- Chile: July GDP of 1.8% y/y (1.0% m/m SA) sets the economy on track for growth equal to or above 2.5%

- Colombia: Financing law release; Current Account Deficit remains low amid mixed forces, trade deficit widens, remittances stay strong

- Mexico: Upward revisions in growth, lower inflation expectations in Banxico’s survey; Remittances extend downward trend in July

- Peru: August inflation reinforces expectations of interest rate cuts

CHILE: JULY GDP OF 1.8% Y/Y (1.0% M/M SA) SETS THE ECONOMY ON TRACK FOR GROWTH EQUAL TO OR ABOVE 2.5%

- The central bank is likely to revise the 2025 GDP growth range to 2.25%–2.75%. September GDP, ahead of the first-round presidential election, could reach between 3.5% and 4.5% y/y.

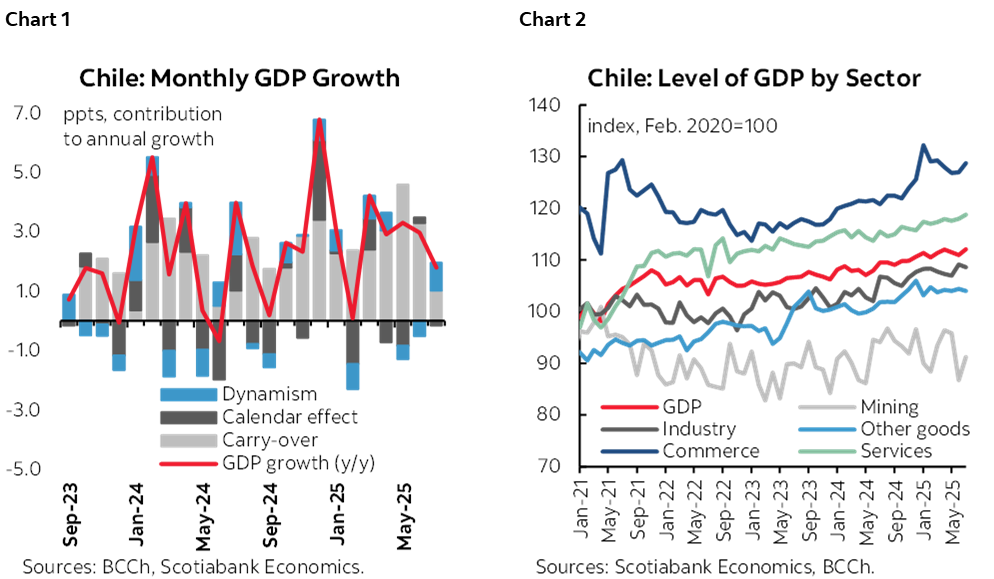

On Monday, September 1st, the central bank (BCCh) released the July GDP, which expanded 1.8% y/y, broadly in line with our expectations and market consensus, supported by solid growth in non-mining activity—particularly commerce and services—and a partial recovery in mining production (charts 1 and 2). Based on these figures, non-mining GDP reached a historical high, driven by services, while the annualized quarterly growth rate regained momentum, reaching 1.8%. Thus, even without further dynamism in August and September, annualized quarterly growth for Q3-25 would exceed 3%. Overall, the carry-over effect for 2025—assuming no further acceleration in the remainder of the year—would place GDP growth at 2.5%. At Scotia, we maintain our GDP growth forecast for the year at 2.5%, with an upward bias given the recent strength in activity and domestic demand.

At the sectoral level, non-mining activity stood out, especially wholesale commerce and business services, where mining and energy appear to be key drivers. The July figures and the recently released Q2-25 national accounts confirm the rebound we anticipated in investment, through wholesale consumption of machinery and equipment (for mining and construction) and strong growth in services, particularly business services. In this regard, services reached their highest historical level (SA series) in July. Investment is expected to continue supporting domestic demand in the coming months, as suggested by the marginal increase in capital goods imports and rising demand for construction inputs. At Scotiabank, we maintain our investment growth forecast of 6.0% for 2025.

The central bank is expected to revise upward its GDP growth range for the year to 2.25%–2.75%. The next Monetary Policy Report (IPoM) will be released on September 10th, when the central bank will update its annual growth forecast range. In light of recent data, we estimate that the Board will raise the lower bound of the range by 25bps, ruling out scenarios of growth below 2.25% and endorsing a baseline scenario of around 2.5% for this year. This would bring the central bank closer to the growth projection we have maintained for several quarters (2.5%), which now carries an upward bias given the recent sectoral momentum, particularly in investment.

The September GDP, ahead of the first-round presidential election, could reach between 3.5% and 4.5% y/y. A less demanding base of comparison, a favourable calendar composition (two additional business days), and the positive momentum observed as the economy entered Q3 suggests that the September GDP will significantly exceed the average GDP growth expected for 2025. The fourth quarter will face much tougher annual comparison bases, so we remain cautious about monthly activity figures significantly exceeding trend growth.

—Aníbal Alarcón

COLOMBIA: FINANCING LAW RELEASE

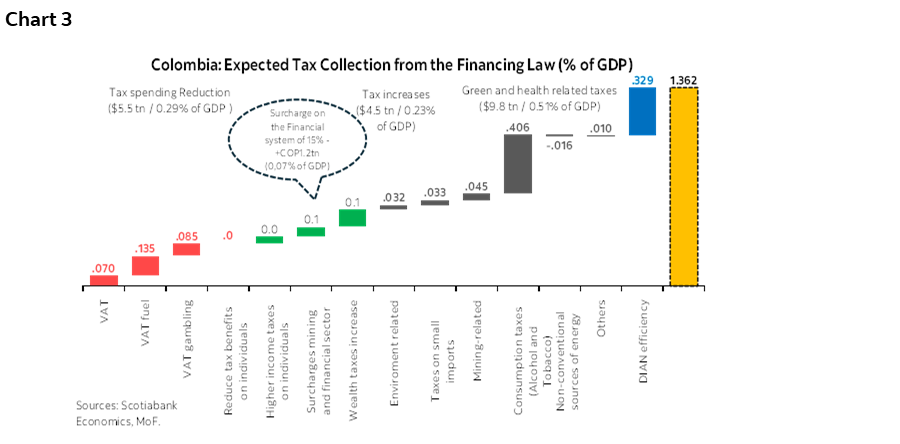

- On Monday, September 1st, the government released the text of the Financing Law (tax reform), aiming to increase the tax income by 1.4% of GDP (COP 26 tn). The proposal includes measures such as imposing VAT on certain services—including online gambling, tobacco and alcoholic beverages, as well as cultural and sports activities. In addition to these measures, we noted that the government intends to impose VAT (between 5% and 8%) on agro-industrial inputs and machinery, as well as on electric vehicles. It also proposes higher income tax rates for individuals, special taxes on the mining and financial sectors, and even on churches. The wealth tax is proposed to have a lower threshold, while consumption taxes are set to increase on alcoholic beverages, cigarettes, vapes, and related items (chart 3).

- While some VAT proposals seem reasonable (e.g., on gambling and vice-related items), other aspects of the reform could discourage investment. Moreover, some proposals, such as taxing the same base of individuals with higher income taxes, have not proven effective in significantly increasing tax revenue.

- We believe it will be difficult to garner broad support for the current tax reform proposal. Our base case scenario points toward total rejection, especially since the government has not demonstrated a clear willingness to moderate its spending, however we have to see if Congress wants to negotiate something of the tax reform. Last week, CARF highlighted that there is room to adjust certain expenditures and also noted that even with the approval of the tax reform—estimated to raise 1.4% of GDP—it would still be insufficient to ensure fiscal sustainability. In fact they said Colombia needs to adjust either the spending side or the income side of the fiscal equation by no less than ~ 2.2% of GDP.

- In the meantime, we have to see how the tax collection in 2025 goes since the calendar for the individuals has already started. For now the MoF has given the sense of being net debt buyer in global and local COLTES markets, however the shortfall in revenues could change the stance of the MoF taking them to the usual role of net debt sellers.

- The next relevant milestone is September 15th, the deadline for Congress to decide about the size of the Budget 2026, it will also show the willingness of Congress to discuss any tax measures.

CURRENT ACCOUNT DEFICIT REMAINS LOW AMID MIXED FORCES, TRADE DEFICIT WIDENS, REMITTANCES STAY STRONG

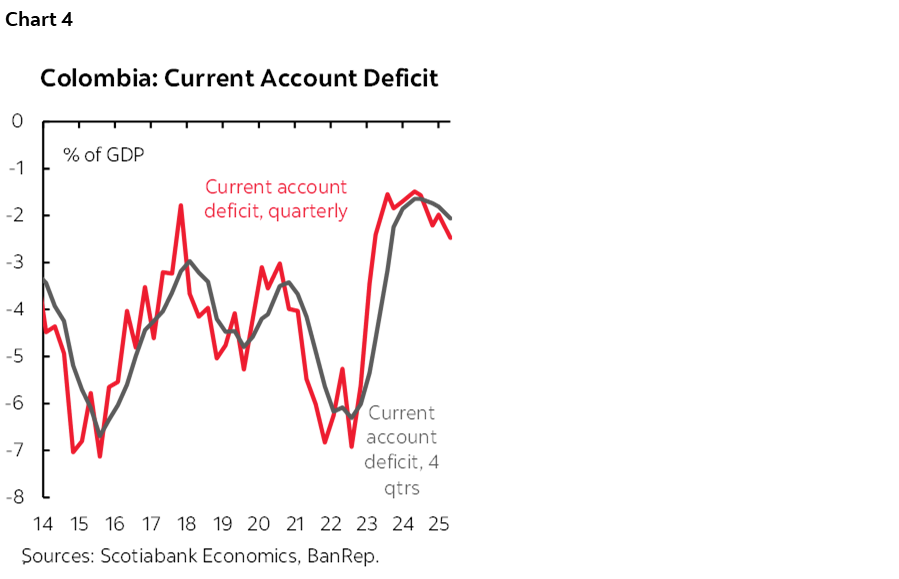

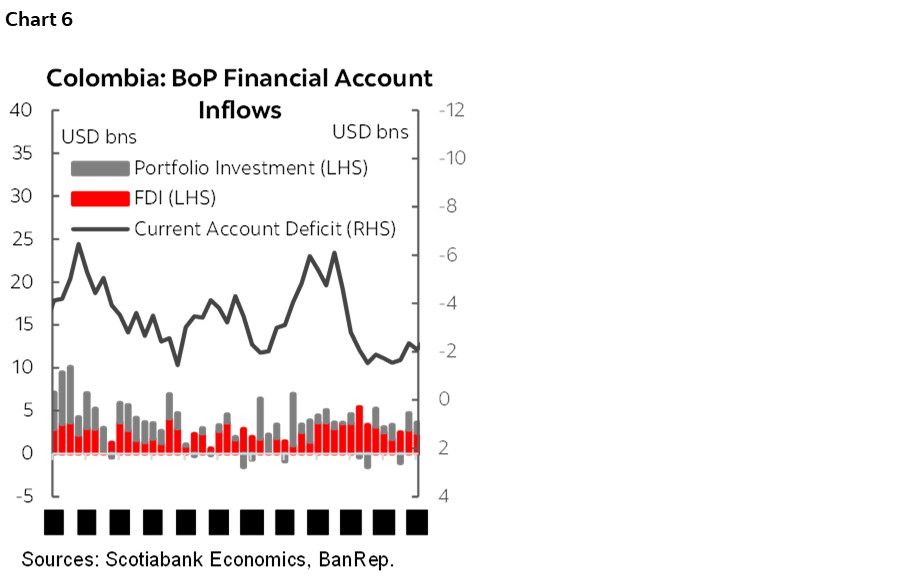

On Monday, September 1st, the central bank (BanRep) released the Q2-2025 Balance of Payments (BoP). The current account deficit stood at USD $2.6 billion, equivalent to 2.5% of GDP, 0.5 percentage points wider than the same period in 2024 (chart 4). Despite this increase, the deficit remains low by historical standards. However, it reflects mixed dynamics: the trade deficit widened to its highest level since 2022, driven by the momentum of economic recovery, while strong transfer inflows, particularly remittances, continued to reach new historical highs, providing a significant offset. The income account deficit remained relatively stable. On the financing side, FDI outflows increased, while FDI inflows were almost unchanged vs the previous quarter. Meanwhile, portfolio investment rebounded, supported by higher external debt issuance by the government.

The BoP data reveals key dynamics in the Colombian economy. First, the recovery is evident in the rebound of imports, contrasting with stagnant exports. Second, remittances are playing an increasingly significant role, not only in the BoP but also in supporting robust household demand. On the investment front, rising FDI outflows warrant close monitoring, especially in the context of the proposed tax reform. Portfolio investments, for now, are supportive and appear to be gaining relevance in financing the deficit, however that dynamic is driven by the high fiscal deficit that is motivating higher debt issuance in international markets. International reserves increased, driven by the financial performance of invested assets.

As of June 2025, the year-to-date current account deficit reached USD $4.69 billion, representing 2.22% of GDP. FDI financed 92% of this deficit, however in Q2-2025 portfolio investments are showing a notable increase, largely driven by higher public borrowing in global markets.

At Scotiabank Colpatria, we project a current account deficit of 2.4% of GDP for the full year 2025, reflecting a wide trade deficit amid ongoing economic recovery. For 2026, we expect the deficit to reach 2.5% of GDP, with potential for further widening if investment activity picks up more strongly by year-end. Under this scenario, we anticipate moderate pressure on the exchange rate, with financial flows volatility continuing to drive short-term currency movements. We maintain our view favouring FX levels above 4,000 pesos, trending toward 4,250 pesos if economic activity leads to wider trade deficits amid a still-challenging fiscal outlook, where a risk premium may be priced into the USDCOP.

We do not expect the BoP figures to be a game changer ahead of BanRep’s next meeting. We maintain our forecast for the policy rate to remain stable at 9.25% through the end of the year.

Further Details about the Balance of Payments Numbers:

Current Account:

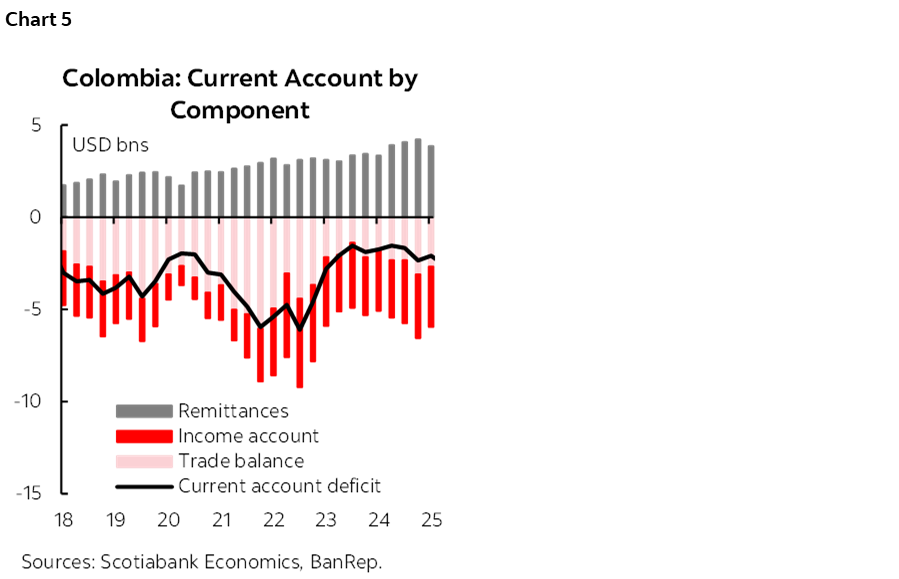

In Q2-2025, the current account deficit stood at USD $2.6 billion (2.5% of GDP; see chart 5), marking the widest level since Q4-2023. For the year-to-date (YTD) period up to June, the deficit reached USD $4.7 billion (2.2% of GDP), an increase of USD $1.4 billion compared to the same period in 2024. The main driver of this deterioration was a higher trade deficit (USD $6.4 billion, up 56.5% year-over-year). Unlike the situation observed a year ago, this increase in the trade deficit reflects an economic recovery, which has led to a rebound in imports. This contrasts with the weak performance of traditional exports, particularly coal and oil. Remittances remained strong, significantly offsetting the impact on the current account deficit.

- Trade balance of goods: In the YTD up to June 2025, the trade deficit in goods was USD $6.43 bn. Exports increased by 0.3% y/y, mainly better coffee exports due to better prices (+63.4% y/y) and quantities (+13.4% y/y), manufacturing products and flowers, that offset the weakening on coal and oil export. In the case of mining exports there was a significant negative impact in exported volumes, -26.4% y/y for coal, while in the case of oil the main impact came from prices (-12.8% y/y).

- Imports of goods stood at USD $32.66 bn in the H1-2025 (+9.2% y/y). The good news is that purchases of inputs and capital goods for the industry is leading the gains (+9.1% y/y), something to be vigilant about is that consumption goods are also expanding (+15.1% y/y), and the former usually doesn’t have a counterpart in the investment side, instead we think a flow that is compensating this deficit is the remittances inflows.

- The trade balance of services turned into a moderate deficit. In the YTD services had a deficit of USD $36 m. The most dynamic part of exports is still tourism-related (+12% y/y), which are advancing at a similar level of other modern exports (+14% y/y) related more with the IT services sector.

- Income account: During the YTD up to June, the income account deficit stood at USD $6.23 bn, lower by USD $143 m compared to the deficit in the same period of 2024, which reflects lower interest payments on hard currency credits (USD $253 m lower outflows), higher earnings on Colombia’s portfolio investments (USD $151 m) and lower earnings of FDI investments in Colombia (USD $47 m).

- Transfers: Transfers continued contributing to a lower current account deficit. Net inflows in the YTD were USD $7.99 bn (+10.6% y/y); remittances were at USD $6.40 bn, increasing by 13.9% and representing 3% of GDP and 13.3% of current inflows of the BoP. The US and Spain remain the main source of remittances for Colombia, and despite the less friendly measures towards migration in the US, we still see decent behaviour.

Financing side:

The financial account registered net inflows of USD $3.538 bn (1.7% of GDP), including the International Reserve Increase of USD $1.09 bn (chart 6). During this period, investment inflows came mainly from portfolio investments (+ USD 7.4bn), that outpaced the FDI inflows (+6.58 bn).

- Foreign Direct Investment: FDI gross inflows stood at USD $6.58 bn in the YTD, increasing 1.5% y/y. The main destinations were oil and mining (30%), financial services (27%), and manufacturing (15%). Around half of FDI inflows correspond to capital investments (USD $3.02 bn), while USD $2.49 bn are due to reinvested earnings and USD $1.07 bn responds to higher debt.

- Portfolio investments: Total inflows stood at USD $7.34bn, reflecting better inflows from offshore investors in local financial assets (USD $2.07 bn), but the highest part of this was also explained by a strong increase of fresh hard currency debt (US $5.33 bn).

—Jackeline Piraján & Valentina Guio

MEXICO: UPWARD REVISIONS IN GROWTH, LOWER INFLATION EXPECTATIONS IN BANXICO’S SURVEY

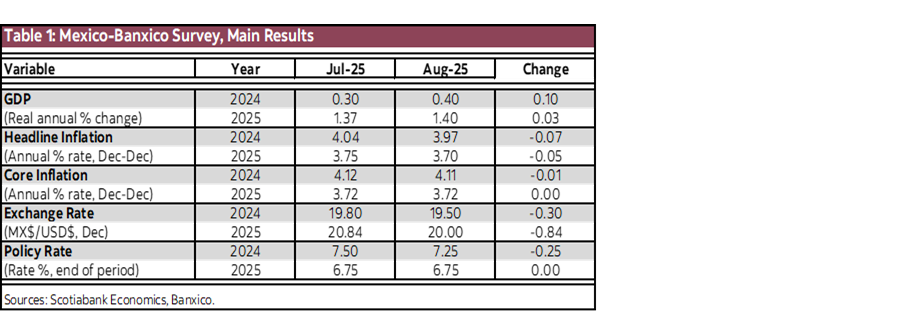

According to Banco de México’s Survey of Expectations, analysts revised their growth forecast upward, now expecting 0.4% for 2025 compared to 0.3% in the previous month, marking three consecutive months of positive revisions. For next year, the consensus also rose, but slightly, from 1.37% to 1.40% (table 1).

In contrast, year-end inflation expectations declined to 3.97% from 4.04%, following upward revisions between April and July. However, core inflation forecasts remained virtually unchanged at 4.11% from 4.12%.

Exchange rate estimates were revised downward for the fourth consecutive time, with analysts now expecting a rate of 19.50 pesos per dollar by the end of this year (previously 19.80), and 20.00 pesos by the end of 2026 (previously 20.84).

Finally, following the August monetary policy meeting, analysts now forecast a year-end interest rate of 7.25%, implying two additional 25bps cuts in the remaining three meetings of 2025. For 2026, the expectation remains unchanged at 6.75%.

REMITTANCES EXTEND DOWNWARD TREND IN JULY

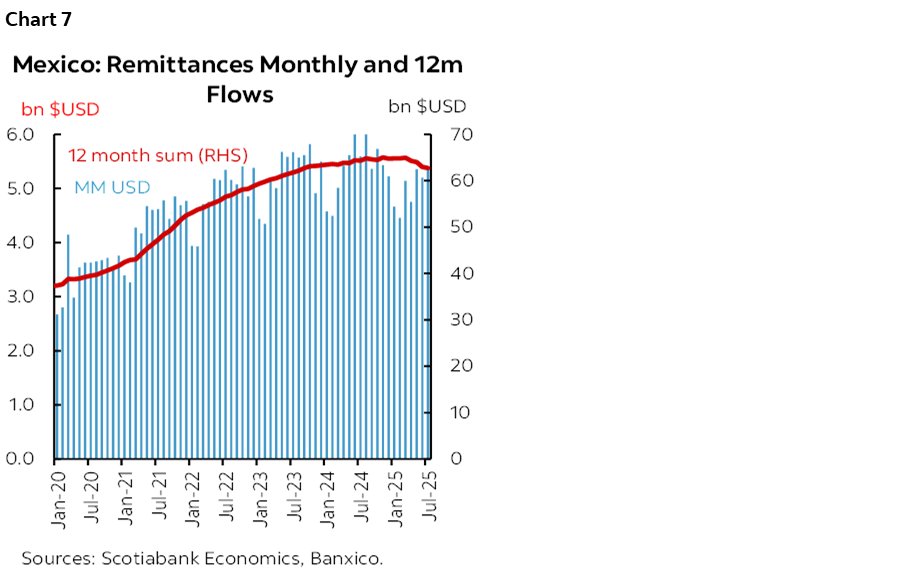

In July, remittances fell year-over-year for the fourth consecutive month, now at -4.7%, totaling $5.329 billion USD (vs. -16.2% previously). The number of transactions also declined by -8.0%, implying an average remittance of $415.5 USD, a 3.6% annual increase (chart 7).

Over the past twelve months, remittances totaled $62.715 billion USD, representing a -2.5% annual decline (vs. -2.22% previously), its slowest pace since September 2013.

—Rodolfo Mitchell & Miguel Saldaña

PERU: AUGUST INFLATION REINFORCES EXPECTATIONS OF INTEREST RATE CUTS

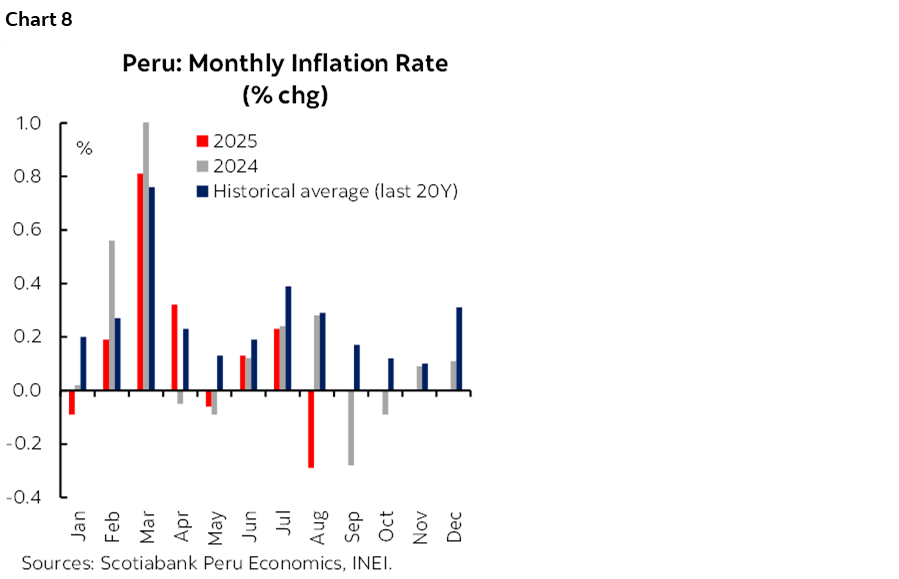

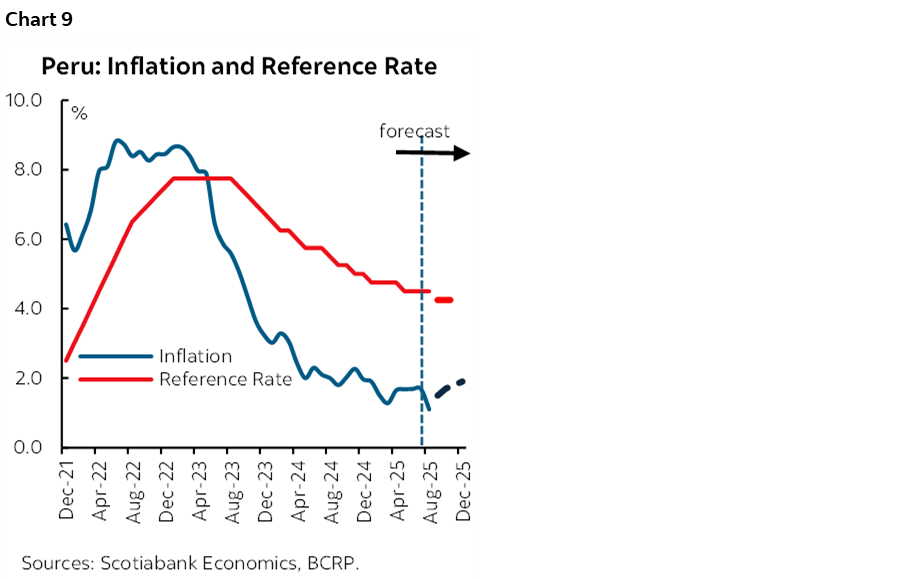

Headline inflation fell by 0.29% m/m in August, contrasting with the increase anticipated by the Bloomberg analyst consensus (+0.17%) and our own forecast of 0.0%. This monthly figure deviates from the 20-year historical average (+0.29%) and from the figure recorded in August 2024 (+0.28%). As a result, annual inflation fell to 1.1%—its lowest level in seven years, since August 2018—after remaining at 1.7% for four consecutive months (chart 8).

At a disaggregated level, the main negative contributions during the month came from three categories:

1. Food and non-alcoholic beverages (-1.05%), primarily due to a significant correction in fish prices (-12.6%) which contributed -0.14% and accounted for 50% of the monthly decline in headline inflation.

2. Lower electricity (-3.5%) and gas (-1.7%) tariffs.

3. Transportation (-0.15%), due to falling fuel and motor vehicle prices.

Core inflation—which excludes food and energy—rose slightly by 0.08% m/m in August. This figure was below the 20-year historical average (+0.15%) but higher than the rate recorded in August 2024 (+0.01%). On an annual basis, core inflation increased from 1.7% in July to 1.8% in August, marking six consecutive months below the midpoint of the target range.

We preliminarily project that monthly headline inflation in September will be positive, around +0.1%. Additionally, a base effect will be present, as the September 2024 figure was -0.24%, compared to the 20-year average of +0.2%. Consequently, annual inflation is likely to rise from 1.1% in August to 1.5% in September.

Low exchange rate levels and declining international prices for oil and agricultural commodities—such as corn, wheat, and soybeans—have contributed to lower domestic inflation. Accordingly, we revise our year-end annual inflation estimate down to 1.9%.

Regarding the reference rate, we now anticipate a terminal rate of 4.25%, implying that the next rate cut will likely occur this year. The recent inflation data may lead to a downward revision in inflation expectations, to be published next month in the BCRP’s macroeconomic expectations survey, thereby creating additional room for further rate cuts (chart 9).

The interest rate differential between the Fed and the BCRP is currently neutral and does not raise concerns, given the strength of the Sol. The market assigns a high probability (90%) that the next rate cut in the U.S. will occur in September, which could also encourage the BCRP to adjust its monetary policy rate in the short term.

—Ricardo Avila

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.