HIGHLIGHTS

- Mexican, Brazilian, and U.S. CPI are the data highlights in the Americas next week, alongside the release of U.S. employment data, with the BCRP’s rounding out the Latam key events calendar while global markets reopen on Monday to the results of Japan’s lower house election.

- Mexican January CPI is first out on Monday, expected to show a slight acceleration in core and headline inflation in line with mid-month readings, just a few days after Banxico’s latest rate hold where upward revisions to its forecasts clashed with guidance language that left the door open to additional easing. In today’s report, the local team goes over recent data and fiscal developments in the country, detailing their new Banxico rate forecast.

- Brazilian inflation is seen picking up a touch in January, from 4.3% to 4.4%, with base effects in domestic power bills driving a great deal of the rise, while most other main categories experience slowdowns in inflation as per mid-month CPI data. The data will likely reinforce market and economists expectations for a half-point cut at the BCB’s March meeting. In politics, Flavio Bolsonaro catching up to Lula in polls suggest he is here to stay as the right’s leading candidate for the October vote.

- Peru’s central bank decision on Thursday is expected to leave the reference rate unchanged at 4.25%—with our team eyeing the next BCRP rate cut at the March meeting. Today, our economists in Lima focus on the continued momentum in financial conditions in the country, despite election risks. In 2025, lending grew at its largest click in six years.

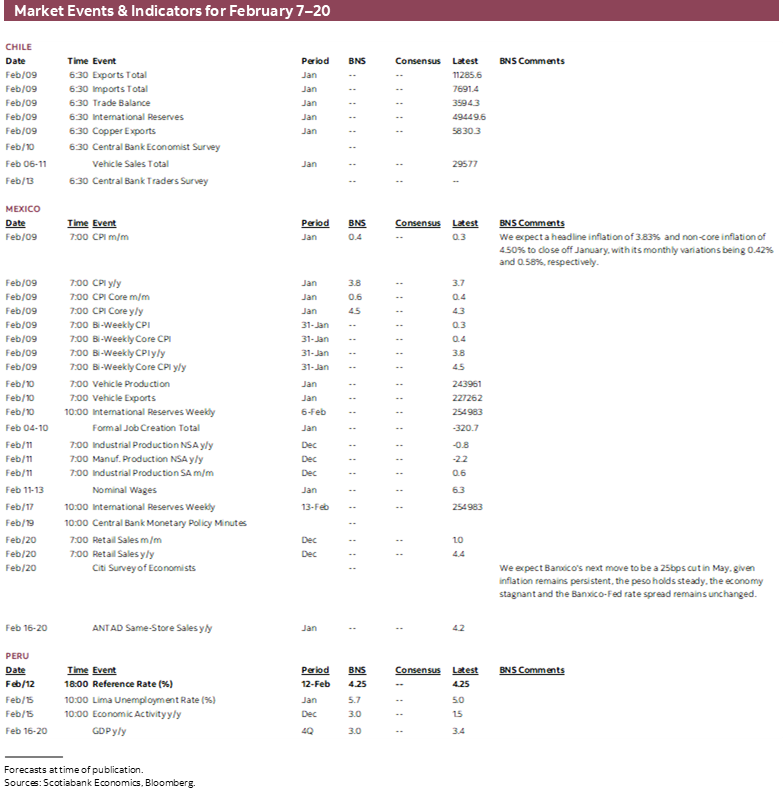

- International trade data out on Monday is the only noteworthy economic release from Chile next week, to feed into GDP estimates for the first quarter of 2026. January data will kick us off after a strong 2025 when Chilean exports in USD terms rose by 7.9%. The team discusses this morning’s in-line CPI release that reinforces their call for a 25bps next month.

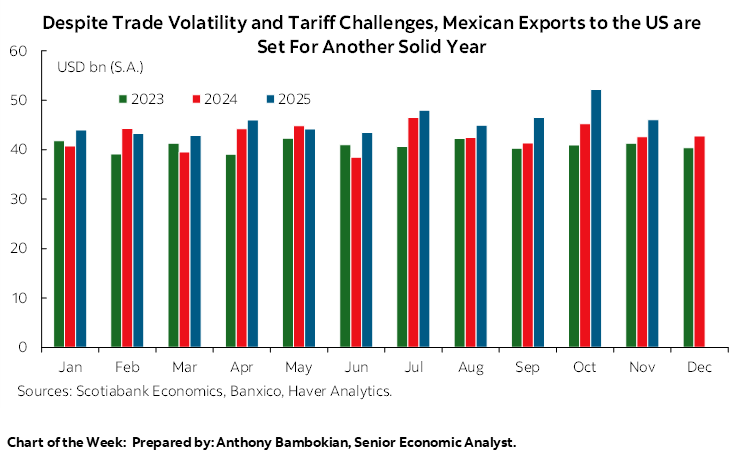

Chart of the Week

MEXICAN & BRAZILIAN CPI, BCRP RATE HOLD

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Mexican, Brazilian, and U.S. CPI are the data highlights in the Americas next week, alongside the release of U.S. employment data, with the BCRP’s rounding out the Latam key events calendar while global markets reopen on Monday to the results of Japan’s lower house election.

- Mexican January CPI is first out on Monday, expected to show a slight acceleration in core and headline inflation in line with mid-month readings, just a few days after Banxico’s latest rate hold where upward revisions to its forecasts clashed with guidance language that left the door open to additional easing. In today’s report, the local team goes over recent data and fiscal developments in the country, detailing their new Banxico rate forecast.

- Brazilian inflation is seen picking up a touch in January, from 4.3% to 4.4%, with base effects in domestic power bills driving a great deal of the rise, while most other main categories experience slowdowns in inflation as per mid-month CPI data. The data will likely reinforce market and economists expectations for a half-point cut at the BCB’s March meeting. In politics, Flavio Bolsonaro catching up to Lula in polls suggest he is here to stay as the right’s leading candidate for the October vote.

- Peru’s central bank decision on Thursday is expected to leave the reference rate unchanged at 4.25%—with our team eyeing the next BCRP rate cut at the March meeting. Today, our economists in Lima focus on the continued momentum in financial conditions in the country, despite election risks. In 2025, lending grew at its largest click in six years.

- International trade data out on Monday is the only noteworthy economic release from Chile next week, to feed into GDP estimates for the first quarter of 2026. January data will kick us off after a strong 2025 when Chilean exports in USD terms rose by 7.9%. The team discusses this morning’s in-line CPI release that reinforces their call for a 25bps next month.

CPI data out of Mexico, Brazil, and the U.S. will be in focus for the Americas next week, alongside Peru’s rate decision, and the mid-week release of delayed U.S. employment figures that will shape global sentiment together with the results of this weekend’s Japanese election. There won’t be much else to catch the markets and economists’ attention over the coming days, easing off a busy period of central bank decisions and key data, while the jury is out on whether market turbulence will continue amid AI disruption fears, volatility in precious metals, and geopolitical risks.

Mexican January CPI is first out on Monday, with economists expecting an acceleration in headline inflation to 3.8% from 3.7% in December and core inflation to 4.5% from 4.3% in line with the pick-up observed in mid-month CPI data. In-line results should not surprise markets, but some attention will be paid to the impact of higher taxes and tariffs at the start of the year as pressures on underlying inflation trends, although it may take a handful of prints to gauge whether these influences are transitory or become more engrained in Mexican price trends.

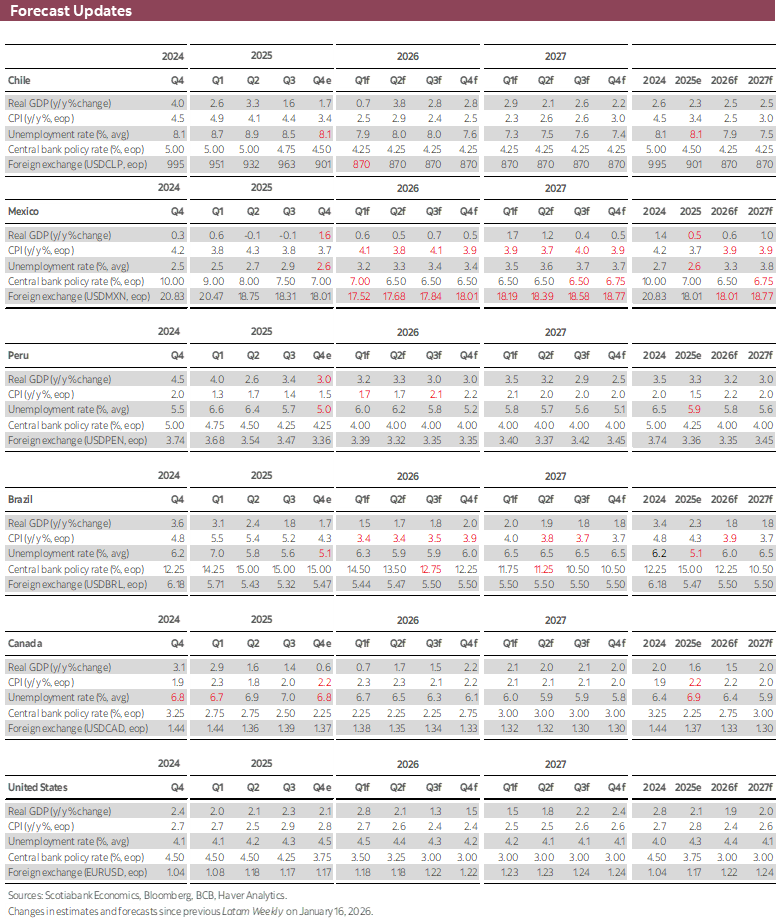

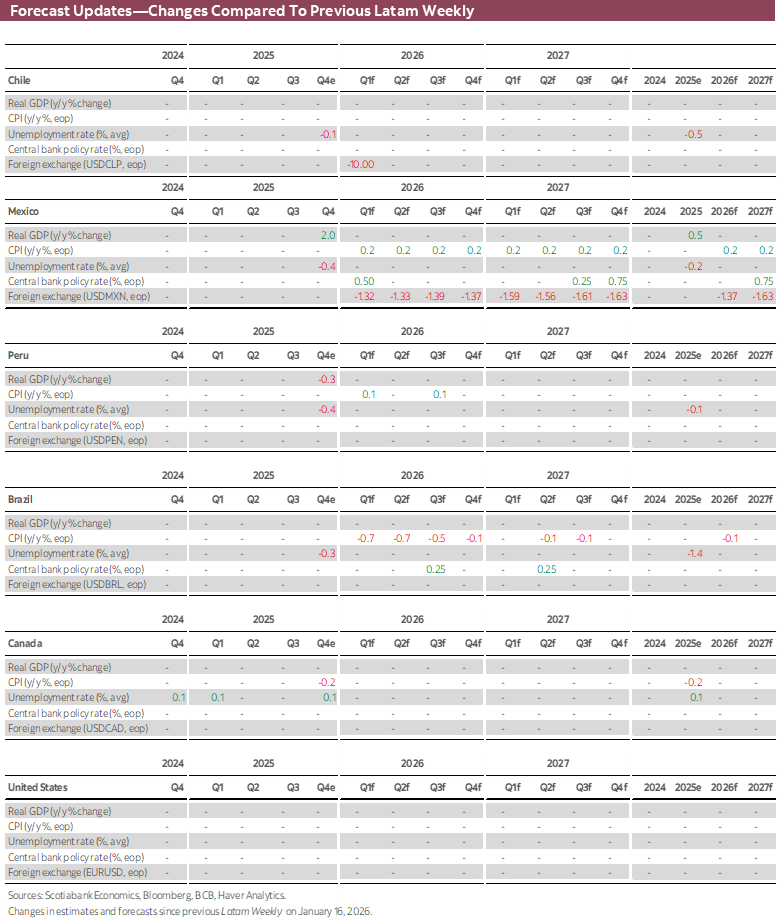

At its February 5th rate pause decision (see here), Banxico’s staff finally caught up to private sector economists with a revision higher to its inflation forecasts, acknowledging the impact of higher taxes and tariffs, but also refreshing its views to firmer inflation trends that were in place even prior to the kicking in of these factors at the start of the year. From projecting that headline and core inflation would both close 2026 at 3.0%, Banxico now anticipates that headline inflation will end the year at 3.5% and core inflation will sit at 3.4%. On the other hand, Banxico made minimal upward revisions to its 2027 inflation forecasts, seeing headline and core inflation reaching the 3.0% target in 2Q27 and staying there over the remainder of the year, unchanged from their previous projections.

This ‘mixed’ forecast revision reflects some but also some underlying dovishness that leaves the door open to additional rate cuts, with the statement also maintaining that “looking ahead, the Board will evaluate additional reference rate adjustments”—an unchanged guidance sentence that may have surprised markets that perhaps anticipated that Banxico could narrow its language around possible cuts.

At yesterday’s close, markets were pricing in a maximum cumulative 31bps in Banxico cuts by its August decision, with about 20% implied odds of a quarter-point cut at its next meeting, in late-March. These 31bps compare to the 22bps total pencilled in as of the previous day’s close.

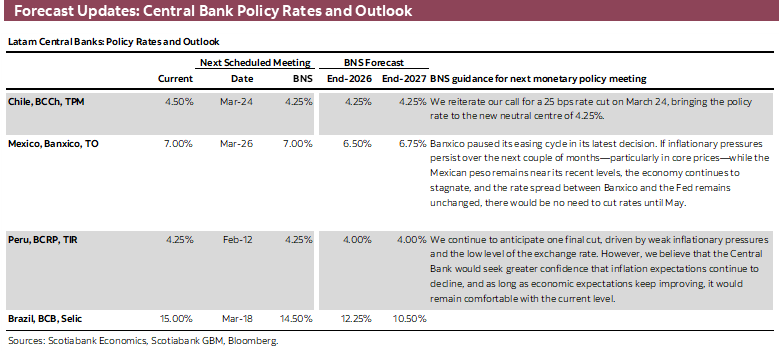

Considering the bank’s stance on inflation and, seemingly, its belief that the inflation overshoot will merely be temporary, we think officials will still deliver two 25bps rate cuts this year—both coming in 2Q26. However, Banxico has for some months now signalled it is within reach of ending its easing cycle. Accordingly, we no longer think that cuts will continue in 2027, and instead of the 50bps in easing to 6.00% that we previously projected, we now believe Banxico will be forced to correct from excessive easing with a 25bps hike to 6.75% in the latter part of 2027.

On Wednesday, Mexico’s INEGI publishes December industrial and manufacturing production data that should show a pick-up from year-on-year declines in November, as guided by 4Q GDP figures released last week, which showed that secondary sector GDP expanded by 0.4% y/y after a 2.7% y/y contraction in 3Q, for its first positive print since 3Q24. In today’s Weekly, the team in Mexico briefly go over recent data and fiscal developments in the country, as well as their updated Banxico rate forecast.

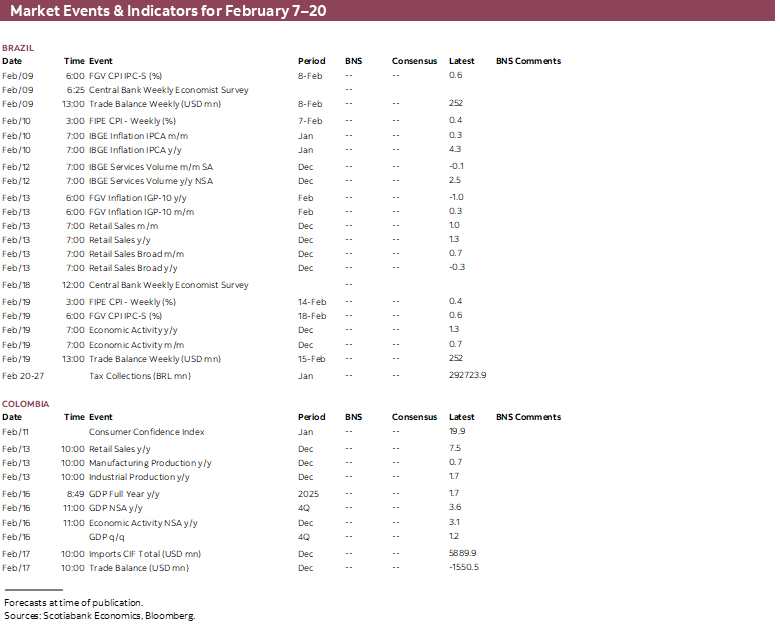

Brazilian inflation is expected to accelerate slightly in January, from 4.3% to 4.4%, with base effects in domestic power bills driving a great deal of the rise, while most other main categories experience slowdowns in inflation as per mid-month CPI data. The focus will be on the performance of core prices measures, likely extending their deceleration since around last April/May in most of the BCB’s and IBGE’s measures, particularly on the core goods front. At writing, markets are betting on a 50bps cut by the central bank at its early-March meeting after the BCB teed up the start of rate cuts in last week’s decision, pointing to it now being appropriate to calibrate policy settings.

Meanwhile, on the political front, it would seem that Flavio Bolsonaro will end up being the right’s leading candidate in the October elections. With continued shows of support and alliance for his candidacy by the market’s preferred candidate, Sao Paulo governor Tarcisio de Freitas, and Flavio’s improving performance in head-to-head polls against incumbent Lula, signs are pointing to former president Jair’s son staying in the race. This contrasts with the earlier belief that his candidacy was mostly a play to obtain better imprisonment terms for his father to then give way to Tarcisio. Lula’s narrowing lead over Tarcisio has partly been behind the strong performance of Brazilian equities in the year to date, with the Ibovespa index’s 13.5% year-to-date gain leading all major equity markets globally with broad-based strength among its constituents.

International trade data out on Monday is the only noteworthy economic release from Chile next week, to feed into GDP estimates for the first quarter of 2026. January data will kick us off after a strong 2025 when Chilean exports in USD terms rose by 7.9%—though the 10.3% rise in imports, reflecting a firmer domestic backdrop resulted in a marginal narrowing of the trade balance. The BCCh will also publish the results to its economists and traders survey, with rate cut expectations standing as the highlight. Following this morning’s CPI release, which our team in Chile discusses in today’s note, we expect that the BCCh will lower its overnight rate by 25bps to 4.25% at the March announcement—remaining here until the end of the forecast horizon in 2027. Markets are also on board with this call, pricing in ~20bps in cuts, an 80% chance, for next month.

Peru’s central bank decision on Thursday is expected to leave the reference rate unchanged at 4.25%—with our team eyeing the next BCRP rate cut at the March meeting. The BCRP often surprises, but we see fewer risks of them doing so this time around compared to past instances, particularly as the bank probably wants to enjoy a bit the recent stability in the PEN exchange rate (aided by USD purchases), and officials can definitely wait a bit more and monitor the rebound in inflation before delivering another reduction.

In today’s Weekly, our economists in Lima focus on the continued momentum in financial conditions in the country, despite election risks. In 2025, lending grew at its largest click in six years (ex. pandemic), by 6.5%, amid favourable dynamics in household and business demand, further supported by BCRP rate cuts. By economic sector, the key parts of the economy, wholesale/retail trade and logistics sectors alongside the food and agricultural exporting industries, drove lending growth last year, but mining and business services borrowing recorded among the largest y/y increases.

Finally, Colombia will publish retail sales and industrial/manufacturing production numbers for December on Friday that will reinforce the perception of strong economic momentum in the country, particularly from a household standpoint as retail sales expanded by ~12% y/y on average in the year through November, in inflation-adjusted terms. It is likely that this spending momentum will not hold up, as the solid employment and wages backdrop should be more firmly offset by stubborn elevated inflation and BanRep rate hikes, although spending may merely decelerate from very strong levels to solid levels.

Elsewhere, economists estimate that the U.S. added 70k jobs in January alongside an unchanged 4.4% unemployment rate in data out on Wednesday, to be followed on Friday by a slight slowdown in headline and core CPI inflation, both to 2.5%, that will likely be insufficient to alter the Fed’s thinking on near-term rate holds. The U.K. publishes 4Q GDP data, with the median projecting a 0.2% q/q gain led by government spending and muted consumption on the heels of this week’s dovish BoE hold (see here). Before all that, global markets will open on Monday to the result of Sunday’s lower house elections in Japan where the ruling coalition is expected to regain control of the legislature but where the degree of this victory could empower or dampen PM Takaichi’s fiscal expansion plans—with implications for local and global debt markets, as well as the JPY.

COUNTRY UPDATES

Chile—Expected Rebound in Goods Prices and Contained Cost Pressures, CLP Appreciation Should Keep Inflation Below 3% for the Full Year

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

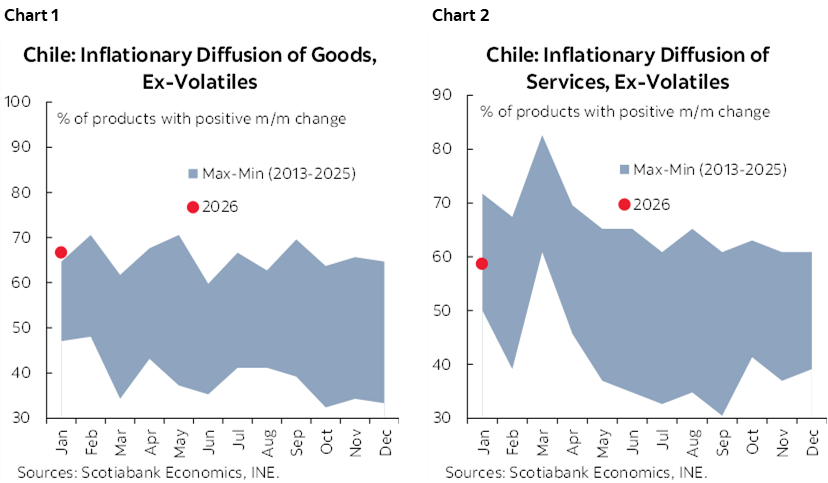

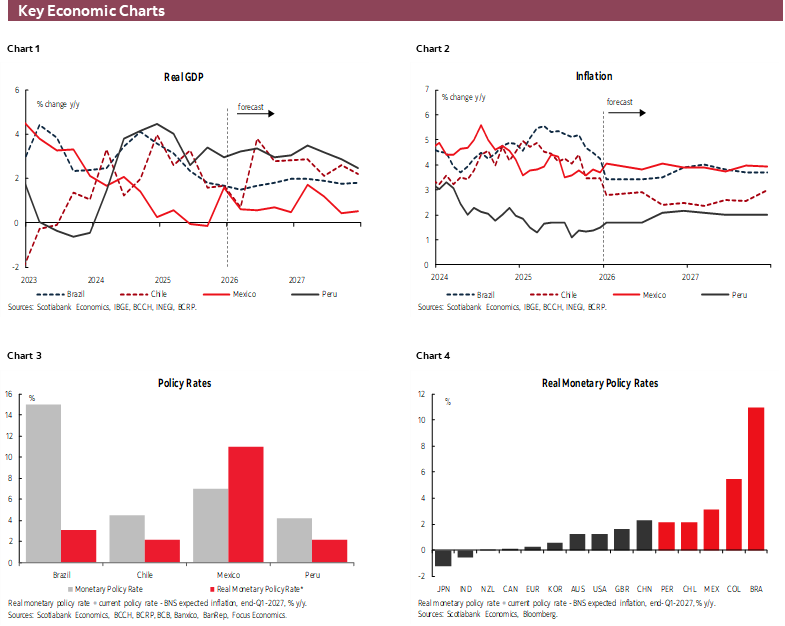

January CPI came in at 0.4% m/m (2.8% y/y), matching both market expectations and our own forecast. With this, annual inflation fell below 3% for the first time since March 2021. Core inflation (excluding volatiles) rose 0.7% m/m, driven mainly by a significant increase in goods prices (1.2% m/m), reflecting the high volatility associated with cyber events in the basket and still not capturing the recent peso appreciation. If CLP strength persists, FX pass-through should become more visible over the next 12 months, pushing market and Central Bank projections down by at least 0.5ppts. Meanwhile, services ex‑volatiles rose 0.4% m/m, consistent with historical patterns and signaling that labour‑cost pressures remain contained. At Scotia, we maintain our year‑end 2026 inflation forecast at 2.5% y/y, below the Central Bank’s 3.2% y/y expectation.

Core CPI saw expected post‑Cyber sales rebound—and then some. While goods ex‑volatiles surprised to the upside with a 1.2% m/m increase, we expect partial reversals in the coming months, alongside downward pressure from the stronger peso. Part of the rebound was anticipated due to the unwinding of discounts applied during December’s Cyber Day event—especially regarding the share of products registering price increases. However, the magnitude of the adjustments was the highest in at least three years. A standout example is computers, which fell 1.8% last month and rose 8% m/m in January—a jump unseen since at least 2013.

CLP appreciation should push market and Central Bank inflation forecasts lower. Since the statistical cutoff of the last Monetary Policy Report (MPR), the peso has appreciated by up to 8%. According to Central Bank estimates, this would imply a pass‑through of roughly 0.8ppts lower inflation over a 12‑month horizon (assuming a 0.1% pass‑through coefficient). Even considering mitigating factors—such as higher fuel prices and potential cost‑push pressures—the adjustment in the Central Bank’s inflation projections should still be at least 0.5ppts.

Services inflation was aligned with historical averages, with limited evidence of labour‑cost impacts. Common expenses, domestic services, and food at restaurants are among services categories where labour costs represent a significant share of inputs and have been influenced by the implementation of the Pension Reform and minimum‑wage hikes. So far, we do not detect meaningful deviations in their price dynamics that could be attributed to higher costs. One exception is dental services, which have increased nearly 10% since June (adding 0.16ppts to the CPI), possibly reflecting part of the labour‑cost adjustments.

Inflation diffusion reached 60.8% in January (charts 1 and 2). Broadly stable compared to last year, this was driven by increases in goods prices (charts 1 and 2 again). The ex‑volatiles basket recorded diffusion at the upper end of historical ranges, especially among goods (66.7%). Services continue to show contained inflation pressures, with diffusion below their historical average (58.7%).

Mexico—Recap and Banxico Forecast Update

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

Over the past two weeks, a series of indicators have shed light on the outlook for the Mexican economy toward the end of 2025. Starting with the first GDP estimates for the last quarter, the data showed a stronger expansion than expected (1.6% y/y) after two quarterly declines year-over-year with the rebound driven mainly by services, though the industrial sector also posted a modest gain after four straight quarters of contraction. As a result, GDP for the full year grew by only 0.5%, which, although slightly above analysts’ expectations (0.4%), still reflects underlying economic weakness.

According to Banxico’s Expectations Survey, also published recently, analysts anticipate GDP growth of just 1.30% for 2026. While this figure is higher than the previous consensus of 1.15%, it remains below the historical average. For our part, at least for now, we maintain a lower forecast of only 0.6%, based on the view that uncertainty and the lack of adequate infrastructure will continue to constrain economic activity.

In public finances, the full-year 2025 public-sector balance was released, showing a wide deficit (Public Sector Borrowing Requirements) of 4.8% of GDP, above the programmed 3.9%. Consequently, the broadest measure of debt—the Historical Balance of the Public Sector Borrowing Requirements—rose to 53.1% of GDP, compared with the originally projected 52.9%. For 2026, the Ministry of Finance projected in September a deficit of 4.1%, based on a slower increase in net spending (5.9% real annual growth) relative to budgetary revenues (6.3%).

For the 2026 fiscal year, key issues will include the performance of tax and non-tax revenues, the low level of public investment, and Pemex’s finances and developments. In this context, we also highlight the recent announcement of the creation of a Technical Planning Council, intended to coordinate public and mixed investment projects. Additionally, the Ministry of Finance expects public and mixed investments to total around 330 billion USD between 2026 and 2030. Unfortunately, details for promoting public-private partnerships remain unclear; however, the announcement of an intention to strengthen them is seen as a positive signal.

In monetary policy, Banxico met consensus expectations by keeping the policy rate unchanged. Unlike most analysts, we had expected a rate cut at this meeting, as—in our view—the recent appreciation of the peso, along with inflation below 4.0% and relatively close to consensus, provided an opportunity for an adjustment before inflation rose above the 4.0% threshold anticipated by several analysts. Moreover, several Board members have expressed a desire to end the year with a lower rate.

Given this, we adjusted our outlook and now expect the two cuts this year to occur in May and June, based on the idea that these two months may show a deceleration in headline inflation, even though the effects of higher excise taxes, tariffs, and wages could appear in the first quarter and persist through much of the year. Notably, Banxico revised its projections for both headline and core inflation upward, pushing the expected convergence to the 3.0% target to 2Q27, from 3Q26 in previous projections, while maintaining a risk balance tilted to the upside.

In this regard, we believe that rate cuts this year will materialize only if there are no second-round effects from tax and tariff increases, if the exchange rate does not experience an accelerated depreciation, and if the interest-rate differential between Mexico and the United States does not fall below 325 basis points.

Peru—Despite Elections, the Financial System is Expected to Maintain Solid Momentum in 2026

Ricardo Avila, Senior Analyst

ricardo.avila@scotiabank.com.pe

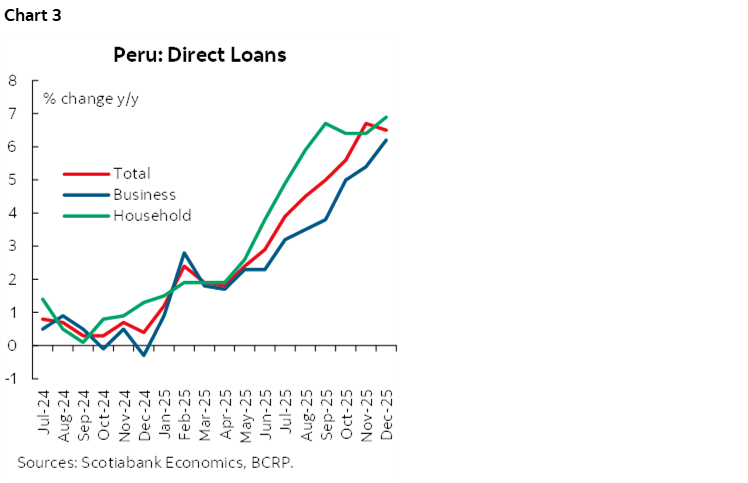

Peru’s financial system closed 2025 with solid momentum (chart 3), driven by the strong performance of loans, which expanded by 6.5% during the year—the highest rate in six years (excluding the pandemic period, as figures are distorted by the Reactiva program). This loan expansion reflects the favourable dynamics of domestic demand—both consumption and investment—and consolidates the uptrend observed since late 2024. The evolution of loans mainly responds to lower interest rates—consistent with the Central Reserve Bank’s (BCRP) flexible monetary policy stance amid easing inflationary pressures—alongside a rebound in private investment, a recovery in private consumption, and a steady improvement in business expectations.

According to BCRP data, business loans—linked to private investment, which we estimate to be close to 10% in 2025—expanded by 6.2% during 2025. This performance was broad-based across most segments. Corporate, medium-sized, and small businesses all showed favourable dynamics, while loans to large firms posted more moderate growth. In contrast, loans to micro-businesses remained in negative territory.

Household loans—associated with private consumption, which we estimate grew 3.7% in 2025—it exceeded expectations, reaching 6.9% growth for the year. The positive momentum was shared by mortgage loans, which accelerated to 7.1% annually—the fastest pace in three years—and by consumer loans, which grew 6.7%. However, consumer loan growth stabilized in the last quarter, as the positive base effect came to an end, and December recorded a flow approximately S/500 million lower due to amortizations associated with the eighth pension fund withdrawal.

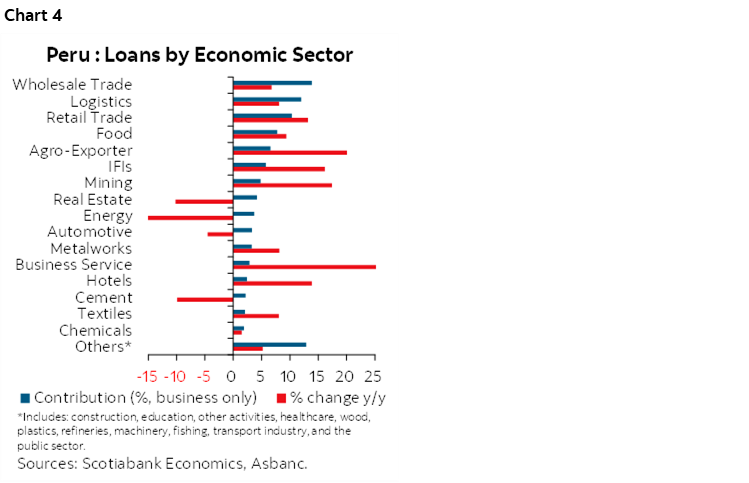

Economic sectors with the greatest weight in the banking system continue to show solid loan growth (chart 4). This includes the trade, logistics and telecommunications, food industry, agro-export, financial institutions (IFIs), and mining sectors. These sectors have been driving the expansion of business loans, in line with the favourable evolution of private investment. It is worth noting that, out of the 28 economic sectors we monitor, 21 show consistent growth.

At the same time, delinquency in the banking system has continued to decline, reflecting an improved financial position of economic agents, supported by stronger economic expectations, higher production levels, a solid labour market, and improved purchasing power amid low inflation. As a result, delinquency fell from 3.8% in 2024 to 3.3% in 2025, the lowest level in just over five years (since September 2020). Among businesses, delinquency declined from 4.2% at the end of 2024 to 3.6% in 2025, while among households it fell slightly from 3.0% to 2.8%.

We maintain our expectation that direct loans will remain solid and grow around 5% in 2026. This is a significant rate considering that 2026 is an election year and that the 2025 base is relatively high (6.5%). Loan growth is expected to moderate during the first half of the year but remain at healthy levels. In the first quarter of 2026, the financial system will continue to feel the impact of amortizations linked to AFP withdrawals, while in the second quarter, the comparison base for businesses will remain elevated. Regarding the electoral cycle, we believe it will not have a significant impact on the financial system. Our baseline scenario assumes that the incoming administration will maintain a pro-investment stance, and there is no sufficient evidence of negative impacts in previous elections. Therefore, there is no reason to expect a materially different outcome this year.

| LOCAL MARKET COVERAGE | ||

| CHILE | ||

| Website: | Click here to be redirected | |

| Subscribe: | anibal.alarcon@scotiabank.cl | |

| Coverage: | Spanish and English | |

| MEXICO | ||

| Website: | Click here to be redirected | |

| Subscribe: | estudeco@scotiacb.com.mx | |

| Coverage: | Spanish | |

| PERU | ||

| Website: | Click here to be redirected | |

| Subscribe: | siee@scotiabank.com.pe | |

| Coverage: | Spanish | |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.