- Peru: Congress to elect an eighth president in ten years today; Vehicle sales reach highest monthly level on record

PERU: CONGRESS TO ELECT AN EIGHTH PRESIDENT IN TEN YEARS TODAY

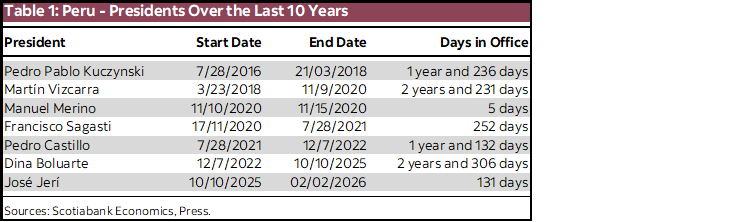

- Yesterday, Peru’s Congress approved a motion of censure against President José Jerí with 75 votes in favour, 24 against, and 3 abstentions. Jerí was Peru’s seventh president in the last ten years, having served for 131 days (table 1).

- The outcome was expected as Congress convened an extraordinary session—despite being currently in parliamentary recess—to debate seven motions of censure that were filed following his unofficial meetings with Chinese businesspeople and the controversial appointment of individuals linked to his inner circle to public office.

- In this context, the election of a new President of Congress will take place today. Under constitutional succession rules, the newly elected congressional leader will assume the presidency of the Republic until July 28th, 2026, when the next president-elect will take office following the April election.

Four candidates have been nominated to assume the President of Congress role: María del Carmen Alva (Acción Popular, centre-right), Héctor Acuña (Honor y Democracia, centre-right), Edgar Raymundo (Bloque Democrático, left), and José Balcázar (Perú Libre, left). If none of these candidates secures an absolute majority in the first round, a runoff election will be held between the two candidates receiving the highest number of votes.

The president-elect is expected to appoint a new cabinet in the coming days, including a new Minister of Economy. Centre-right candidates are considered to have the best chance of winning today's election, thus maintaining the pro-private investment economic policies pursued by recent administrations.

Impact

Although news of President Jerí's removal broke after the close of foreign exchange markets, there were no significant movements in the exchange rate or in the yields of Peruvian sovereign bonds or credit default swaps (CDS).

As seen in recent presidential transitions, investors appear to be differentiating political developments from underlying economic fundamentals. Accordingly, we do not anticipate significant short-term changes in financial variables, economic activity, or business expectations.

Nevertheless, public investment projects may experience delays associated with cabinet turnover and changes among high-ranking officials due to the learning curve of the new authorities.

Finally, the country's political instability over the last decade has imposed an opportunity cost for the Peruvian economy. Currently, Peru's potential GDP is around 3% due to the slower pace of private investment; however, with less political turmoil, potential GDP could rise to between 5% and 6%, aligned with growth rates seen in past decades.

—Pablo Nano

VEHICLE SALES REACH HIGHEST MONTHLY LEVEL ON RECORD

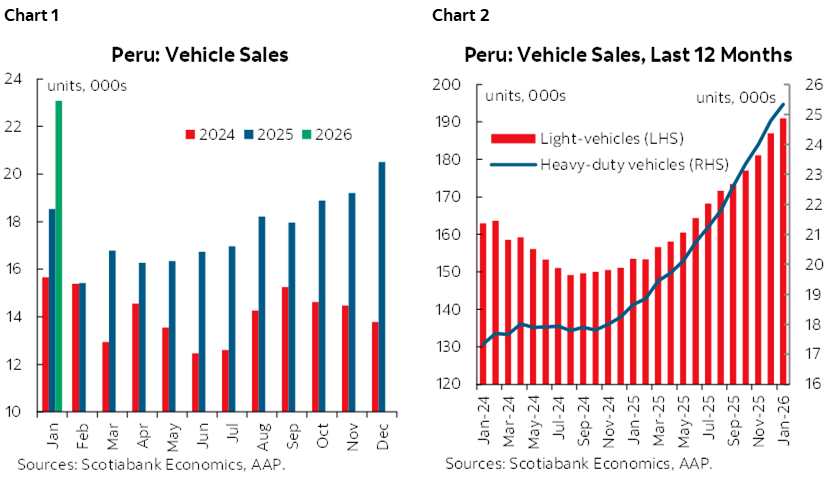

New vehicle sales reached 23,069 units in January (chart 1), according to data from the Automotive Association of Peru (AAP). This figure represents the highest monthly sales volume in Peru’s history, surpassing the previous record set in December 2025 (20,496 units). The January result exceeded our expectations, marking a 24% year‑over‑year increase relative to January 2025 and reflecting the solid momentum in the new vehicle market (chart 2).

Looking ahead, we expect the growth uptrend to remain at least through Q1‑26, supported by the continuation of the same drivers that boosted sales during 2025. While we anticipate some moderation in Q2‑26 due to the presidential elections in April, we expect momentum to rebound in the second half of 2026, ending the year with at least single‑digit growth.

By segment, light‑vehicle sales reached 20,628 units, an increase of 24% from January of the previous year. This was also the highest monthly figure on record, surpassing the December 2025 peak (18,124 units) and coming in above our projections. Several factors contributed to this strong performance: improvements in formal private‑sector employment, easing inflationary pressures (the national consumer price index increased only 0.12% in January), a relatively low sol‑dollar exchange rate compared with prior years (reducing the local‑currency cost of imported vehicles), access to extraordinary funds at the end of 2025—particularly the eighth withdrawal from private pension funds—and an expanded range of vehicle models in this category, especially those of Chinese origin. These conditions sustained robust demand through January.

Heavy‑vehicle sales reached 2,441 units in January, up 28% from January 2025. This marked the second‑highest monthly figure on record, just below the historical high reached in September 2025 (2,443 units), and was broadly in line with our expectations. Ongoing private‑sector investment supported growth in this segment, as firms showed a greater willingness to renew their fleets—even ahead of the Q2‑26 electoral season, a departure from the dynamics observed in earlier presidential cycles. Companies continued to benefit from a lower sol‑dollar exchange rate compared with recent years (which reduced import costs), improved financing conditions (lower credit rates), and a wider variety of available truck and bus models.

—Carlos Asmat

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.