MEXICO: THE GOVERNING BOARD COULD CONTINUE ITS PAUSE UNTIL CONFIRMING THE ABSENCE OF SECOND‑ROUND EFFECTS FROM TARIFFS AND THE INCREASE IN IEPS

- The Governing Board unanimously decided to pause the rate‑cut cycle in February, emphasizing the need to assess the impact of fiscal adjustments (IEPS and tariffs), the behaviour of the exchange rate, and the degree of monetary tightening.

- In the international environment, they highlighted that global economic activity continued to moderate in 4Q25, with inflation near target levels and high uncertainty stemming from U.S. trade policy, along with increases in yield curves and a depreciation of the dollar.

- Regarding the domestic outlook, the Board noted a moderate rebound of the economy in 4Q25, although persistent weakness remains in manufacturing, historically low investment, and signs of cooling in the labour market despite resilient consumption.

- On inflation, they highlighted the uptick to 3.77% in January driven by food goods following the IEPS adjustment, while non‑core inflation remains unusually low; inflation expectations for 2026–2027 were revised upward, delaying convergence to the 3% target until mid‑2027 and maintaining an upward‑skewed risk balance.

- Although there is room for additional cuts, the Board stressed that these will depend strictly on confirming the transitory nature of fiscal shocks; even so, we maintain our expectation of a 2026 terminal rate of 6.50%, without ruling out an additional cut in March if peso appreciation and inflation stability persist.

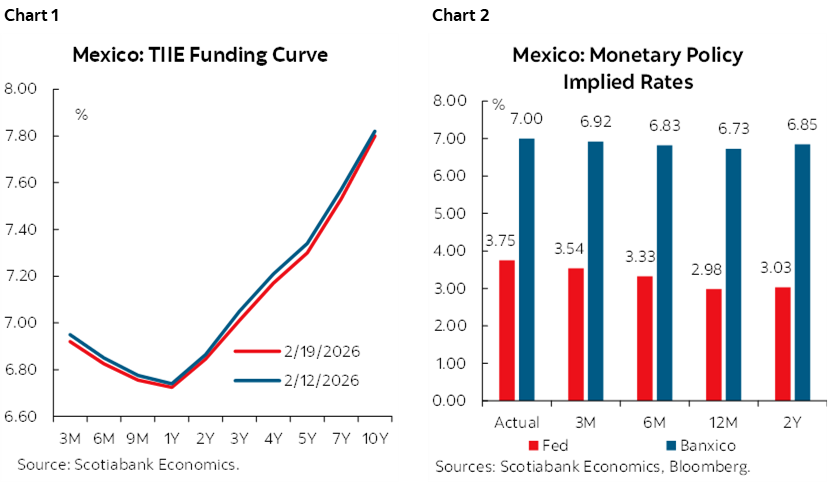

The Bank of Mexico published the minutes of the February 5th meeting, offering details on the discussion around inflation and monetary policy, with a unanimous decision to pause the rate‑cut cycle and keep the policy rate at 7.00%. This decision reflects the current inflation landscape and the need to continue assessing the impact of fiscal changes—IEPS increases and the imposition of tariffs—as well as the recent behaviour of the exchange rate, persistent economic weakness, and the degree of monetary restriction in place. Despite the unanimous vote, Deputy Governor Jonathan Heath warned that inflation may be underestimated and risks remain tilted to the upside; he sees it as premature to signal future cuts and criticizes the decision for not highlighting the deteriorating inflation dynamics and forecast errors observed last year.

Regarding the international economy, the Board noted that the pace of economic expansion continued to moderate in 4Q25, pointing to an environment of elevated uncertainty due to U.S. trade policy. Inflation has remained close to—or slightly above—central bank targets. They observed that the Federal Reserve cut its policy rate by 25 basis points for a third consecutive meeting, maintaining the expected rate path unchanged. Most members indicated that global financial markets showed limited fluctuations, and in most economies government bond yields increased across the curve. Finally, they highlighted that the dollar depreciated.

Regarding Mexico’s economy, it showed a moderate rebound in 4Q25 with quarterly growth of 0.79% and full year annual growth of 0.5%, though activity remains sluggish and the output gap stays negative. Momentum came from services and a partial recovery in construction, while manufacturing remains weak. Private consumption stayed resilient due to higher labour income, but consumption of domestic goods remains fragile and investment is still at historically low levels despite slight improvements. Non‑automotive manufacturing exports continue to be the main external driver supported by U.S. tech‑sector dynamism, tariff advantages, and USMCA benefits. The labour market, however, shows signs of cooling: labour force participation is declining, formal employment is growing slowly, and wages continue rising above historical averages, contributing to persistent services inflation; although labour slack remains ample, its disinflationary effect has yet to clearly materialize.

On inflation, the Board noted that 2025 closed at 3.69% and that headline inflation in January 2026 rose slightly to 3.77%, driven by increases in core inflation—especially food goods—after the IEPS adjustments (special taxes). Non‑core inflation remains unusually low due to declines in energy and some agricultural products. While long‑term inflation expectations remain relatively stable and anchored, forecasts for 2026 and 2027 were revised upward, pushing the expected convergence to the 3% target to the second quarter of 2027.

Regarding financial markets, they indicated that the peso showed notable appreciation driven by global dollar weakness and carry‑trade strategies. Government bond yields fell across the curve, while inflation compensation rose slightly. The stock market reached new all‑time highs, and market consensus had already anticipated the February pause, with expectations of a potential cut in May.

In the monetary policy discussion, the Board unanimously decided to pause the rate‑cut cycle and maintain the policy rate at 7.00%, emphasizing the need to evaluate the impact of fiscal changes (IEPS and tariffs), monitor price pass‑through, and analyze exchange‑rate strength and economic weakness. Internally, several members noted that fiscal effects will be one‑off and transitory. However, three members argued that it is necessary to remain vigilant or cautious and wait for new data confirming the transitory nature of these effects before continuing with rate cuts, given that inflation risks remain tilted upward and monetary policy transmission has been less effective. Overall, the Board acknowledges that there is still room for future cuts, but strictly conditioned on inflation dynamics and the absence of second‑round effects.

Looking ahead, based on members’ comments, we believe the probability of an extended pause has increased significantly, although we do not rule out an additional 25 basis point cut at the March meeting, contingent on continued peso appreciation, headline inflation remaining within the 3% ±1% target range, and stable monetary conditions between the U.S. and Mexico. We thus maintain our expectation of a 2026 terminal rate at 6.50%, though a higher year‑end level cannot be excluded.

—Rodolfo Mitchell, Miguel Saldaña & Martha Cordova

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.