- Colombia: BanRep keeps interest rate at 9.25%; announces cancellation of IMF credit line; August unemployment rate remains robust despite job creation decelerates

- Chile: August GDP at 0.5% y/y does not jeopardize 2025 GDP growth between 2.5% and 2.75%; 120K jobs created YoY

COLOMBIA: BANREP KEEPS INTEREST RATE AT 9.25%; ANNOUNCES CANCELLATION OF IMF CREDIT LINE

BanRep maintained the monetary policy rate at 9.25% in a divided vote, with the same distribution as in recent meetings. Four members voted to keep the rate unchanged, two voted for a 50 bps cut, and one voted for a 25 bps cut. In its statement, the central bank emphasized that the decision was made in a context of rising inflation expectations, robust economic activity, and ongoing global and regional uncertainty. Finance Minister Germán Ávila stated that the government believes it is necessary to continue advocating for an interest rate cut to support a stronger economic recovery and help Colombia face geopolitical uncertainty.

During the same press conference, Governor Leonardo Villar announced the cancellation of Colombia’s Flexible Credit Line (FCL) with the IMF. The decision followed the release of the Article IV Consultation for Colombia (see here), in which the IMF highlighted that the country’s fiscal policy and policy framework had weakened below the threshold required to qualify for the FCL. Governor Villar also noted that there are no expectations of increasing international reserves, as the current level is sufficient to protect Colombia’s economy against negative shocks.

It is worth noting that yesterday’s statement was very straightforward and lacked references to concerns about the fiscal situation. The focus was on the FCL cancellation, with both BanRep and the Ministry of Finance emphasizing that Colombia has a robust buffer of international reserves.

During the press conference, Governor Villar stated that the possibility of increasing the interest rate is not under discussion. He emphasized that the Board’s current focus is on maintaining a contractionary stance to ensure inflation converges toward the target.

The Finance Minister also said that the government will follow the usual procedure for negotiating the minimum wage. However, Minister Ávila emphasized that the government would seek an increase above inflation, although he did not mention the 11% increase proposed by President Petro.

At Scotiabank Colpatria Economics, we continue to anticipate a stable interest rate environment at least through the end of Q1-2026. Our projections suggest that inflation will remain volatile, with a rebound expected to continue and end 2025 above 5%. Furthermore, any potential rate cuts would likely resume only after assessing the inflationary impact of the 2026 minimum wage adjustment.

Decision highlights:

- Regarding the FCL, Governor Villar reiterated that Colombia has strong international reserves exceeding USD $65 billion, and there are no expectations of using the FCL. Therefore, he does not foresee any material impact on Colombia’s financing.

- On the economic outlook, Governor Villar stated that economic growth remains at 2.7%. As for inflation, he expects a slower convergence toward the 3% target, which is projected to be achieved by the end of the second half of 2027.

- Regarding the minimum wage debate, Governor Villar mentioned that the central bank has conducted several studies demonstrating the impact of minimum wage increases on inflation. He noted that traditionally in Colombia, the minimum wage rises above inflation. However, he expects the increase in 2026 to be lower than in 2025, as—despite the purchasing power benefits for some employees—it affects a broader segment of the population through other channels.

AUGUST UNEMPLOYMENT RATE REMAINS ROBUST DESPITE JOB CREATION DECELERATING

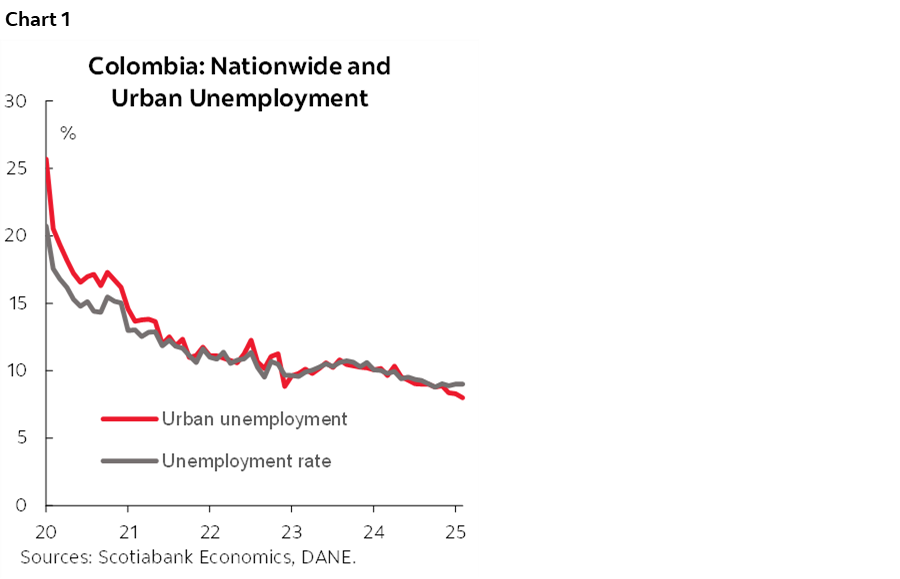

On Tuesday, September 30th, DANE published labour market data for August 2025. The national unemployment rate stood at 8.6%, down 1.1 percentage points (ppts) from the 9.7% recorded in August 2024. Urban unemployment showed the most significant improvement again, falling from 10.0% in August 2024 to 7.8% in the latest data. In contrast we are seeing deterioration in rural areas that posted a 7.8% unemployment rate deteriorating by 0.9 ppts.

Despite yesterday’s data posting a robust balance, it took place in a context in which the participation rate is diminishing; in fact, for the nationwide figure, the participation rate stood at 63.9% vs the previous year’s figure of 64.5%. Seasonally adjusted figures show the divergence between urban and rural dynamics: the national unemployment rate remained stable at 9.0% in August, while the urban rate decreased from 8.3% to 8.0% (chart 1). The urban unemployment rate is in the lowest level since 2001, while the nationwide figure is closer to a historical low.

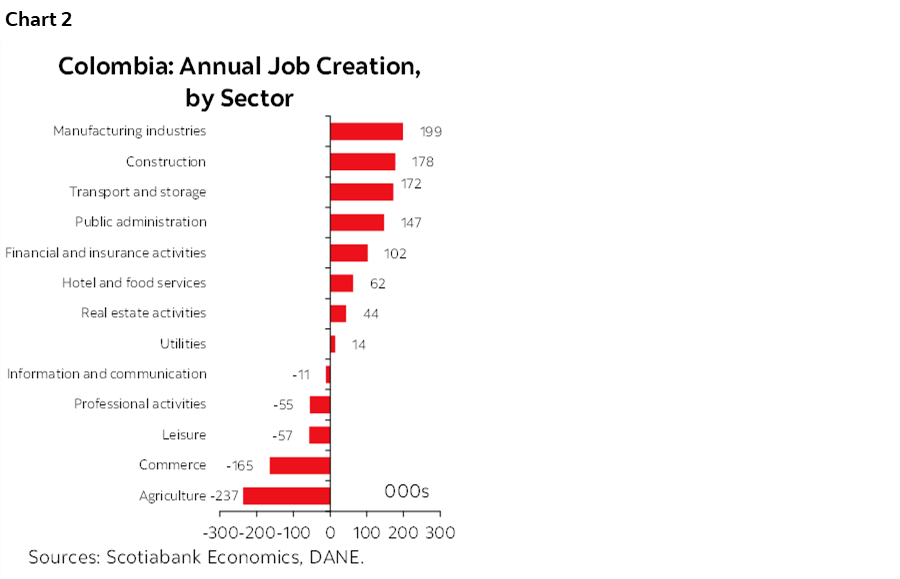

Compared to one year ago, the economy created 393 thousand jobs, a 1.7% y/y increase. The job creation pace has slowed down as July job creation exceeds 750 thousand y/y. Urban areas contributed the most with 337 thousand new positions, while rural areas had a job destruction of 196 thousand.

By sector, manufacturing (+199 thousand), construction (+178 thousand) and transport and storage activities (+172 thousand) contributed the most. Particularly in those activities we saw better hiring for male population that posted an unemployment rate of 6.7%. On the side of employment reduction were: agriculture (-237 thousand), commerce (-165 thousand) and leisure-related activities (-57 thousand). Agriculture is strongly related with a low employment dynamism in rural areas as the agricultural cycle is wakening versus one year ago. In the case of commerce and leisure activities, we see it affected female employment, in fact the female unemployment rate stood at 11.2% in August (chart 2).

The labour force participation rate stood at 63.9%, contributing to the decline in unemployment during the period. Compared to one year ago, the inactive population increased by 421 thousand, with the rise concentrated in rural areas, where inactivity grew by 250 thousand. In these areas, the labour force participation rate fell by 3 ppts to 54.3%. This increase in inactivity is correlated with the historic inflow of remittances (+14% YTD), which appears to be discouraging labour market entry.

Regarding employment quality, job gains were also reflected in a lower informality rate, which declined from 56.0% in August 2024 to 55.7% during the same period in 2025. According to DANE, 60% of the jobs created during the period were formal and concentrated in urban areas. As noted in previous reports, part of this formal employment may be indirectly driven by public sector hiring, which we will continue to monitor.

The average unemployment rate is expected to decline from 10.2% in 2024 to 9.5% in 2025, supported by stronger labour force participation and a faster pace of job creation. However, a lower unemployment rate cannot be ruled out, depending on how effectively the economy absorbs new labour market entrants. The implementation of certain aspects of the labour reform will also be a key factor to monitor in the coming months, along with future minimum wage decisions, which could increase the share of informal employment in the economy.

For now, employment data is not a major concern for the central bank. On the contrary, such robust figures support our call for rate stability at 9.25% for the remainder of 2025.

—Jackeline Piraján & Valentina Guio

CHILE: AUGUST GDP AT 0.5% Y/Y DOES NOT JEOPARDIZE 2025 GDP GROWTH BETWEEN 2.5% AND 2.75%

- Mining and calendar effect surprises point to a particularly strong September GDP

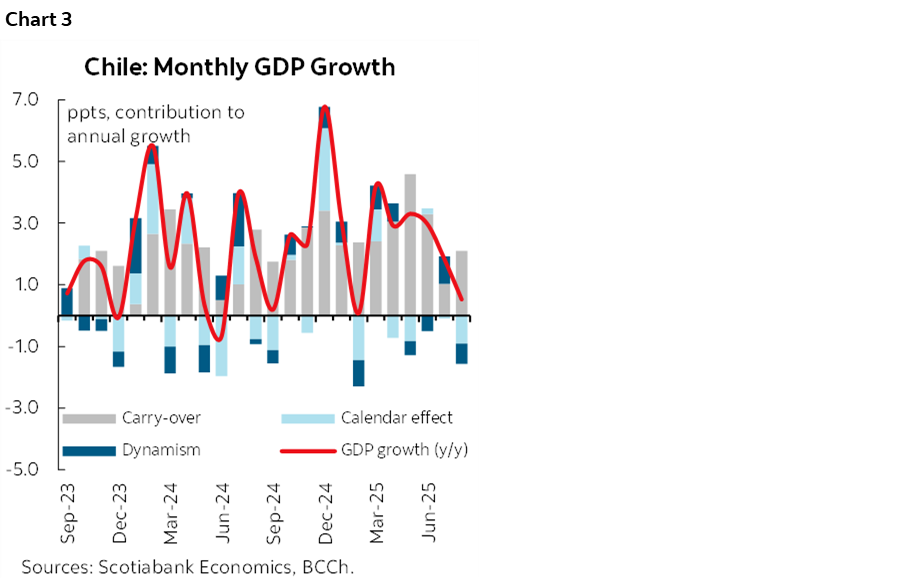

August GDP expanded 0.5% y/y, coming in below both market expectations (1.7% Bloomberg median) and our own (1.8% y/y), driven by slower growth in mining and commerce, as well as an unusually low seasonal adjustment factor that will likely reverse in the short term (chart 3), generating significant y/y growth, especially in September.

Activity contracted 0.7% m/m SA, mainly explained by declines in business services and mining GDP, the latter reflecting the temporary shutdown of El Teniente mine early in the month (chart 4). While August had one fewer business day than last year, the seasonal factor also played a key role in the y/y surprise, reaching its lowest level in recent history. In fact, SA GDP grew 1.3% y/y, nearly one percentage point above the original series. The direct implication is that September GDP will likely exceed the average growth expected for the year, reflecting two additional business days and a seasonal factor well above historical patterns.

What the seasonal factor subtracted in the first eight months of the year will be mostly returned in September. While sectoral dynamics matter more for the economy, the number of business days also plays a fundamental role. This year has the same total number of business days as last year, but by August 2025 there were two fewer business days than in the same period of 2024, which has undoubtedly weighed on y/y growth. Indeed, August (with one fewer business day than last year) surprised with an exceptionally low seasonal factor. Thus, in the remainder of the year (September–December), the factor will reflect the two additional business days, particularly in September, adding to growth.

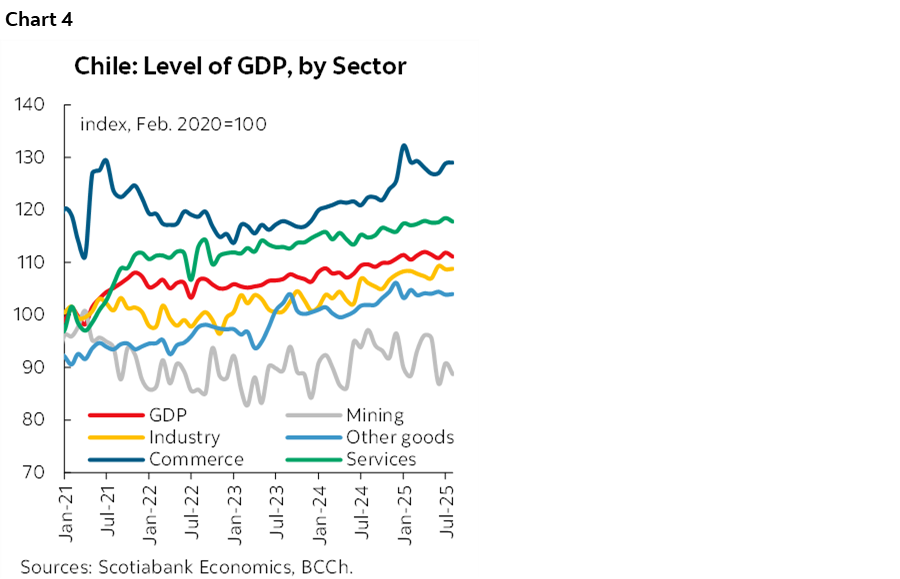

By sector, mining and retail commerce showed weaker-than-expected performance. In mining, the SA decline (-2.3% m/m) was largely explained by lower copper output. Meanwhile, retail commerce remains subdued (especially in durable goods), but this is offset by wholesale commerce and manufacturing, which posted SA monthly gains, signaling strong investment momentum.

We maintain our 2025 GDP growth forecast within the 2.5–2.75% range. This assumes a recovery in sectors such as mining, business services, and retail commerce in the coming months, as well as a rebound in the seasonal factor (especially in September) due to the higher number of business days.

120K JOBS CREATED YOY

- Employment creation recovers and SA unemployment rate declines amid rising labour costs

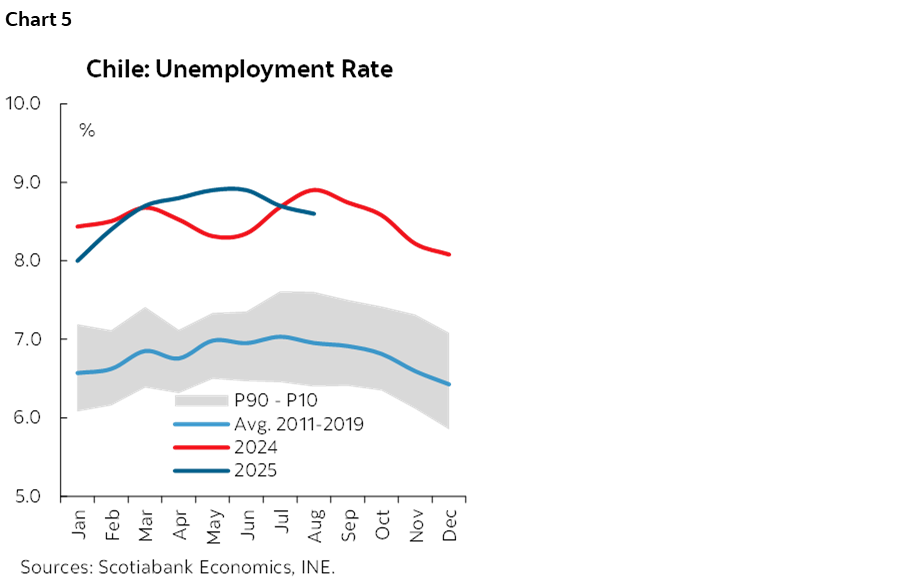

On Tuesday, September 30th, the INE released unemployment data showing a jobless rate decline to 8.6% in the quarter ending in August (chart 5), surprising market expectations (Bloomberg: 8.7%) due to stronger job creation (+25K) relative to labour force growth (+12K), as anticipated by Scotiabank. Similarly, the seasonally adjusted (SA) unemployment rate declined to 8.4%, reflecting job creation above seasonal levels for August (+42K SA). In terms of composition, 20K formal jobs were created, while informal employment rose by 5K. Overall, 120K jobs were created YoY, marking the best performance since the quarter ending in January.

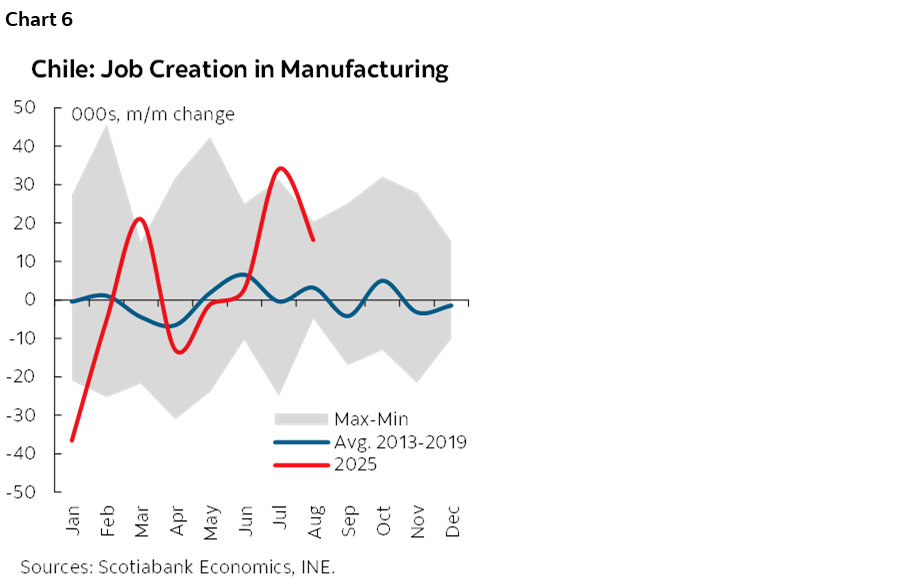

By sector, manufacturing and commerce stood out with job creation above seasonal expectations (chart 6), alongside some services and a nascent recovery in construction, which is beginning to show positive figures. Manufacturing reached its highest level since early 2018, partly reflecting the continued traction of investment in the economy. In contrast, mining and public administration showed marginal job losses.

Labour Costs: The Elephant in the Room

The focus on minimum wage hikes and the 40-hour workweek has drawn significant attention due to their impact on corporate labour costs and, simultaneously, on the wage bill that drives private consumption. However, labour costs include another component with similar or even greater quantitative relevance: the increase in pension contributions under the Pension Reform, which began in August with a 1 ppts employer-side contribution and will gradually rise to 7 ppts.

We estimate that the minimum wage increase over the past 18 months has cost firms around USD $81 million per month, based on a 17% nominal wage hike and a universe of 950K workers directly affected. Similarly, based on administrative records, we estimate that each additional percentage point in pension contributions costs employers USD $79 million per month. It’s worth noting that the macroeconomic impact of both policies differ: while the minimum wage hike entails a cost, it also represents a resource transfer to households, positively impacting consumption.

Monetary Policy: No Rush, No Need to Cut

From a monetary policy perspective, this employment report supports a cautious stance and holding the policy rate. The SA unemployment rate fell to 8.4%, within the estimated NAIRU range, suggesting no evident labour market slack that would warrant proactive monetary action. We maintain our view of a possible rate cut in December, with a 50% probability, contingent on an expected upward revision of the neutral rate in the December IPoM. We see no urgency or delay in continuing the easing cycle.

—Aníbal Alarcón

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.