ECONOMIC OVERVIEW

- Key data awaits in Latam and the G10 as markets brace for a two-week festival of central bank announcements. Mexico, Brazil, U.S., U.K., Canada, and Japan CPI, and Global PMIs are on tap, all the while markets pay close attention to [pick a U.S.-related topic that is causing anxiety].

- In today’s report, the team in Colombia discusses the country’s solid economic backdrop against worrying inflation and fiscal policy trends and risks. From Mexico, we discuss the IMF’s updated (rosy) projections for the local economy, while our colleagues in Chile outline their expectations for strong GDP growth in September.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, and Mexico.

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period October 18–31 across the Pacific Alliance countries and Brazil.

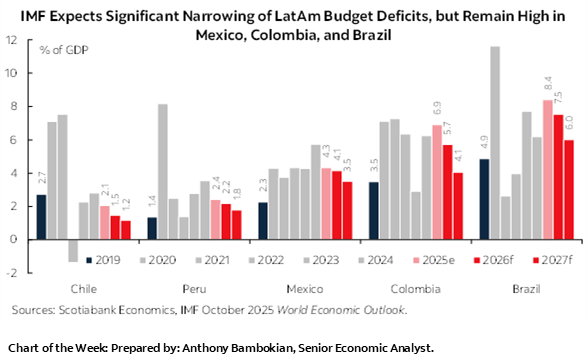

Chart of the Week

ECONOMIC OVERVIEW: MID-MONTH CPI, ECONOMIC ACTIVITY, GLOBAL PMIS

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Key data awaits in Latam and the G10 as markets brace for a two-week festival of central bank announcements. Mexico, Brazil, U.S., U.K., Canada, and Japan CPI, and Global PMIs are on tap, all while markets pay close attention to [pick a U.S.-related topic that is causing anxiety].

- In today’s report, the team in Colombia discusses the country’s solid economic backdrop against worrying inflation and fiscal policy trends and risks. From Mexico, we discuss the IMF’s updated (rosy) projections for the local economy, while our colleagues in Chile outline their expectations for strong GDP growth in September.

U.S. credit cracks, China-U.S. trade tensions, the U.S. government shutdown, and Friday’s release of U.S. CPI (there’s a country pattern) will continue to drive global market sentiment next week alongside company earnings releases and a new round of Global PMIs on Friday. But it’s not just the U.S. that is out with inflation figures next week, as Mexico and Brazil unveil the first set of October CPI readings (mid-month) and Canada, the U.K., and Japan all publish September prints.

Next week’s economic figures will be key towards refining expectations for central bank decisions that will be densely compressed in the two weeks that follow. The BCCh, the Fed, the BoC, the BoJ, the ECB, and BanRep take part in the first round of announcements during the week of the 27th. The RBA, the BCB, Banxico, the BoE, and the Norges Bank deliver their own decisions the week of the 3rd of November.

Mexico’s calendar is the busiest of all next week, with economic activity (IGAE), retail sales, and the latest Citi economists survey results on tap, and on top of H1-Oct CPI data. After contracting by 1.1% y/y in July, economic activity is guided to improve slightly based on INEGI’s early indicator ticking higher from -0.2% in July to 0.2% (magnitudes track poorly, but trends are a rough guide). After a non-seasonally adjusted rise of 0.53% m/m in July, history would point to a m/m decline in August, but even a flat performance for the month would translate into a 0.2% y/y decline in the IGAE figures due on Wednesday.

Economic headwinds remain a key justification for continued rate cuts by Banxico, and behind our expectation for 25bps moves at each of the November and December decisions (in line with market expectations and the economist consensus) despite elevated inflation. Thursday’s H1-Oct CPI data is expected to again show very limited movement in headline and core inflation, seen respectively at ~3.8% and ~4.3% y/y but, again, it’s tough to see the data dissuading Banxico from continued easing, especially with markets convinced that the Fed will cut twice more this year; Friday’s U.S. CPI data may even have a greater impact on Banxico bets than Mexico’s own inflation reading.

In today’s report, our local team recaps the IMF’s latest update to its global macroeconomic projections that included a rosy outlook for Mexico’s economy. The IMF projects that growth will clock in at 1.0% in 2025, rebounding to 1.5% in 2026. For comparison, we project practically no growth this year and only a mild acceleration to a weak expansion of 0.6% next year. The median economist surveyed by Citi, with responses updated next week, is more positive with a 0.5% projection for 2025 followed by 1.3% for 2026.

Colombia kicks off the week with August economic activity growth that we estimate at 2.2%, or around half of July’s 4.3%. The deceleration will mainly owe to calendar effects given one fewer business day in August 2025 than twelve months prior. Calendar effects aside, Colombia’s economy remains in solid shape thanks to firm household demand, as reflected in strength seen in retail sales, which grew 12.4% y/y in August and 18% y/y in July. Imports data due on Tuesday may also reflect consumption trends.

In today’s weekly, our economists in Colombia discuss the country’s economic resilience, where household spending strength stands in contrast to softer results in the manufacturing sector. The team highlights the various drivers behind this strength, like remittances and labour market tailwinds. Alongside the positive demand backdrop, upside inflation risks remain front and centre for BanRep, delaying the resumption of cuts—with even one hawkish member, Villamizar, opening the door to rate hikes, if necessary. The government’s suggested 11% minimum wage hike, if realised, would significantly limit downside room for rates, in turn impacting Colombia’s fiscal trajectory—as the team also discusses today.

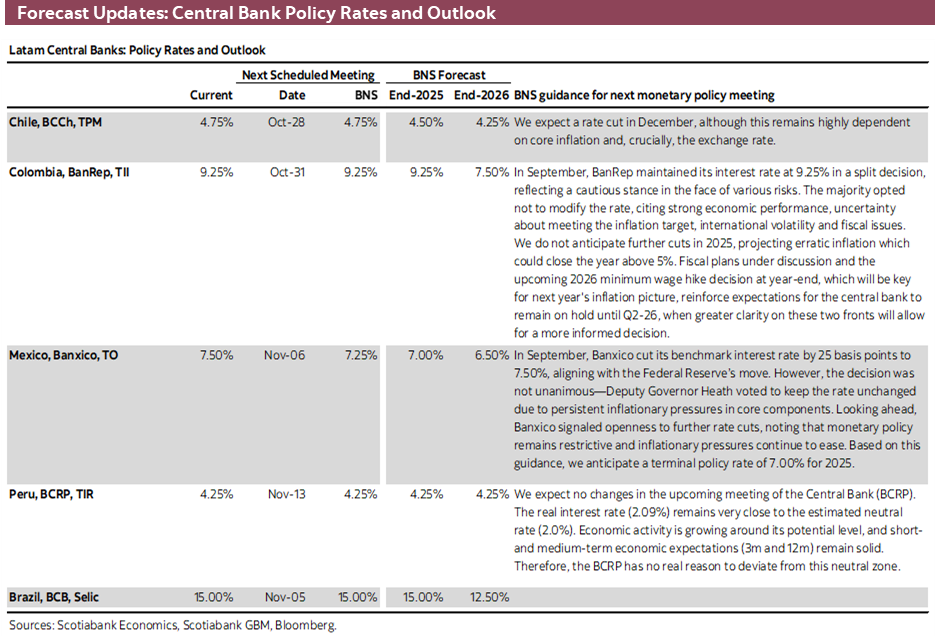

There’s little of note out of Chile next week, but we’ll focus on the results of the BCCh’s economists survey due on Thursday. Recent inflation and output data have chipped away at expectations for Chilean rate cuts to resume in December, after a practically guaranteed rate hold in October just a few days before general elections. At Friday market close, traders were only pencilling in about a 40% chance of a December reduction, instead seeing the next full rate cut at the January announcement.

Our latest published forecast anticipates that the BCCh will opt for a rate cut to 4.50% at the December meeting, though this is highly conditional on core inflation readings due prior to the decision as well as the behaviour of the CLP. As of the latest BCCh economists survey, the median also expects a December rate cut; we’ll see if that has changed. Our economists in Chile go over their estimates for September GDP data scheduled for November 3rd, eyeing a very strong 4.5–5.0% y/y rise in non-mining output thanks to seasonal factors but also reflecting firm economic momentum that may leave the BCCh with limited justification to ease policy again this year.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—Non-Mining GDP Likely Grew 4.5–5.0% y/y in September, Well Above Consensus

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

We project non mining GDP to have expanded between 4.5% and 5.0% y/y in September, with broad-based monthly growth across sectors. Our now-casting models suggest that services, commerce, and manufacturing posted seasonally adjusted gains in September, fully reversing the decline observed in August and pushing non-mining GDP to a new historical high. This performance reflects a combination of favourable base effects, a positive calendar impact, and a genuine recovery in sectoral activity. The release of these data will precede the first round of the presidential election by a couple of weeks.

If confirmed, this result would significantly surprise market expectations, as reflected in the BCCh’s Economic Expectations Survey (non-mining GDP: 2.7% y/y), and could lead to upward revisions in the market’s full-year growth forecasts. At Scotiabank, we reaffirm our full-year GDP growth forecast of 2.5%, which should be seen as a floor.

Overall GDP is expected to have expanded between 3.5% and 4.5% y/y in September, implying Q3 GDP growth of around 2.0% y/y. While this would fall short of the central bank’s scenario (Q3-25 IPoM: 2.5% y/y), the main deviation stems from weaker mining activity, following lower output at the Escondida mine early in the quarter, the partial shutdown of El Teniente in August, and a recent decline in production at Quebrada Blanca (all copper mines).

Seasonal factors played a key role in September, with the calendar effect exceeding historical patterns. Between January and August, the year had two fewer business days than 2024, which will be fully recovered between September and December. In fact, September alone had two additional business days compared to the same month last year, ensuring a reversal of the seasonal adjustment observed in August and contributing roughly one percentage point to the y/y growth in the original series. Additionally, we estimate that seasonally adjusted non-mining GDP expanded between 0.5% and 1.0% m/m, reflecting genuine momentum beyond the calendar effect. This would place annualized quarterly growth of non-mining GDP between 2.3% and 2.9% in Q3.

Non-mining GDP likely reached historically high levels, driven by services, commerce, and manufacturing. Preliminary data confirm that non-mining activity continues to lead the recovery, with services near record highs and robust investment signals in machinery and equipment. Capital goods and intermediate goods imports (machinery parts and components) reached historically high levels for September, positively impacting manufacturing output and wholesale trade. This was further supported by strong new car sales and solid consumer goods imports during the month.

Given this backdrop, the central bank will face limited room to cut the policy rate in October and likely in December as well. The combination of stronger domestic momentum, a policy rate in the “neutral zone,” and inflation risks tied to internal demand constrains the space for further monetary easing. We expect the Board to hold the policy rate steady at its upcoming October 28th meeting, maintaining a cautious stance in its rate-cutting strategy.

Colombia—Resilience Amid Structural Challenges and Policy Uncertainty

Jackeline Piraján, Head Economist, Colombia

+57.601.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Valentina Guio, Senior Economist

+57.601.745.6300 Ext. 9166 (Colombia)

daniela.guio@scotiabank.com

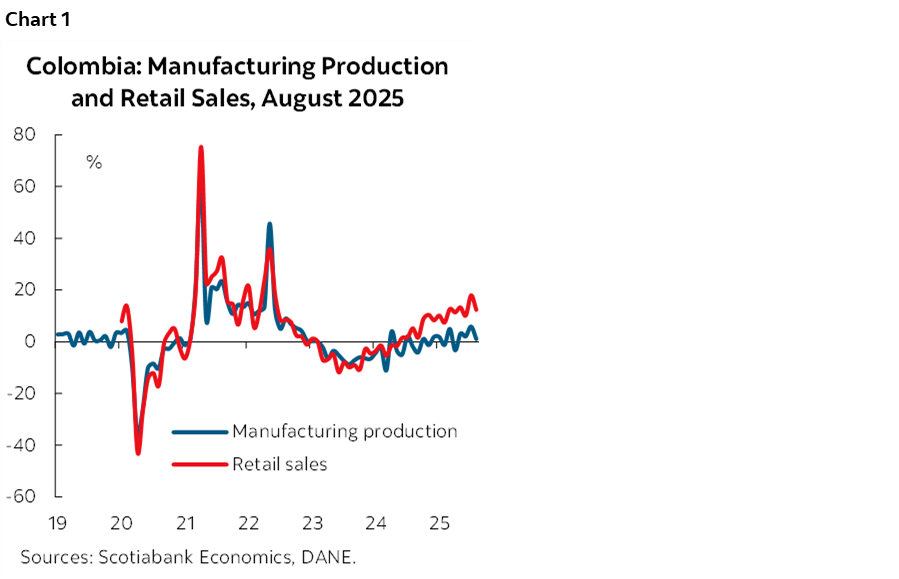

Recent economic activity data shows resiliency. In August, retail sales increased by 12.4% y/y, with 18 out of 19 merchandise groups showing growth. This performance was driven by telecommunication equipment (+51.0% y/y), vehicles (+27.5% y/y for household vehicles, +27.8% y/y for other vehicles), and home appliances (+23.1% y/y). The rebound in retail sales takes place in a context of lower exchange rate, which has supported higher consumption of durable and semi-durable goods since prices has been relatively stable. Meanwhile, the manufacturing industry showed a mixed performance, with an average variation of 1.0% y/y, partly affected by a lower number of working days. 22 out of 39 industrial activities recorded positive variations, with notable increases in oil refining (+17% y/y), chemical product manufacturing (+11.7% y/y), and other transport equipment manufacturing (+42% y/y). In contrast, industries linked to fixed investment, such as basic iron industries (-22.7% y/y), among others, continued to show negative variations (chart 1).

Colombia’s economic growth is projected to remain close to its potential level, driven mainly by domestic demand. This expansion is supported by factors such as record remittance inflows (USD 8.6 bn, +13% YTD up to August), improvements in the labour market, reflected in a historically low unemployment rate of 8.6% in August (see here), compared to an average of 11.5%, and the relative stability of the exchange rate. These elements support a projected growth of 2.6% for 2025 and 2.9% for 2026, a period during which the output gap is expected to close, in line with an estimated potential growth rate of 2.9% for that year. However, lagging fixed investment remains a limiting factor for long-term growth. A clear example can be seen in the post-pandemic period, when investment fell by more than 20%, reducing Colombia’s potential GDP by approximately 0.6 ppts, from 3.5% before the pandemic to 2.9% currently.

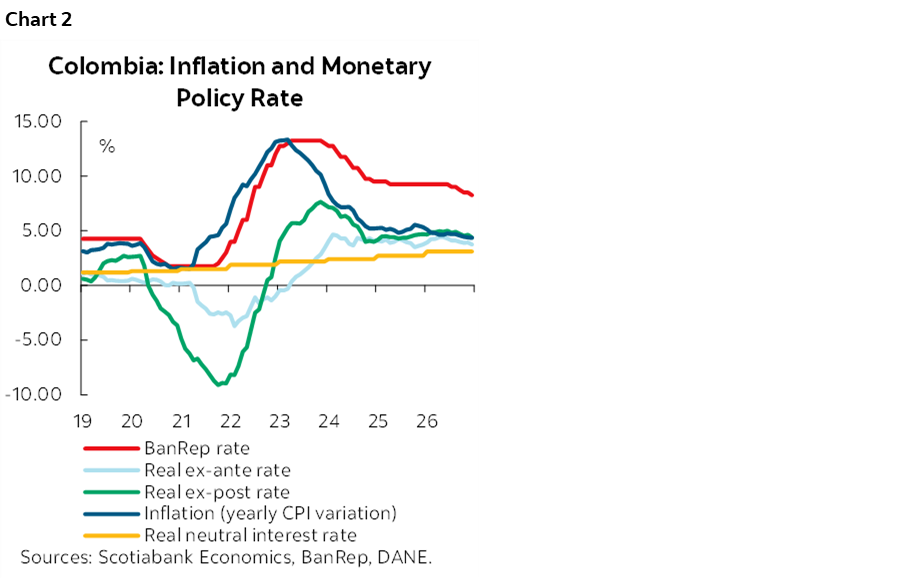

Upside risks in inflation would reduce the room for interest rate cuts. In Colombia, the period for minimum wage negotiations is approaching, during which business associations, labour unions, and the government meet to agree on the nominal increase that directly affects around 2 million employees (9% of the total workforce). The government has suggested an 11% increase for 2026, which, if implemented, would become the highest real increase in the country’s history. This context, combined with the rebound in household consumption, represents upside risks to inflation. As a result, we forecast inflation to close at 5.34% in 2025 (vs. 5.19% y/y in the previous forecast), and 4.34% y/y in 2026 (vs. 3.89% y/y previously). This would significantly reduce the room for interest rate cuts by BanRep, which is expected to remain unchanged at 9.25% by the end of 2025, with cuts resuming only in the second half of 2026, ending the year at 8.25%. This level would remain above the estimated real neutral rate set by the central bank for that period (3.1%) (chart 2).

Fiscal challenges are unlikely to be resolved with the arrival of a new administration.

For 2025, the Government estimates a total fiscal deficit of 7.1% of GDP. According to the Autonomous Fiscal Rule Committee (CARF), without a spending adjustment of COP 8.3 tn, the deficit could even accelerate to 7.6% of GDP. The outlook for 2026 is even more challenging. This week, Congress approved the National Budget for 2026, totaling COP 546.9 tn, which includes a COP 10 tn cut compared to the original proposal submitted by the Government. As a result, the tax reform that the Government will need to reintroduce before Congress would now amount to COP 16.3 tn (approximately 0.87% of GDP), rather than the initially proposed COP 26.3 tn (1.4% of GDP). The original proposal included measures such as health-related taxes and changes to the VAT system (see here).

For 2026, the deficit would remain above 7.0% of GDP if the tax reform is not approved. In addition, the reduction in interest payments resulting from the ambitious Treasury borrowing strategy would translate into an increase in primary spending in 2026, further exacerbating the urgent fiscal situation. This scenario would require structural reforms to public spending, which are unlikely to materialize before the new administration takes office in August 2026.

Regarding the Public Credit Director’s remarks. Director Cuéllar has once again been very vocal about the goal of achieving a debt-to-GDP ratio below 60% through liability management operations. One key strategy involves removing discounted bonds from the market and replacing them with instruments closer to par, thereby lowering the nominal value of the debt. Debt swaps in local currency under the market makers scheme have reduced the nominal debt by approximately COP 16 tn (0.89% of GDP) (see here), adding the FONPET operation the nominal debt reduction reaches 1.2% of GDP and similar actions are expected to continue.

In terms of global bonds, the Public Credit Director highlighted the removal of around USD 3 bn (nominal value) of USD-denominated bonds from the market and subsequently issued EUR 4.1 bn. According to his remarks, this substitution strategy may continue. In fact, the Total Return Swap (TRS) built with six global banks is expected to mature in July 2026. However, the Ministry of Finance’s strategy includes gradually unwinding this operation through the issuance of euro-denominated bonds. However, the goal of reducing interest payments remains the most challenging target. Interest payments are projected to represent 4.7% of GDP in 2025 (according to the MTFF-2026) and 3.8% in 2026 (according to the budget proposal).

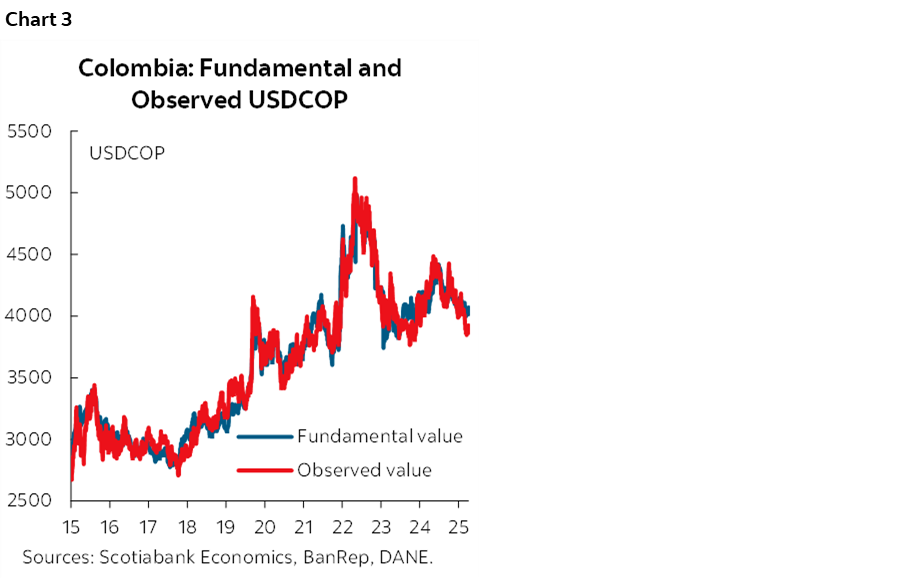

The exchange rate has remained below its fundamental level. So far this year (up to October 15th), the USDCOP has appreciated by 24%, making it the fourth most strengthened currency among emerging markets. While part of this trend can be explained by structural factors such as the global depreciation of the US dollar, record remittance inflows, and widening interest rate differentials, there are also potentially temporary factors at play (see here). Currently, our fundamental model indicates levels above those observed, although we do not rule out that the current trend may persist until mid-2026. For now, we maintain our exchange rate forecast at USDCOP 4,156 by the end of 2025 and USDCOP 4,181 by the end of 2026, with geopolitical conflicts, regional election cycles, and other factors potentially causing further deviations from the fundamental value of the dollar (chart 3).

Mexico—IMF; Global Economic Slowdown: Short- and Medium-Term Growth Risks

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Special Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

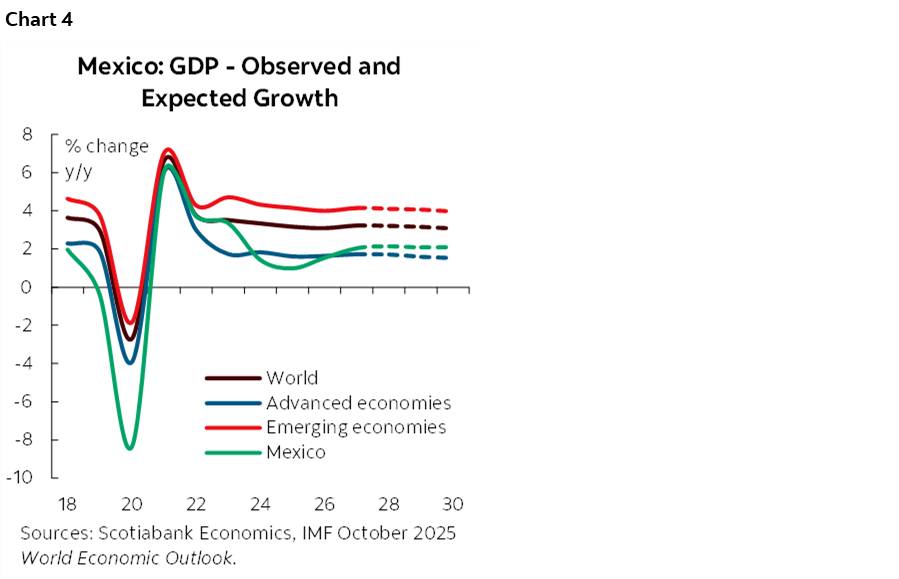

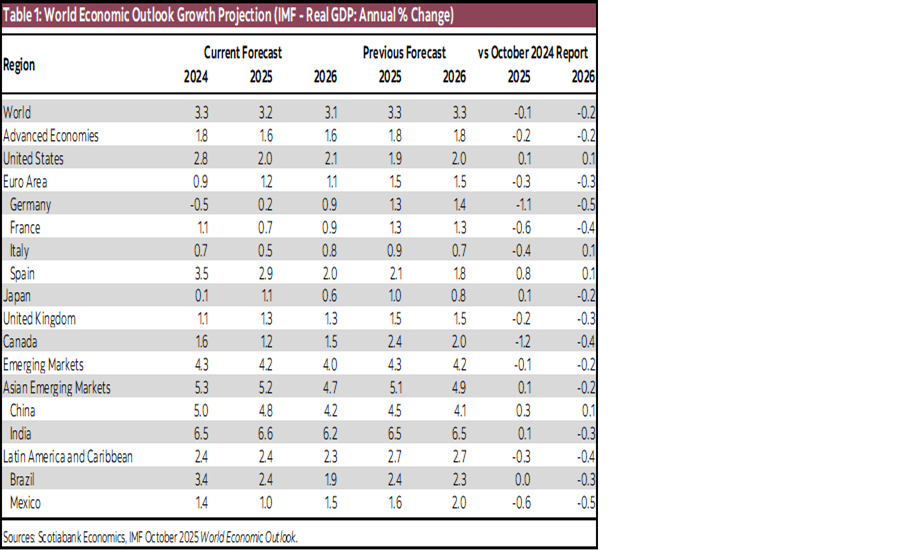

Last Tuesday, the International Monetary Fund (IMF) released its World Economic Outlook (WEO). The report highlights that the global economy is undergoing a period of high uncertainty and fragmentation, marked by shifts toward more protectionist trade policies, migration restrictions, and cuts in international aid. Although global growth showed resilience at the beginning of 2025, a moderate slowdown is expected, with growth projections declining from 3.3% in 2024 to 3.2% in 2025 and 3.1% in 2026. A similar trend is anticipated for advanced economies, with growth adjusted downward from 1.8% in 2024 to 1.6% in 2025, remaining stable in 2026. While emerging economies show higher growth rates, they also face a slowdown: 4.3% in 2024, 4.2% in 2025, and 4.0% in 2026 (chart 4 and table 1).

Global inflation is also expected to moderate. Some countries are projecting lower variations than last year: Mexico shows an annual variation of 3.9% (compared to 4.7% last year), the United States 2.5%, and the Euro Area 2.2%. Meanwhile, global trade is being affected by fragmentation, with downside risks including increased protectionism, fiscal vulnerabilities, and tensions in financial markets. Global trade volume is expected to grow by 3.5%, a slight decline from last year’s 3.6%.

In Mexico’s case, economic growth is projected to slow from 1.4% in 2024 to 1.0% by the end of this year, followed by a moderate recovery of 1.5% in 2026. These figures are noteworthy, especially considering previous projections: just 0.2% growth in July, a contraction of -0.3% in April, and a 1.7% difference compared to January’s forecast.

This raises a key question: what is driving this growth projection? According to the technical staff’s statement following the Article IV mission conducted in September, a heterogeneous performance is expected across aggregate components—some showing slight expansions, while others face contractions. International trade is expected to slightly boost growth, with exports projected to grow by 6.6% and imports by 1.6%. Regarding consumption, the IMF anticipates a 0.5% increase, in line with INEGI’s forecast: a slight stagnation in private consumption in recent months and a modest 0.6% growth in September. Investment shows a concerning decline, dropping from 3.3% to -5.1% between 2024 and 2025, particularly hindered by public investment, which is expected to contract by 16.6%. Finally, government spending is projected to decrease its share of GDP from 30.3% to 28.5%.

The IMF’s economic growth forecasts appear optimistic compared to analysts’ projections and our own estimates. The Citi survey released a few weeks ago showed an expected growth of 0.5%, unchanged from the previous month. In contrast, Scotiabank's expectations are more conservative, with a projected contraction of 0.1% for 2025 and only a mild recovery to 0.6% for 2026, still well below the IMF’s forecast.

In this context, considering the global economic slowdown and the need to support countries with growth potential in the coming years, the IMF recommends strengthening the credibility of economic policies, preserving central bank independence, advancing fiscal consolidation through balanced plans, and accelerating structural reforms that enhance productivity and resilience. These measures are especially necessary for emerging economies like Mexico, which face significant challenges in laying the foundation for sustainable and long-lasting growth.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.