- Chile: BCCh raises neutral policy rate by 25bps as macro scenario aligns with Scotia’s outlook

- Mexico: Retail and wholesale sales for October

- Peru: Cement market—2025 local sales projected to reach a three-year high

CHILE: BCCH RAISES NEUTRAL POLICY RATE BY 25BPS AS MACRO SCENARIO ALIGNS WITH SCOTIA’S OUTLOOK

The Central Bank released its December Monetary Policy Report (IPoM), revising upward its GDP growth forecast for 2025 and 2026, moving closer to Scotia’s long-standing projection of 2.5% for both years. As anticipated, the main driver behind the upward revision is stronger investment dynamics, particularly in Machinery and Equipment. Accordingly, the investment forecast for 2025 was raised from 5.5% to 7.0%, while the 2026 estimate increased from 4.3% to 4.9%. Private consumption has accelerated slightly, in line with the September IPoM outlook.

The Central Bank’s scenario assumes a peso appreciation and a decline in copper prices from current levels. A key assumption is the expected trajectory of the Real Exchange Rate (RER), which is projected to follow an appreciating trend from the latest estimated level (105 points in October). Based on our estimates, the spot RER stands near 102 points, consistent with a nominal exchange rate around CLP 920. Regarding copper prices, although the forecast was revised upward across the projection horizon (US¢450/lb in 2026), we find the expected rapid convergence toward long-term values noteworthy, given current prices near US¢530/lb and persistent supply constraints and market deficits anticipated in the coming years.

As expected, the Central Bank raised its estimate of the neutral Monetary Policy Rate by 25 bps. In mid-Q3, Scotia revisited neutral real rate estimates, obtaining a range between 0.8% and 1.9%, with a median of 1.3%. In its December IPoM, the Central Bank conducted a similar exercise, arriving at a range of 0.9% to 1.7%, with a median of 1.2%. This confirms our earlier call for a 25-bps increase in the neutral rate, implying nominal values between 3.75% and 4.75%, with a midpoint at 4.25%. However, we note the slow convergence assumed in the December IPoM toward neutral levels, which would materialize only by Q3-26 (July 2026), despite inflation reaching the 3% target in Q1 and remaining near that level for most of the year. Beyond the IPoM guidance, we continue to project a policy rate cut to 4.25% in Q1 (January or March meeting), conditional on inflation converging to target and the peso appreciation we expect consolidating.

—Aníbal Alarcón

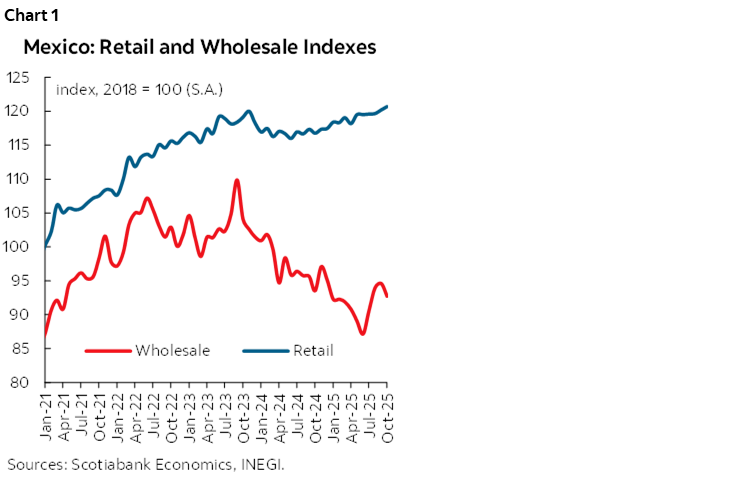

MEXICO: RETAIL AND WHOLESALE SALES FOR OCTOBER

In October, according to the Monthly Survey of Commercial Companies (EMEC), retail sales (chart 1) showed a marginal monthly increase in seasonally adjusted figures, with a variation of 0.4%. Regarding employed personnel and average salaries, variations of 0.1% and 1.1% were observed, respectively. In wholesale trade, there was a decrease of -1.8% in total revenues, while employed personnel and average salaries were adjusted upwards, with figures of 0.3% and 1.6%, respectively. At an annual rate and in original figures, retail trade registered generalized increases: revenues increased 3.4%, employed personnel 1.0% and average salaries 3.3%. For its part, wholesale trade showed mixed results, with a fall of -1.3% in revenues and increases of 0.3% in employed personnel and 2.4% in average salaries.

—Rodolfo Mitchell, Miguel Saldaña & Martha Cordova

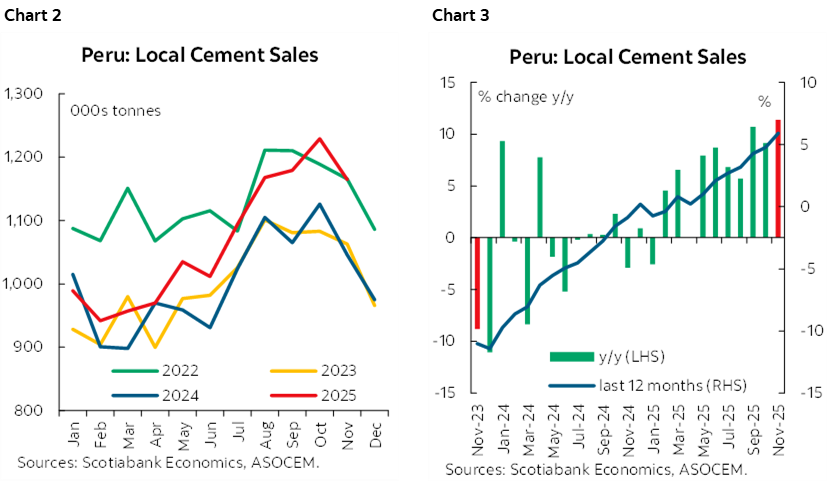

PERU: CEMENT MARKET—2025 LOCAL SALES PROJECTED TO REACH A THREE-YEAR HIGH

In November, local cement sales reached 1.16 million metric tonnes (chart 2), one of the highest monthly volumes this year, posting the strongest annual growth rate of 2025 at +11.4% YoY (chart 3). Based on this performance, we project full-year local cement sales to close at 12.6 million metric tons, representing a 5% increase versus 2024. If achieved, this would mark the highest annual volume in the past three years.

We expect cement demand to remain in positive territory at least through 1Q26, supported by several factors: i) Liquidity from pension fund withdrawals authorized in mid-December, part of which is likely to boost consumption; ii) ongoing private sector investment in construction projects, underpinned by optimistic business expectations and reduced electoral uncertainty; iii) improved household purchasing power, driven by easing inflationary pressures; and iv) dynamic real estate activity, benefiting from lower credit rates compared to previous years. Additionally, a favourable base effect will contribute to growth, considering that 1Q25 was the weakest quarter relative to 2Q25 and 3Q25.

Performance as of November 2025

From January to November, local cement sales posted a solid 4.9% YoY increase—growing nearly 6% over the last twelve months through November—totaling 11.7 million metric tons, in line with our initial forecasts. This performance underscores the market’s resilience and confirms the sector’s positive trend.

Growth was primarily driven by the self-construction segment, which accounts for nearly 70% of national cement consumption. This momentum reflects the gradual recovery of formal private employment, lower inflationary pressures compared to previous years, and relative stability in local cement prices. Additional support came from increased private infrastructure works and public investment projects, particularly at the subnational level. Private residential investment also resumed growth from 1Q25, according to Central Bank data. Finally, the real estate sector—especially in Lima—continued to strengthen, with new mortgage loans expanding 26% YoY as of October.

—Carlos Asmat

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.