ECONOMIC OVERVIEW

- Sunday’s elections in Chile, Q3 GDP data from across Latam, Banxico and Fed meeting minutes, U.S. jobs data, and G10 CPIs and PMIs all await alongside Nvidia results to shake up anxious markets. Mexican markets are closed for holidays on Monday.

- In today’s report, our team in Chile briefly goes over their expectations for Sunday’s vote and highlight strong forward-looking investment readings. The economists in Colombia discuss BanRep’s latest meeting minutes and chatter around the possibility of rate hikes. Mexican 3Q GDP data may be revised lower according to our local team, while our colleagues in Peru talk about the PEN’s strength in 2025 that has prompted some pushback in markets by the BCRP.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico and Peru.

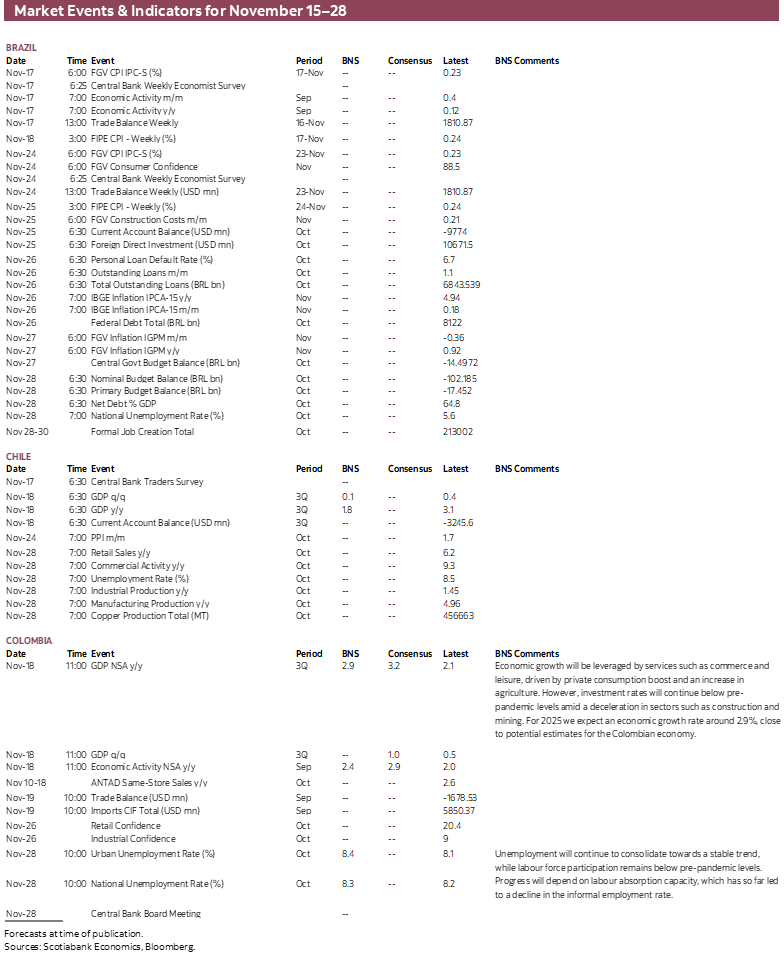

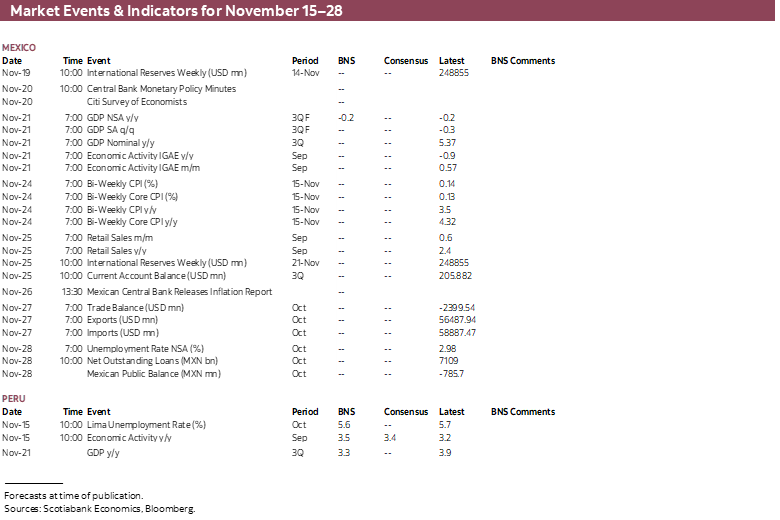

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period November 15–28 across the Pacific Alliance countries and Brazil.

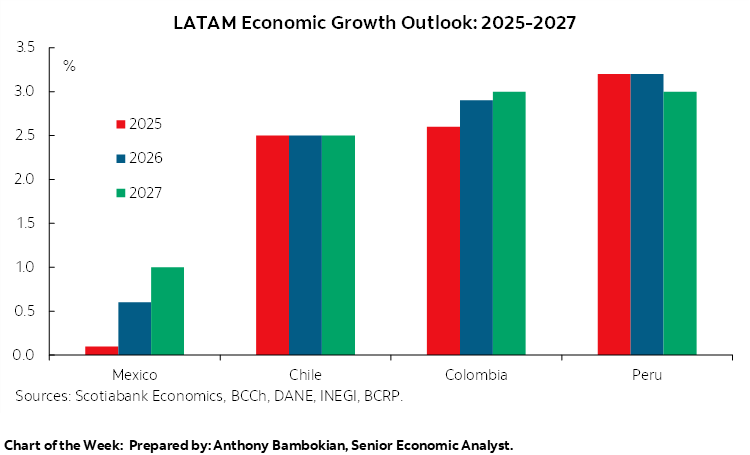

Chart of the Week

ECONOMIC OVERVIEW: CHILE ELECTIONS, LATAM GDP, G10 CPI/PMIs, U.S. JOBS

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Sunday’s elections in Chile, Q3 GDP data from across the Latam region, Banxico and Fed meeting minutes, U.S. jobs data, and G10 CPIs and PMIs all await alongside Nvidia results to shake up anxious markets. Mexican markets are closed for the holiday on Monday.

- In today’s report, our team in Chile briefly goes over their expectations for Sunday’s vote and highlight strong forward-looking investment readings. The economists in Colombia discuss BanRep’s latest meeting minutes and chatter around the possibility of rate hikes. Mexican 3Q GDP data may be revised lower according to our local team, while our colleagues in Peru talk about the PEN’s strength in 2025 that has prompted some pushback in markets by the BCRP.

Markets will have a lot to chew on over the next few days, kicking off the week to the results of Sunday’s legislative and presidential elections on Sunday, to then get a series of key Latam and G10 data that will include September nonfarm payroll figures out of the U.S. thanks to the end of the government shutdown (and perhaps other secondary data). Canadian, U.K., and Japanese CPI are on tap, with global S&P PMIs for November closing out a week that will also include Nvidia’s quarterly results—just in time for markets that are looking anxious about AI-driven gains in equity indices.

In Latam, the focus will be on fresh 3Q GDP readings from Chile, Colombia, and Peru, with Mexico releasing revisions to its preliminary negative reading for the quarter, while Brazil publishes September economic activity data that will give us a good idea for 3Q GDP due in early-December. From Mexico (where markets are closed on Monday), we will also get the minutes to Banxico’s latest meeting, Peru will publish monthly GDP and unemployment data over the weekend, Colombia releases international trade figures and Chile’s central bank publishes the results of its traders’ survey.

Chileans take to the polls this Sunday to cast votes for the next president, the whole of the Lower House, and just under half of the Senate. In today’s report, our local team highlights that markets may be under-pricing the implications of the Lower House vote, with their analysis pointing to the right-wing coalition winning a majority in the chamber, with positive read-throughs to domestic asset prices. This may also be supportive of business confidence, lifting already-strong investment plans which the team also discusses in today’s Weekly.

Voters will pick among eight candidates for the presidency, with none of them expected to obtain the absolute majority of votes needed for victory this weekend, thus requiring a two-way runoff vote on December 14th. Polls point to the runoff vote likely featuring Jeanette Jara from the left against one of Kast or Kaiser from the right (with Kast generally polling better than Kaiser). Aside from knowing who will face Jara next month, Sunday’s results could also act as a strong guide for how December’s vote could go. The latest pre-blackout polls showed that either Kaiser or Kast would defeat Jara, but a stronger than expected performance for the latter could impact these expectations.

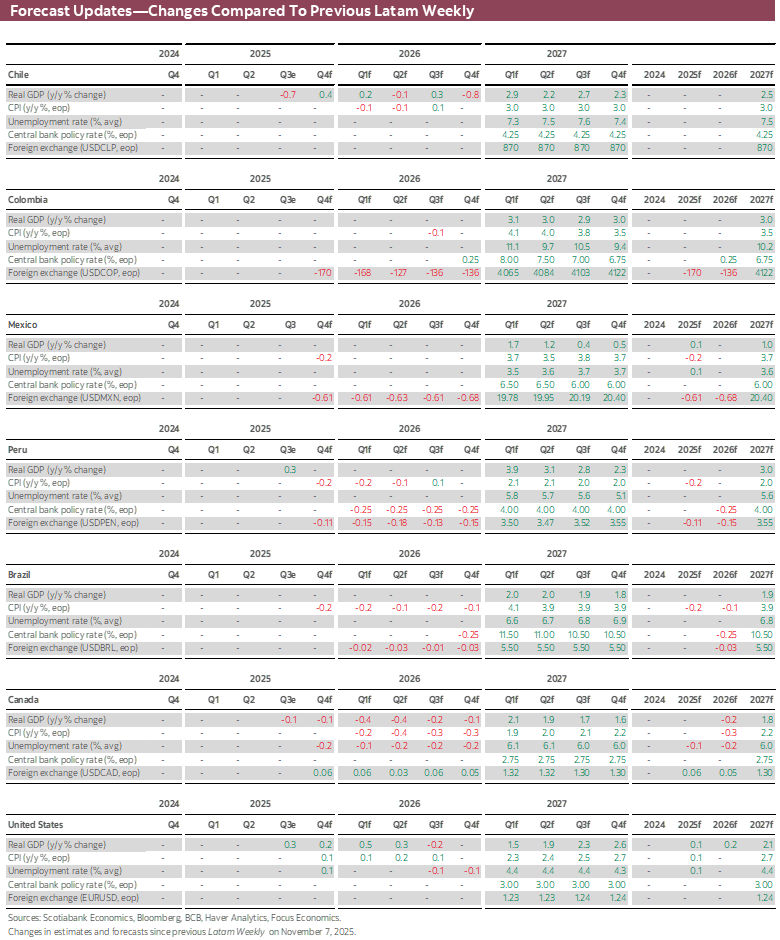

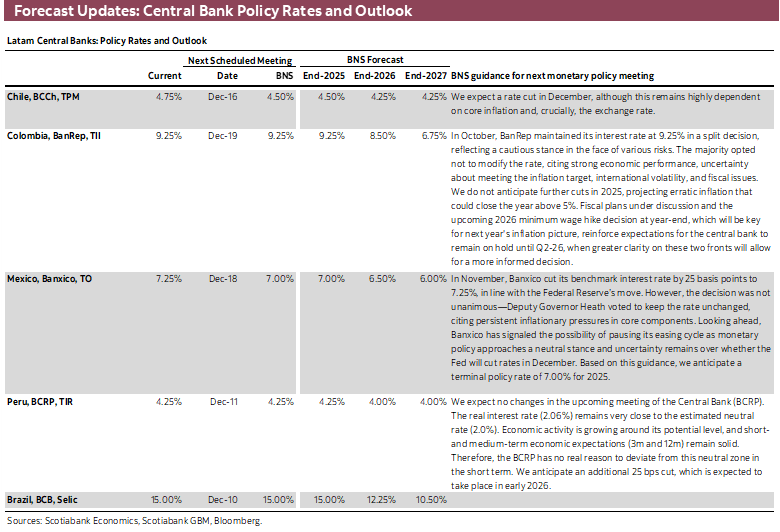

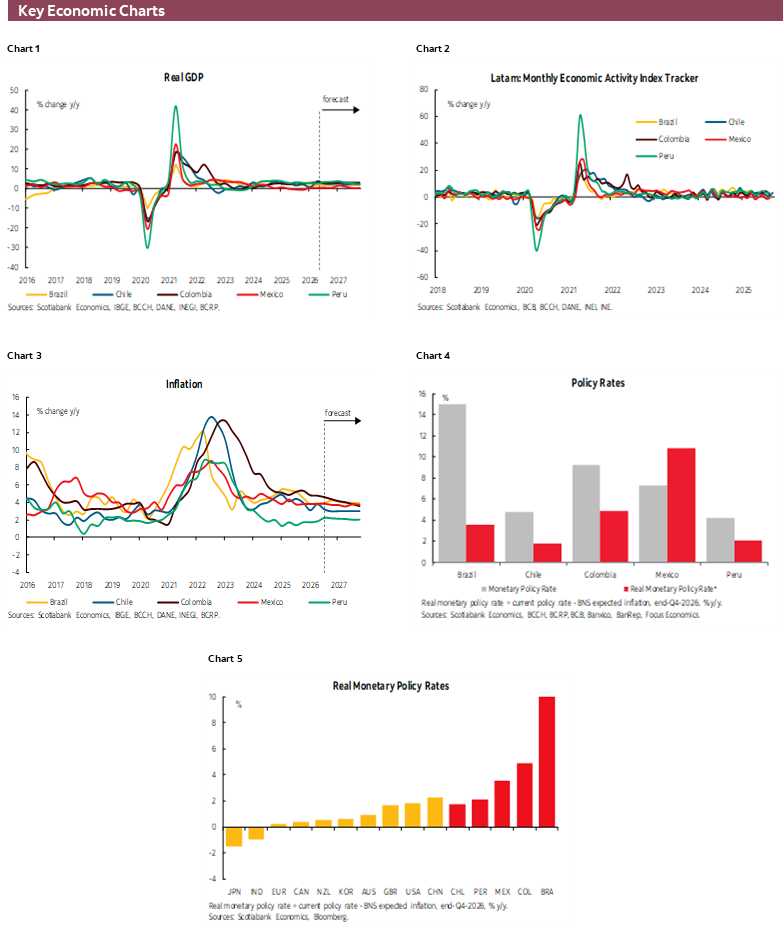

On the GDP front, Tuesday’s 3Q figures should not surprise since we already have monthly economic activity (IMACEC) data at hand. According to the IMACEC, Chile’s economy grew by 1.8% y/y, slowing from the 3.1% y/y expansion seen in 2Q due to a sharp decline in mining GDP of 4.7% related to the temporary shutdown of the El Teniente mine. In contrast, the deceleration in non-mining GDP, from 3% to 2.7% y/y, is a better reflection of ongoing strength in underlying economic conditions. We will also watch the results to the BCCh traders’ survey out on Monday, with the markets pricing in about a 75% chance of a rate cut at the bank’s December 17th meeting.

Colombian GDP is estimated to have accelerated in the third quarter, to around 3% y/y from 2.1% y/y in 2Q. The pickup in momentum has owed to continued improvement in household demand supported by firmer labour markets and international remittances, all while the investment side of the ledger remains disappointing. Colombia’s economy has been resilient despite continuously restrictive monetary policy, which is our team’s topic of discussion in today’s report.

The minutes to BanRep’s latest decision highlighted that some on the board requested that the possibility of rate hikes not be dismissed, a scenario that has now become the market’s central case with a couple of rate cuts priced up to mid-2026. Our economists in Colombia highlight the mismatch between the cautious views among BanRep policymakers gleaned from the meeting minutes and those reflected in the bank’s staff’s forecasts that may underestimate inflationary risks due to neutral assumptions on next year’s minimum wage increase. We continue to expect that the next BanRep rates move will be to the downside and think it would take material changes to inflation forecasts and neutral range estimates for the bank to consider higher rates.

Saturday’s September GDP reading out of Peru should clean up expectations for next Friday’s 3Q release. We estimate that the country’s economy expanded by around 3.5% at the close of the quarter, to translate into a 3.3% y/y 3Q rise in GDP, down from the 3.9% gain in 2Q. Overall, growth remains firm, roughly settling around a 3% annual pace outside of some base effects and choppiness in resource sectors. Macroeconomic data continue to justify an on-hold stance by the BCRP, as ratified with yesterday’s unchanged rate decision.

The BCRP is, however, perhaps a bit more concerned about PEN strength throughout 2025, as discussed by our Lima economists in today’s note. The central bank has already intervened in currency markets twice this month, after a five-year-plus hiatus, to send traders a signal that it is uncomfortable with the Sol’s appreciating trend. The team goes over the three main factors driving the PEN’s gains this year and their expectations for some weakening into year-end, with some risks for the currency ahead of the April 2026 election.

Mexican economic figures have been particularly poor of late and, according to our economists, next week’s second release of 3Q GDP data will probably show a deeper contraction than the 0.2% y/y drop initially reported. Industrial production data published since the preliminary GDP print, with the sector stringing y/y declines for over a year (with the exception of March 2025) including a 2.4% y/y drop in September. Muted job gains, declining remittances, and soft consumer confidence are all factors behind Mexico’s disappointing economic performance for 2025, with GDP on track to barely expand this year and only post a weak gain in 2026.

Banxico’s meeting minutes due on Thursday will be monitored for signs that there could be some in the Board, aside from Dep Gov Heath, that may soon consider voting for a rate hold. The latest decision statement (see our take here) included a small tweak to rates guidance that has opened the door to the bank holding as soon as December—although this looks unlikely. Comments from Banxico officials in the days that followed their rate decision have also broadly suggested that a rate hold will not be under serious consideration at their final meeting of they year, but the minutes may offer some colour on what data or developments could motivate a pause—and when.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—On Track to See Investment Growth of 6% in 2025. For Next Year, the CBC Survey Already Incorporates USD 20.9 bn.

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

On Wednesday, November 12th, the Capital Goods Corporation (CBC) released its Q3-25 survey, which revealed a notable increase in the total amount of expected investment to be materialized over the next five years (2025–2029), reaching USD 78.96 bn, up from USD 74.12 bn in Q2-25. This 6.5% increase was mainly driven by new energy projects, particularly in generation and storage, which added USD 2.3 bn (+15%) to the sector’s pipeline.

Investment is concentrated in four key sectors. Mining leads with 34% of the total, followed by public infrastructure at 27%, energy at 23%, and real estate at 9%. Mining and energy are largely private-driven, while public works show a more balanced mix of public and private funding. Real estate investment is entirely private.

By 2025, the total amount of investment to be materialized (with defined schedule) rose to USD 24.1 bn (+2%), while projections for 2026 and 2027 were also revised upward by 7.7% and 13%, respectively. In our baseline scenario, fixed investment is expected to remain resilient, supported by strong momentum in energy, mining, and public infrastructure. This information reinforces our forecast of a 6% increase in investment for 2025 and could prompt the central bank to revise its own projection upward once again (currently at 5.5%).

We expect the right-wing coalition to achieve a majority at the lower house for the first time since the return to democracy.

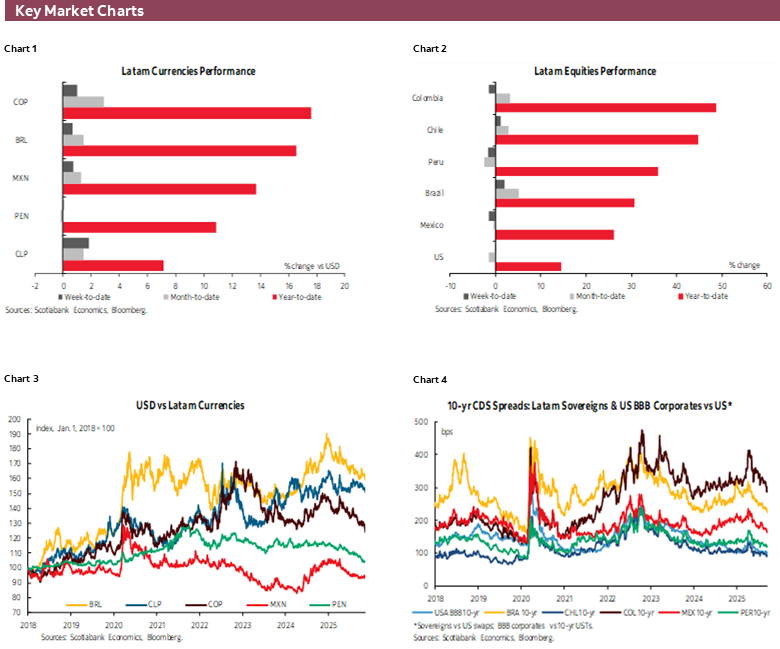

The time has come: Chile heads to the polls this weekend. According to our analysis (see our Latam Insights), the 2024 councillor election results point to a potentially transformative political shift in Chile. Although the market has eased the penalty on local assets in recent days, showing a performance orthogonal to that of emerging economies, markets may not be fully pricing in the legislative implications, leaving room for repricing following the 2025 parliamentary elections—especially if a right-wing majority in the Lower House is confirmed.

If this materializes, in the coming weeks we could observe a market dynamic favourable for local assets, including appreciation of the Chilean peso, a re-rating of domestic equities—particularly in sectors sensitive to regulatory reform—and a compression of sovereign and corporate credit spreads, reflecting an improved fiscal and policy outlook. These adjustments would signal a shift in investor sentiment toward local assets, supported by reduced risk premiums and expectations of greater macroeconomic stability.

Colombia—The Debate About Hikes to the Policy Interest Rate

Jackeline Piraján, Head Economist, Colombia

+57.601.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Valentina Guio, Senior Economist

+57.601.745.6300 Ext. 9166 (Colombia)

daniela.guio@scotiabank.com

Last week, the central bank released the minutes of its October monetary policy meeting, where the board decided to keep the policy interest rate at 9.25%, maintaining the same divided vote observed in previous meetings: four members voted to keep the rate unchanged, two supported a 50 basis point (bp) cut, and one favoured a 25 bp reduction. Additionally, the economic staff published the quarterly Monetary Policy Report (MPR), providing a new set of macroeconomic projections.

The key takeaway from both publications is that, according to the minutes, one part of the board explicitly requested not to dismiss the possibility of rate hikes. Meanwhile, the MPR’s inflation projections assume a significant minimum wage increase based on the technical rule of inflation plus productivity, with risks tilted upward for inflation and negatively skewed for economic activity.

Overall, these documents suggest that monetary policy will remain in a contractionary stance for longer than previously expected. At Scotiabank Colpatria, we still do not see a case for rate hikes in the near term. Although the minimum wage increase is at the centre of the debate, we believe a hike would only be triggered if the structural trend of inflation changes—likely requiring an additional shock beyond a potential 11–12% increase in the minimum wage.

About the discussion in the minutes:

The behaviour of inflation would require maintaining a restrictive stance for a longer period. Several board members who voted to keep the policy rate unchanged indicated that future rate hikes could be considered if certain risks—currently not part of the baseline scenario—materialize. In addition, the strengthening of domestic demand, reflected in a significant widening of the current account deficit, has been driven by higher public spending (fiscal deficit at 5.1% of GDP as of August), increased remittances, and high coffee prices. This points to a risk balance that justifies maintaining caution for an extended period.

The minority group of the Board argued that there is room to accelerate rate cuts and questioned Colombia’s inflation structure. The board members who voted for a 50 bp cut stated that the current interest rate is sufficiently restrictive to allow for reductions, adding that there are inflationary sources beyond the control of monetary policy, such as food and regulated prices. Along these lines, the member who voted for a 25 bp cut explained that Colombia’s inflation structure is largely driven by supply-side factors rather than demand, which means that a restrictive monetary policy in this context could have adverse effects on the recovery of economic growth.

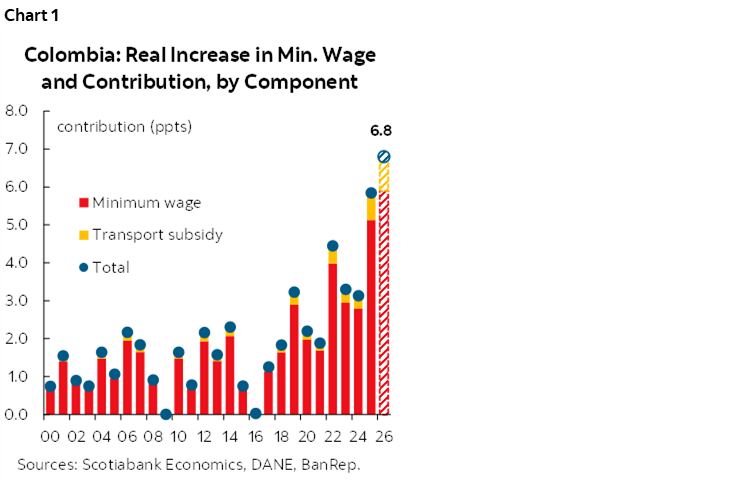

The Board’s disagreement over the minimum wage increases for 2026. On several occasions, government officials have suggested the possibility of raising the minimum wage by more than 11% in 2026, which would result in a real increase of 6.8 ppts—the highest seen in the past 26 years—which would stand as an attractive measure during the administration’s final year (chart 1). The majority group argued that this could increase the rigidity of core and regulated inflation, undermining the credibility of the bank’s inflation-targeting framework. In contrast, part of the minority group argued that, following the real wage increase since 2022, reductions in inflation and growth in employment have been observed, which should not be dismissed despite empirical estimates suggesting otherwise (see here).

The behaviour of the exchange rate is part of the risk balance considered by the entire Board. So far in 2025, the exchange rate has appreciated by 16%, driven by wider monetary policy rate spreads between Colombia and advanced economies, which has encouraged portfolio inflows (carry trade). In addition, significant government monetizations—~USD 4.2 bn between September and October—have contributed to this trend. The majority group noted that this exchange rate behaviour could reverse amid potential increases in risk premiums stemming from greater external imbalances, while the minority group highlighted that stronger currency appreciation could increase financial vulnerability. These arguments open the discussion on the temporary nature of the movement and potential inflationary pressures once this trend reverses.

The Monetary Policy Report points to mixed risks: upside for inflation and downside for growth

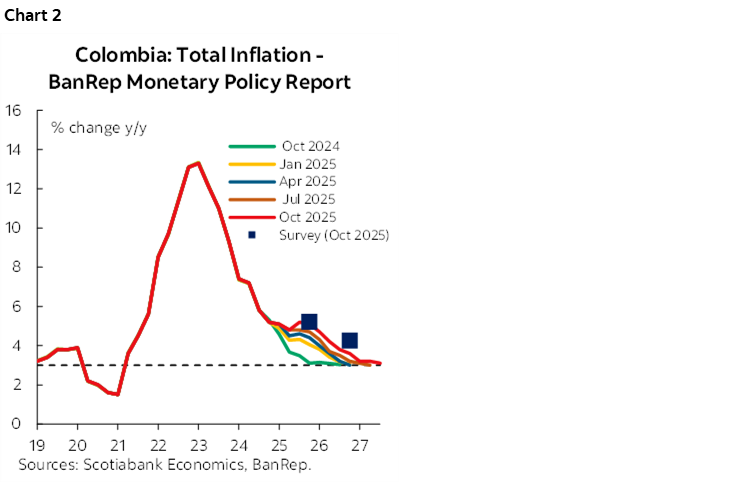

In its recently published Quarterly Monetary Policy Report, the central bank’s staff revised its inflation forecasts upward: from 4.7% to 5.1% for year-end 2025, and from 3.2% to 3.6% for 2026 (chart 2). This reflects inflationary risks related to greater indexation through the minimum wage in 2025 and uncertainty around regulated and food prices. Ahead of 2026, the projection assumes that the minimum wage increase will follow the technical rule inflation plus productivity (~6%), which has an evident upside risk given government’s communication.

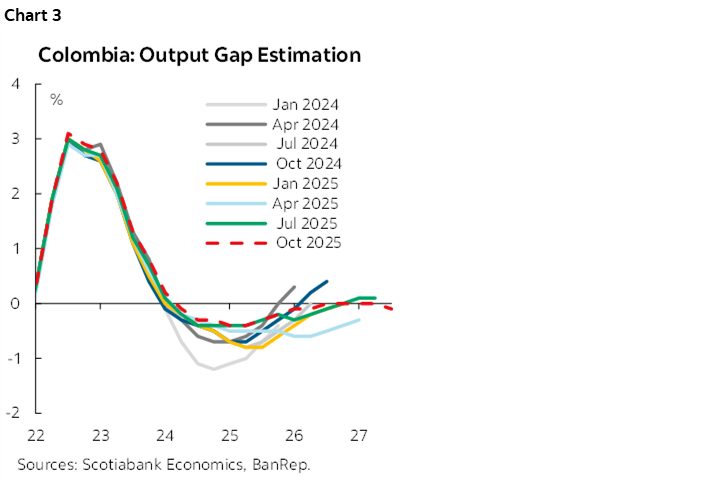

Additionally, the staff expects economic growth to accelerate from 1.6% in 2024 to 2.7% in 2025 and 2.9% in 2026—similar to Scotiabank Colpatria’s projections—with the output gap closing in 2026 amid stronger domestic demand (chart 3). Meanwhile, the neutral real policy rate remained unchanged at 2.7% for 2025 and 3.1% for 2026.

Staff projections differ from the Board’s views. On one hand, the majority group advocating for greater caution contrast with the staff projections that at first glance are more conservative. However, it has an explanation in that the staff is assuming what technical rules suggest for the minimum wage increase (i.e. lower than risks point to), while a majority of the BanRep’s board can think on the political risk of having a higher adjustment. On the other hand, the minority group is even questioning the current monetary policy target range of 2% to 4%, while also downplaying the impact of the minimum wage on inflation. This discord has been reflected in a clearly divided vote within the Board, which is expected to persist until its composition changes.

Recent inflation data confirm that monetary policy will remain restrictive for longer than expected. In October 2025, headline inflation rose from 5.18% in September to 5.51% y/y, exceeding analysts’ expectations, with housing and utilities, as well as restaurants and hotels, accounting for 89% of the total increase. Core inflation also moved higher: inflation excluding food rose from 4.94% to 5.51% y/y, while inflation excluding food and energy accelerated from 4.84% to 4.99% y/y (see here). Given evident inflationary pressures and their impact on inflation expectations, a restrictive monetary policy stance is expected to persist for longer. For this reason, Scotiabank Colpatria anticipates a policy rate of 9.25% through the first half of 2026, which in real terms—averaging the ex-ante and ex-post rate—would reach 4.1% by year-end 2026.

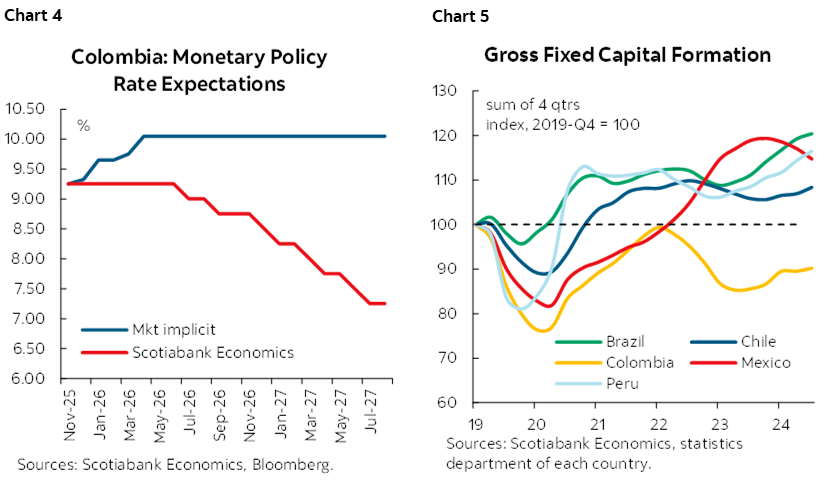

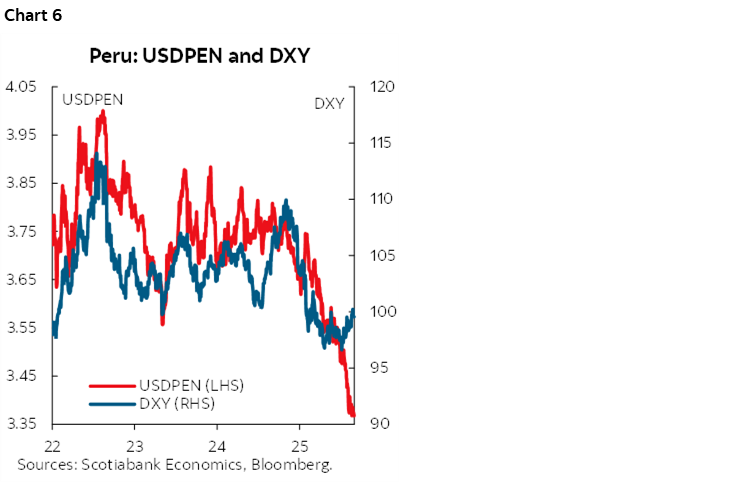

The risk balance that could lead to interest rate hikes remains unclear. While market expectations are pricing rate increases by mid-2026 (chart 4), Board members have stated that the justification for such hikes goes beyond minimum wage decisions. Factors include a prolonged period during which the staff’s inflation expectations exceed the target range in 2026, and even a reversal of the downtrend anticipated for next year, combined with an increase in estimates of the neutral real rate that would force the bank to raise rates if it wishes to keep the level of contractive policy unchanged in the face of inflation remaining outside the target range. It is worth noting that, historically in Colombia, decisions to raise interest rates are contentious because they have direct implications for capital-intensive sectors such as construction, mining, and industry, which rely heavily on private financing—especially given that the country still faces a 10% investment gap compared to pre-pandemic levels, while other regional economies have advanced (chart 5).

Mexico—GDP Weakness Driven by Industrial Activity

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

This week, we’ll get the full details on Q3 GDP. The initial estimate pointed to an annual drop of -0.2%, but the latest industrial production data suggests the contraction could be even deeper.

Existing GDP figures for Q3 already showed signs of weakness: activity slipped from 0.0% in April–July to -0.2% in August–September, leaving year-to-date growth at just 0.2%, thanks to the 0.9% boost at the start of 2025. The slowdown is mainly in industry, which has been posting annual declines since late last year, driven by rising uncertainty at home and abroad, pauses in investment, and lower public spending. In the early Q3 estimate, services grew 1.0% year-over-year, primary activities rose 3.6%, while industry fell -2.9%. Monthly industrial production data gives us a closer look at secondary activities through September.

On a monthly basis, industrial activity dropped -2.4% year-over-year in September, marking consecutive declines since August 2024—except for March 2025, when tariff news may have temporarily boosted some export-oriented manufacturing subsectors. As of September, industry shows a cumulative annual drop of -1.8%. From January to September, all four main components posted declines: mining at -8.4% (mostly oil extraction), negative since late 2023; utilities (electricity, gas, water) at -1.1%; construction at -2.7%; and manufacturing, with mixed performance, at -0.5%.

In construction, the hardest-hit subsector has been heavy works, with a steep cumulative fall of -26.7%, while building construction shows a modest but positive increase of 3.0%. In manufacturing, the picture is mixed: the most affected subsector, transportation equipment, saw a sharp drop of -10.1% in September alone, and a cumulative decline of -4.9%, mainly due to the collapse in heavy vehicle production. Light vehicle output has been more stable but faces challenges as several automakers announce plans to adjust production lines in the medium term.

Taking this industrial breakdown into account, plus signs of moderation in services—hit by weak private consumption due to slow job creation, lower remittances, and stagnant consumer confidence—we don’t expect major downward revisions in this week’s GDP data. Still, it will confirm a tough outlook for year-end. After the final Q3 estimate, many analysts will likely revise their growth forecasts downward.

Peru—BCRP Sends Warning Signals Amid Persistent Currency Gains

Ricardo Avila, Senior Analyst

+51.1.211.6000 Ext. 16558 (Peru)

ricardo.avila@scotiabank.com.pe

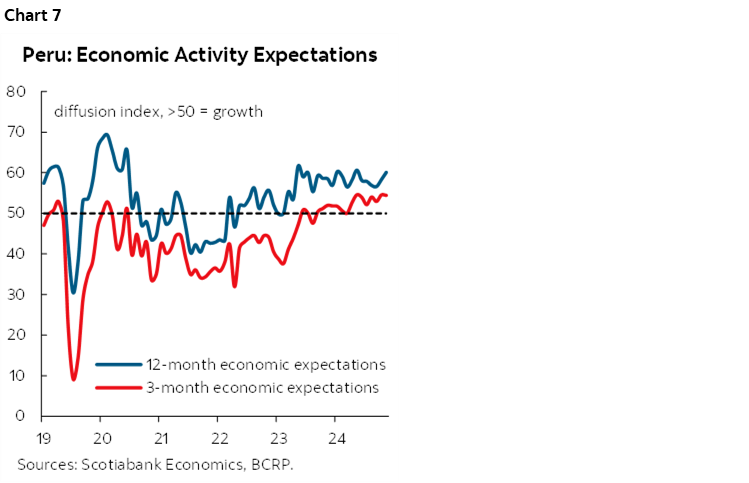

The USDPEN exchange rate has reached its lowest level in five and a half years (since April 2020). The PEN has appreciated by 10.4% so far in 2025, driven by three main factors (chart 6):

- High precious metal prices: Year-to-date, gold prices have surged by 57%, while copper has gained 24%. This has led to a record trade balance, supported by higher foreign currency inflows into the country.

- A weaker U.S. dollar globally (DXY): The dollar index has trended downward throughout the year, remaining below 100 points since Q2 2025. Although it recently corrected, the DXY remains weak, posting an 8.2% decline year-to-date.

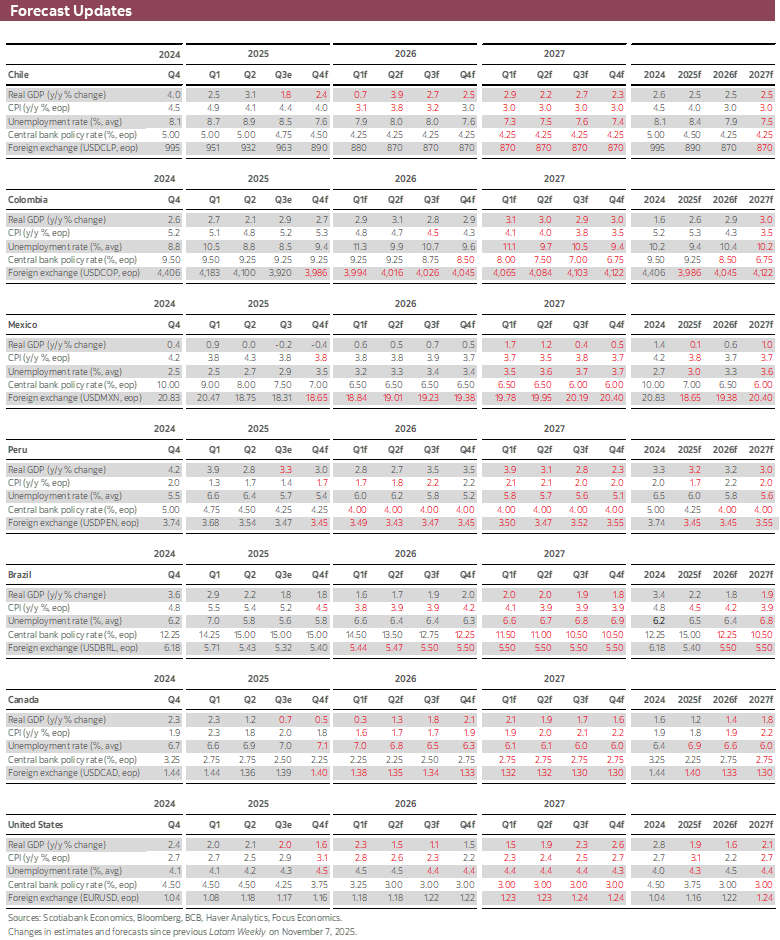

- Greater foreign capital inflows into local assets: This reflects Peru’s macroeconomic strength (chart 7). The supply of dollars to purchase local currency bonds has exerted downward pressure on the exchange rate.

Over the past two years, the PEN has been the most appreciated currency among its regional peers. Since late 2023, the PEN has strengthened by 9%, compared to a 3% gain for the COP. In contrast, the CLP weakened by 7%, the MXN by 8%, and the BRL by 9%. The PEN’s sharp appreciation could impact export competitiveness and domestic production by making imports cheaper.

Recently, the BCRP intervened twice in the spot market after a five and a half years break (since April 2020). The first intervention occurred on Wednesday, November 5th, with a spot purchase of $27 million. The second took place on Tuesday, November 11th, with a spot purchase of $77 million. Both transactions were executed at an exchange rate of 3.36 per dollar. Although the amounts were not significant, the BCRP aimed to signal caution regarding the magnitude of the PEN’s appreciation.

Market expectations for 2026, according to LatinFocus, show a wide dispersion. While the consensus stands at around 3.60 per dollar, the minimum estimate is 3.20 and the maximum is 3.85. This range reflects a high degree of uncertainty among economic agents, linked to external factors (such as metal prices) and internal factors (such as the general election on April 12th), which could influence the exchange rate trajectory.

We estimate the exchange rate will be around S/3.45 at the end of 2025 and 2026. We expect metal prices to remain elevated next year and the DXY, which has already corrected, not to weaken as much as in 2025. Although the DXY has recently decoupled from the sol, we expect the correlation to reestablish in the short term, leading to a depreciation of the local currency. The main risk lies in the general election, which could exert upward pressure from late Q1 2026, though this may be offset by the tax payment season. Our baseline scenario assumes the new government will maintain an investment-friendly stance and continue responsible macroeconomic policies.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.