- Colombian, Chilean, and Peruvian CPI await next week, with Colombia’s influencing minimum wage negotiations, Chile’s shaping BCCh December meeting expectations, and Peru’s again below 2% keeping a rate cut on the table.

- Mexican remittances, investment, and formal employment data will likely remain weak, while Brazil’s economy is estimated to have decelerated in 3Q.

- In today’s report, the team in Colombia go over recent developments in sovereign debt markets, our economists in Mexico discuss 3Q’s record (with caveats) FDI figures, and our team in Peru preview next week’s CPI release and go over macroeconomic indicators for October pointing to another solid GDP month.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Colombia, Mexico and Peru.

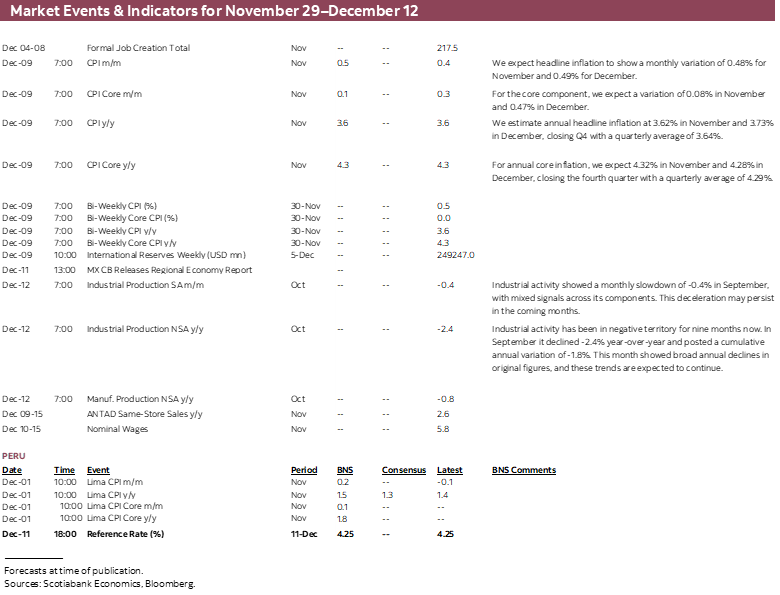

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period November 29–December 12 across the Pacific Alliance countries and Brazil.

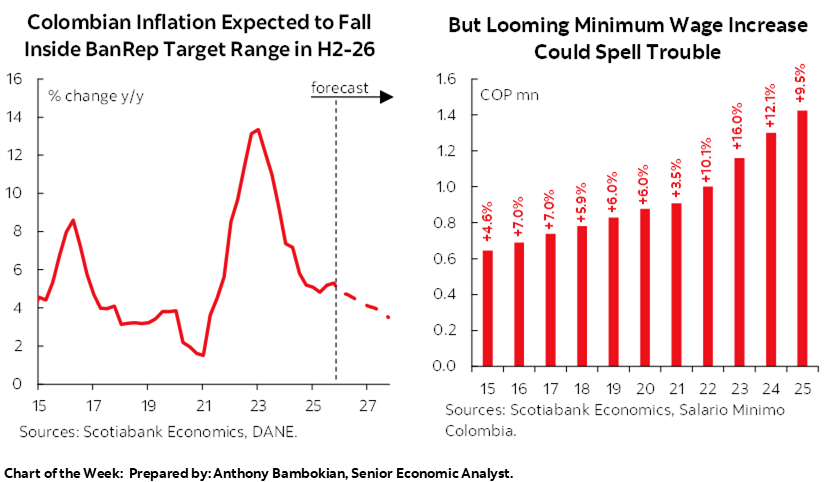

Chart of the Week

ECONOMIC OVERVIEW: CPI TRIO, MEXICO MACRO, BRAZIL GDP

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Colombian, Chilean, and Peruvian CPI await next week, with Colombia’s influencing minimum wage negotiations, Chile’s shaping BCCh December meeting expectations, and Peru’s again below 2% keeping a rate cut on the table.

- Mexican remittances, investment, and formal employment data will likely remain weak, while Brazil’s economy is estimated to have decelerated in 3Q.

- In today’s report, the team in Colombia go over recent developments in sovereign debt markets, our economists in Mexico discuss 3Q’s record (with caveats) FDI figures, and our team in Peru preview next week’s CPI release and go over macroeconomic indicators for October pointing to another solid GDP month.

There is plenty on tap next week to keep economists and markets busy across Latam and the G10 ahead of the final round of central bank decisions of the year clustered during the second and third weeks of the month. All four Andean countries, Colombia, Peru, Chile, and Bolivia (which we don’t cover) publish CPI data for November next week, Mexico releases key data on remittances, investment, and employment, and Brazil releases 3Q GDP data.

From the U.S., we’ll get ISM surveys, ADP employment, stale PCE readings, and the U Michigan consumer survey results. Elsewhere, Canadian labour market data, Chinese official PMIs, Eurozone-wide inflation data, and Australian GDP are the highlight, while we also keep an eye on Russia-Ukraine peace talk developments and OPEC+’s final meeting of the year this weekend.

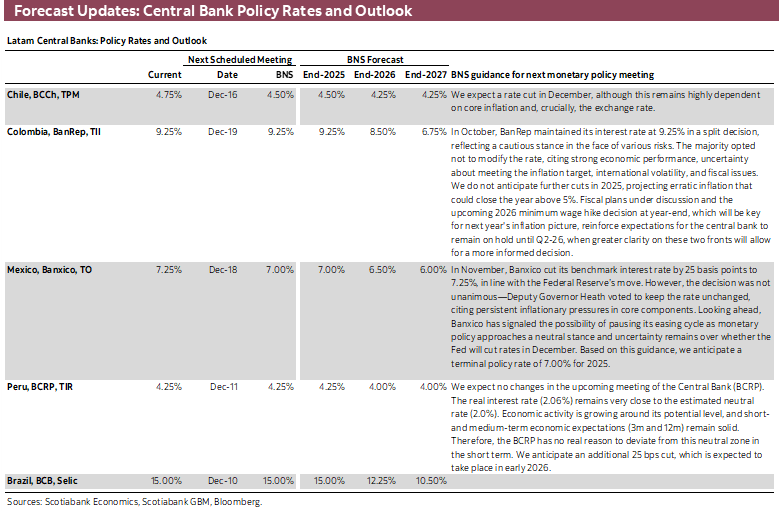

Colombia’s CPI release on Friday likely represents the greatest risk event for its domestic markets—although its 18ET release time means traders won’t be able to materially act on it until the following Tuesday, with holidays on the 8th. Economists and policymakers will surely have a lot to think upon the release of the figures given their importance for 2026 minimum wage negotiations. Headline inflation is expected relatively unchanged from October’s rise of ~5.5% y/y, with core prices growth holding similarly steady at 5.2%.

An overshoot in next week’s figures could stoke growing odds or market expectations that BanRep could not only not cut in the near term but instead choose to tighten policy (a view that we do not currently share). Comments by BanRep board members have added fuel to this fire. Taboada said last week that rate stability has perhaps not been sufficient to control inflation, and Villamizar said on Friday that a rate hike is on the table were a few key risks to materialise among a large minimum wage hike, a reversal of COP strength, a wider fiscal deficit, and higher natural gas prices.

With government officials suggesting that Colombians will be pleasantly surprised by next year’s minimum wage hike (with an eye on next year’s elections) likely in the double digits, the first condition may be met. A higher-than-expected inflation print next week would bolster the government’s case as discussions get going in the next couple of weeks ahead of the first legal deadline of December 15th to decide on next year’s hike.

On the fiscal front, our team in Colombia discuss recent developments in sovereign debt, shaken up by BanRep rate expectations and the Treasury’s reduced activity in markets which had previously helped Colombia yields lower. The MinFin has had to extend issuance in the latter part of December—last seen in 2020 and 2021—to cover its financial requirements. Meanwhile, the country unveiled another EUR-denominated issuance last week with €2bn on offer receiving over €7bn in offers, with the proceeds flipped to repurchase deeply-discounted external debt.

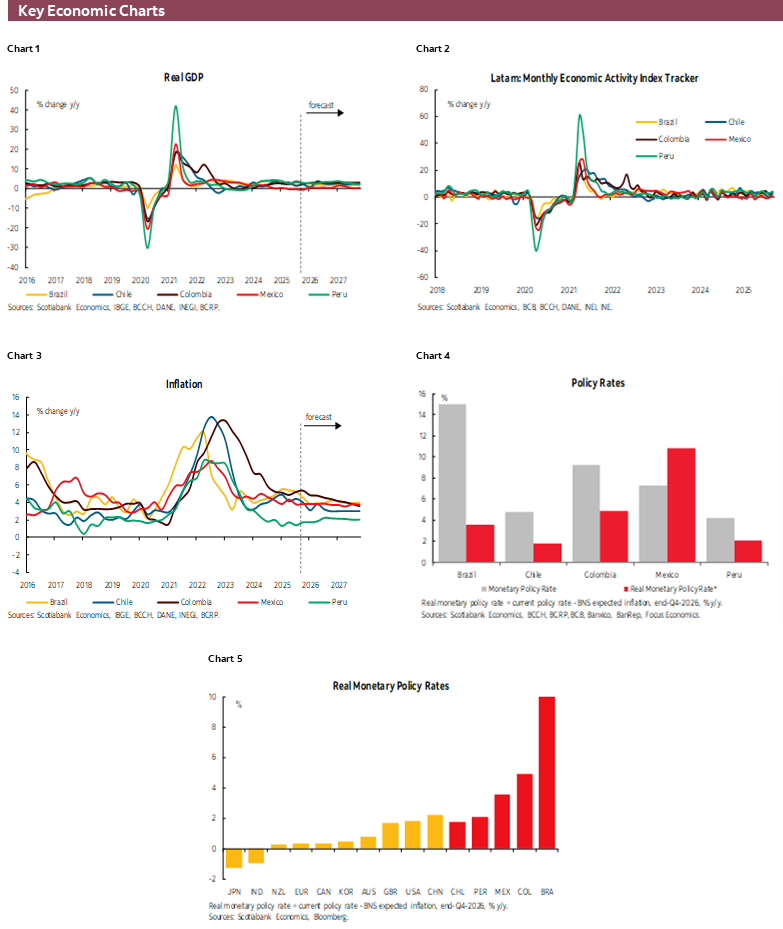

Peru will be first out the gate with CPI data on Monday, with the 1.45% y/y print that our team projects representing a completely different picture of inflation than in Colombia. This marginal acceleration from 1.35% y/y in October would extend the streak of sub-2% inflation prints in Peru to twelve months or 18 of the past 19 months. This isn’t only a huge feat for Peru in comparison to its Latam peers, but in comparison to most countries around the world (the Fed wishes it had sub-2% inflation for such a long time). With that, the BCRP could mull another rate cut in coming months.

In today’s weekly, our economists in Lima go over their expectations for Monday’s data and also cover recent macroeconomic and credit figures that continue to reflect economic resilience. Industry-level indicators for October suggest conditions remained as firm as in September, with auto sales growing at a double-digit click and lending to the business sector extending its uptrend. Pending possible economic disruptions ahead of the April 2026 elections, Peru’s economy remains well on track to meet our expectations for 3%+ growth this year and next.

Chilean CPI is also seen little changed around the mid-3s in next Friday’s release, with a roughly on-consensus print likely giving the green light to the BCCh to cut at its December 16th rate decision. Our colleagues in the country see some upside risks in next week’s release, with their 3.6% y/y forecast above the Bloomberg median’s 3.4% call, but it will be important to see whether it is non-volatile prices that drive the acceleration from 3.5% in October (we think food prices will play an important role here). The BCCh’s policy announcement is scheduled for only a couple of days after the presidential runoff vote, but Kast’s sizable lead over Jara is teeing up an unsurprising result (or one that would influence the bank’s decision).

Chile also starts the week with October economic activity data expected to show 1.9% y/y growth, slowing from the 3.2% y/y expansion in September. Friday’s macro data run was mixed, as retail sales surged 8.4% y/y after an already strong 6.5% rise in September, but industrial production surprisingly contracted with manufacturing having its worst month February. Excluding mining, our team estimates that Chile’s economy expanded by a solid 2.7% y/y in October.

Turning to Mexico, next week’s local data releases are not usually first tier, but are nevertheless all in the spotlight. Monday’s remittances data for October will likely show another decline, although likely continuing its trend of smaller contractions to possibly sit close to flat on a y/y basis; rather than improving flows, the fall in remittances has now possibly stalled. Thursday’s formal employment numbers may continue the uptrend in y/y figures that began around mid-year, but the root of the recovery being the reclassification of gig workers to formal employment leaves a lot to be desired from a mere 0.8% y/y rise in October; last month, manufacturing headcounts fell 2% y/y.

On Wednesday, fixed investment is seen contracting again in September, though ‘improving’ from a 10% y/y contraction in August. Investment trends are the focus of our team in today’s Weekly, as our economists go over the latest foreign direct investment data for 3Q. FDI reached a record last quarter, but the details behind this historic development are less encouraging than the headline figures suggest, with reinvestment flows accounting for over two-thirds of FDI. These data also stand in contrast to aggregate investment in the country, which remains significantly depressed as domestic players take a cautious stance.

Finally, Brazilian GDP is seen decelerating in year-on-year and quarter-on-quarter terms in 3Q data released on Thursday. After a 2.2% y/y expansion in 2Q, economists believe Brazilian growth may have slowed to as low as the mid-2s; the Bloomberg median forecast is 1.7% but 10 of 18 economists project a weaker print. The services sector is expected to lead the charge against some weakness in the primary sector. The slowdown may support expectations for BCB rate cuts, with markets eyeing the first one at the January meeting (~20bps priced in).

There were some rumblings on the electoral front this week, with Sao Paulo governor Tarcisio do Freitas, the market’s seemingly preferred option to lead the right in next year’s vote, saying that the right’s candidate should be announced in early-2026. According to Tarcisio, anxious financial markets need calm, and that “change next year means that a team that knows exactly what to do will come in.” Keep an eye out for comments from those ‘in-the-know’ about whom former President Bolsonaro intends to back for next year’s vote. Tarcisio may be the market’s favourite but it’s unclear whether he’s Bolsonaro’s favourite, and the latter’s support is practically a necessity to beat out Lula next year.

PACIFIC ALLIANCE COUNTRY UPDATES

Colombia—Fiscal Risk Premium Is Back in Focus

Jackeline Piraján, Head Economist, Colombia

+57.601.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Valentina Guio, Senior Economist

+57.601.745.6300 Ext. 9166 (Colombia)

daniela.guio@scotiabank.com

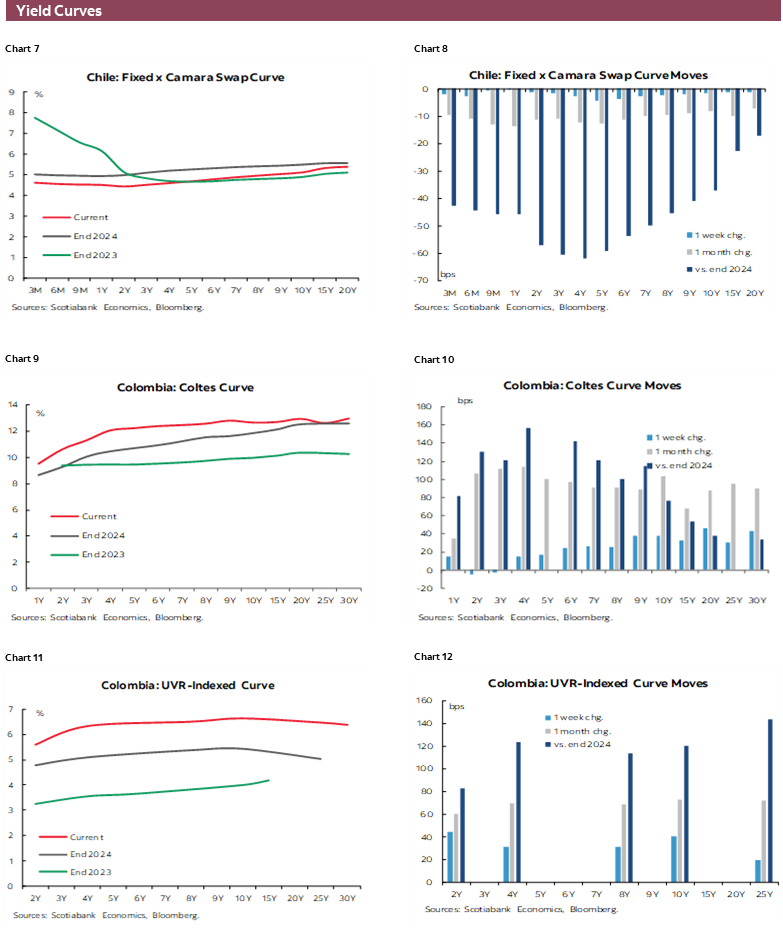

Year-to-date, the Public Credit Direction office has executed seven domestic debt management operations with market makers and two external debt management transactions. These, alongside the structuring of the TRS with six international banks, were probably the stronger fundamentals behind the appreciation in the public debt and FX market (see our thoughts here). However, in recent weeks, volatility increased in the context of concerns over potential interest rate hikes by the Central Bank, combined with some signals that shine again the spotlight on the country’s fiscal challenges, with weakness in sovereign debt, threatening to offset the gains achieved so far post the 2025 Medium Term Fiscal Framework.

Domestic Debt: Chronicle of a Foretold Depreciation

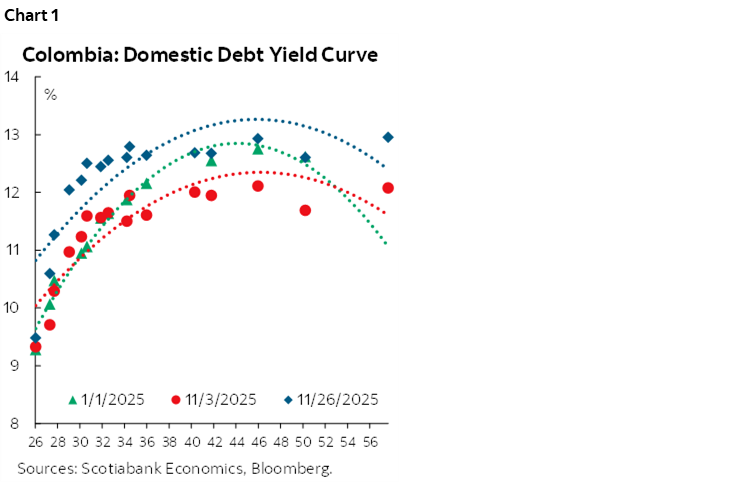

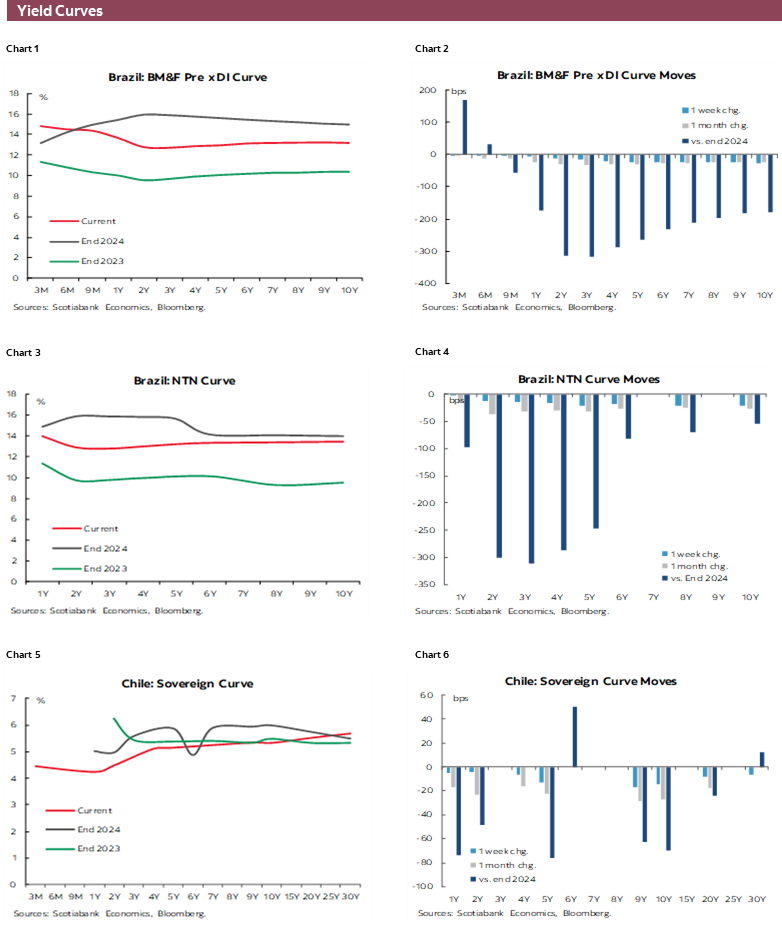

The recent weakening of the local debt curve reflects the market’s underlying concerns. Last week, the curve experienced significant flattening, with an average cheapening of 24 bps, as the short end jumped by 35 bps amid expectations of a new interest rate hike cycle by the BanRep (see here). Meanwhile, the long end jumped by 20 bps, as Treasury reduced its activity in purchases of deeply discounted securities, a factor that had previously supported appreciation at longer maturities (chart 1). Month-to-date, the curve has already posted an average loss of 80 bps, a trend that risks becoming permanent amid subdued investor appetite and a scaled-back capacity of the Ministry of Finance to be a net buyer.

Contrary to mid-year guidance, Public Credit Direction is now doing carrying out debt management operations. The high concentration of one-year bonds (TCOs), which represents 20.6% of total outstanding, and upcoming maturities have prompted internal swaps. Between October 20th and November 14th, there were seven debt swaps reducing short-term bonds outstanding by COP 13 tn, including COP 2.7 tn in an operation with the Treasury. In turn, long-term fixed-rate bonds maturing in 2035, 2040, 2046, and 2058 were issued, several through off-auction mechanisms. Additionally, Public Credit is estimated to have directly issued COP 8.3 tn in TCOs during the third week of November. Initial hypotheses suggest these resources were used to finance part of the USD 4 bn external bond buyback executed in the last week of November, although we cannot rule out their use to rebuild the COP 21.6 tn collateral posted for the TRS following the recent depreciation of those securities.

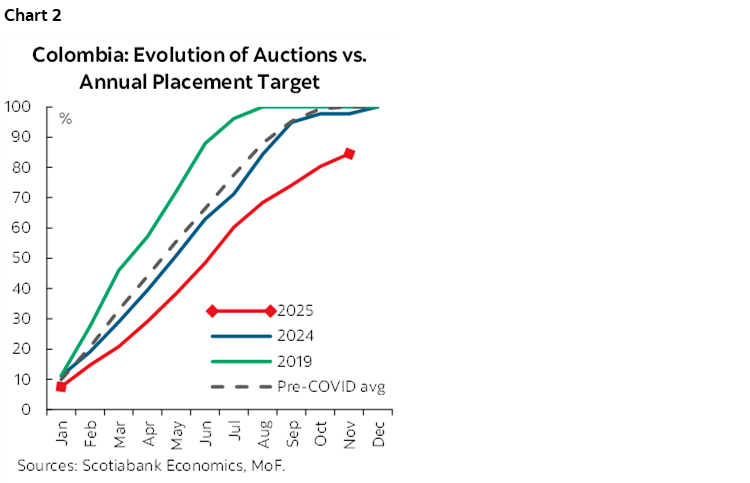

This context highlights liquidity constraints faced by the Ministry of Finance. As of November 19th, long-term COLTES auctions accounted for over 86% of the new target set by Public Credit (COP 67.3 tn vs. COP 58 tn under 2025 MFMP), leaving over COP 9 tn to be auctioned before year-end. This implies weekly auctions of at least COP 1.8 tn—above typical weekly allocations. In Colombia, the last time the long-term auction calendar was extended through year-end (excluding green bonds) was in 2020 during the pandemic and again in 2021 (chart 2).

External Debt: A New Euro Curve Emerges as Multilateral Loans are Again on the Table

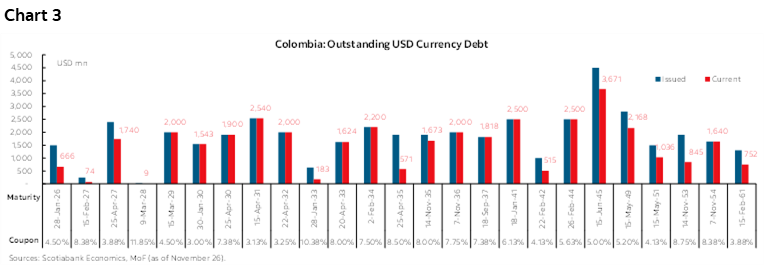

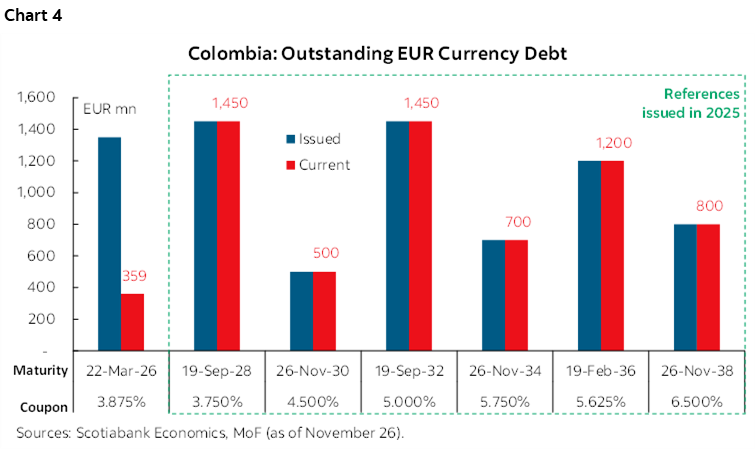

Colombia continues to advance its external debt management strategy. Last week, Public Credit announced a new euro-denominated issuance totaling EUR 2 billion, with maturities in 2030 (4.50% coupon), 2034 (5.75%), and 2038 (6.50%), attracting demand of over EUR 7 billion. The proceeds, combined with Treasury cash, were used to repurchase global bonds in various denominations, amounting to USD 4 billion, across maturities in EUR 2026 (USD 317 million), COP 2027 (USD 421 million), and USD 2033 (USD 157 million), 2035 (USD 1,548 million), and 2053 (USD 1,054 million) (chart 3).

With this transaction, year-to-date, Public Credit has completed two external debt management operations, totaling approximately USD 7 bn in repurchases of deeply discounted bonds, reducing outstanding external debt and establishing a new euro yield curve (chart 4). It is worth noting that demand for this second operation was significantly weaker compared to the first, a factor to consider given that Public Credit has congressional authorization to issue up to EUR 4.3 bn and still plans to tap the European market to finance the 2026 budget.

Multilateral loans are not out of the picture. In October, the national government reportedly secured USD 2 bn in loans from development and multilateral institutions, covering nearly 100% of the 2025 target for multilateral borrowing, which was revised down from USD 4.55 bn to USD 2.05 bn. These inflows are likely to explain the increase in the Ministry of Finance’s dollar cash position, which closed at approximately USD 3.83 bn in October despite USD 4.2 bn in monetizations recorded between September and October.

Next year will be heavy for maturing debt and interest payments. According to Scotiabank Colpatria’s estimates, payments on TCOs and COLTES in 2026 could reach COP 87 tn, with maturities alone totaling COP 41 tn—COP 30 tn of which are TCOs. It is worth noting, TCO maturities of COP 21.6 tn in August 2026 are excluded from this estimate, as they correspond to contingent liabilities from the Total Return Swap with foreign banks and would be extinguished upon closing the operation. External debt payments—considering only dollar- and euro-denominated bonds—are estimated at USD 3.37 bn (COP 12.8 tn). These sizable maturities justify continued debt management operations to smooth near-term obligations in both domestic and external markets; however, the purpose probably won’t be focusing in fiscal efficiencies, but in managing liquidity constraints.

Mexico—Record-High FDI (With Caveats)

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

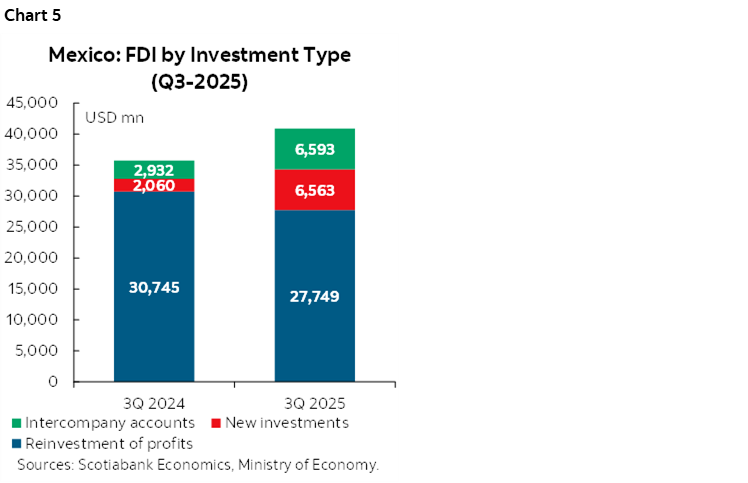

Last week, the Ministry of Economy and Banxico released Foreign Direct Investment (FDI) figures for the third quarter of 2025. So far this year, Mexico has received $40.9 billion, representing a 14.5% increase compared to the cumulative amount for the first three quarters of 2024. While this figure marks an all-time high, it is important to provide context: part of the increase is due to profit reinvestment and, to a lesser extent, the global trend of supply chain relocation, rather than an internal structural change. The challenge will be to sustain this pace amid an uncertain international environment and domestic infrastructure and security issues.

Breaking down by type of investment (chart 5), profit reinvestment remains the most significant component, accounting for 68% of the total, equivalent to $27.8 billion. Although this share is lower than in the same period last year (86%), the data indicates that foreign companies established in Mexico continue to trust the local market. Meanwhile, new investments and intercompany accounts nearly tripled, reaching $6.56 billion and $6.59 billion respectively, each representing a 16% share.

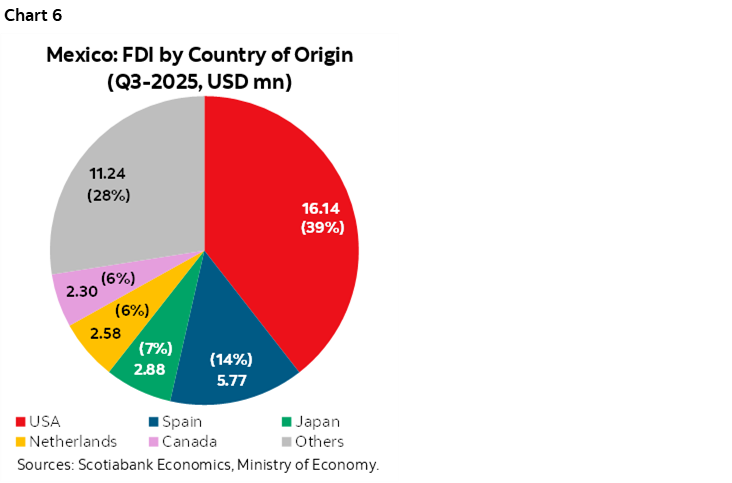

Regarding the origin of FDI (chart 6), the United States remains the main investor with nearly 40% participation, followed by Spain (14.09%), Japan (7.05%), the Netherlands (6.31%), and Canada (5.61%). This concentration reflects dependence on the USMCA framework, which provides certainty but also exposes Mexico to risks from trade tensions or changes in U.S. policies.

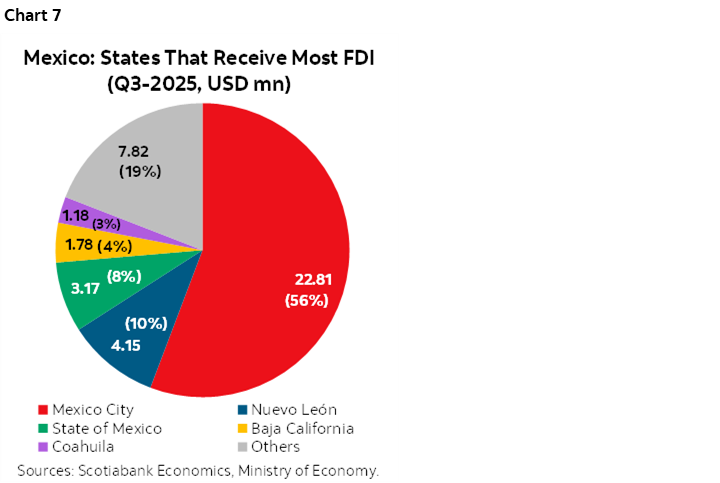

By state (chart 7), Mexico City accounts for 55% of FDI, while no other state exceeds 10%, with Nuevo León, Estado de México, Baja California, and Coahuila standing out. This pattern shows a high concentration of investment in the capital, driven by corporate headquarters and financial services, although the participation of industrial states highlights the strengthening of manufacturing.

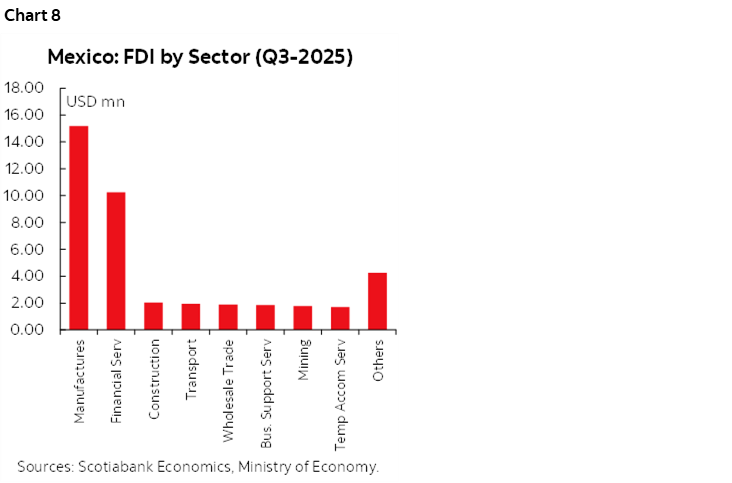

By sector (chart 8), manufacturing and financial services lead FDI inflows, with 15% and 10% respectively.

Although foreign direct investment in Mexico shows a significant rebound, driven by profit reinvestment and new projects linked to nearshoring, this momentum contrasts with the decline in total investment, which has fallen 6.8% so far this year. Since FDI represents only 17% of total investment, its growth does not offset the weakness of domestic investment, affected by regulatory uncertainty and institutional risks. Without a recovery in domestic investment, Mexico’s economic growth potential will remain limited, despite its attractiveness to foreign capital.

Peru—Economic Performance Maintains a Solid Pace Amid a Calm Electoral Landscape—At Least For Now

Ricardo Avila, Senior Analyst

ricardo.avila@scotiabank.com.pe

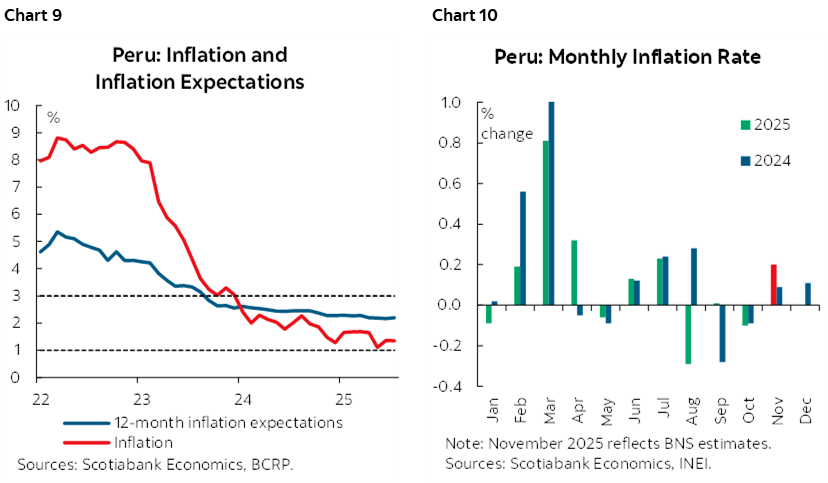

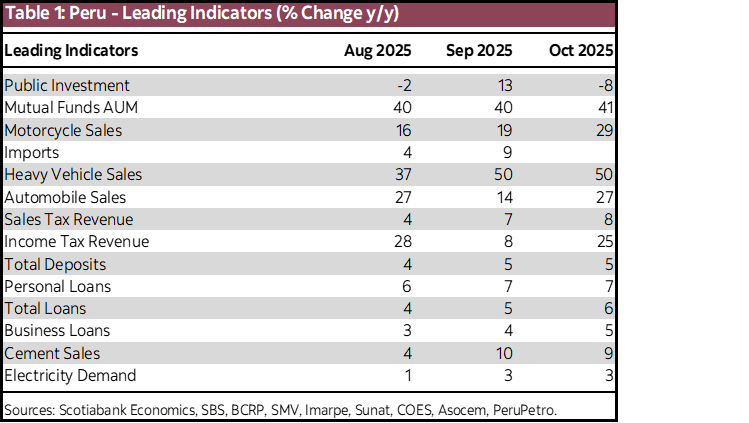

If you are reading this on Monday, you likely already know the inflation figure. The key price indicators we monitor point to a positive monthly headline inflation rate of 0.2% for November, slightly higher than the figure recorded in November 2024, when inflation stood at +0.09% MoM. As a result, annual inflation would rise slightly from 1.35% in October to around 1.45% in November. On the other hand, core inflation would also be positive, increasing by 0.1% MoM in November. As a result, the annual figure would remain around 1.8% (charts 9 and 10).

We anticipate an additional boost to headline inflation in December, considering the withdrawal of AFP funds and the fact that the monthly figure for December 2024 was only 0.11%, an atypical result and the lowest for a December since 2006. With this, inflation would approach the 1.7% we estimate for year-end.

Low inflation reinforces our expectation that the BCRP will reduce the policy rate once more, to 4.0% at some point during the early months of 2026. With inflation expectations currently at 2.19%, the real interest rate stands at 2.06%, close to the neutral rate of 2.0%. We believe that an additional cut would still keep the Central Bank within a neutral zone. We do not expect further reductions that would bring the policy rate below 4.00%. There is no justification for lowering the interest rate below its neutral range, as economic growth is performing well, hovering around its potential level.

Meanwhile the economy continues cruising along at a moderate clip. Our key indicators for October are very similar to those in September (table 1), with the exception of public investment, which typically exhibits a significant degree of volatility. Our key indicators for October are more aligned with non-resource sectors (linked to domestic demand), which grew at a more moderate 4.0%, YoY, in September. Thus, we expect non-resource sectors to rise around 4.0% in October, once again.

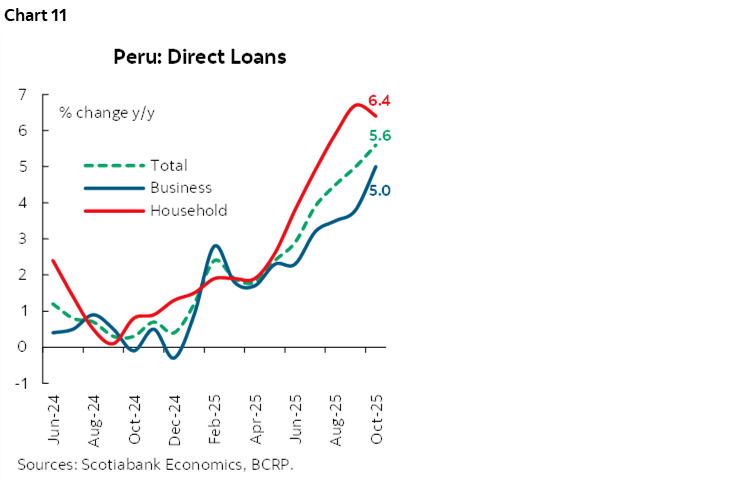

Finally, last Thursday, the Central Bank released data on direct loans to the private sector, which continued to accelerate, posting annual growth of 5.6% in October (chart 11).

On the business side, linked to private investment, loans maintains a strong upward trend, reaching 5.0% YoY, driven by wholesale loans. However, due to a base effect, it is expected to stabilize toward year-end. On the household side, associated with private consumption, loans continues to show solid dynamics, growing 6.4% annually, reflecting consumer strength both in consumer loans and in mortgage loans, which remains robust with improving flows each month. We also anticipate a moderation in household loans over the coming months—until approximately January—due to amortizations resulting from AFP fund withdrawals.

We continue to believe that the loans market will maintain a solid pace throughout 2026. Loans growth is expected to be around 5.0%, which represents goods performance considering the high base of 2025.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.