- Peru: A shift in politics … we hope not in the economy

- Mexico: Mixed signals in commerce—strong retail momentum and wholesale recovery

PERU: A SHIFT IN POLITICS … WE HOPE NOT IN THE ECONOMY

Peru’s political landscape underwent a 180-degree turn on the night of Thursday, February 19th. Following the censure of President José Jerí the previous day, Congress elected José Balcázar as the new President of Congress, thereby assuming the Presidency of the Republic on an interim basis until July 28th, 2026.

Balcázar is the eighth president in the last ten years. While the development may appear destabilizing to some external observers, it is important to note that the process has fully adhered to constitutional procedures and has unfolded in an orderly and peaceful manner.

The newly elected president comes from the left-wing political party Perú Libre, in contrast to Jerí, who was backed by a center-right political coalition. It is worth noting that Perú Libre won the 2021–2026 presidential elections; however, President Pedro Castillo was removed from office in December 2022 after a failed attempt to dissolve Congress. In other words, Perú Libre returns to power after five years, albeit for a brief five-month period leading up to July 28th.

In his initial remarks, the newly appointed president has adopted a conciliatory tone. He has pledged to ensure a transparent democratic transition, preserve economic continuity, and pursue what he described as a “genuine pacification” process, in reference to ongoing public security concerns.

The key question is whether Balcázar will govern alongside his close political allies or whether Perú Libre will exert broader influence over the administration. The party’s platform advocates for a stronger role of the state in the economy and higher public spending positions that could weigh on business expectations and potentially widen the fiscal deficit.

In the coming days, the appointment of the new Prime Minister (Head of the Cabinet) is expected. The profile of this individual will offer important signals as to whether key ministers—particularly in strategic portfolios such as economy and finance—will remain in place or whether Perú Libre will consolidate its influence within the executive.

Financial variables have so far reflected limited market disruption. At the end of the session, the local currency had depreciated by 0.2% against the U.S. dollar (from 3.35 to 3.36), while yields on Sovereign Bonds, Global Bonds, and Credit Default Swaps (CDS) showed only marginal fluctuations. It should be noted that Peru has international reserves of around US$90 billion, equivalent to 30% of GDP, one of the highest levels among emerging economies.

The return of a left-leaning administration could nonetheless affect business sentiment. Prior to this development, expectations had been trending positively despite the ongoing pre-election period, reflecting the economic momentum with which Peru entered 2026. While Balcázar’s abbreviated tenure makes sweeping structural reforms unlikely—such as convening a constituent assembly—policy measures that weaken fiscal discipline or introduce tighter regulation in specific sectors cannot be ruled out.

Moreover, significant turnover across ministries could delay the execution of public investment projects, given the learning curve faced by incoming authorities.

—Pablo Nano

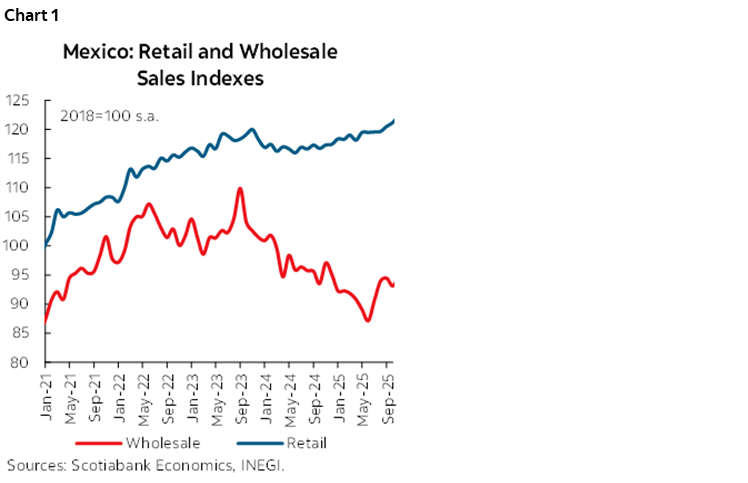

MEXICO: MIXED SIGNALS IN COMMERCE—STRONG RETAIL MOMENTUM AND WHOLESALE RECOVERY

According to INEGI’s Monthly Commercial Enterprises Survey, in December, retail sales revenues maintained their annual dynamism (chart 1), posting a 4.3% real annual increase (vs. 4.4% previously), while wholesale sales returned to positive territory at 0.6%, up from -3.7% previously. Within retail sales, the rebound in sales of household appliances and computers (17.8%) stands out, surpassing the increase in online and catalog sales (11.3%), while groceries, food, and beverages recorded a modest 0.9% rise. On the other hand, within wholesale trade, the 8.1% increase in machinery and equipment was notable, though it was offset by declines in trucks and auto parts (-10.2%) and in intermediation (-7.5%).

—Rodolfo Mitchell, Miguel Saldaña & Martha Cordova

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.