- Resilient domestic sales: In 2025, light-vehicle sales grew 1.4%, reaching 1.52 million units, their highest level since 2017, driven by new competitors, although with a lower official market share for Chinese brands

- Production and exports in decline: Light-vehicle production fell 0.9% and exports dropped 2.7% in 2025, affected by trade uncertainty with the U.S., input shortages, and strategic adjustments by automakers

- Heavy vehicles in sharp contraction: Heavy-vehicle sales fell by nearly one third, with drops of up to 51% in wholesale sales and 34% in production, reflecting low investment and high uncertainty

- Forward-looking risk factors: Tariffs on Chinese vehicles (50%) and on Mexican heavy vehicles in the U.S. (25%), along with lower investment and stalled formal employment, will limit demand

- 2026 outlook: The industry will most likely face challenges from trade volatility, input shortages, and low investment, but also opportunities from nearshoring, technological shifts, and new players in the domestic market

DOMESTIC DEMAND: SLIGHT RISE IN SALES

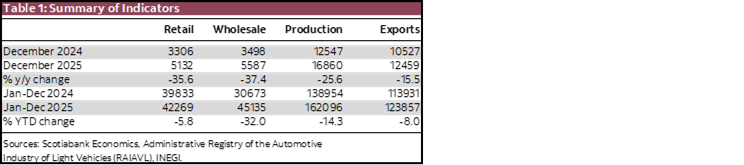

Mexico’s automotive industry faced a deterioration in the outlook for light vehicles during 2025, with significant declines in production and exports, accompanied by a widespread collapse in heavy vehicles. Domestic light-vehicle sales were the only indicator that showed growth during the year (table 1).

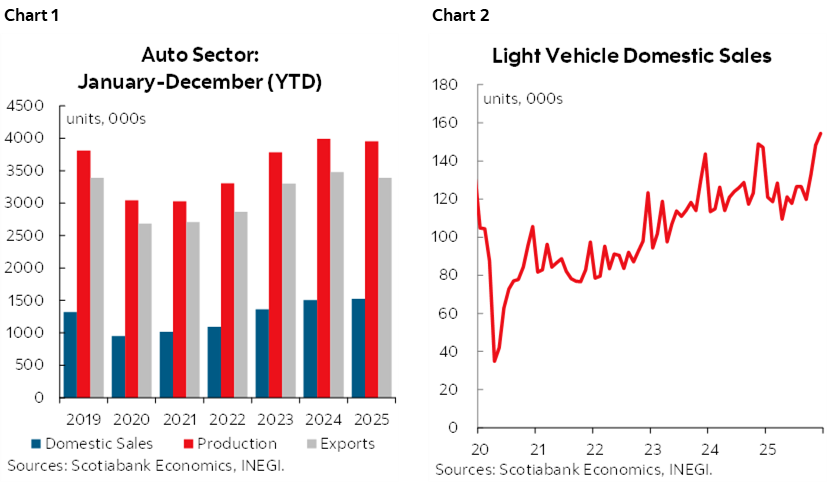

In December, domestic sales of light vehicles grew 5.0% annually, rebounding from the -0.3% drop in the previous month. With this positive close, domestic sales averaged 1.4% growth throughout 2025, totaling 1,524,638 units (charts 1 and 2). This is the highest level since 2017 (1.534 million units) and approaches the historical record of 2016 (1.607 million).

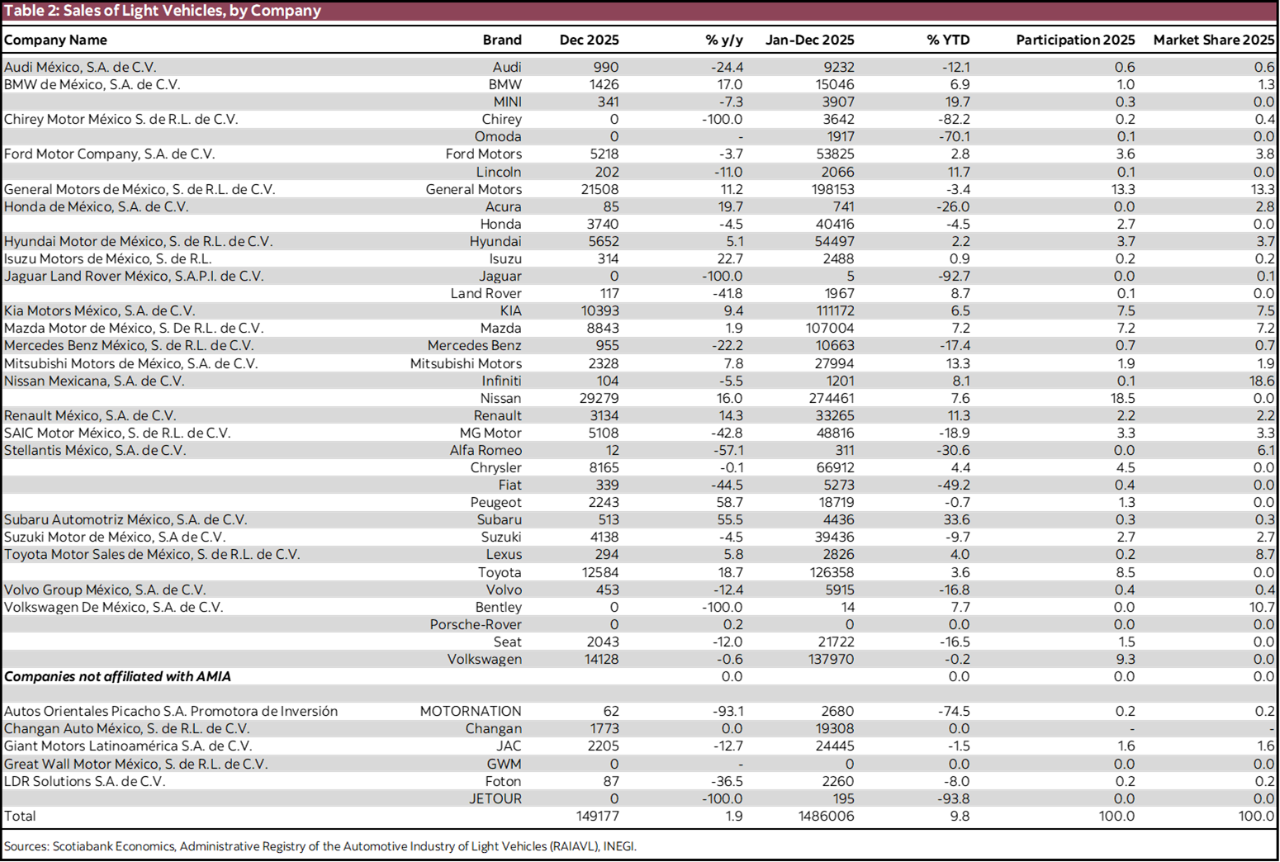

As in previous years, sales benefited from the entry of new competitors, particularly Chinese brands (table 2). However, compared with 2024, the official share of these brands fell for the first time, representing 9.2% of the total, down from 9.9% the year before. Notably, Chirey was removed from the administrative registry, and several electric-vehicle brands such as BYD and Tesla were absent, meaning their market share is not included in the RAIAVL (Administrative Registry of the Light-Vehicle Automotive Industry). According to the Mexican Association of Automotive Distributors (AMDA), total sales of Chinese brands, including those not reported, could reach 244,000 units—equivalent to a 15% market share, higher than the official figures suggest.

Among registered vehicles, Nissan stood out as the leader with an 18.0% share, supported by 7.6% growth (274,461 units). It was followed by General Motors and Volkswagen, with 13.0% and 9.0% shares, respectively, although both recorded annual declines of -3.4% and -0.2%.

The performance of domestic sales will depend on factors such as stagnation in the formal labour market, the imposition of 50% tariffs on Chinese vehicles as stipulated in the 2026 Revenue Law, and weaker remittance flows, which could limit demand. Nonetheless, lower interest rates and the expansion of new market players could partially cushion these risks.

WEAK LIGHT-VEHICLE PRODUCTION AND EXPORTS

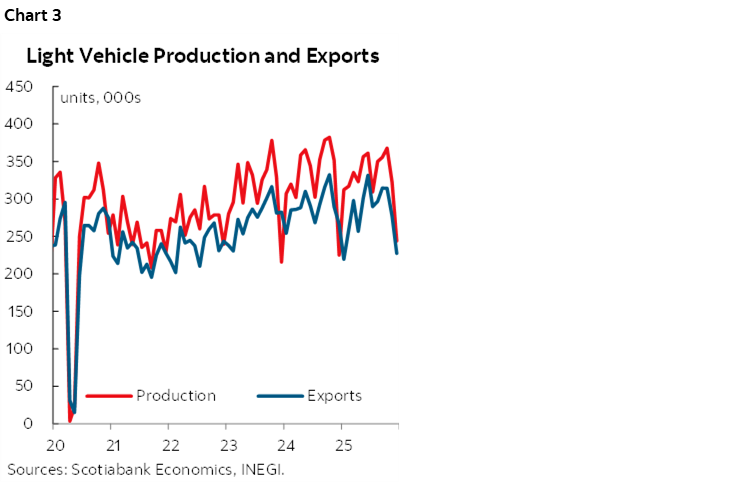

Amid international uncertainty and changes in U.S. trade policy, light-vehicle production and exports declined in 2025 compared to the previous year (chart 3). In December alone, production grew 8.5% annually; however, this final rebound was insufficient to prevent an accumulated contraction of -0.9%, totaling 3.953 million units, compared to 3.989 million in 2024, when production reached a record high.

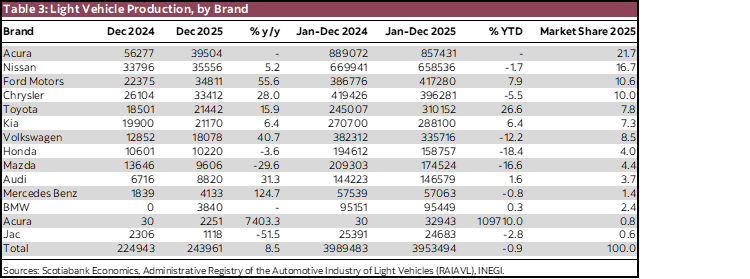

Throughout the year, production – was affected by assembly-line adjustments driven by strategic changes in anticipation of potential U.S. tariff modifications, as well as input shortages—especially semiconductors. The decline was practically widespread across brands (table 3), with the exception of new production by Acura and a 27% increase at Toyota, both with facilities in Guanajuato, and gains at Ford (8%) and Audi (2%). In contrast, notable declines were seen at Honda (-18%), Mazda (-17%), and Volkswagen (-12%). In terms of market share, General Motors maintained its lead at 21.7%, followed by Nissan at 16.7%, and Ford at 10.6%.

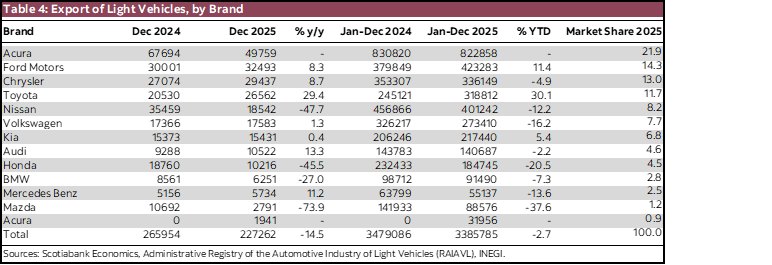

Exports suffered a larger contraction during 2025, mainly due to changes in U.S. trade policy. In December, foreign sales fell -14.5%, marking the fourth consecutive month of declines and totaling eight negative months during the year. As a result, light-vehicle exports dropped -2.7% annually, totaling 3.385 million units, compared with the 2024 record of 3.479 million. By brand (table 4), Toyota stood out with a 30% increase, consistent with its higher production levels, along with gains by Ford (11%) and KIA (5.4%). In contrast, the most affected brands were Mazda (-37%), Honda (-20%), and Volkswagen (-16%).

The industry will continue adjusting production lines amid nearshoring dynamics toward the U.S. and input shortages, particularly semiconductors. These same factors will pressure exports, making the upcoming mid-year USMCA review critical for automakers’ strategic planning.

DEPRESSED HEAVY-VEHICLE DEMAND AND SUPPLY

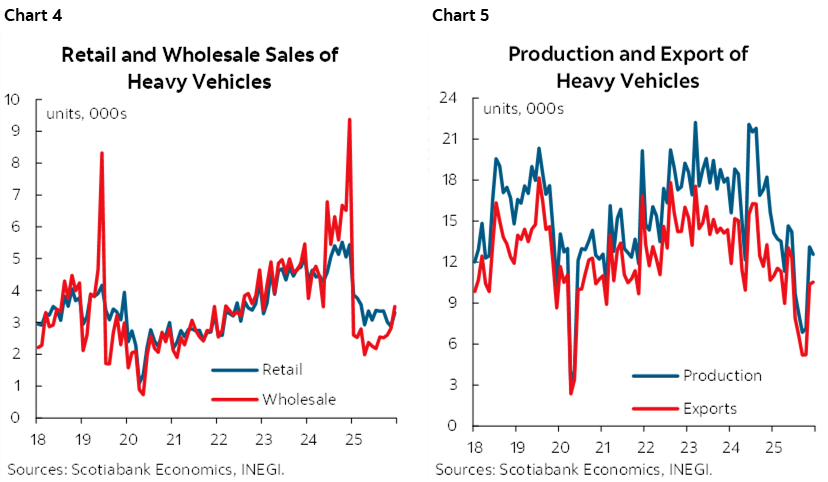

The impact of rising uncertainty and changes in U.S. trade policy was most evident in heavy-vehicle indicators, which saw contractions of nearly one third in both domestic sales and production/export volumes, reaching their lowest levels since the 2020 pandemic (charts 4 and 5).

In the domestic market, heavy-vehicle sales declined in 2025 in both retail and wholesale categories, with a sharper fall in the latter: -51% in wholesale and -27% in retail, totaling just 21,763 and 30,644 units, respectively. This weakness in internal demand, especially in wholesale sales, is linked to stagnant investment and weak business confidence, influenced by both international factors and domestic issues, including uncertainty surrounding the judicial reform and worsening security conditions.

External demand also deteriorated sharply due to U.S. tariffs. However, in the last two months of the year, exports moderated their decline to -22% in November and -1.3% in December, after four months of drops exceeding -50%. Even so, exports totaled 113,931 units for the year, down -28.6%. U.S. efforts to promote reindustrialization in strategic regions with domestically produced vehicles represent an additional risk for Mexico’s competitive position.

In this context, the 25% tariffs imposed by the U.S. on heavy vehicles from Mexico—justified on national security grounds—will significantly increase export costs, undermining automakers’ competitiveness. Although USMCA grants tariff preferences to products that meet rules of origin, the application of these tariffs has generated tensions, given that many Mexican vehicles do comply (91%, according to AMIA). Nonetheless, the lack of clarity regarding exemptions and political pressure in the U.S. have cast doubt on the USMCA’s effectiveness as a commercial shield. In parallel, Mexico has responded with proposals for 50% tariffs on Chinese vehicles, seeking alignment with the U.S. and strengthening the North American bloc, potentially serving as leverage in the 2026 USMCA review.

Finally, heavy-vehicle production deteriorated similarly throughout 2025, accumulating a -34% annual drop. Yet, declines moderated in the last two months, with production falling “only” -19% in December after average slides near -59% in Q3. The adverse domestic environment, combined with expectations of a more complicated trade relationship with the U.S., remain key factors shaping medium-term supply prospects, although nearshoring opportunities could present upside risks for the industry.

The heavy-vehicle sector will remain relatively stagnant under high uncertainty and low investment. Although annual rates may show apparent improvement in upcoming months, this will mostly reflect arithmetic effects from the sharp declines early in 2025. That is, year-on-year comparisons will naturally look less negative—or even positive—due to the low base, even if underlying activity remains weak in absolute terms. The lack of investment, persistent uncertainty, and risks tied to U.S. trade relations will continue to limit a sustained recovery. Taken together, the industry faces a scenario of limited dynamism, shaped by weak investment prospects and high international and domestic uncertainty.

IN CONCLUSION

The performance of the automotive industry during 2025 reflects a sector pressured by weakening domestic demand, strategic adjustments by automakers, and a challenging and uncertain external environment. While light-vehicle sales proved resilient and reached their highest levels since 2017, production and exports suffered from U.S. trade uncertainty and supply-chain fragilities. In the heavy-vehicle segment, severe contractions in both domestic and export markets underscore weak investment and the sector’s high sensitivity to global geopolitical developments. Although some growth figures may appear to improve due to base effects, the sector’s activity will remain dependent on the evolution of regional trade conditions, input availability, and automakers’ ability to adapt to a volatile and competitive landscape. Accordingly, the industry faces significant challenges in 2026, but also opportunities linked to Mexico’s commercial positioning, technological transitions, and the arrival of new players in the domestic market.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.