ECONOMIC OVERVIEW

- Key data await, with Peru and the Eurozone kicking off September CPI prints, a Chilean and Mexican macro flood, Chinese PMIs, and the U.S. out with key nonfarm payrolls.

- BanRep and the RBA are scheduled to announce respective rate holds at 9.25% and 3.60%, while the U.S. government is cutting it close to shutting down with funding running out at midnight on Tuesday.

- In today’s report, our colleagues in Colombia go over their fundamental exchange rate estimates, the IMF’s updated assessment of conditions in Mexico, and next week’s expected rise in Peruvian inflation.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Colombia, Mexico and Peru.

MARKET EVENTS & INDICATORS

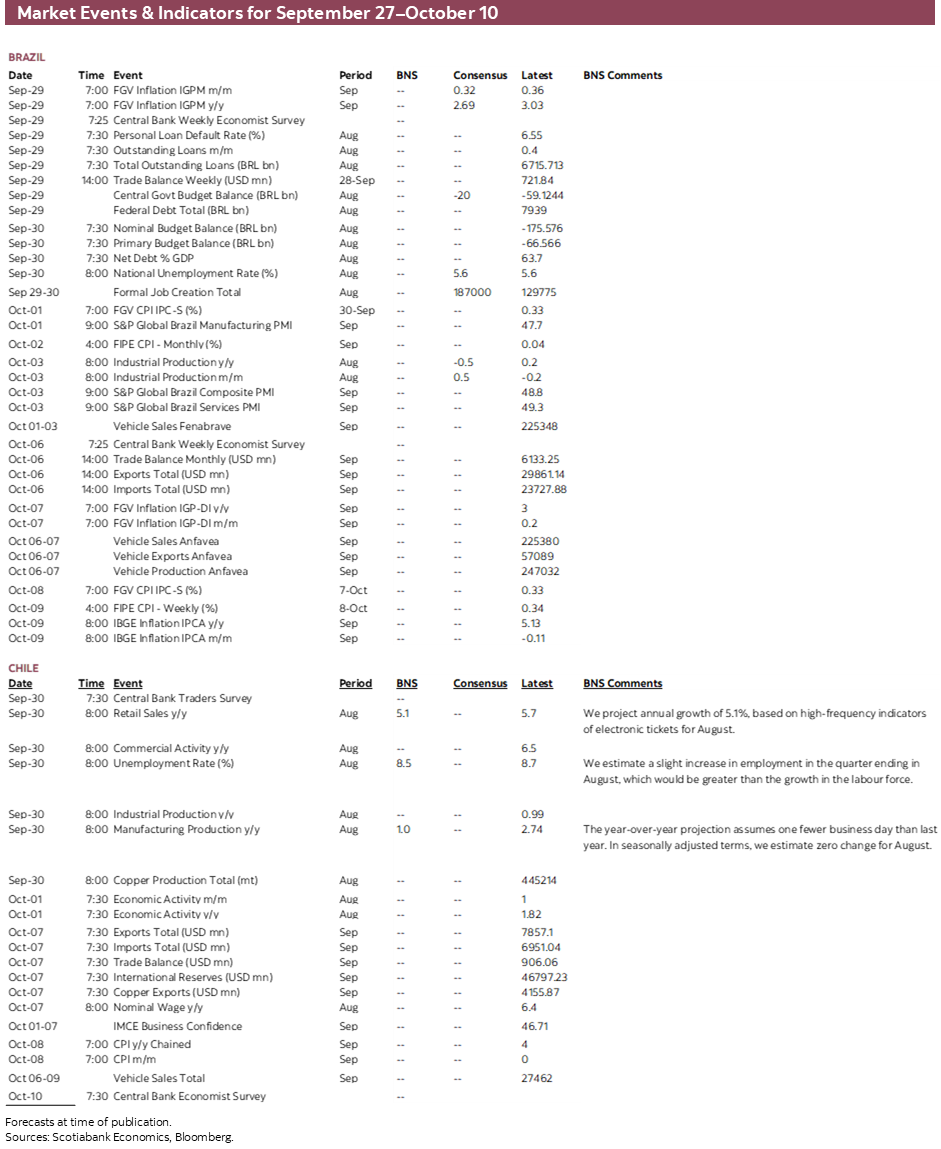

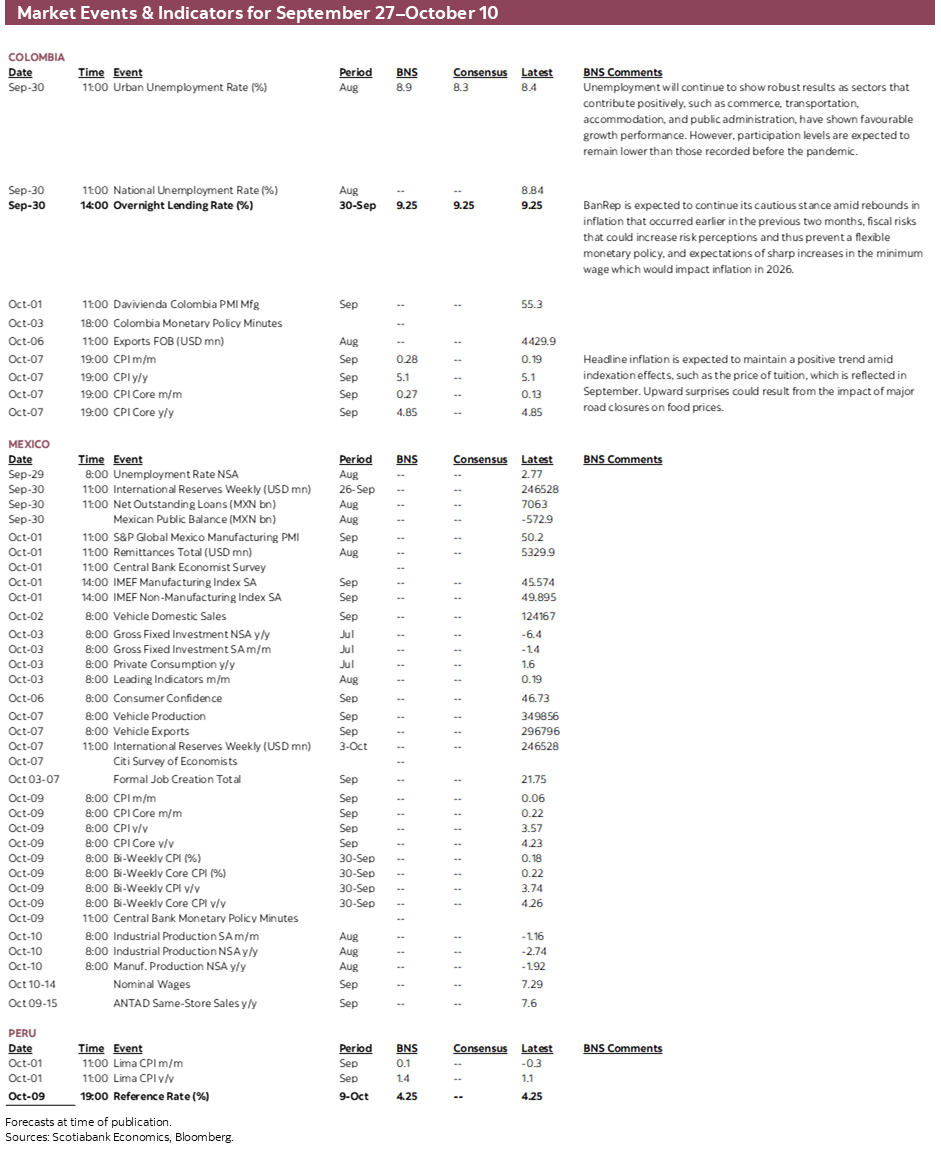

- A comprehensive risk calendar with selected highlights for the period September 27–October 10 across the Pacific Alliance countries and Brazil.

Chart of the Week

ECONOMIC OVERVIEW: CHILE AND MEXICO MACRO, PERU CPI, BANREP HOLD

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Key data await, with Peru and the Eurozone kicking off September CPI prints, a Chilean and Mexican macro flood, Chinese PMIs, and the U.S. out with key nonfarm payrolls.

- BanRep and the RBA are scheduled to announce respective rate holds at 9.25% and 3.60%, while the U.S. government is cutting it close to shutting down with funding running out at midnight on Tuesday.

- In today’s report, our colleagues in Colombia go over their fundamental exchange rate estimates, the IMF’s updated assessment of conditions in Mexico, and next week’s expected rise in Peruvian inflation.

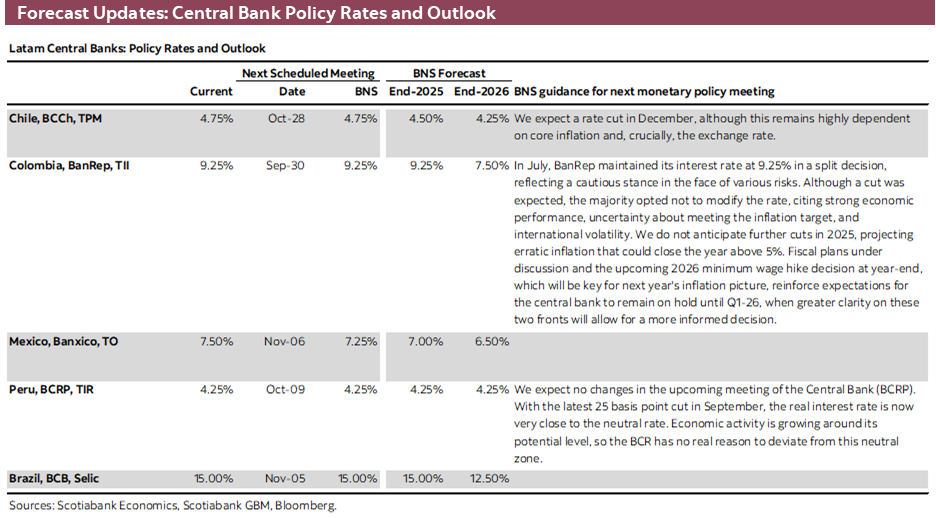

Key data await across the globe over the next few days, with Peru and the Eurozone kicking off September CPI prints, Chile publishing an August macro flood including monthly GDP figures, Mexico releasing remittances, investment, and employment readings, Chinese PMIs on tap, and the U.S. closing out the week with the biggest global data event of the month, nonfarm payrolls (on top of ISM gauges, ADP employment, and jobs vacancies). BanRep and the RBA are also scheduled to announce respective rate holds at 9.25% and 3.60%, while the U.S. government is cutting it close to shutting down with funding running out at midnight on Tuesday unless lawmakers reach an agreement over the next few days.

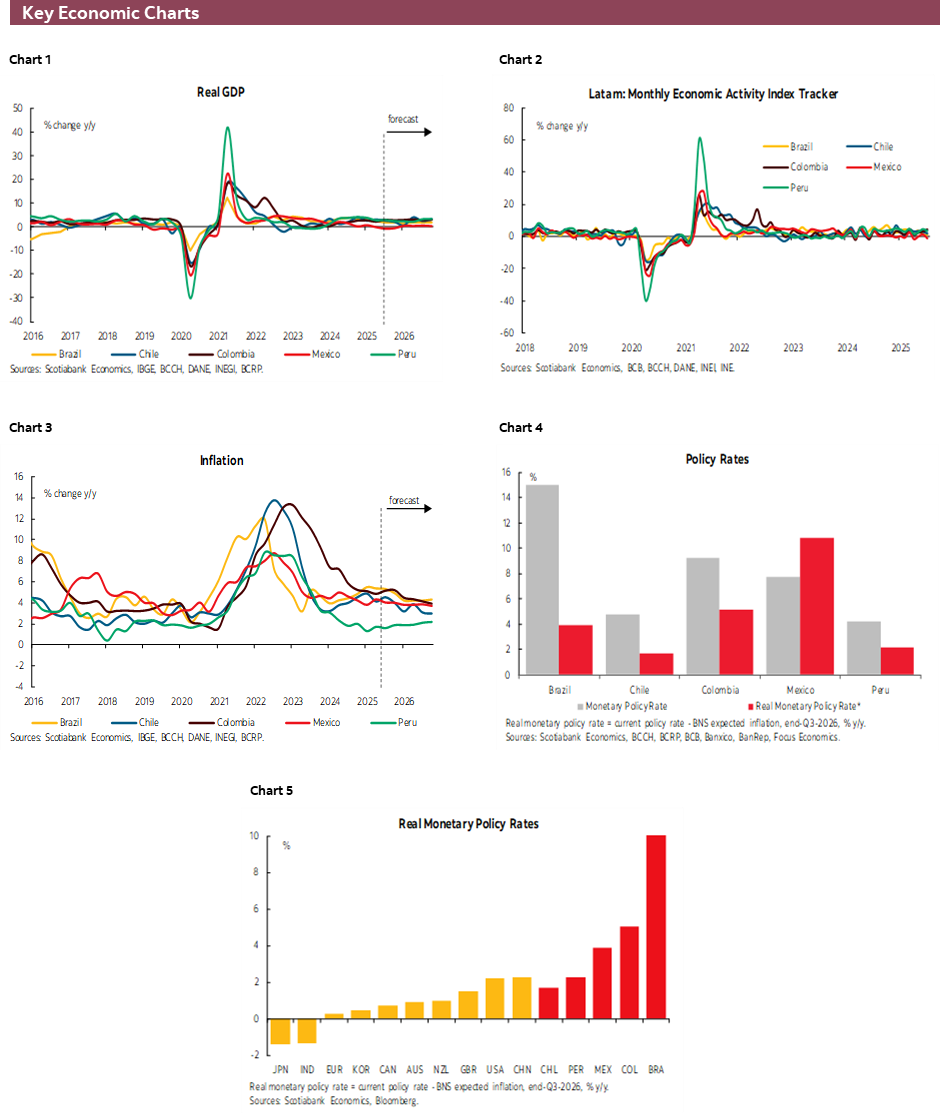

Starting with Chile, Tuesday brings the release of the BCCh’s traders survey alongside retail sales, industrial production, commercial activity, copper output, and unemployment rate figures, all for August. The central bank’s survey will likely show respondents almost universally expecting a rate hold at the late-October decision (just a few days before general elections) followed by high odds of a rate cut in December—in line with recent market pricing. The BCCh may be facing a tricky situation where overall consumption and investment trends remain firm, but labour market results have been underwhelming of late.

Estimates for Chilean economic activity growth out on Wednesday will be heavily dependent on the results of Tuesday’s macro releases, coming off a solid 1% m/m seasonally adjusted rise in output in July that owed to a strong recovery in mining. The latter will now weigh on overall activity levels due to an earthquake-related collapse at the El Teniente copper mine (the world’s largest underground copper mine) on July 31st. The focus should therefore be on non-mining output which gained 0.5% m/m in July, though slowing to 2.5% from 4.5% in y/y terms.

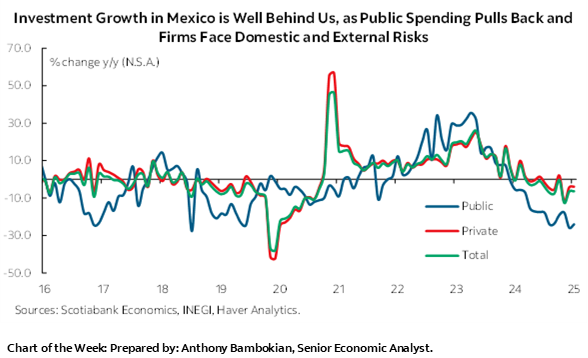

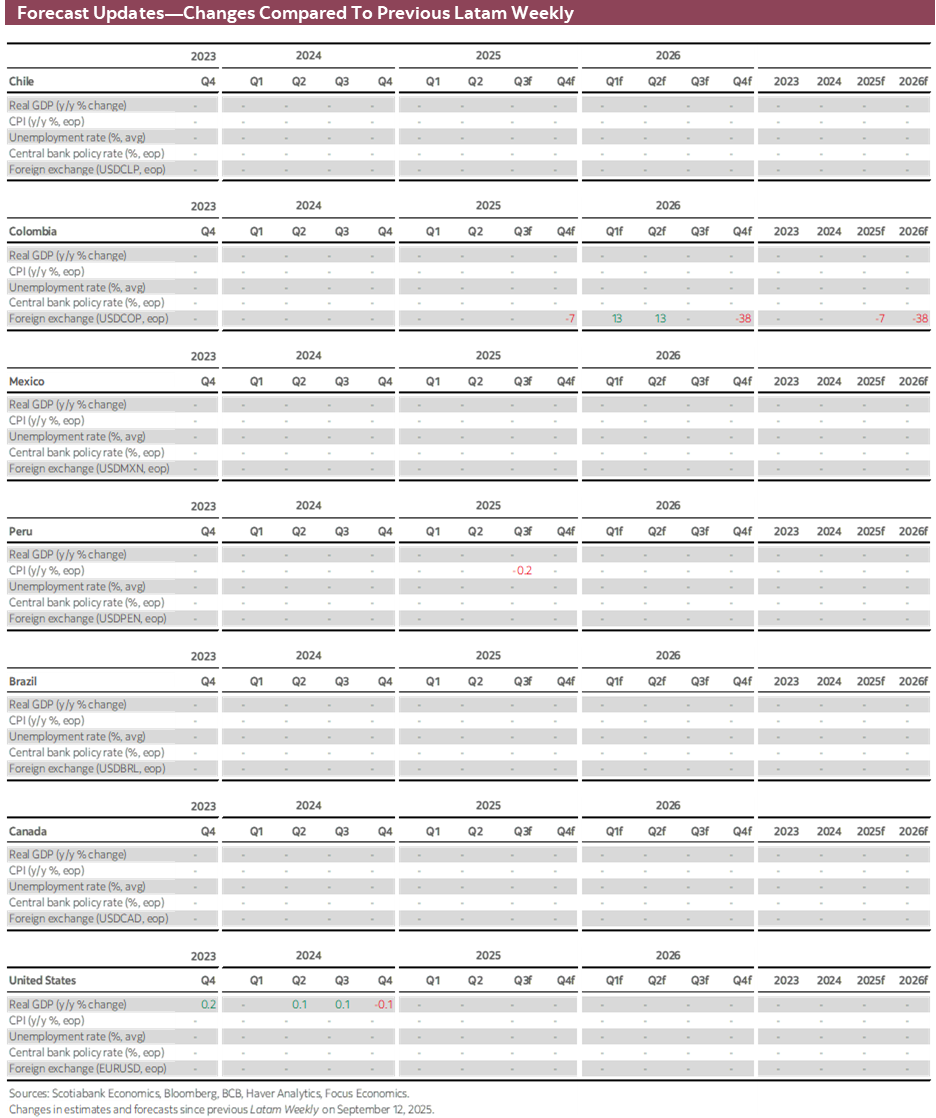

Mexican investment and formal jobs data out on Friday will likely continue to reflect weakened domestic conditions, while remittances figures on Wednesday will probably show the fading support of external income to support household spending in the country. Despite underwhelming economic trends and fundamentals, the IMF’s recently published assessment of macroeconomic conditions in Mexico still pencils in a 1% expansion in GDP for 2025, well above the median survey forecast of 0.4%, as discussed by our local team in today’s Weekly.

Over 1H25, gross fixed investment in Mexico has contracted by 6.8% when compared to the same period last year, with the private sector shrinking spending by 4.7% alongside a huge decline in government spending of 22% on the other side of the previous government’s mega-infrastructure projects. Residential construction is in good shape, however, growing by 8.5% in 1H, but that may be about the only positive development on the investment front, as private outlays on machinery and equipment have fallen 9.2% year-to-date, reflecting anxiety over U.S. tariffs but also coming off knock-on effects/partnerships with the government in infrastructure projects.

Mexico’s formal employment trends are worrying, having practically flatlined on a year-on-year basis with the latest small gains y/y merely reflecting the formalization of gig-economy workers rather than pure jobs creation. Alongside a stalling out of insured employment, Mexican remittances are no longer providing an offset to soft domestic momentum. Strict U.S. immigration policy, whether in the form of deportations, fear of deportations (and thus staying unemployed), and a sharp decline in new entrants to the U.S. has translated into a deep drop in remittance flows to Mexico that are averaging a 5% y/y decline in the January to July period, having already considerably slowed from 7.6% growth in 2023 to 2.3% in 2024. Banxico rate cuts may help a bit, but challenges continue to cloud positives for Mexico’s economic horizon, now with the USMCA review around the corner next year.

In contrast to Banxico set to roll out a couple of additional rate cuts this year, we’ll have BanRep’s rate decision on Tuesday when Colombian officials are widely expected to keep the reference rate unchanged at a 9.25% level. We think this will be the case until year-end, with policy easing (from fairly restrictive conditions) only possibly restarting in 1Q26, but much hangs on the decision for next year’s minimum wage hike that could augment indexation practices that have entrenched high inflation in Colombia. With that information still missing, there likely won’t be a significant change to the central bank’s guidance. We may get a few more details on how their views have evolved upon the release of the meeting minutes on Friday. In today’s Weekly, our colleagues in Colombia discuss the performance of the Colombian peso in the year-to-date, with adjustments to their medium-term macro estimate for the exchange rate reflecting positive impacts from easing trade uncertainty and the recent policy mismatch between BanRep (on hold) and the Fed (resuming cuts).

On Wednesday, Peru releases the first of the region’s full-month CPI data for September, which the team in Lima covers in today’s write-up. Our tracking of price readings for the month points to practically unchanged prices compared to September, which would compare to a 0.3% drop in prices a year prior and thus lift headline inflation to 1.4% from 1.1%, continuing on an uptrend towards our year-end forecast of 1.9% owing to less favourable bases of comparison, rebounding off a seven-year low. A solid economy and a realignment in headline inflation with the 2% range midpoint goal is providing little ammunition for the BCRP to consider another rate cut, though inflation expectations and the path for the Fed’s own policy rate could maybe see officials eye another reduction (for now, we don’t think so).

PACIFIC ALLIANCE COUNTRY UPDATES

Colombia—Regarding the Exchange Rate Puzzle

Jackeline Piraján, Head Economist, Colombia

+57.601.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Valentina Guio, Senior Economist

+57.601.745.6300 Ext. 9166 (Colombia)

daniela.guio@scotiabank.com

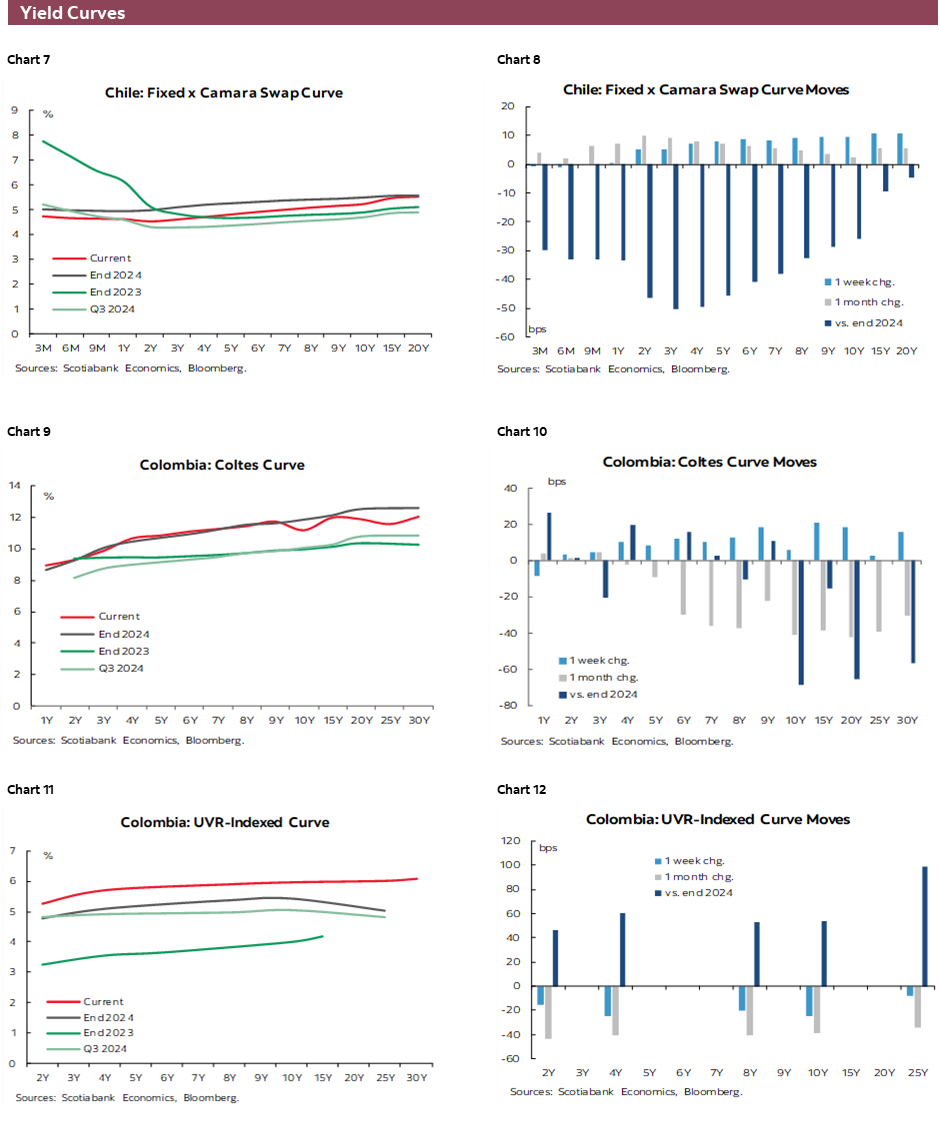

In the year-to-date (YTD) 2025, the Colombian peso ranks as the second-best performer among Latin American currencies, and sixth among all emerging market currencies versus the U.S. dollar. Part of this performance can be attributed to changes in the macroeconomic landscape; however, some of it also appears to be driven by what can currently be considered temporary shocks.

In this piece, we analyze the forces behind the recent behaviour of the COP and share our perspectives, based on our traditional macro framework. Our FX framework involves analyzing blocks of variables related to Colombia’s external accounts, the interest rate differential versus the U.S., and metrics related to perceived risk in the Latam region, Colombia specifically, and a variable that helps us measure the fiscal risk premium embedded in the exchange rate.

Fundamental Long-Term Forces

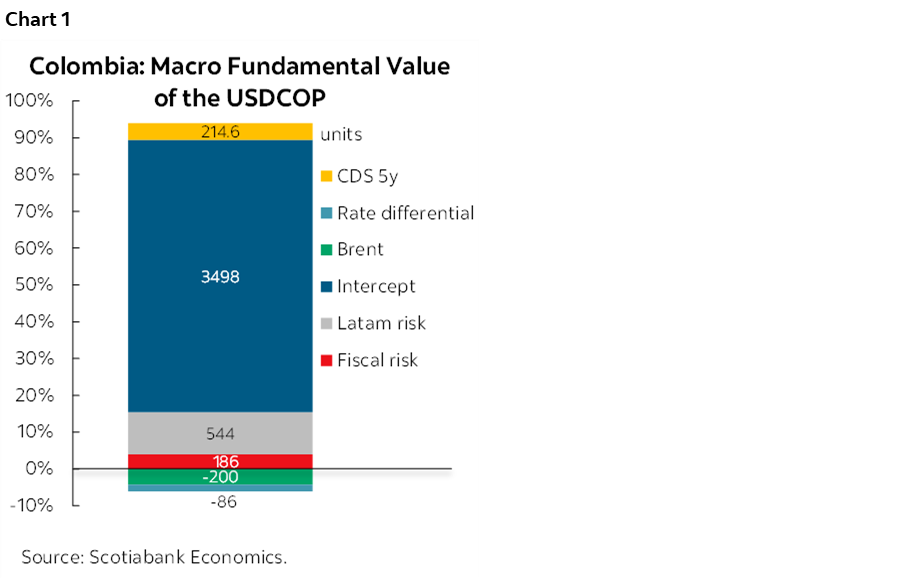

Since the beginning of the year, we have revised our medium-term macro fundamental value for the COP exchange rate from 4,350 to 4,150 pesos (chart 1), in two stages:

- The first 100 pesos downward revision was due to a reassessment of the risk posed by the trade war to the global economy and Colombia. As initial risks of a trade war faded, this dynamic contributed to a global trend of dollar weakness. We incorporated this effect into our model through the Latin America risk factor variable.

- The second 100 pesos downward revision is attributed to the Federal Reserve resuming its easing cycle, while BanRep is expected to maintain its current nominal rate. This effect is captured through the structural interest rate differential channel.

- Another force that may be settling as a structural characteristic is the resilience of Colombia’s current account deficit. Despite wider trade deficits, remittance inflows are providing an offsetting effect. Remittances continue to grow at a double-digit pace, with monthly averages slightly above USD $1 billion, currently representing ~3% of GDP. For now, this helps keep the economy’s net dollar needs under control; however, it also increases Colombia’s exposure to the U.S. economic cycle.

- A structural force in our model that remains unchanged—and may even be increasing—is fiscal risk. Since mid-2021, when Colombia lost its investment-grade rating, we incorporated a premium into our macro model to reflect this event. This premium has hovered around 200 pesos.

Short-Term and Potentially Transitory Forces

Although our fundamental value model still supports a medium-term USDCOP level of 4,150 pesos, recent market pricing shows FX levels well below this mark. We attribute this to two main forces:

- Overshooting in the carry trade: Colombia has one of the highest interest rate differentials versus the U.S., and our central bank remains far from normalizing rates. While this contributes to a strong peso, we believe the current level exceeds what can be explained by this structural rate differential.

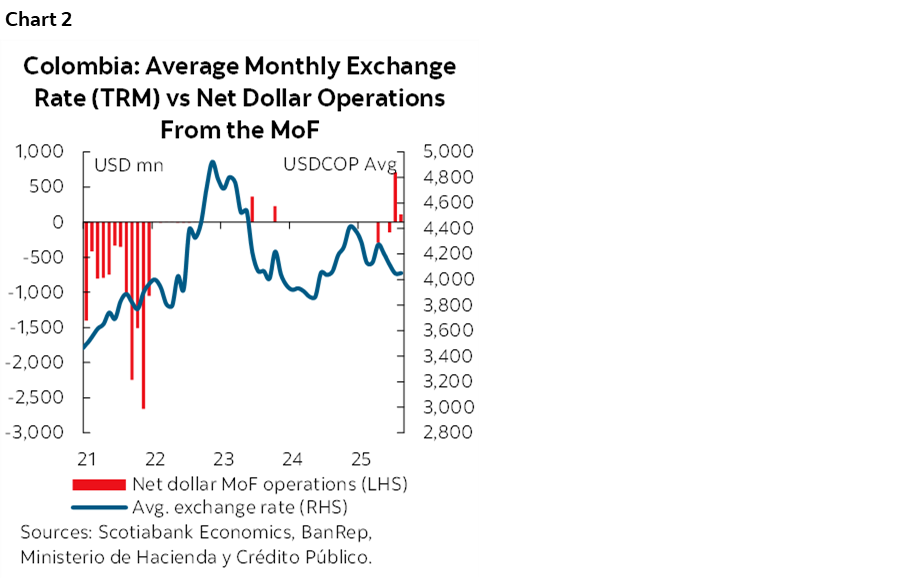

- Expectations surrounding the government’s international debt operations: In the 2025 Medium-Term Fiscal Framework, the government emphasized its intention to increase international funding, with plans to issue bonds up to USD $6 billion in 2025 and USD $9 billion in 2026. Additionally, the government disclosed liability and liquidity management structures involving significant foreign currency transactions. In a recent communication, the Ministry of Finance revealed it holds up to USD $6.4 billion in international liquidity. Since then, some FX transactions have attracted market attention, potentially linked to government monetization.

- Historically, the impact of public sector FX monetization has been limited, with low potential to generate sustainable trends. The last time we saw large-scale government FX operations was in 2021 and, during that year, the FX depreciated due to offsetting macro forces (chart 2). In the short-term, structural forces for COP depreciation are moderate, but significant government activity in the FX market is likely in the coming months. If the government’s debt plans proceed as expected this noise—deviating USDCOP from our fair value estimate—could persist through the rest of 2025.

While we believe the structural level of USDCOP should be higher, government monetization is occurring in a context where structural depreciation forces for the COP are limited. We maintain a medium-term expectation of 4,150 pesos. However, we anticipate FX levels below this mark for the remainder of 2025 and at least through Q1-2026, when we expect the government to begin unwinding short-term international market operations.

Mexico—IMF Updates its Mexico Outlook

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

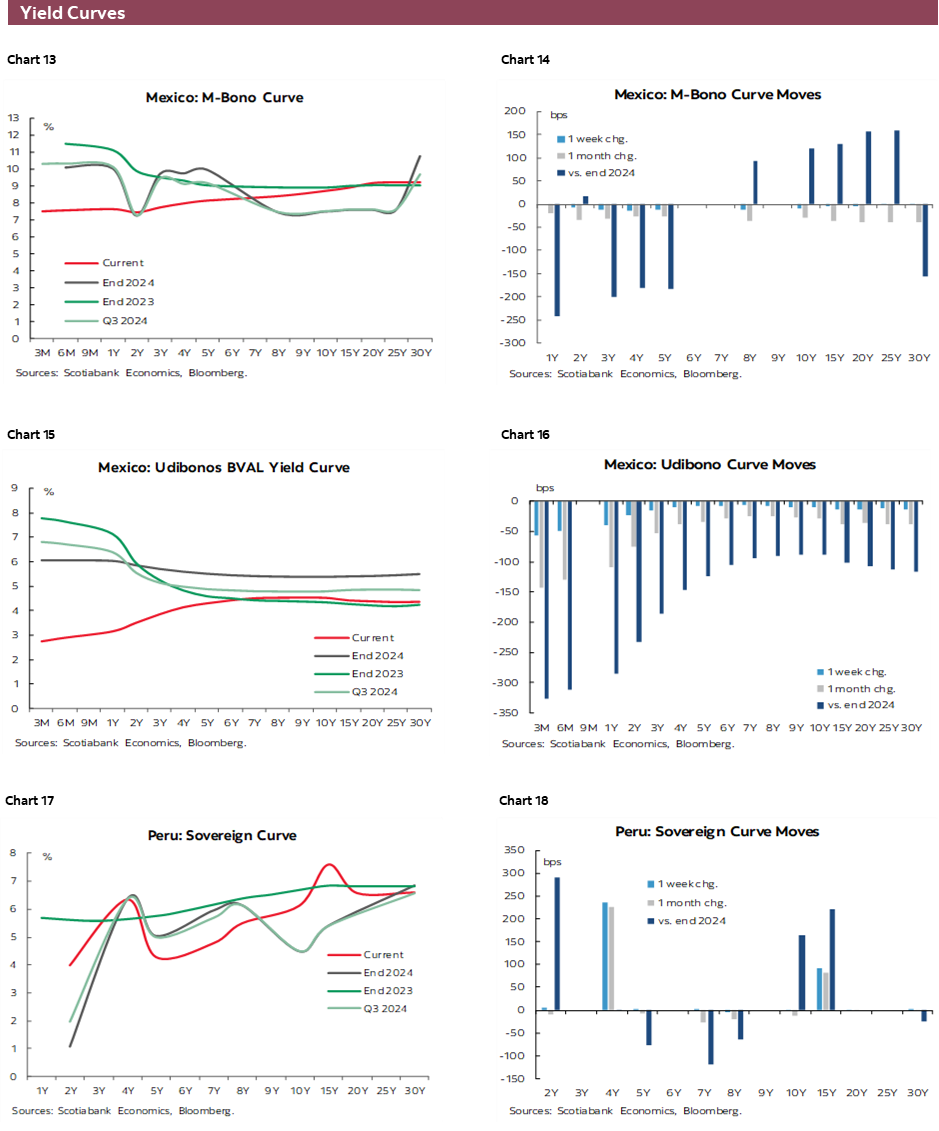

The International Monetary Fund (IMF) published the conclusions of its Article IV technical mission to Mexico. Among the highlights are a revision to the country’s growth outlook for this year and updated public finance estimates, which suggest that public debt could exceed 60% of GDP in the coming years. Regarding monetary policy, IMF experts emphasized the importance of clear signals that inflation is on track toward the target before implementing further rate cuts.

Although the statement acknowledges weak economic activity, the IMF’s growth forecast of 1.0% for this year contrasts with private-sector analysts’ expectations, which stand at 0.4% according to the latest Banxico Survey, despite recent upward revisions. The IMF considers short-term risks to be balanced: downside risks stem from escalating trade tensions, while upside risks include stronger external demand driven by U.S. activity and reduced tariff uncertainty. However, the statement makes limited reference to domestic downside risks in the short-term, such as high political uncertainty, labour market stagnation, and weak internal demand. However, it addresses the importance of fostering rule of law to boost long-term growth.

The IMF also commented on the fiscal policy outlook. The expert committee noted that the proposed 2026 fiscal budget would increase public debt as a share of GDP. According to their estimates, the projected fiscal path implies a rise in debt to 61.5%. In this context, the IMF stressed the importance of creating fiscal space to enable countercyclical responses to economic shocks and to enhance the credibility of fiscal plans. The Fund projects a Public Sector Borrowing Requirement (PSBR) deficit of 2.5% for 2027—one percentage point below the estimate provided by Mexico’s Ministry of Finance in the Fiscal Package. While the IMF acknowledged improvements in tax collection, it also emphasized the need for a comprehensive tax reform to further boost revenues. Additionally, it called for a clear separation between the social objectives of Pemex and CFE and their operational activities, with greater transparency.

On monetary policy, the IMF made relevant observations, especially in light of Banxico’s dovish statement following Thursday’s meeting, where it cut the policy rate to 7.50% without surprises. In this context, the Fund recommended that further easing should only be implemented once there are clearer signs that both headline and core inflation are on a sustained path toward the target.

Peru—With Inflation Low, the BCRP Remains Firmly Within its Comfort Zone

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

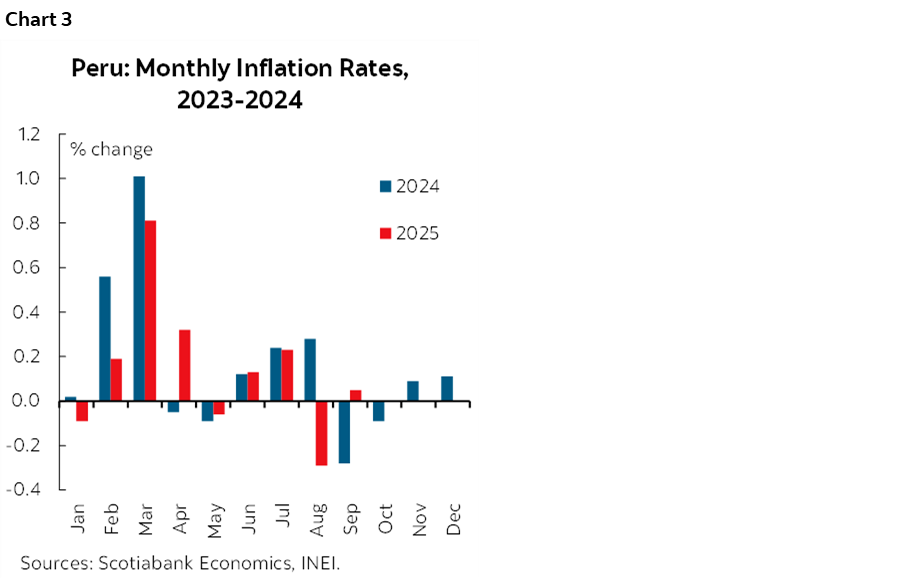

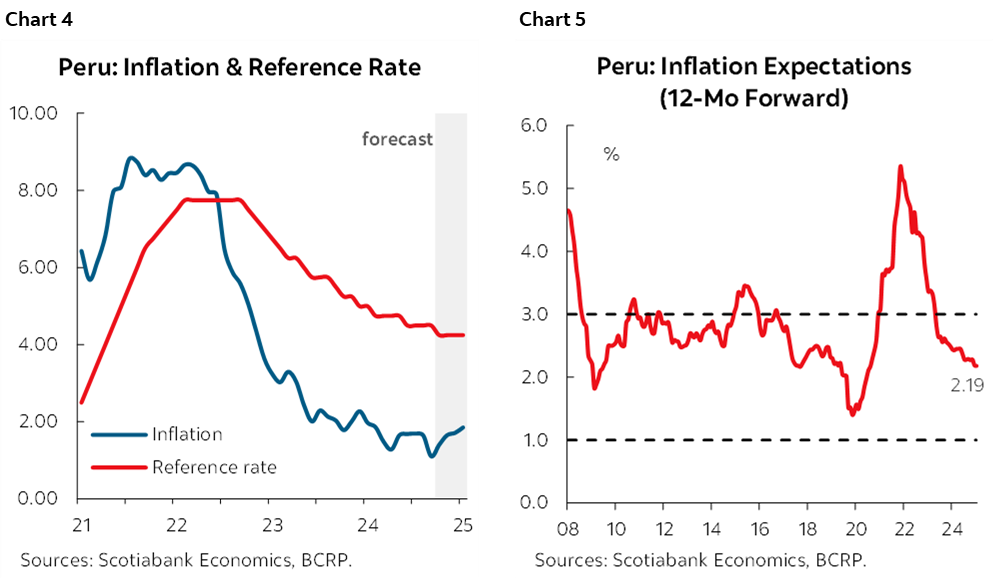

On October 1st, official September inflation figures will be released. The key price figures we are tracking suggest that monthly inflation will come in around nil (0.05% is our latest estimate). This will replace -0.3% inflation in September 2024 (chart 3) and, as a result, yearly inflation should rise from 1.1% last month, to 1.4% for September.

This is in line with our forecast of 1.9% inflation for the full-year 2025. Yearly inflation should rise again in October, as monthly inflation was also negative in October 2024.

The bottom line is that inflation is moving comfortably within the BCRP target range. The question is whether the BCRP, which lowered its reference rate from 4.50% to 4.25% in September, is now also comfortable with the rate where it is. The answer depends on two issues: the Fed rate on the one hand, and inflation expectations in Peru on the other.

The last two times (including September) that the BCRP has lowered its rate, it did so at a time when expectations of the Fed lowering its rate were also high. The more likely the Fed is to lower its rate, and the more aggressive it is in doing so, the more likely it will be that the BCRP will also lower its rate.

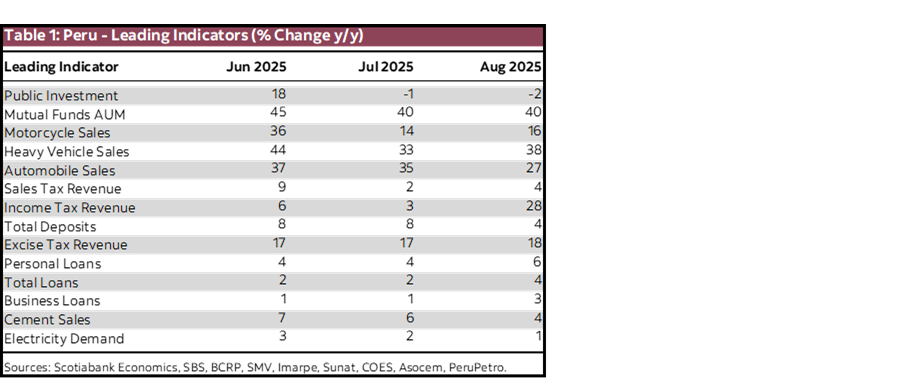

At the same time, however, the BCRP does not really have very much space to lower its reference rate. With inflation expectations at 2.19%, and a neutral real rate of 2.0%, the current reference rate of 4.25% is very close to the nominal neutral level of 4.19% (charts 4 and 5). With GDP growth moderately healthy, the BCRP has no real reason to deviate from this neutral zone. Thus, the possibility that the BCRP may lower its rate again seems contingent on inflation expectations moving lower. Another, more remote, possibility, is that the BCRP lower its neutral rate consideration below 2.0%. There have been periods in the past in which the BCRP has considered a neutral rate of 1.5%.

For now, and until the Fed makes further moves, and/or, inflation expectations decline, our expectation continues to be that the BCRP will maintain its reference rate at 4.25%.

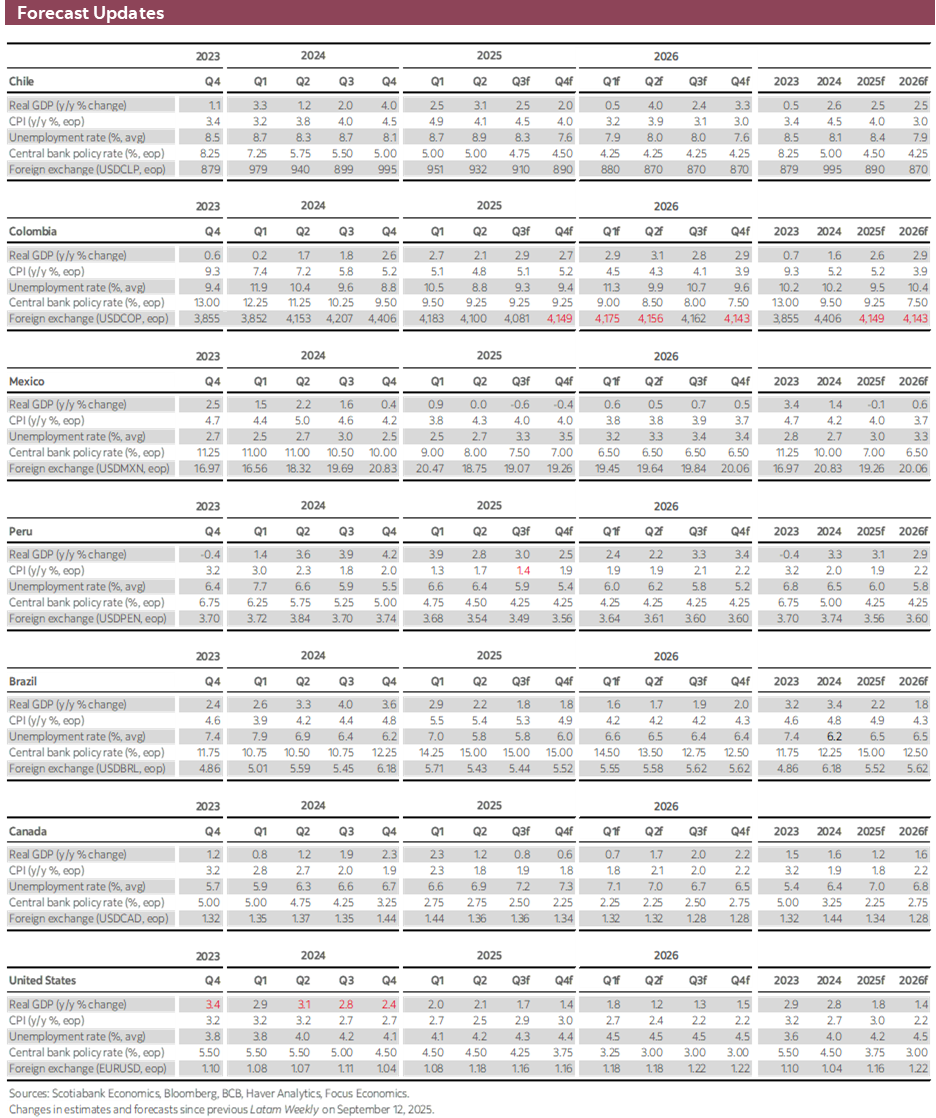

Meanwhile the economy continues cruising along at a moderate clip. Our key indicators for August are very similar to those in July (table 1). In July GDP growth was 3.4%, YoY. However, resource sectors (agriculture, fishing, mining) led in growth in July, rising 4.8% YoY. Our key indicators for August are more aligned with non-resource sectors (linked to domestic demand), which grew at a more moderate 3.0%, YoY, in July. Thus, we expect non-resource sectors to rise around 3.0% in August, once again. The final GDP growth figure for August will depend on the strength of resource sectors, which tend to be more volatile month to month. As an additional note, the deceleration of public investment—a policy decision to contain the fiscal deficit—has started to bear down on growth, as expected.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.