HIGHLIGHTS

- Mid-month CPI and economic activity data out of Mexico is the highlight in Latam, as economists maintain their calls for two more cuts by Banxico while markets see only toss-up odds of just one 25bps reduction.

- Colombian macro figures on Friday may reinforce bets on BanRep to hike by 50bps at its late-January decision with economic strength due to combine with heavy price pressures from the government’s 20%+ minimum wage hike.

- Chile’s calendar only offers PPI and the central bank traders’ survey, with the latter likely confirming market pricing for no cut in January and high odds of a move in March. Our economists believe the BCCh will opt for easing at its decision on the 27th, backed by the latest inflation data and CLP strength.

- We’ll get little from Peru and Brazil on the economic front, where political developments, ahead of respective April and October elections, may be in focus, especially in Brazil with little public movement on a possible candidacy withdrawal by Flavio Bolsonaro breeding market anxiety.

- Outside of Latam, news out of the World Economic Forum in Davos (including a Trump address), the BoJ’s decision and a likely snap election call by PM Takaichi, global PMIs and U.S., U.K., and Canadian inflation data are the highlights.

- In today’s report, our team in Mexico goes over their call for Banxico to cut twice in the coming months—in contrast to hawkish markets—and discuss the weakness in domestic demand over 2025. From Peru, our economists lay out their forecast for growth to recover in December based on preliminary indicators for the month, following a mining driven deceleration in November.

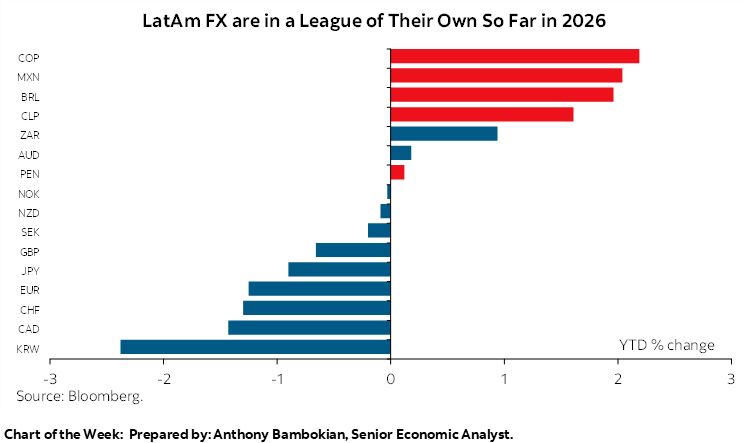

Chart of the Week

MEXICAN DATA TO DRIVE DIVIDED BANXICO EXPECTATIONS

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Mid-month CPI and economic activity data out of Mexico is the highlight in Latam, as economists maintain their calls for two more cuts by Banxico while markets see only toss-up odds of just one 25bps reduction.

- Colombian macro figures on Friday may reinforce bets on BanRep to hike by 50bps at its late-January decision with economic strength due to combine with heavy price pressures from the government’s 20%+ minimum wage hike.

- Chile’s calendar only offers PPI and the central bank traders’ survey, with the latter likely confirming market pricing for no cut in January and high odds of a move in March. Our economists believe the BCCh will opt for easing at its decision on the 27th, backed by the latest inflation data and CLP strength.

- We’ll get little from Peru and Brazil on the economic front, where political developments, ahead of respective April and October elections, may be in focus, especially in Brazil with little public movement on a possible candidacy withdrawal by Flavio Bolsonaro breeding market anxiety.

- Outside of Latam, news out of the World Economic Forum in Davos (including a Trump address), the BoJ’s decision and a likely snap election call by PM Takaichi, global PMIs and U.S., U.K., and Canadian inflation data are the highlights.

- In today’s report, our team in Mexico goes over their call for Banxico to cut twice in the coming months—in contrast to hawkish markets—and discuss the weakness in domestic demand over 2025. From Peru, our economists lay out their forecast for growth to recover in December based on preliminary indicators for the month, following a mining driven deceleration in November.

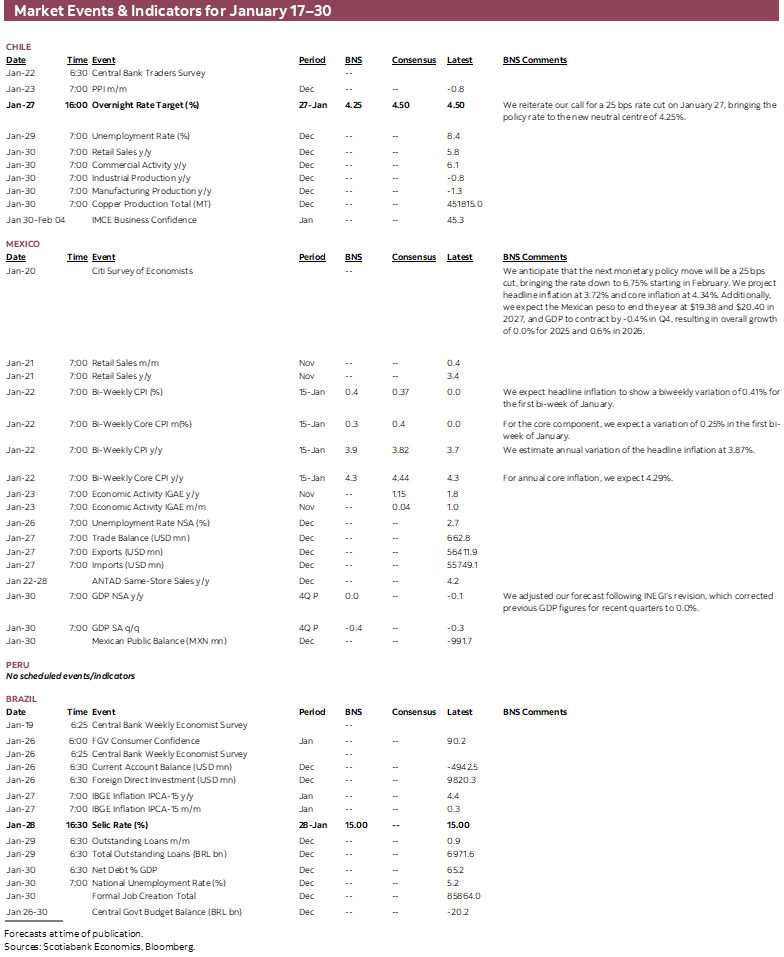

A relatively quiet week awaits in Latam as far as the data and events calendar goes, particularly outside of Mexico and Colombia, with G10 countries having beefier schedules while off-calendar items may stand again as the main drivers of global trading in the coming days. Developments in Iran with nationwide protests and risks around the regime being toppled or the U.S. striking the country should remain an important determinant of price action in energy and precious metals markets, as well as broad market sentiment. Oil should also take its cue from news out of Venezuela regarding the country’s crude output in deals with the U.S. following the exfiltration of President Maduro.

Global leaders also meet at the World Economic Forum in Switzerland, with President Trump scheduled to give an address on Wednesday. Possible comments regarding the White House’s lust for Greenland and international trade will be in focus—particularly as USMCA review discussions gather momentum. Markets also await an announcement by Japanese PM Takaichi late next week calling for a snap election to capitalise on her popularity, with the Bank of Japan (BoJ) delivering a likely rate hold that same day but with rates and currency guidance possibly reverberating globally. Chinese 4Q GDP out on Monday morning local time will get the ball rolling on the data front, with U.S. PCE, Global PMIs, U.K. and Canadian CPI, among other key releases, scheduled for the balance of the week. Note that U.S. markets are closed on Monday for MLK Jr. Day.

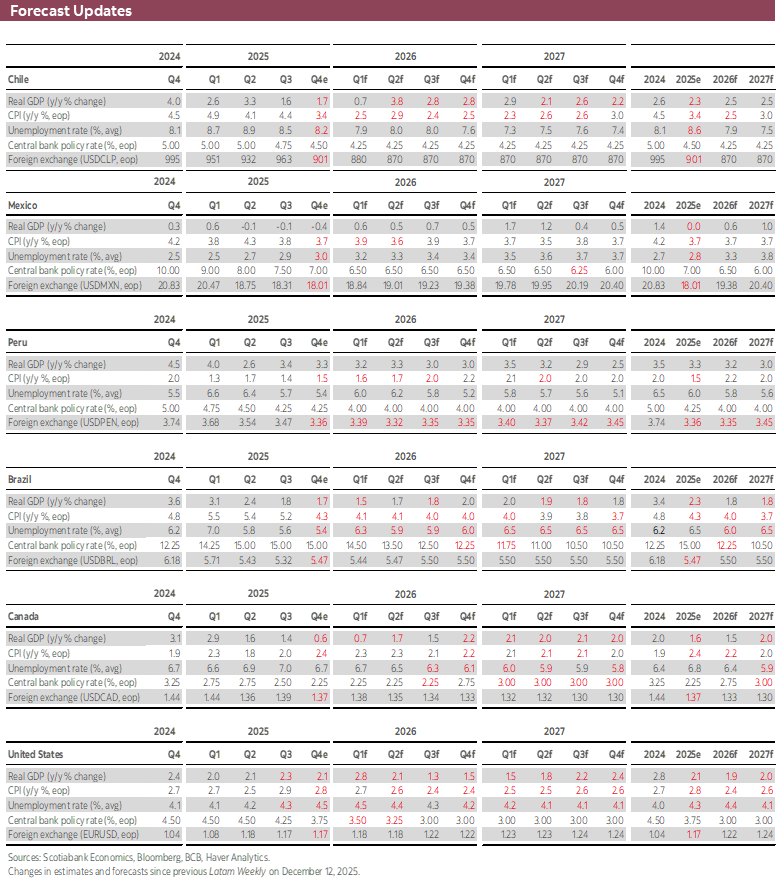

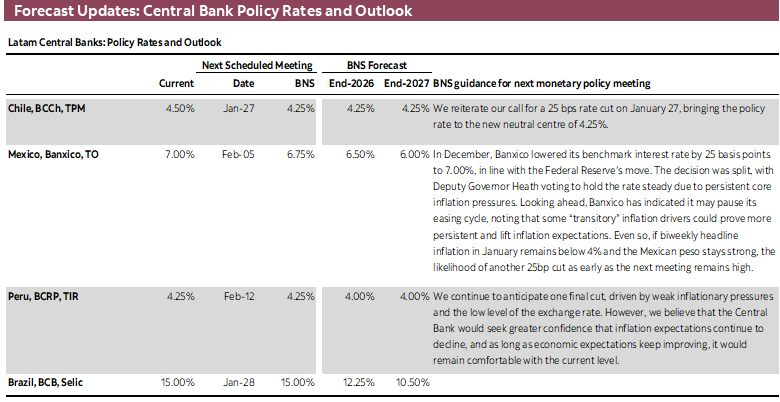

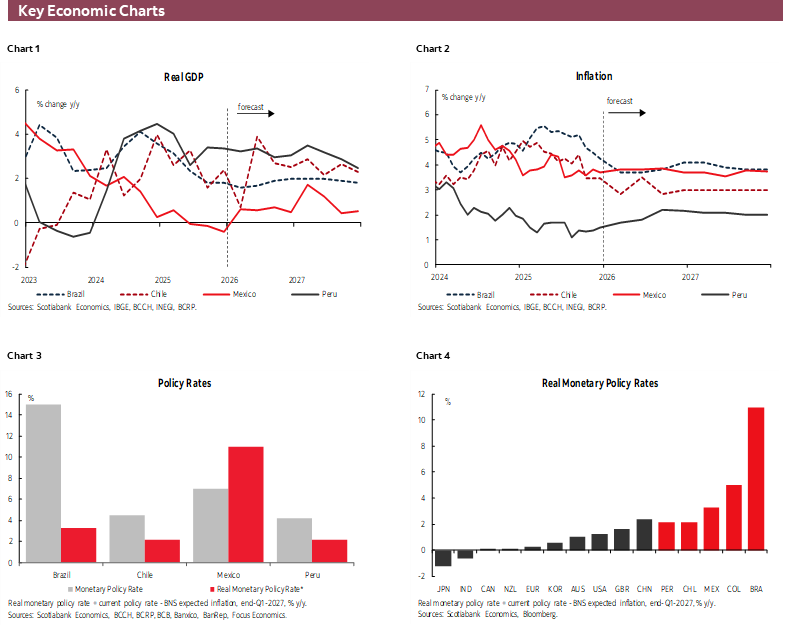

Mexico’s schedule is the busiest of all in the region, with bi-weekly CPI for the first half of January on Thursday standing as the highlight, looking ahead to Banxico’s February 5th rate announcement. In both headline and core terms, Mexican inflation is seen accelerating by about a couple decimal points from 3.7% and 4.3% in 2H-Dec, respectively, with base effects and the introduction of additional taxes on soft drinks and tobacco pressing higher. Despite the risks to the outlook from these higher taxes, labour cost pressures, and the implementation of new import tariffs (mostly from Asia), Banxico’s stance remains one that is clearly open to additional easing, as reflected in the minutes to its December meeting.

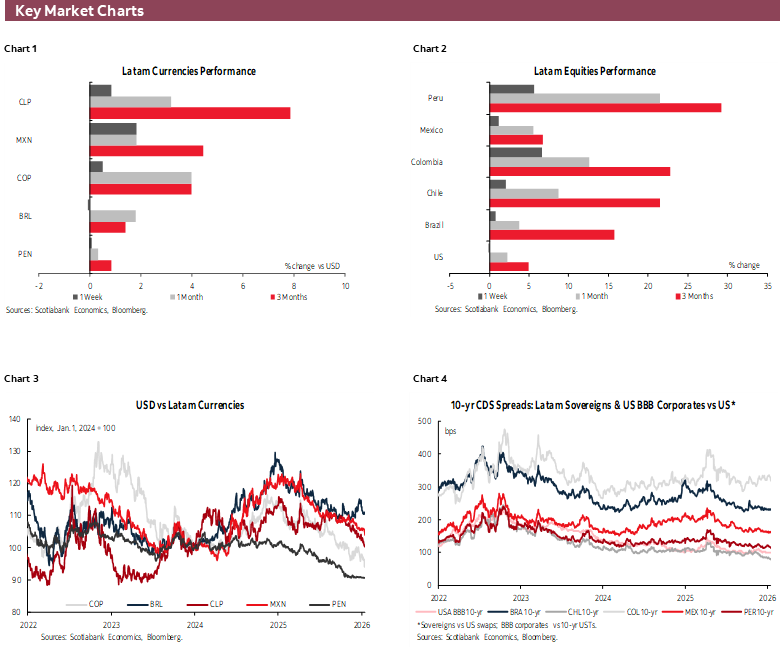

In today’s note, our colleagues in Mexico go over the uncertain course for Banxico policy in 2026. Yesterday, Scotiabank Economics updated its global macroeconomic projections for the next couple of years, with our team in Mexico sticking to their call for Banxico to roll out two more rate cuts in the current quarter, to a 6.50% level. One of these may slip into the second quarter, but we continue to believe more easing awaits. Recent (or continued) MXN strength—with the latest leg higher seemingly driven by positioning or technical factors rather than fundamentals—remains supportive of additional cuts as does within target-range inflation, from Banxico’s optimistic (read: dovish) standpoint. We’ll see what information next week’s CPI data provides. On Monday, we’ll also get the view of economists polled by Citi, which as of the survey’s latest edition showed the median economist expecting that Banxico will not cut until May. Markets are a good deal more hawkish, with at most 12–13bps in total cuts expected by mid-year.

Tricky inflation dynamics aside, Mexico’s economic backdrop remains weak, as our team also discusses in today’s Weekly. INEGI data published in recent days showed domestic demand lethargy as a constant throughout 2025 with muted consumption and shrinking investment justifying looser monetary policy settings. Despite the government’s wishes with its Plan Mexico to kickstart faster growth over the remainder of the decade, political and regulatory uncertainty, insufficient utilities, and trade risks should remain a headwind for private investment over the medium-term. On Friday, Mexico publishes November economic activity figures that should show a deceleration in year-on-year growth to the low-1s from 1.8% y/y in October. Retail sales for November are also due Wednesday.

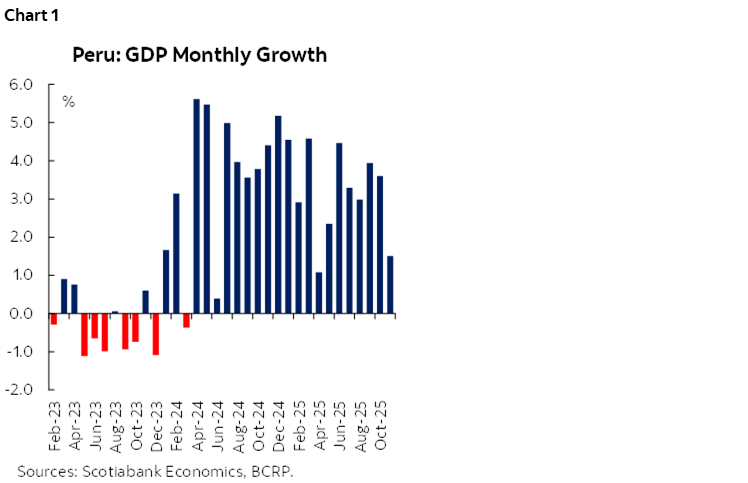

Peru’s calendar will give us nothing next week, but our local economists discuss the latest GDP data for November—which fell short of estimates at 1.5% y/y due to a sharp drop in mining—that should show some improvement in December as non-resource sectors maintain their solid momentum. According to the key indicators tracked by the team, they estimate that GDP expanded by 3% y/y in the final month of the year, which would leave monthly average GDP growth averaging 3.4% in 2025 (about in line with our full-year forecast). We’ll have to keep an eye on how data and confidence measures evolve over the next few weeks, with the April general elections fast approaching but polls still not showing any candidate getting more than around 10% of voting intention.

Elsewhere in the region, Chile’s calendar will only offer the BCCh’s traders survey on Thursday and December PPI on Friday, the same day as Colombia releases a flood of macroeconomic figures (economic activity, retail sales, and industrial output). Chile’s releases should be rather uneventful, with the traders survey likely confirming pricing on screens pointing to minimal expectations of a BCCh rate cut in late-January and about a 75% chance of a quarter-point reduction in March; our economists believe that the latest inflation data will motivate a cut this month. Colombian data are expected to remain strong, adding fuel to the fire of market bets on hikes by BanRep with traders eyeing a 50bps hike at the January 30th meeting—namely on the back of the massive 23% minimum wage hike for 2026 (and whose influence on other prices the Petro government is now racing to restrict).

Brazil will also not give us much to go on data-wise on the heels of a nice beat (and revisions) in November economic activity data published this morning. Brazil’s economy grew by 1.3% in November, overshooting the 0.7% Bloomberg median that was also the rate of expansion in October (revised up from 0.4%). Despite the upside surprise, Brazilian growth remains unspectacular and largely dependent on government stimulus measures and subsidies which should continue to catalyse growth in the coming months, perhaps incrementally ahead of the October election. The BCB is seen returning to cuts with a 25bps move in March, with traders seeing a total of ~225bps in easing by year-end.

Overall local markets remain anxious about who will be Lula’s main opposition in this year’s vote, with little movement—publicly, at least—around Flavio Bolsonaro (the former president’s eldest son) withdrawing his candidacy and clear the road for the market’s preferred option, Tarcisio do Freitas (who this morning said the right will be united around Flavio, however). Tarcisio is reportedly making some moves behind closed doors to push for a lighter treatment or sentence for the imprisoned Jair Bolsonaro, but markets may need to see some progress here to gain some optimism that Lula will not be re-elected. The latter leads Flavio by about 10ppts in head-to-head second-round opinion polls, compared to about 5ppts or less against Tarcisio.

COUNTRY UPDATES

Mexico—The Uncertain Course of Monetary Policy in 2026

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

The year began with a particularly dynamic environment in terms of monetary policy. On one hand, Citi’s survey of private-sector analysts shows that the vast majority anticipate that Banco de México will pause during the first two decisions of the year and that the rate-cutting cycle could resume in May or even later. In this scenario, the next expected move would be a 25 basis point reduction in the target interest rate, bringing it to 6.75%. Consequently, the median projection among analysts is at a terminal rate of 6.50%; however, the range of responses is broad, from 6.00% to 7.00%, reflecting a high dispersion in expectations.

Another relevant factor for monetary policy in 2026 is the recent evolution of inflation. Headline inflation closed 2025 at 3.69%, below our estimated 3.75% and slightly lower than the market consensus. This level falls within Banco de México’s target range (3% ±1%) and represents a significant decrease compared to the 4.21% observed in December 2024. However, core inflation pressures persist, ending the year at 4.33%, above the upper limit of the target range and marking eight consecutive months above that reference. This persistence has led several analysts to question the Central Bank’s commitment to its primary mandate of preserving the stability of the national currency’s purchasing power.

In this context, a third element that, far from clarifying the outlook, generated greater uncertainty was the minutes from the December 17th monetary policy decision. These reveal a clear heterogeneity of views among the Governing Board members. Some indicated that there is still room to continue the rate-cutting cycle, though emphasizing the need to proceed more gradually given the risk of potential second-round effects stemming from price increases associated with the IEPS tax and the implementation of tariffs on imported products from countries without trade agreements with Mexico. Other members considered that, in an environment of heightened inflationary risks, it is more prudent to adopt a “wait-and-see” strategy before further easing monetary policy. Meanwhile, Deputy Governor Jonathan Heath argued that it is necessary to pause the rate-cutting cycle, given that inflationary pressures persist and factors such as economic slowdown and peso appreciation have had a limited effect in offsetting them.

Even so, from our perspective, it is not entirely clear why most analysts anticipate a prolonged pause in the rate-cutting cycle until May. We believe there is still a window for Banco de México to lower the reference rate as early as February, considering the exchange rate level and the likelihood that inflation in the first half of January remains below the upper limit of the target range. Additionally, a moderate probability that the Federal Reserve cuts its rate in January could create room for Banco de México to continue the cycle without compromising the interest rate differential. This scenario contrasts with the prevailing market sentiment, and it is difficult to identify a clear catalyst that would justify an immediate cut, beyond a potential Fed adjustment that Banco de México decides to follow.

Nevertheless, going forward, the risk remains that inflationary pressures will persist throughout 2026, particularly due to increases in the IEPS tax and tariffs, which could complicate inflation’s convergence to the 3% target in the third quarter of 2026, as currently projected by the central bank. A potential revision of this forecast, delaying such convergence, could significantly limit the room to continue the rate-cutting cycle during the rest of the year. Thus, the start of 2026 is characterized more by accumulating questions than by clarity in the direction of Mexico’s monetary policy.

Weakness of Domestic Demand and Challenges to Achieving the Investment Targets of the Mexico Plan

Domestic demand continues to look quite weak. Last week, INEGI published the indexes for both investment and consumption for October, showing mixed results.

Consumption began 2025 in negative territory and has shown mixed behaviour throughout the year. After remaining stagnant in July and August, it has seen slight increases over the past two months. In September and October, real annual variations were positive, at 3.2% y/y and 4.6% n.s.a. respectively, maintaining a GDP share close to 48–49% since the third quarter of 2023. Historically, the lowest range for consumption’s share of GDP falls between 47% and 50%, so although recent months have shown upticks, this does not necessarily translate into particularly strong figures.

For its part, gross fixed investment in October marked fourteen consecutive months in negative territory. However, the decline has gradually eased, going from -10.9% y/y in August, to -6.7% in September, and -5.5% in October, reaching -7.4% in the YTD January–October cumulative figure. Public investment has seen particularly sharp drops, staying between -21% and -23% since May, and only slightly improving to -19.7% in October. Meanwhile, private investment saw its worst decline in April at -12.89% and has since stabilized at -2.7% in October.

Regarding GDP participation, since the first quarter of 2018—and with only a few exceptions—investment has remained below 24%, representing minimum historical levels. Moreover, in the third quarter of 2025, it fell to 22.7%, the lowest figure since the third quarter of 2022 and close to levels seen during the pandemic.

The second goal of the Mexico Plan, which aims to increase investment to 25% of GDP in 2025 and 28% by 2030, contrasts with the current reality of weak domestic demand and gross fixed investment that has been negative for over a year. Although consumption has shown slight recent rebounds, its share of GDP remains historically low. Public investment continues experiencing sharp declines, while private investment is only beginning to stabilize.

The factors limiting this objective are clear: business confidence remains weak due to political and regulatory uncertainty; there is a lack of adequate infrastructure; and key sectors—particularly industry and public utilities—remain stagnant and have not fully recovered since the pandemic. Additionally, public investment remains at historically low levels, forcing greater reliance on private capital. To reverse this trend, it will be essential to create a climate of legal certainty and secure public–private agreements to accelerate infrastructure projects and establish clear incentives for private investment, especially in sectors with strong potential for productive linkages. Without these conditions, the goals outlined in the Mexico Plan and in development programs will be difficult to achieve, increasing the risk of moderate economic growth and limiting the country’s ability to establish itself as one of the leading economies by the end of the decade.

Peru—After November’s Surprise, GDP is Expected to Maintain its Momentum in December

Ricardo Avila, Senior Analyst

ricardo.avila@scotiabank.com.pe

Peru’s GDP expanded by 1.5% YoY in November (chart 1), falling short of our growth forecast of 2.2% and the market consensus of 2.4%, according to Bloomberg’s survey.

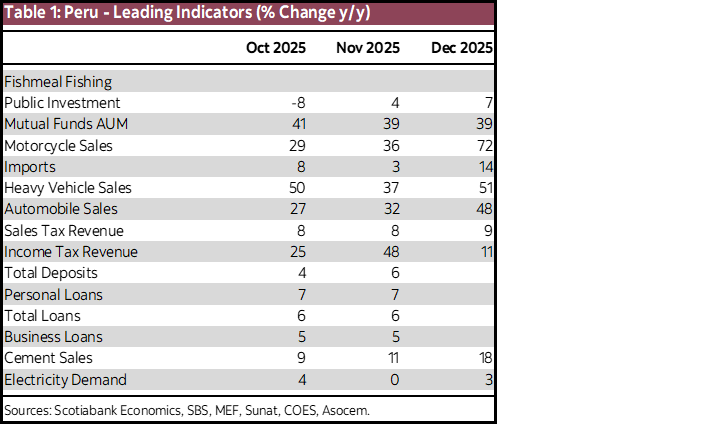

The performance across sectors was mixed. Non-resource-based sectors such as construction, trade, and services stood out for their solid growth. Construction surged by 9.9% YoY, driven by robust domestic cement consumption and the acceleration of public investment (table 1). Trade grew by 4.2%, supported by seasonal stocking ahead of the Christmas campaign and wholesale sales, particularly of fuel. Meanwhile, services expanded by 3.0% YoY.

Conversely, resource-linked sectors posted negative results. Mining contracted by 6.5% YoY, reflecting lower copper and tin (output due to a one-week maintenance shutdown at Minsur, the country’s sole tin producer). Agriculture declined by 1.0% YoY, affected by reduced harvested areas amid adverse weather conditions. Finally, fishing plummeted by 17.9% YoY, as a delayed start to the anchoveta fishing season and lower catch quotas weighed on activity.

Looking ahead, non-resource sectors are expected to maintain strong momentum. Our key indicators for December point to an improvement over November (table 1 again), with stronger growth in vehicle sales and imports of goods linked to the Christmas campaign, continued resilience in savings through investment funds, and better performance in indicators closely tied to economic activity, such as public investment, electricity consumption, and cement sales. Based on these trends, we anticipate an economic rebound in December, with growth around 3.0%.

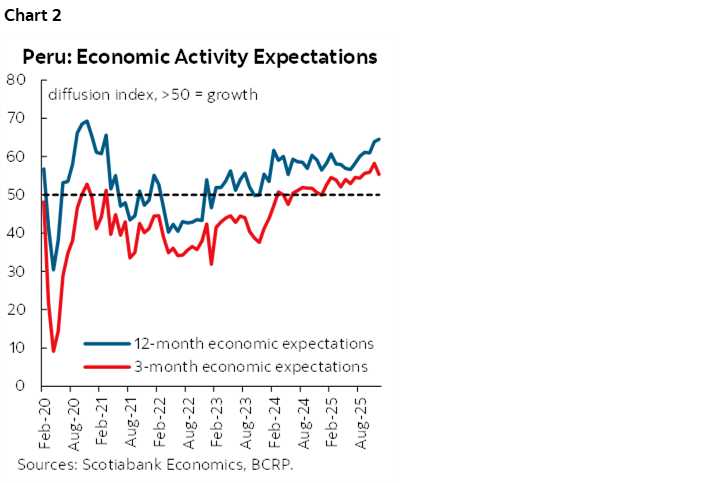

On the other hand, on January 9th, the Central Reserve Bank published the results of its Macroeconomic Expectations Survey, reaffirming economic agents’ perception of a solid economy (chart 2). Three-month economic expectations have registered a slight deterioration, likely due to the proximity of the next general elections (April 12th). However, they remain within the optimistic range. Meanwhile, 12-month expectations continue their uptrend, reaching a four-and-a-half-year high. This suggests that market participants assign a higher probability to a smooth electoral process and anticipate that the incoming administration will maintain a pro-investment stance.

| LOCAL MARKET COVERAGE | ||

| CHILE | ||

| Website: | Click here to be redirected | |

| Subscribe: | anibal.alarcon@scotiabank.cl | |

| Coverage: | Spanish and English | |

| MEXICO | ||

| Website: | Click here to be redirected | |

| Subscribe: | estudeco@scotiacb.com.mx | |

| Coverage: | Spanish | |

| PERU | ||

| Website: | Click here to be redirected | |

| Subscribe: | siee@scotiabank.com.pe | |

| Coverage: | Spanish | |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.