HIGHLIGHTS

- Next week should be a quieter one across Latam and the G10, with global trading thinned by U.S. and Canadian holidays on Monday (and Chinese New Year celebrations).

- Key releases and events are backloaded to the second half of the week, including Brazilian GDP and Banxico’s minutes, as well as U.S. PCE and GDP, a possible decision by the U.S. Supreme Court on Trump’s tariffs, and global PMIs.

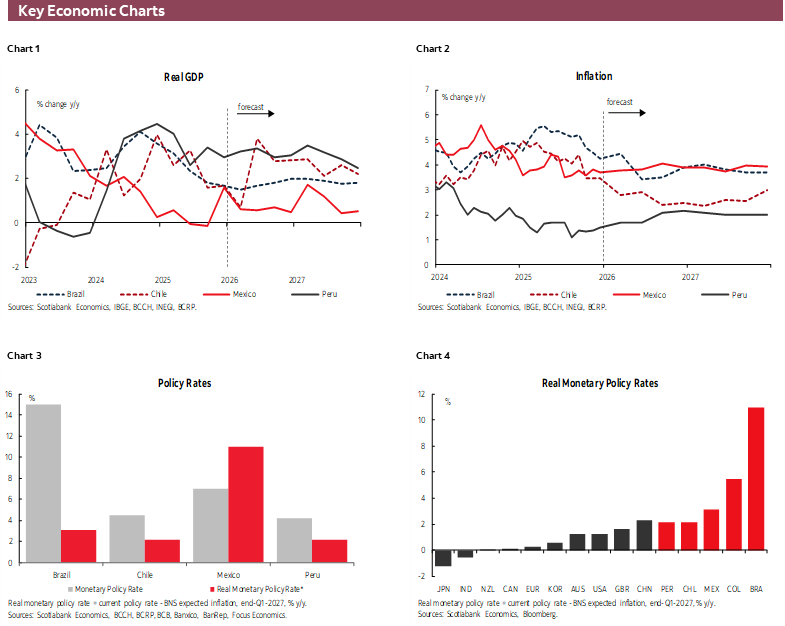

- Latam kicks off the week with Peruvian and Colombian Dec/4Q GDP, on Sunday and Monday, to close out activity figures for 2025 showing Peru and Colombia grew by ~3.3% and ~2.8%, respectively, last year. Meanwhile, Brazil should clock in at a ~2.5% expansion, in spite of highly restrictive policy rates.

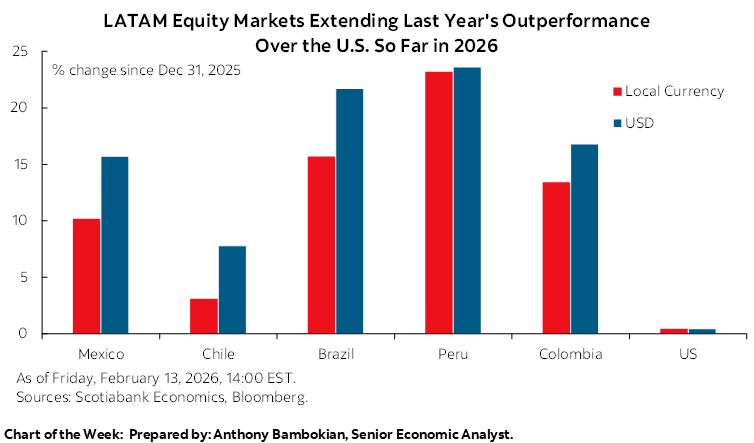

Chart of the Week

REGIONAL GDP AND BANXICO MINUTES

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Next week should be a quieter one across Latam and the G10, with global trading thinned by U.S. and Canadian holidays on Monday (and Chinese New Year celebrations).

- Key releases and events are backloaded to the second half of the week, including Brazilian GDP and Banxico’s minutes, as well as U.S. PCE and GDP, a possible decision by the U.S. Supreme Court on Trump’s tariffs, and global PMIs.

- Latam kicks off the week with Peruvian and Colombian Dec/4Q GDP, on Sunday and Monday, to close out activity figures for 2025 showing Peru and Colombia grew by ~3.3% and ~2.8%, respectively, last year. Meanwhile, Brazil should clock in at a ~2.5% expansion, in spite of highly restrictive policy rates.

Next week will generally be a quieter one across Latam and the G10, with global trading thinned by U.S. and Canadian holidays on Monday (and Chinese New Year celebrations). The majority of key events are scheduled for the latter half of the week, which will close on Friday with global PMIs, U.S. PCE and 4Q GDP data, and a possible decision by the U.S. Supreme Court on the White House’s emergency powers tariffs. Canadian and U.K. CPI on Tuesday and Wednesday, and Tuesday’s U.K. employment report will influence local markets though the global mood will likely remain driven by AI disruption fears that have shaken trading sentiment in recent weeks. U.S.-Iran tensions should also continue to shape global energy markets.

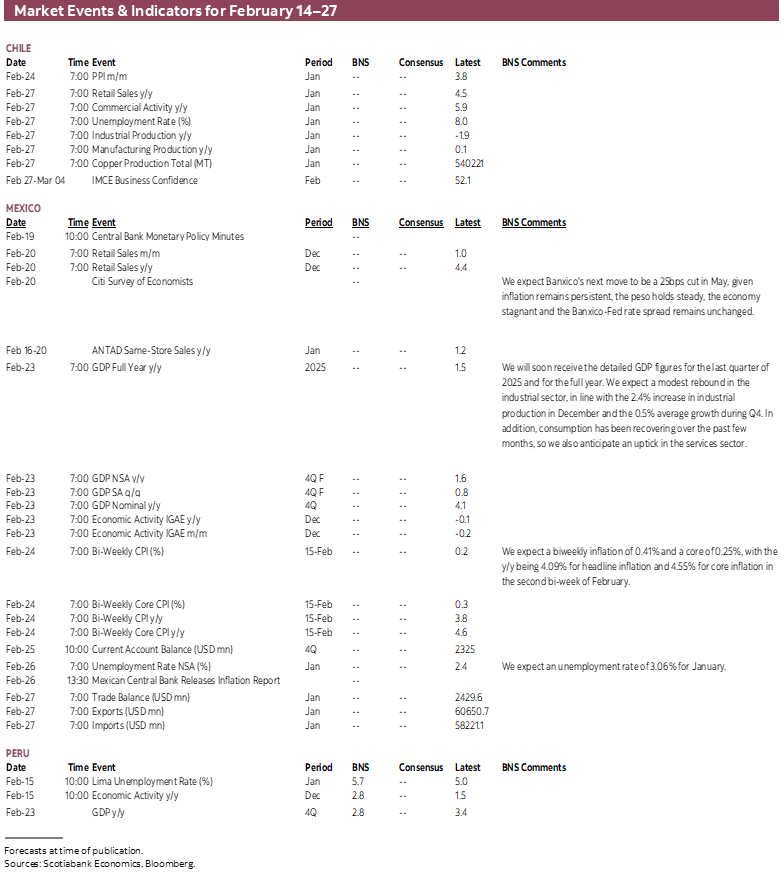

In Latam, we kick off the week to Sunday releases of January unemployment rate and December GDP data from Peru, with Colombian 4Q GDP scheduled for Monday morning before a two-day break until Thursday’s Brazilian December economic activity and Banxico’s February meeting minutes, followed by Friday’s Mexican December retail sales and the Citi survey of economists. Chile’s calendar is bare of major economic releases with markets counting down the days to the start of Kast’s presidency on March 11th.

Peru is estimated to have rebounded in December to around a 3% expansion, doubling November’s rise of 1.5% that was its weakest since April in an otherwise strong year for GDP growth in the country. A large 6.5% y/y contraction in mining sector output due to a fall in tin production owing to maintenance by Minsur (the country’s sole tin miner) should somewhat correct in December data, as should a 17.9% y/y drop in fishing production due to a delayed catch season and reduced quotas. Economic indicators for construction, investment, and personal spending were solid for the month.

With the 2.8% y/y GDP rise projected by our economists, Peru’s economy would have grown by 3.3% over the whole of 2025 closing with a 2.8% y/y gain in 4Q. Supportive inflation and monetary policy levels as well as the boost from another round of pension withdrawals and strong investment trends should see the country grow by about the same pace in 2026, with some drag from the election period and the start of a new administration. With about two months until the first-round vote for the presidency, the field remains wide open, although conservative candidate Rafael López Aliaga has steadily lead polls since last August, albeit with only a 12% voting intention in the latest Ipsos survey, with Keiko Fujimori (also from the right) following with an 8% share.

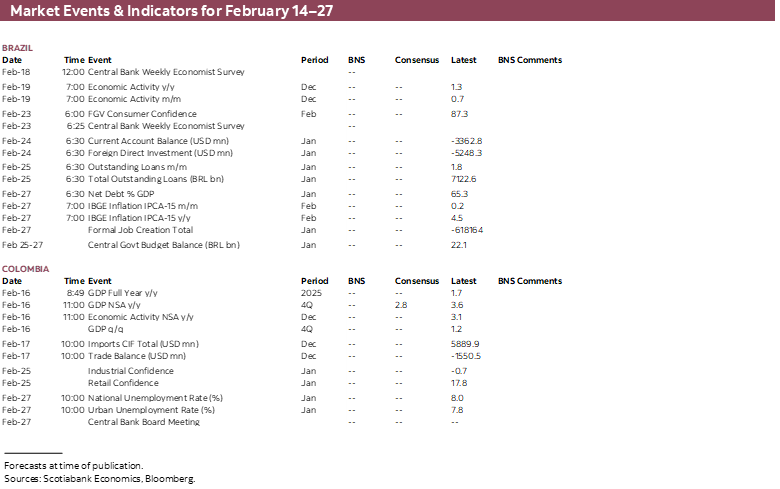

Like Peru, Brazil’s economy is expected to have picked up in December, to somewhere around 2% after its 1.3% November gain. Industrial production bounced back from a 1.4% contraction to a 0.4% rise in December as mining strength offset a decline in manufacturing output (its eighth y/y drop in the past nine months). Meanwhile, real retail sales growth of 2.8% y/y marked a recovery from a 0.2% drop in November. With a 2% expansion in December, Brazil’s economy activity would have grown by 2.4% over 2025, roughly in line with our GDP growth forecast of 2.3%.

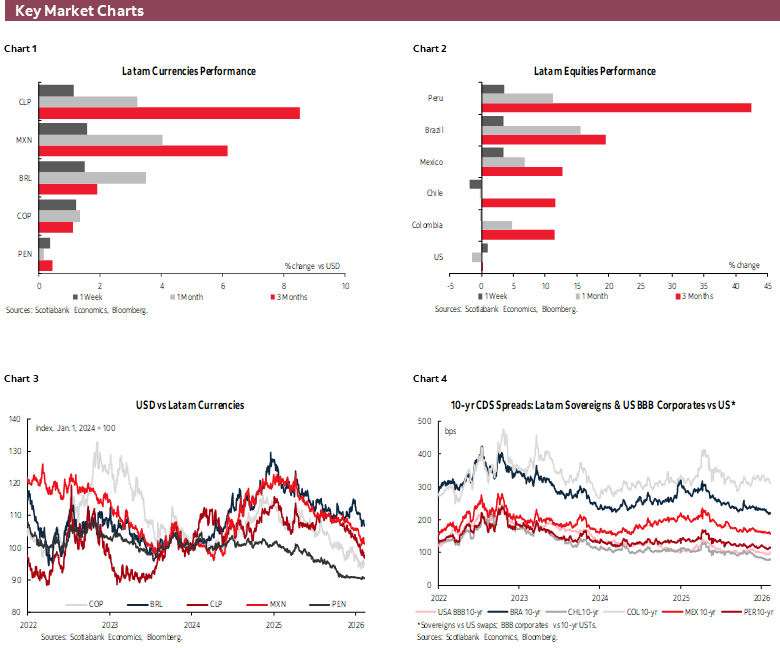

Unlike Peru, there’s really only two candidates to follow in polls for Brazil’s October election, the incumbent Lula and his top challenger Flavio Bolsonaro. The recent narrowing of Lula’s lead in polls against Flavio (from about 10ppts to about half in the space of two months) has built market confidence in the latter’s chance at beating the current president, and with that bring more pro-market/business policies. However, business leaders were seemingly unimpressed with Flavio’s economic plans or the lack of clarity for these and who will make up his cabinet. An underwhelming challenge to Lula may begin to reverberate as a fear in Brazilian markets, denting the Ibovespa’s strong 15%+ gain so far this year.

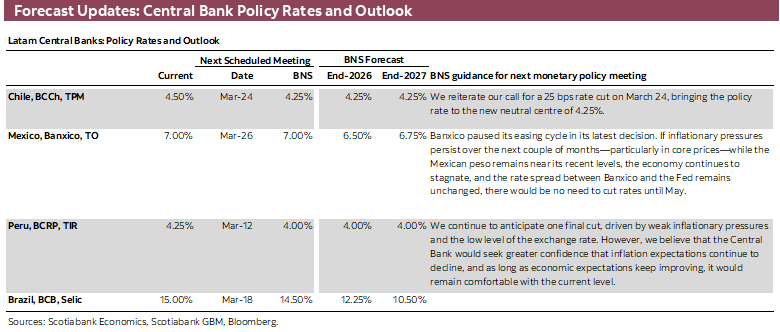

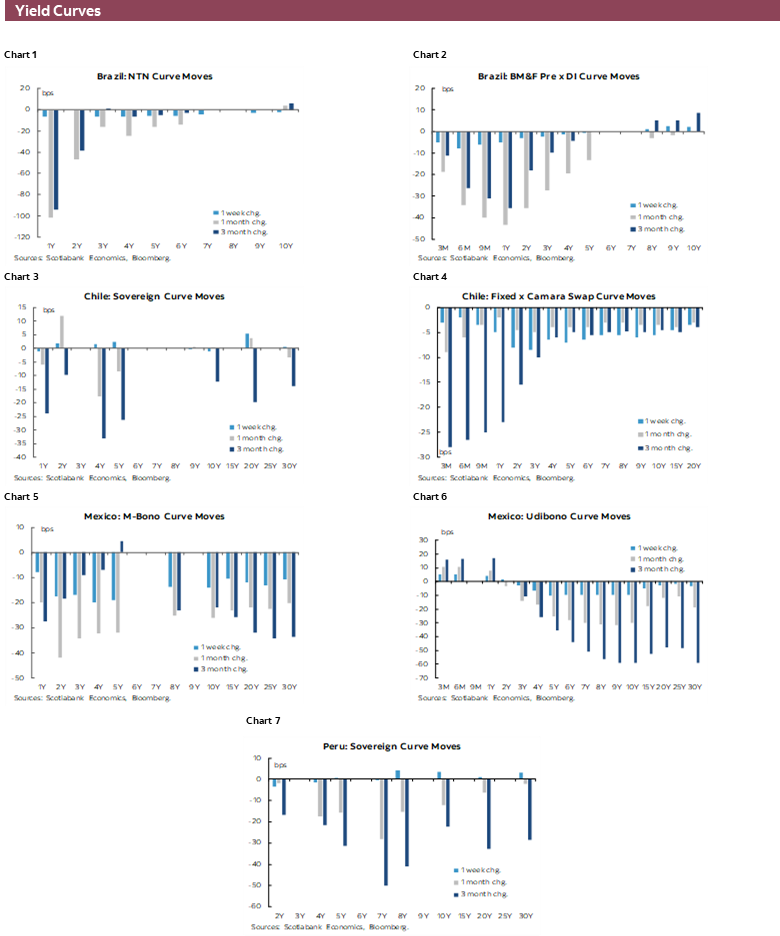

Banxico’s meeting minutes out on Thursday will shed some light on why the bank decided to lift its inflation forecasts substantially over the near term, but still saw a convergence to the 3% target in 1H27, and simultaneously left the door open to more rate cuts in spite of these near-term inflationary risks. We may have to pay particularly close attention to the views of hawkish board member Heath in the minutes (comments are anonymous, but one can tell) as he recently floated the possibility of a cut at one of the upcoming meetings despite his generally hawkish stance. Mexican retail sales due on Friday should not move the needle too much, nor should the results to the Citi survey of economists which are nevertheless worth following for possible shifts in Banxico rate cut expectations. We continue to forecast that Banxico will cut twice to 6.50% by around mid-year.

Finally, Colombia releases 4Q/2025 GDP data on Monday which is expected to show a ~3% y/y expansion in the final quarter of the year to wrap up a full-year GDP rise in the high-2s. Strong economic growth and pronounced inflationary pressures continue to advocate for BanRep policy rate increases. However, BanRep rate expectations were thrown a curveball today with Council of State suspending the government’s 23% minimum wage hike decree, giving them eight days to come up with a well-justified alternative. How the government intends to play this, or even how firms will walk back this increase, will be in focus over the next few days but the high court’s ruling was a strong reminder to markets of institutional strength in the country, supporting the currency and Colombian borrowing rates (on top of revised BanRep expectations).

| LOCAL MARKET COVERAGE | ||

| CHILE | ||

| Website: | Click here to be redirected | |

| Subscribe: | anibal.alarcon@scotiabank.cl | |

| Coverage: | Spanish and English | |

| MEXICO | ||

| Website: | Click here to be redirected | |

| Subscribe: | estudeco@scotiacb.com.mx | |

| Coverage: | Spanish | |

| PERU | ||

| Website: | Click here to be redirected | |

| Subscribe: | siee@scotiabank.com.pe | |

| Coverage: | Spanish | |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.