- We expect the right-wing coalition to achieve a majority at the Lower House for the first time since the return to democracy

Current market dynamics suggest that investors are increasingly pricing in a likely victory for the right-wing presidential candidate in Chile’s upcoming election. This expectation is supported by consistent polling data and prediction markets, which indicate a high probability of a right-wing win in the second round. Historically, markets have reacted positively to expectations of pro-business governance, and current pricing appears consistent with that pattern.

However, markets appear to be overlooking a second, less certain but highly relevant scenario: the possibility that the right-wing coalition secures a majority of members in the Lower House of Congress for the first time since Chile’s return to a democratic system in 1990. In this note, we put forward that the two coalitions representing the center-right voters (Chile Grande y Unido and Cambio por Chile) will get “no less than” 50% of the seats in the Lower House, a scenario that we consider is not internalized in Chilean asset prices.

Recent surveys consistently show that any right-wing candidate—whether José Antonio Kast or Evelyn Matthei—would defeat the incumbent government-backed candidate, Jeanette Jara, in a second-round runoff.1 This trend is also corroborated by Polymarket pricing, where contracts for a right-wing victory in the presidential race trade at a significant premium, reflecting market confidence in this outcome. While these signals provide a strong anchor for expectations regarding the presidency, they do not extend to congressional races.

We are two months away from the election of Chile’s next president, under mandatory voting.2 The first round of the 2025 presidential election will take place on Sunday, November 16th, while the runoff between the two highest-voted candidates is scheduled for Sunday, December 14th. This year, the entire Lower House (155 seats) and half of the Senate will also be renewed (23 of 50 seats), with only one round of voting taking place on November 16th. Currently, the ruling coalition does not have a majority in either chamber. In the senatorial elections, 10 seats held by the center-left and 13 by the center-right must be elected. These elections will be under mandatory voting, as has been the case since 2022 following the Constitutional Plebiscite.

While presidential outcomes dominate headlines, legislative dynamics are equally critical for policy execution. A fragmented Congress has historically constrained reform agendas, regardless of the president’s political alignment.

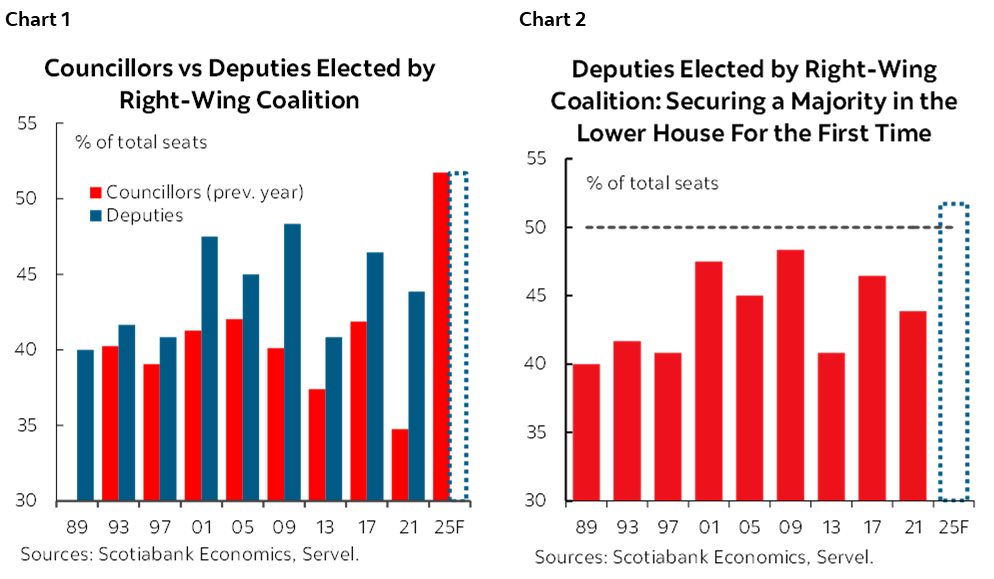

However, the 2024 municipal elections—particularly the strong performance of right-wing parties in councillor races—signal a potential realignment at the parliamentary level. If replicated in the upcoming legislative elections, this could grant the center-right coalition an outright majority in the Chamber of Deputies, an unprecedented development in the post-1990 democratic era.

Municipal elections—particularly the vote for councillors—have historically served as a strong leading indicator of subsequent parliamentary elections. The comparative data between councillor and deputy elections from 1989 to 2025 (charts 1 and 2) confirms a consistent pattern: vote shares in councillor elections tend to anticipate the composition of the Lower House one year later. For our analysis, we used the official Electoral Service results for the councillors and deputy elections, considering the parties that formed part of the right-wing coalition in each election.

In the 2024 municipal elections, the right-wing coalition achieved its best electoral performance since the return to democracy, far exceeding the percentage of councillors elected in previous years. If this historical correlation holds, the 2025 parliamentary elections could result in the first-ever majority for the right in the Chamber of Deputies, exceeding 50% of seats.

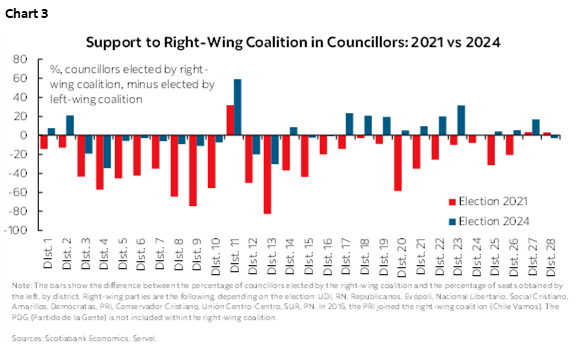

The strongest support for the right-wing coalition is observed even in districts that have historically been predominantly center-left and that elect the largest number of seats (eight each), such as Districts 6 and 7 in the Valparaíso region, Districts 8 and 93 in the Metropolitan region, and District 20 in the Biobío region.

The advance of the right in districts historically dominated by the center-left is not an isolated phenomenon but part of a broader trend of electoral realignment, as seen in the results of the recent councillors’ elections (chart 3). The coalition’s ability to consolidate in high-magnitude constituencies—such as Districts 6 and 7 in Valparaíso, 8 and 9 in the Metropolitan region, and 20 in Biobío—is politically significant: these territories concentrate urban populations, middle-class sectors, and areas historically linked to the Concertación and the Frente Amplio.

In 2021, for example, in District 6 (Valparaíso interior) the right secured 3 out of 8 seats, and in District 8 (Maipú, Cerrillos, Estación Central) it reached 3 out of 8, breaking the progressive hegemony. A similar outcome occurred in District 20 (Concepción and surrounding areas), where the right obtained 4 out of 8 seats—a result unthinkable a decade ago.

This pattern reflects a structural shift: issues such as security, migration, and disaffection with traditional parties have driven a more conservative vote even in urban areas that were once left-wing strongholds. At the macro level, this anticipates a more fragmented Congress and a legislative agenda where the right would hold veto power in key areas.

In Chile’s upcoming 2025 parliamentary elections, the right-wing political sector is expected to compete via two separate coalitions—Chile Grande y Unido and Cambio por Chile—rather than presenting a unified electoral front. This fragmented approach may limit their ability to optimize seat allocation under the D’Hondt proportional representation system, which tends to favour larger, consolidated lists. Nevertheless, the left-wing parties are also expected to run on separate lists, which could offset the advantage typically gained from a broad coalition. As a result, the positive effect of list consolidation may be neutralized for both political blocs.

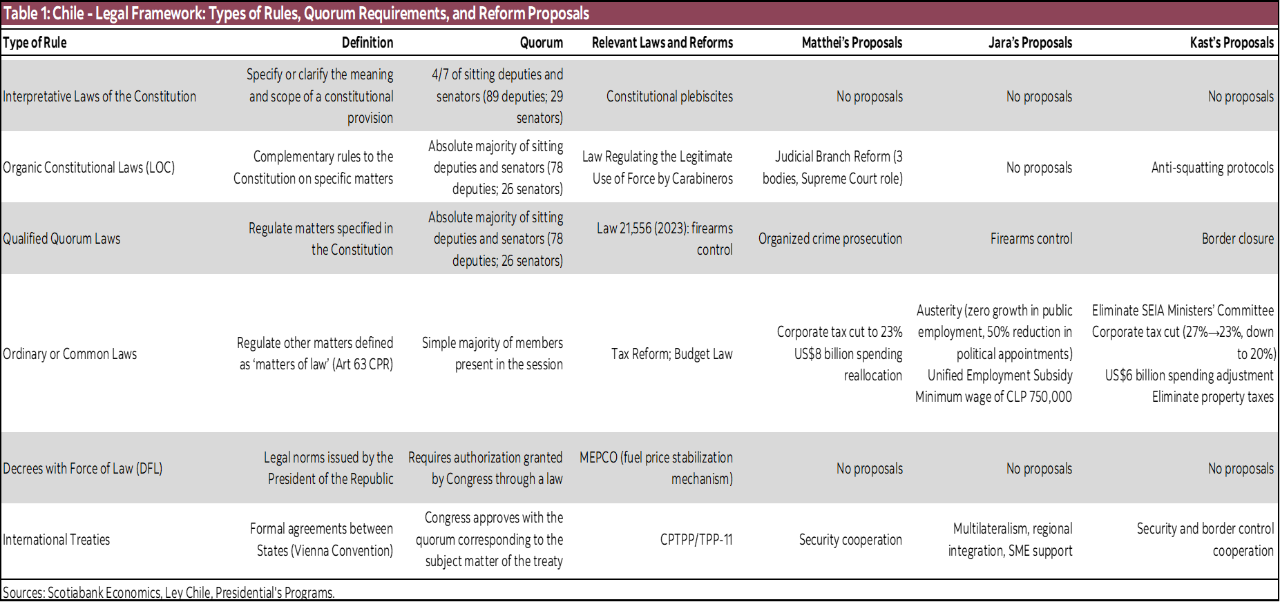

Such a majority in the Lower House would allow the coalition to pass legislation without needing support from the left-wing parties. Examples of laws that could be approved under this scenario include (table 1):

- Tax reforms aimed at stimulating investment and reducing corporate burdens.

- Labour market flexibility measures to enhance competitiveness.

- Fiscal consolidation and investment initiatives.

- Security and migration legislation aligned with conservative platforms.

While asset prices likely already reflect expectations of a right-wing victory in the 2025 presidential election, they do not appear to fully incorporate the possibility of a legislative majority, particularly in the Lower House. This is suggested by the current valuation discount observed in Chilean equities and the exchange rate, which may reflect residual uncertainty around legislative governability. If the right does secure a legislative majority, the alignment between executive and legislative branches would reduce political risk and facilitate policy implementation. This could lead to:

- Appreciation of the Chilean peso, as political uncertainty diminishes.

- Re-rating of domestic equities, particularly in sectors sensitive to regulatory reform.

- Compression of sovereign and corporate credit spreads, reflecting improved fiscal and policy outlook.

In summary, the 2024 councillor election results point to a potentially transformative political shift in Chile. Yet, markets may not be fully pricing in the legislative implications, leaving room for repricing following the 2025 parliamentary elections—especially if a right-wing majority in the Lower House is confirmed.

1 Cadem (September 7th) second round scenarios: Jara (32%) vs Kast (42%); Jara (32%) vs Matthei (43%). Criteria (September 28th) second round scenarios: Jara (35%) vs Kast (44%); Jara (34%) vs Matthei (39%).

2 While voting is mandatory, no sanctions will be applied to eligible foreign residents. Nonetheless, turnout among the nearly 900,000 registered foreign voters is expected to remain robust. Consequently, participation rates are projected to be broadly in line with the previous electoral cycle.

3 In the 2021 election, Communist Party (PC) deputy Karol Cariola secured a seat for fellow party member Boris Barrera in District 9 through the D’Hondt system. A similar outcome was anticipated this year with Daniel Jadue heading the list. However, his disqualification creates room for a potential realignment in the district, favouring center-right candidates.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.