ECONOMIC OVERVIEW

- Mexican and Brazilian CPI will influence Banxico and BCB expectations, with markets expecting that the former may only have one cut left in the cycle, while the latter is seen starting its cutting cycle in early-2026—a move that it may tee up at its Wednesday announcement. Developments in Brazilian politics will also be in focus, after former president Jair Bolsonaro backed his son Flavio for the 2026 presidential race shook local markets in recent days.

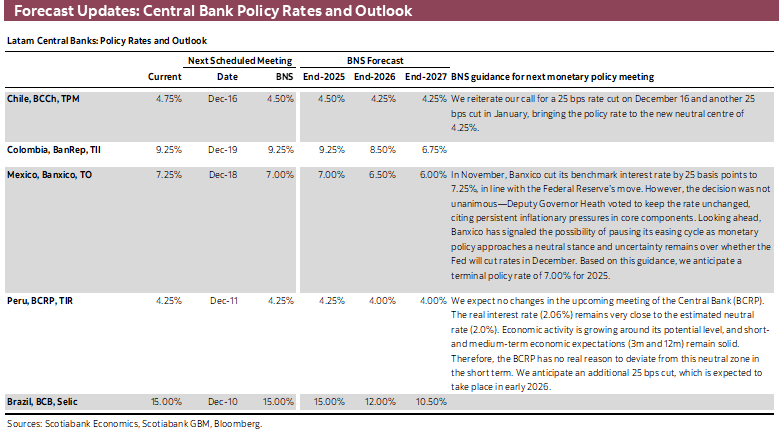

- We think the BCRP will keep rates on hold at its Thursday decision, but with recent inflation data and falling expectations it would not be terribly surprising that they opt for a cut next week instead of in early-2026, as we expect. Ultimately, it’s a minor adjustment and the timing of it next week or next month is not of major significance.

- The Fed’s expected cut with refreshed projections is the main event next week, with markets also paying close attention to guidance by the BoC, RBA, and SNB with all three expected to hold but the first two facing hike bets in markets while the latter is seen possibly going back to negative rates next year.

MARKET EVENTS & INDICATORS

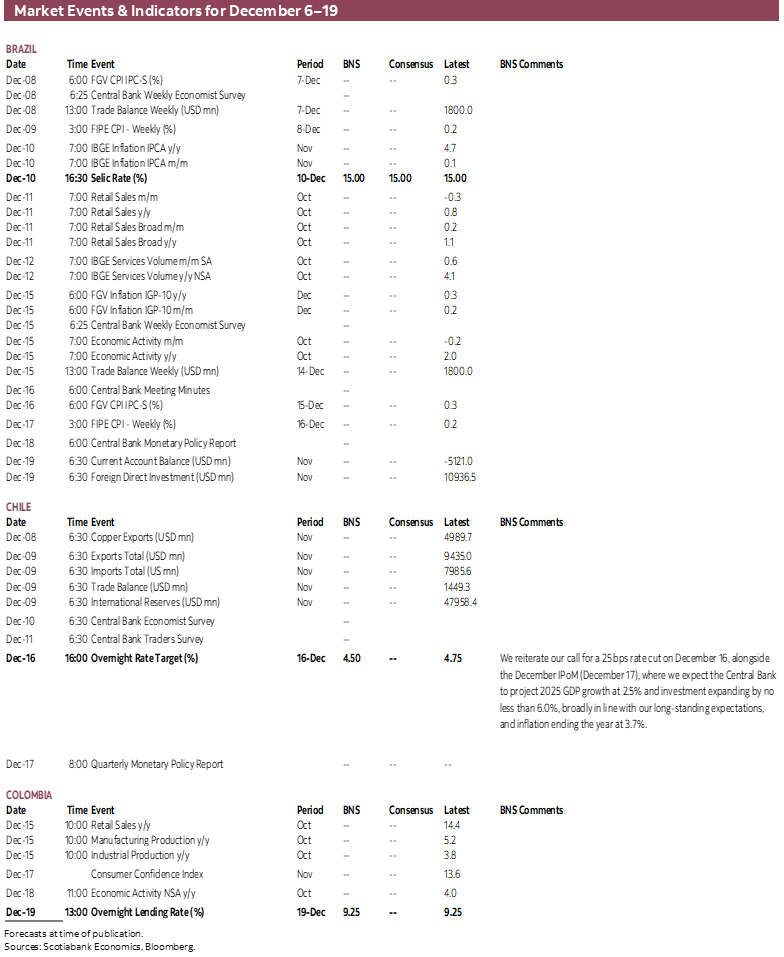

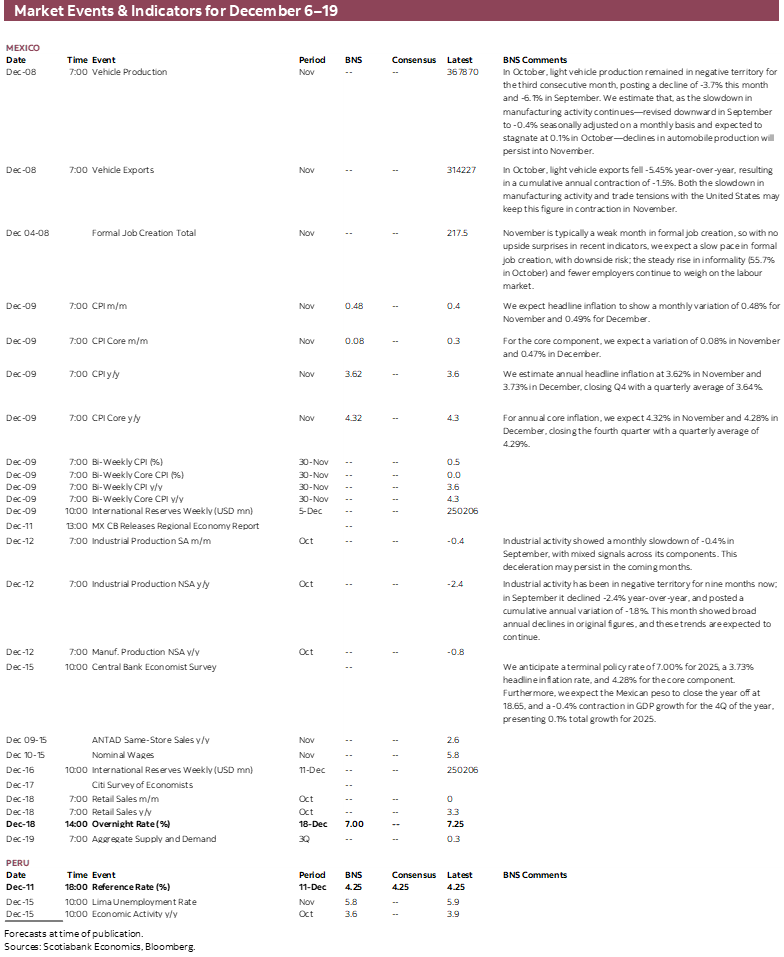

- A comprehensive risk calendar with selected highlights for the period December 6–19 across the Pacific Alliance countries and Brazil.

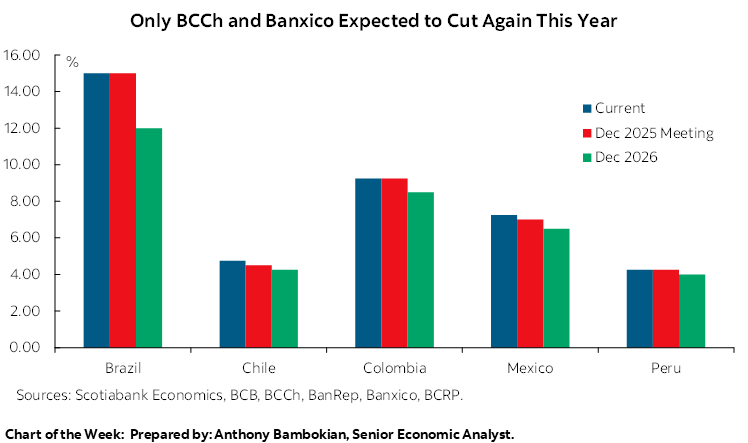

Chart of the Week

ECONOMIC OVERVIEW: REGIONAL CPI, GLOBAL CENTRAL BANKS

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Mexican and Brazilian CPI will influence Banxico and BCB expectations, with markets expecting that the former may only have one cut left in the cycle, while the latter is seen starting its cutting cycle in early-2026—a move that it may tee up at its Wednesday announcement. Developments in Brazilian politics will also be in focus, after former president Jair Bolsonaro backed his son Flavio for the 2026 presidential race shook local markets in recent days.

- We think the BCRP will keep rates on hold at its Thursday decision, but with recent inflation data and falling expectations it would not be terribly surprising that they opt for a cut next week instead of in early-2026, as we expect. Ultimately, it’s a minor adjustment and the timing of it next week or next month is not of major significance.

- The Fed’s expected cut with refreshed projections is the main event next week, with markets also paying close attention to guidance by the BoC, RBA, and SNB with all three expected to hold but the first two facing hike bets in markets while the latter is seen possibly going back to negative rates next year.

The biggest event of what’s left of 2025, Wednesday’s Fed decision seen as near-certain cut, will likely shape the trading mood in global markets until the new year (and in its early innings), but a few key markets will have their own major events on tap to shape sentiment into 2026. In Latam, the BCRP may consider another rate cut at its Thursday meeting, while the BCB may, on Wednesday, lay the groundwork more clearly for a return to easing in early-2026. Each of the BoC, RBA, and SNB should keep rates on hold, but close attention will be paid to guidance as hike speculation builds for the first two, while Swiss officials face slight pressure to consider negative rates.

On the data front, Mexican and Brazilian inflation data for November is the main release in Latam, with the former also having industrial/manufacturing production data and Banxico’s regional economies report on tap, and the latter releasing retail sales and services volumes figures. Chile offers international trade data and the BCCh’s economists and traders survey (which may confirm decent odds of a December cut), while Peru’s and Colombia’s data schedule is bare of anything major. Still, Chilean markets will be looking ahead to Sunday’s runoff vote for the presidency and Colombian traders will track discussions regarding next year’s minimum wage hike. Elsewhere, data highlights include U.S. job openings and international trade, U.K. GDP, Australian employment, and Chinese international trade.

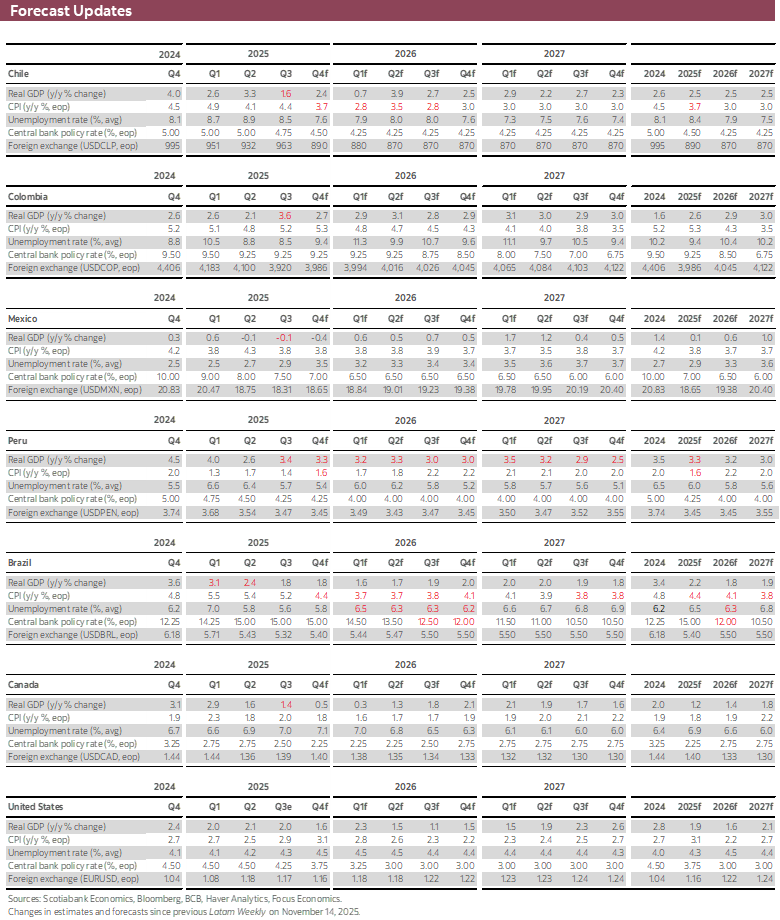

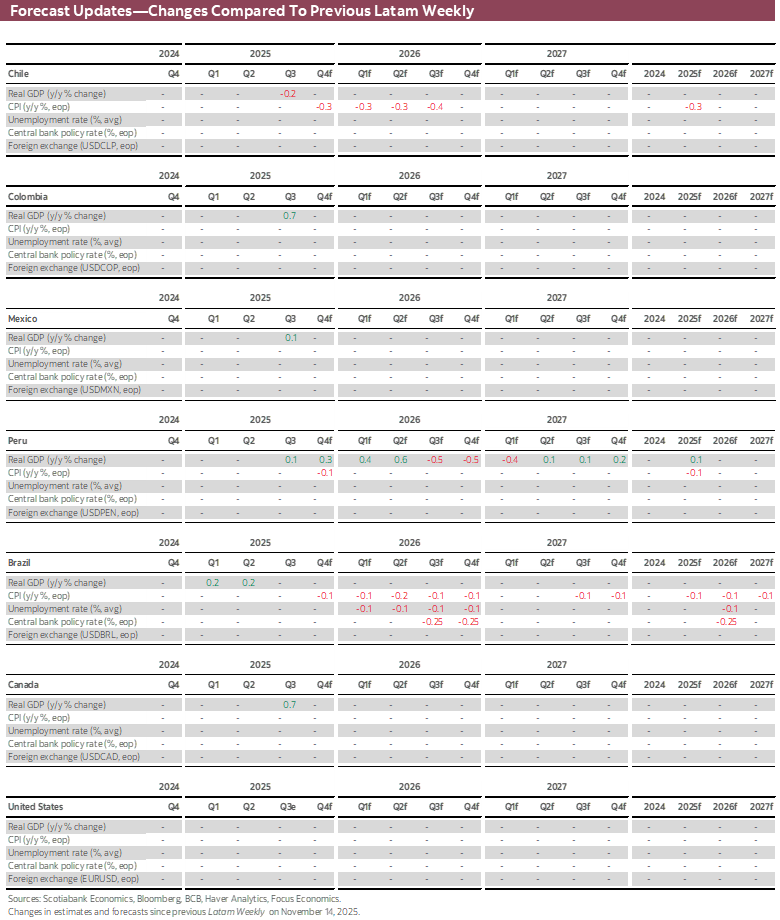

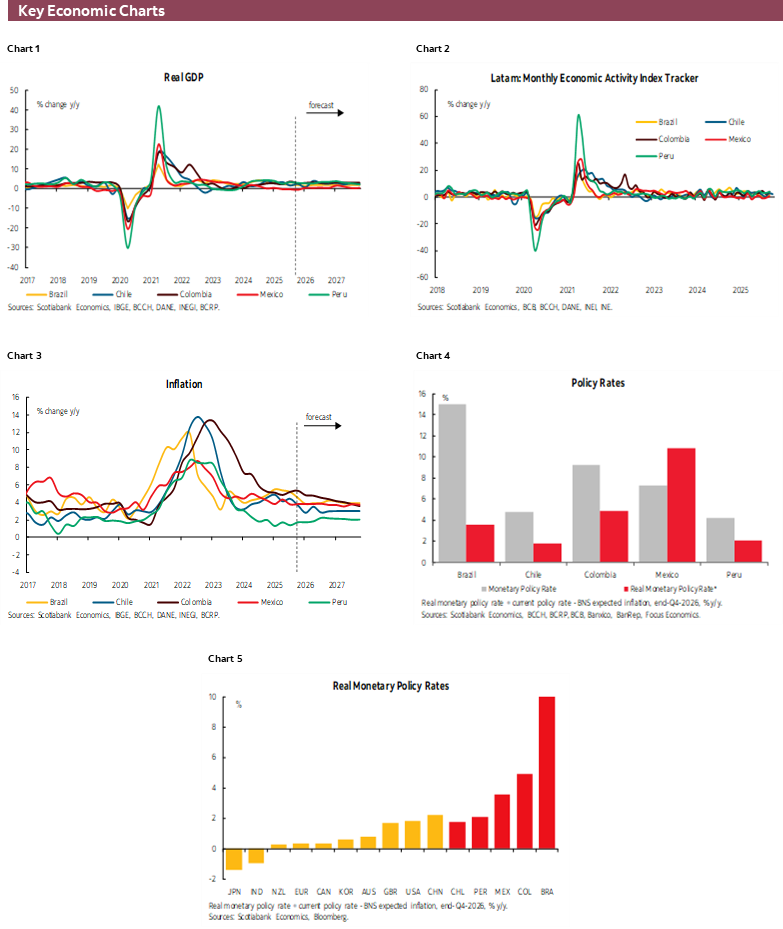

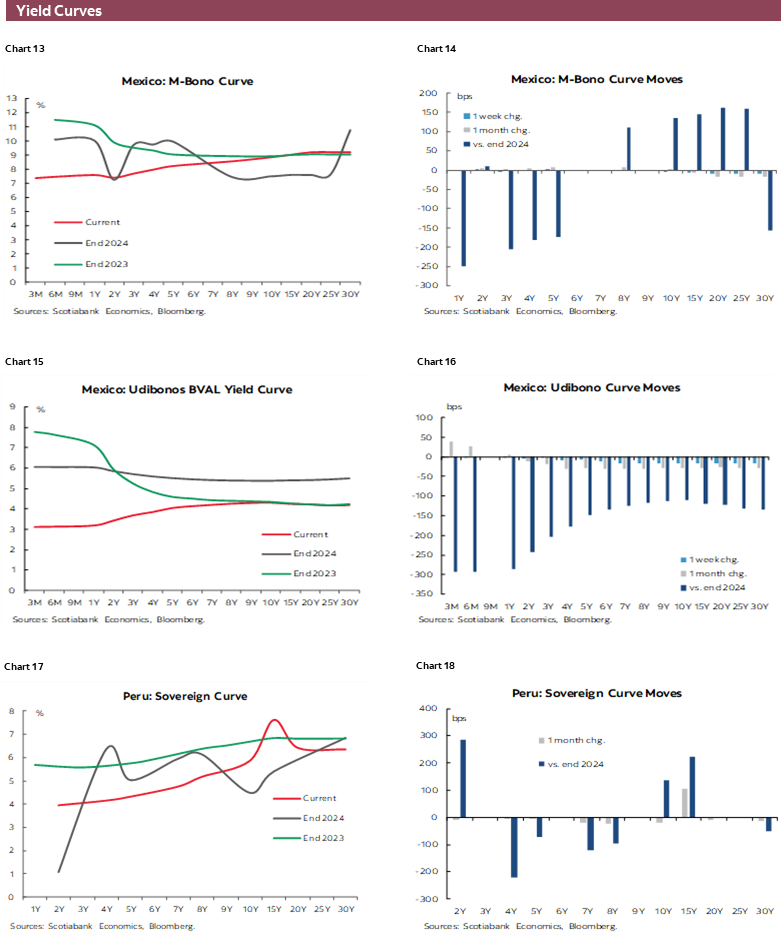

As always, the bar for a surprise is high for monthly Mexican inflation data since we already have mid-month data at hand. In the first half of November, Mexican CPI rose by 3.6% and 4.3% y/y in headline and core terms, respectively, with full-month readings due next week expected to come in slightly higher as base effects compound for the full period alongside pressure in food prices. We don’t expect that Mexican inflation will move all that much throughout 2026 from the 3.8% rate that we project for end-2025, which is a factor that we think requires a more cautious stance on additional rate cuts.

Despite these risks, Banxico guidance tells us that they will still deliver 75bps in easing between now and March 2026. Markets are taking the bet that Banxico will be forced to change its tune, pricing in that they will only cut again this month, sticking to a lengthy pause before they possibly consider rate hikes. The Fed’s decision will accompany Mexican CPI data in shaping expectations for Banxico policy, although it’s important to highlight that a new Fed Chairman taking over Powell in May 2026 means the U.S.’s central bank stance could be significantly more dovish than what may be reflected in next week’s communications. As for Banxico’s regional economies report, our attention will be on how the country’s manufacturing hubs are faring amid U.S. tariffs and trade tensions, and how issues such as crime or power supply may be impacting the broader economy. Note that Mexican markets are closed on Friday.

In Brazil, inflation is seen slowing from 4.7% to around the mid-4s in line with the IPCA-15 slowdown from 4.9% to 4.5%, thus within the BCB’s tolerance range of 3+/-1.5%. That same afternoon, the BCB will announce a widely expected rate hold, but the within-target print would help it deliver a message that tees up the start of rate cuts at some point in 1Q26. Markets are currently assigning about 70% odds to a quarter-point reduction in January, with expected cuts totalling ~250bps by end-2026. This is about 25bps less than what markets expected at last Friday’s close, as Brazilian yields were pressured higher this week on talk that former President Bolsonaro would support his son Flavio in next year’s elections.

Today, after rumours swirled all morning long, Flavio confirmed that his father entrusted him with “continuing our national project.” We will now have to see whether Flavio will fully aim to be Lula’s main opposition, or whether the Bolsonaros want to strengthen their position among the political right in the country. Markets will be hoping it’s the latter rather than the former, with the Ibovespa equity index dropping over 3% today as Lula has a strong chance of defeating Flavio in the October 2026 vote, impacting the market’s hopes of a more market-friendly administration. We will watch what Tarcisio de Freitas, governor of Sao Paulo, the market’s preferred option, and the best performer in head-to-head polls against Lula has to say about the latest developments.

BCRP decisions have a recent history of being tough to call, but our expectation for Thursday’s announcement is that Peru’s central bank will opt for a rate hold. Data published earlier this week showed inflation slowed to 1.2% in November from 1.3% and while we expect an acceleration in December, headline inflation may still only close the year in the mid-1s. Falling actual and expected inflation (as per the BCRP’s survey) have given the bank room to cut by an additional 25bps without impacting its neutral stance. It may come next week, or in early-2026, but ultimately this small tweak should not be massively impactful for macroeconomic outcomes. Next year’s election is of greater relevance, but good luck getting a good sense of who will be the top contenders for the April vote (June second round).

| LOCAL MARKET COVERAGE | ||

| CHILE | ||

| Website: | Click here to be redirected | |

| Subscribe: | anibal.alarcon@scotiabank.cl | |

| Coverage: | Spanish and English | |

| MEXICO | ||

| Website: | Click here to be redirected | |

| Subscribe: | estudeco@scotiacb.com.mx | |

| Coverage: | Spanish | |

| PERU | ||

| Website: | Click here to be redirected | |

| Subscribe: | siee@scotiabank.com.pe | |

| Coverage: | Spanish | |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.