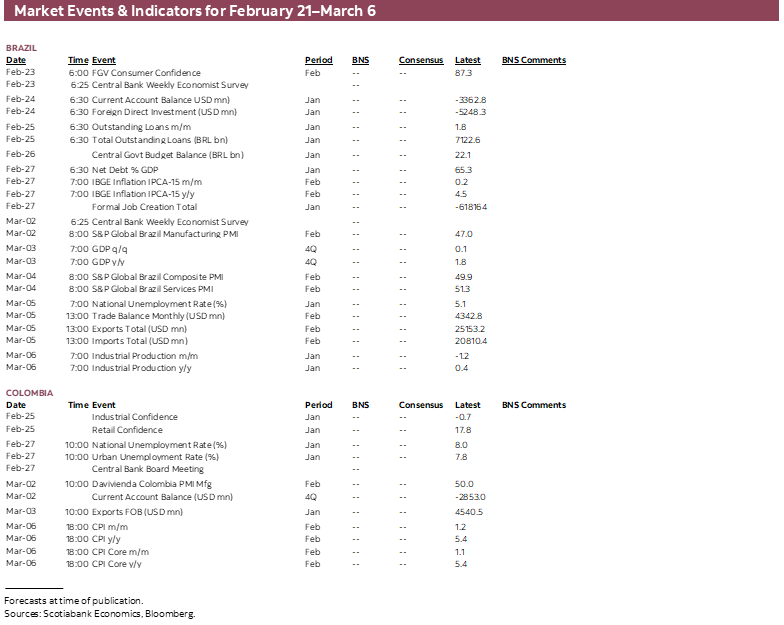

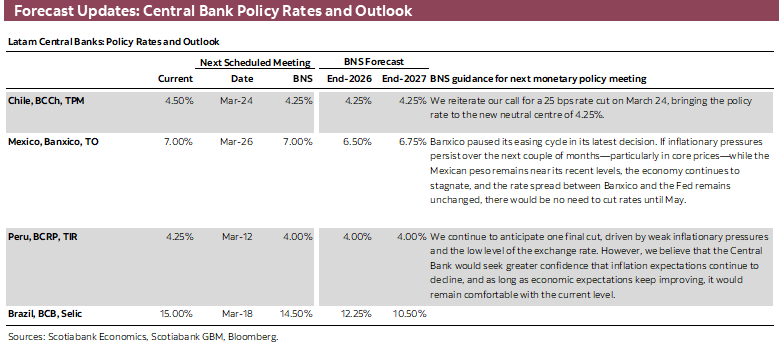

On the Latam data front, Mexico and Brazil mid-month inflation figures out on Tuesday and Friday, respectively, are the highlight, accompanied by Chile’s January macro flood at the close of the week. From Mexico, we also get the second release of 4Q GDP and December economic activity figures on Monday, and Banxico releases its quarterly report on Thursday on the heels of the latest meeting minutes (see here), with a focus on how the bank assesses the impact of soft drinks and cigarette tax hikes and tariff hikes. Colombia only offers unemployment rate data.

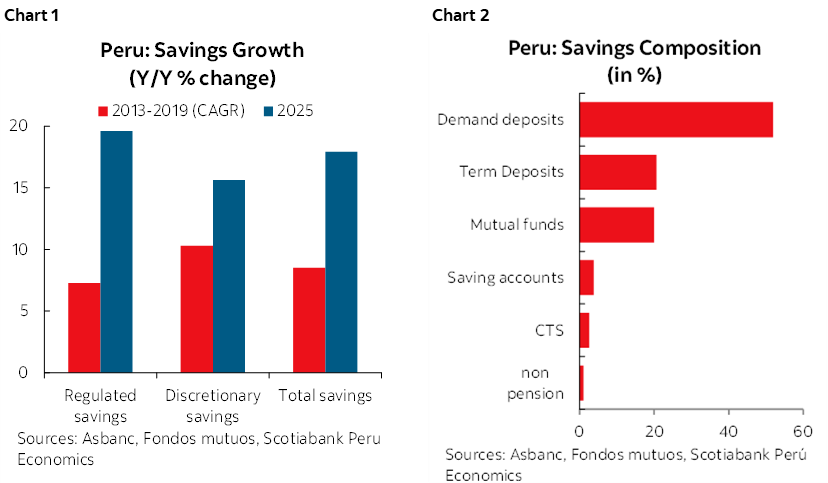

Peru’s calendar is bare outside of the INEI’s own release of 4Q GDP data, which we already know from the BCRP grew by 3.2% y/y. However, the attention will be on Balcázar’s first days as the country’s president (see here), whose first hours already saw the unexplained removal of Petroperu’s head by the state-owned oil company’s board—possibly taking advantage of the leadership void in government since President Jeri’s impeachment earlier this week. Peru continues to chug along despite political noise, while Peruvians grew their savings by the most on record last year (ex. pandemic), as covered by our local team in today’s Weekly, benefitting from solid growth and low inflation.

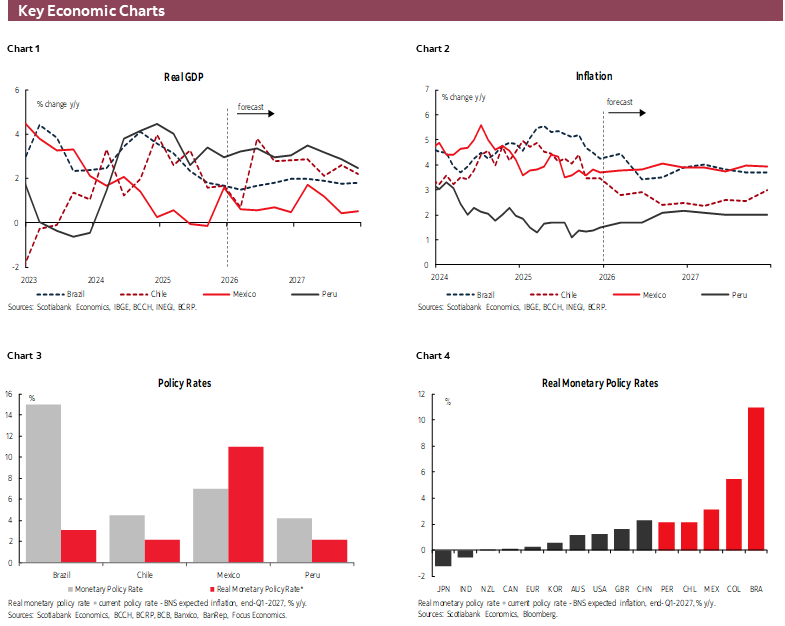

Our economists estimate that Mexican inflation accelerated to 4.1% y/y in the first half of February, from a 3.8% pace in H2-Jan, pressured by higher fresh food prices off a low base of comparison last year, while core inflation is seen holding steady at 4.6% y/y with no real impact from higher import tariffs (yet, at least) and higher drinks/tobacco taxes already having been reflected in last month’s data. There may be more interest in how inflation evolves a few months from now to gauge whether merchandise prices are impacted by tariffs and if inflation shows signs that it could converge to the 3% goal in 2Q27, as Banxico expects but economists do not. The reasons behind this optimistic view on inflation should be laid out in Thursday’s quarterly report, which will also include new projections for GDP growth. Monday’s second 4Q GDP release should offer no surprises, while our team goes over the mixed drivers behind Mexico’s economic weakness in today’s note, pinning depressed industrial activity and investment against consumer resilience resulting in a net underperformance for growth.

Brazilian inflation likely slowed down considerably in February IPCA-15 data to the high-3s from 4.5% y/y in January due to base effects mainly concentrated in energy prices (residential electricity costs climbed 16% m/m last February in mid-month print). That aside, the focus will be on underlying components of the basket for signs of additional deceleration across the various core measures that the BCB follows. Local markets have had a bit of a difficult time in pinning down the size of the BCB’s firs rate cut next month, but yesterday’s stronger than expected economic activity reading for December (growth of 3.1% vs 2.3% median) nevertheless reinforced traders’ views that officials will kick off the cycle with a 50bps move.

On Friday, Chile’s INE publishes January retail sales, unemployment rate, and industrial/manufacturing/copper production figures that will paint a fairly comprehensive picture of how Chile’s economy has kicked off the year after a muted close to 2025, with December economic activity only expanding by 1.7% due to setbacks in copper production while non-mining GDP ended with a firmer 3% y/y rise. Retail sales are expected to slow to the high-3s from a 4.5% gain in December continuing a decelerating trend since October from a very strong pace to more ‘normal’ yet still solid growth.

Outside of Latam, and aside from geopolitical and tariff developments, markets will digest only the Conference Board Survey report and PPI figures out of the U.S., with a fuller calendar in the other advanced economies that includes Australia, Tokyo, German, French, and Spanish CPI, as well as Canadian 4Q GDP data. Trump’s State of the Union address on Tuesday may be more noise than policy. In markets, Nvidia’s results on Wednesday may end up shaping the equities mood for the balance of the week, and possibly beyond with a lot (index-wise and economy-wise) riding on the AI buildout wherein Nvidia plays a central role.

COUNTRY UPDATES

Mexico—The Resilience of Consumption: The Main Driver of Aggregate Demand

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

The Mexican economy has shown sustained weakness over recent quarters. On the side of economic activity, the industrial sector has experienced a marked slowdown: since April it had been posting negative rates, and only toward December did it begin to stabilize. From the perspective of aggregate demand, investment has also been a source of fragility, accumulating fifteen consecutive months of declines with no clear signs of recovery. Added to this is a less dynamic external sector, which has limited the growth contributions coming from international trade.

In contrast, domestic consumption has continued to play a fundamental role as the main driver of aggregate demand. The strength of household spending since June of last year has allowed economic activity to maintain some dynamism, even amid a broader slowdown. In recent months, consumption indicators have shown moderate but steady growth; although some components have lost momentum—particularly the segment of domestically produced goods—household spending has remained relatively firm. This has supported the continuity of consumption even as overall economic activity has tended to weaken.

This trend is noteworthy considering that the general consumer confidence index remains below the 50-point threshold, although both the current situation and household expectations components have consistently remained above that benchmark.

This behavior is also reflected in the performance of formal commerce. In December, sales reported by INEGI showed broad-based increases across components, while in January 2026, ANTAD sales also displayed generalized gains. Altogether, ANTAD sales in January reached 136.3 billion pesos, confirming that despite a less dynamic economic environment, consumption continues to demonstrate resilience—particularly in categories linked to essential goods and related services.

While risks lie ahead, particularly those associated with financial conditions and the labour market, consumption is expected to remain a key pillar of growth in the coming months. The crucial factor will be whether those drivers that have maintained or recently shown strength can continue to hold up amid an uncertain domestic environment.

Peru—Household Savings Reached a Record High in 2025, with a Stable Outlook Ahead

Ricardo Avila, Senior Analyst

ricardo.avila@scotiabank.com.pe

Household savings add to the set of positive indicators that have performed better than expected. Savings expanded by 17.9% in 2025, accelerating from the 14.3% recorded in 2024. This performance was supported by a favourable macroeconomic environment:

- Low inflation, currently at 1.7% as of January, and which we expect to remain below the 2% midpoint of the target range through the third quarter of 2026. This boosts household purchasing power and provides greater room for savings.

- A solid labour market, with adequately employed workers increasing by 11.8% during the year and labour income rising 9.0%.

The rise in savings marks a record high, except for 2020—a non‑comparable pandemic year during which four extraordinary withdrawals from pension funds (AFPs) totaling S/ 33.7 billion were authorized, prompting households to prioritize savings while limiting consumption amid heightened uncertainty. The current situation, however, is markedly different given the stability of the macroeconomic environment.

Regulated savings—Funds deposited mandatorily as part of labour‑related compensation consist of savings accounts, demand deposit accounts, and Compensation for Time of Service (CTS) accounts. This category registered strong growth of 19.6% at the close of 2025, well above the historical average of 7.3%.

Savings deposits led this performance, growing 18.1%. They are the largest component of household savings, representing 52% of the total. This form of savings continued to grow at a double‑digit rate throughout the year, with additional momentum in the last two months due to pension fund withdrawals, which are typically deposited first in these accounts. This effect is expected to continue through the first quarter of 2026.

The balance of CTS accounts increased by 10.2% year‑on‑year. This reflects a base effect, as fewer withdrawals occurred in 2025 compared with 2024 amid expectations that full liquidity access will remain in place through the end of 2026. Nevertheless, CTS balances remain 60% below pre‑pandemic levels due to the continuous withdrawals authorized since 2020. CTS deposits currently account for only 2.6% of total deposits, compared with more than 10% before the pandemic.

Discretionary savings—Voluntary savings, consisting of term deposits, mutual funds, and non‑pension investment funds, grew 15.6% at year‑end, well above the historical average of 10.3%.

Assets under management in mutual funds for retail investors continued to support discretionary savings, recording robust growth of 40% in 2025. This type of savings has maintained strong momentum for more than two years, during which it has grown at double‑digit rates. Term deposits entered negative territory in 2025, decreasing by 0.6% due to lower interest rates. Finally, non‑pension investment funds, which represent 1.0% of total savings, closed the year with 19.0% growth and a balance of S/ 2.5 billion.

We expect household savings to grow around 10% this year, assuming current conditions persist. Growth will continue to be supported by mutual fund investments and savings accounts. Conversely, term deposits are likely to remain weak, and CTS balances are expected to decline as the period of full liquidity access expires in December.

| LOCAL MARKET COVERAGE | ||

| CHILE | ||

| Website: | Click here to be redirected | |

| Subscribe: | anibal.alarcon@scotiabank.cl | |

| Coverage: | Spanish and English | |

| MEXICO | ||

| Website: | Click here to be redirected | |

| Subscribe: | estudeco@scotiacb.com.mx | |

| Coverage: | Spanish | |

| PERU | ||

| Website: | Click here to be redirected | |

| Subscribe: | siee@scotiabank.com.pe | |

| Coverage: | Spanish | |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.