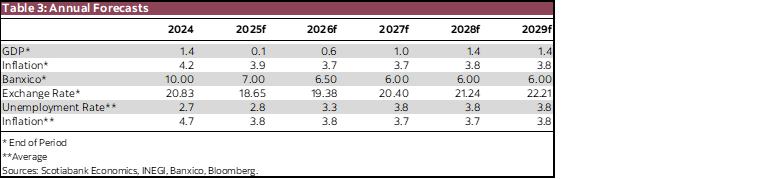

- Inflationary Pressures Persist: Despite economic stagnation, core inflation remains above 4%, limiting room for further monetary easing. However, Banxico cut rates by 300 basis points in 2025.

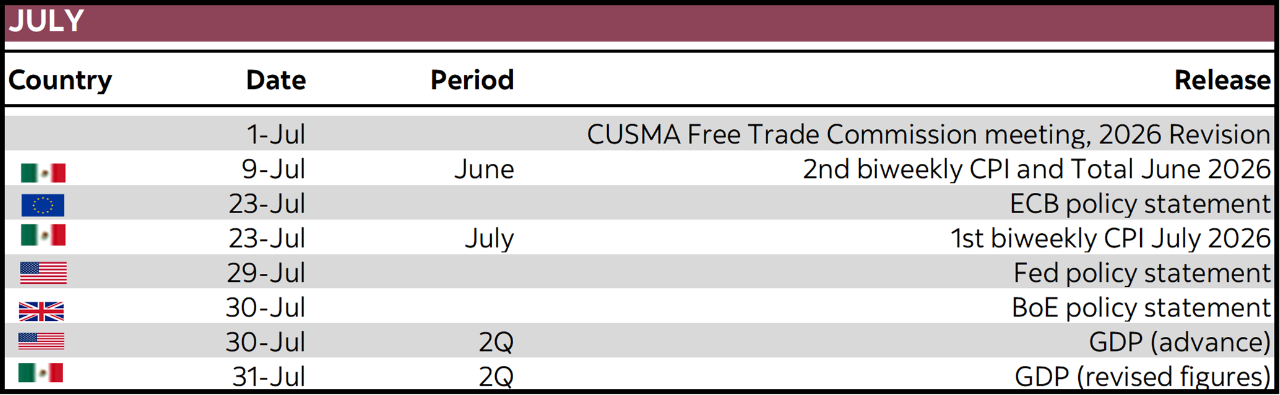

- USMCA Review in 2026 Brings High Uncertainty: The scheduled review could lead to ratification, partial adjustments, or full renegotiation, with implications for trade, investment, and regulatory frameworks across North America.

- Economic Stagnation: Mexico’s GDP growth slowed sharply from 3.4% in 2023 to an estimated 0.1% in 2025, with quarterly figures showing stagnation and slight declines.

- Investment Weakness: Gross fixed investment fell for 13 consecutive months (-7.6% YTD), driven by political uncertainty, reduced public spending, and security concerns.

- Sectoral Divergence: Primary activities rebounded modestly, as well as services, while industrial sectors continued contracting, reflecting structural weaknesses.

- Fiscal Outlook and Risks: Public finances show optimistic projections by SHCP, but debt remains high (52.3% of GDP), and tariff hikes plus Pemex support strain fiscal space.

Mexico’s economy is facing a complex scenario characterized by internal uncertainty stemming from constitutional changes and a restrictive fiscal stance, which have limited public and private investment and deepened deficiencies in infrastructure and structural conditions necessary for growth. Added to this is external uncertainty associated with the upcoming review of the USMCA, the evolution of trade relations with the United States, and that country’s own policies—factors that have increased risk perception and stalled productive projects.

As a result, the country faces economic stagnation that compromises short-term growth prospects. Alongside this adverse context, inflationary pressures persist, which could complicate Banco de México’s rate-cutting cycle, reducing its room to stimulate economic activity. These pressures arise from shocks in input prices, wage adjustments, and logistical costs, adding tension to monetary policy in a low-growth environment.

Everything indicates that this situation will hardly reverse in 2026, as structural factors and the lack of regulatory and trade certainty will continue to weigh on investment decisions. In this context, the challenge will be to design strategies that strengthen confidence, boost infrastructure, and mitigate inflationary risks to prevent prolonged stagnation from translating into a deeper deterioration of economic and social conditions.

Adding to the uncertainty is a very volatile close to financial markets, in Mexico and abroad, which has clouded the outlook for some of the key themes that have dominated for several months, such as the outlook for rate cuts, USD weakness etc. have become less clear over recent weeks.

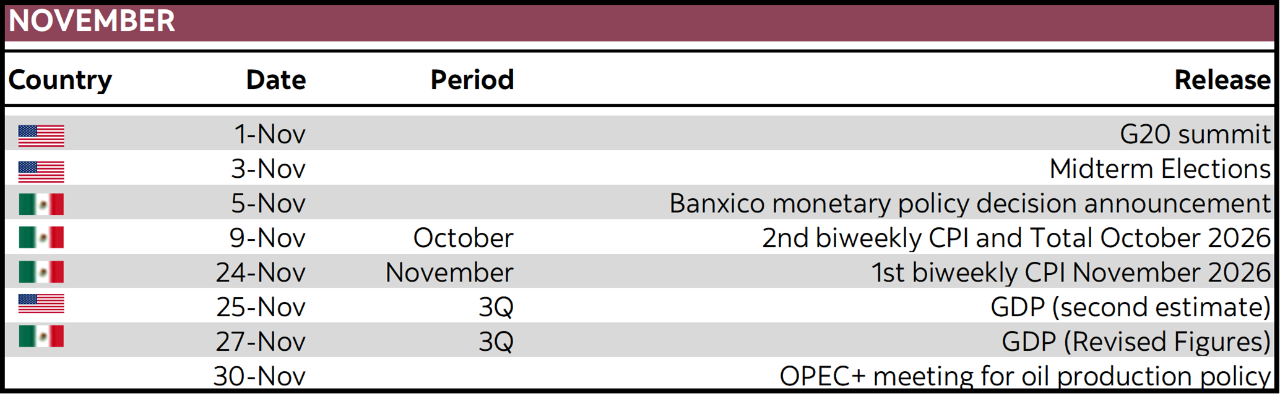

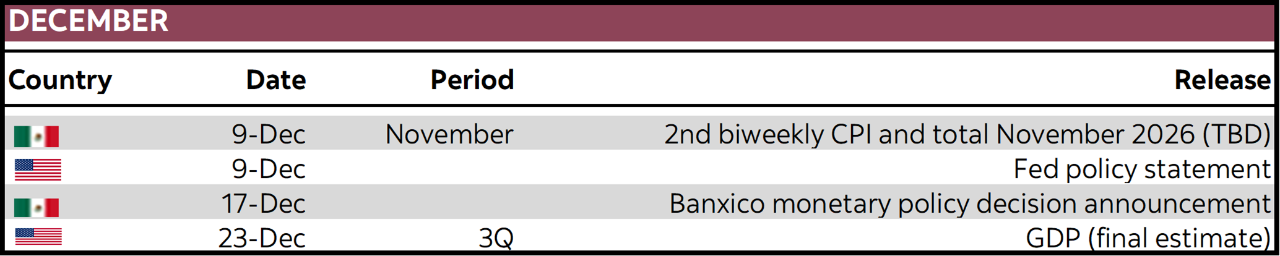

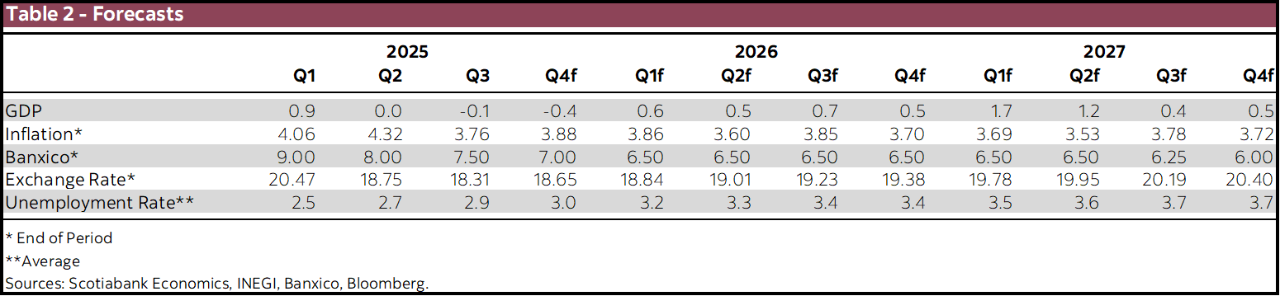

In this document, we present a summary of the main macroeconomic factors, as well as the events that shaped Mexico’s trajectory in 2025 and will continue to do so in 2026. Likewise, at the end of the document, we include a calendar of key events to monitor in 2026 and our forecasts for the coming periods.

MONETARY POLICY AND INFLATION: BANXICO HAS VERY LITTLE ROOM TO CONTINUE ITS RATE-CUTTING CYCLE

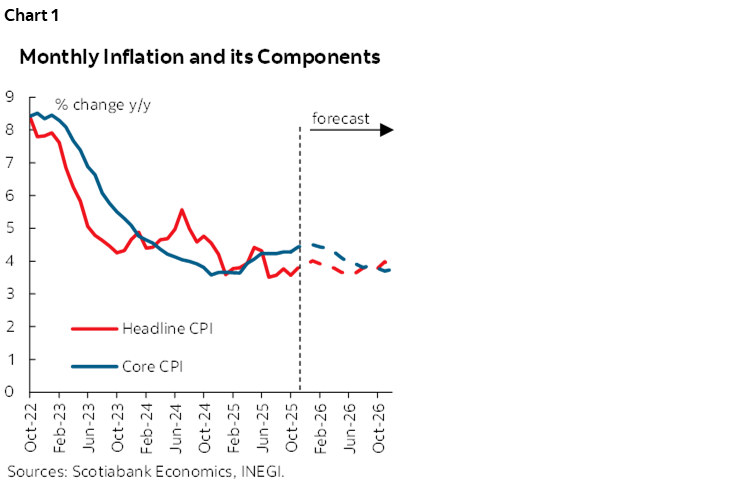

During 2025, headline inflation increased slightly (chart 1), although it remained within Banco de México’s tolerance range, rising from 3.59% in January to 3.80% in November, showing some volatility throughout the year. It reached a peak of 4.42% in May and a low of 3.51% in July, then stayed within the upper end of the target range. This behaviour was influenced by a marked slowdown in non-core prices during the second half of the year, which fell from a peak of 5.34% to 1.18% in October, mainly due to sharp declines in fruit and vegetable prices amid more favourable weather conditions. However, this effect was offset by pressures in the core component, which has remained stuck around 4.20% since June. It is worth noting that both services and goods inflation remain above 4%, despite the economic slowdown, which could reflect a structural issue in price formation.

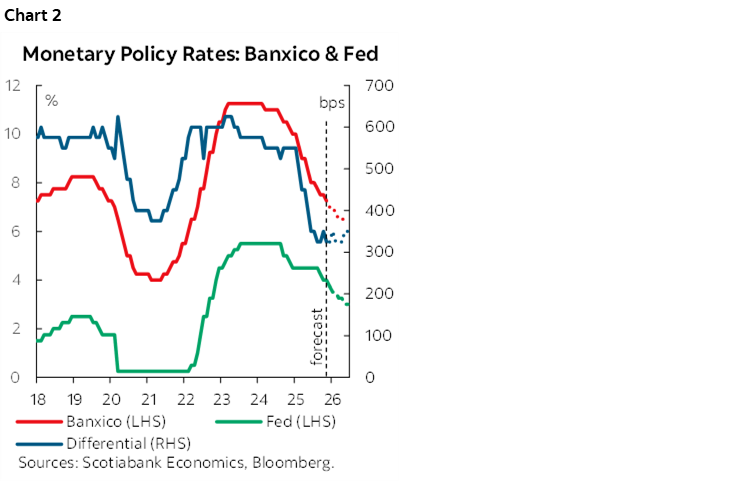

Given the apparent decline in inflationary pressures, Banco de México decided to continue the rate-cutting cycle that began in the second half of 2024, reducing the policy rate by 300 basis points over eight meetings in 2025—from 10.00% to 7.00%. Cuts of 50 basis points were made in February, March, May, and June, followed by four additional cuts of 25 basis points each in August, September, November, and December. The central bank argued that the rate was in highly restrictive territory, which, along with lower inflationary pressure, provided room for further adjustments. However, inflation expectations remain anchored at elevated levels: 3.9% for 2026 and 3.7% for 2027, above the 3% target. These projections differ from the central bank’s own forecast, which anticipates convergence to the target in Q3 2026.

Currently, monetary policy is in a neutral position, meaning it no longer actively combats inflationary pressures, even though expectations remain above target, which could limit room for further cuts. Additionally, the relative monetary stance between the United States and Mexico—measured by the differential between Banco de México’s and the Federal Reserve’s policy rates—stands at 325 basis points, below the historical average of 450 basis points over the past 15 years (chart 2). This may not reflect the country risk premium that should compensate international investors, further limiting the rate-cutting cycle. However, the dollar’s weakness, influenced by Trump administration policies, the Fed’s rate-cutting cycle, and the fact that domestic inflation remains within the target range amid economic slowdown, have served as justification for Banco de México to keep lowering its policy rate.

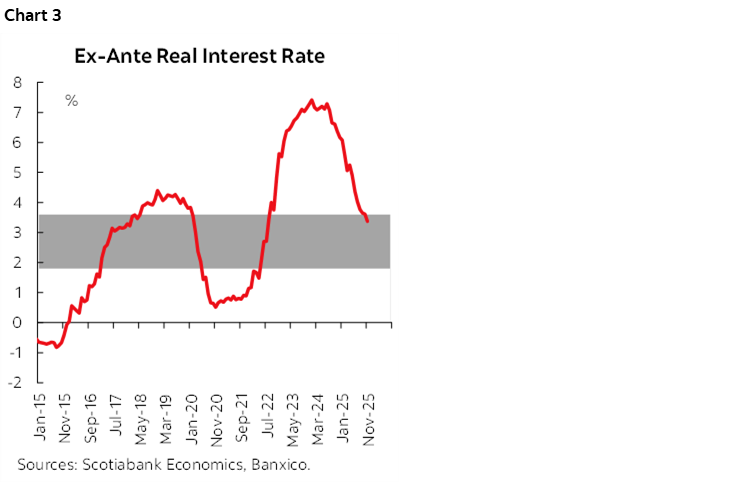

For 2026, we anticipate headline inflation will remain within the target range, provided climate change effects do not significantly impact agricultural prices, which could generate pressures on the non-core component. Additionally, during the summer, we could see a notable price increase as a result of the FIFA World Cup in Mexico, which could drive up service prices—such as housing due to limited hotel room supply—as well as other services amid increased tourist inflows. On the goods side, we expect an increase in processed food prices, affected by the global event. Likewise, we could see some pressures from the 13% increase in the minimum wage for 2026, as well as higher taxes on imported products from Asia without trade agreements with Mexico and on health-harmful products. In this sense, we see convergence to the 3% inflation target as highly unlikely in 2026 or even 2027. Therefore, Banco de México will have to continue fighting inflation, and we anticipate that if inflation remains within the 3% ± 1% band, the peso stays at current levels, and the Fed continues its rate-cutting cycle, Banxico could lower the policy rate to 6.50% by the end of 2026. This would place the ex-ante real rate at 2.8%, practically at the midpoint of the neutral range (1.8%–3.6%), assuming inflation of 3.7% by end-2027 (chart 3).

Finally, it is worth mentioning that implied rates in the TIIE funding curve anticipate the terminal rate of the cutting cycle at 7.00%, remaining there throughout 2026. Thus, investors are betting that Banco de México will continue fighting inflationary pressures. For 2027, the curve discounts a 25 basis point hike. In this regard, market reaction will be critical if Banco de México decides to cut below 7%.

Therefore, it will be essential to monitor inflation risks. Upside risks include: (1) currency depreciation; (2) persistence of core inflation; (3) escalation of geopolitical tensions causing distortions; (4) climate change impacts; and (5) higher cost pressures. Downside risks include: (1) continued weakening of the Mexican economy; (2) lower cost pressures; and (3) sustained peso strength.

TRADE: POSSIBLE SCENARIOS FOR THE NORTH AMERICAN TRADE BLOCK IN 2026

The USMCA review is formally scheduled for July 1st, 2026, where the original agreement requires a re-ratification by the executive branches of the 3 countries, but trade teams are already engaged in consultations and discussions over the future of the deal. This review process is outlined by article 34.7 of the USMCA Agreement. The process in the 3 countries is led by the USTR (USA), Global Affairs Ministry (Canada) and the Secretary of the Economy (Mexico). By the deadline, the 3 countries can decide on the following courses:

- Ratify: If the three countries decide to ratify the agreement, it will be extended for an additional 16 years (until 2042). However, the agreement still faces a review in 2032, with the possibility of extension until 2048.

- Do not ratify: In this case, the agreement remains in place for another 10 years (2036) but requires annual reviews until then. At any point in that period, the countries can decide to renew it for an additional 16 years. If no consensus is reached, the agreement expires by July 1st, 2036.

- Terminate: Article 34.6 of the USMCA states that the head of the executive of any of the 3 countries may at any point withdraw from the agreement, with a 6-month written notice. We see this action by any party as highly unlikely.

However, at the moment it seems likely that a partial renegotiation of USMCA is on the table, which could include a number of new chapters, including on migration and security (especially applicable to Mexico), as well as some who argue the discussion of the creation of a customs union, and possibly some policies that relate to trade and investment from outside the block (possibly indirectly aimed at China). A full re-negotiation could require a new ratification process by the corresponding legislative branches of the 3 countries, in which case it’s worth noting that the U.S. is holding midterm elections in November 2026, adding an additional layer of uncertainty to the potential process.

Although there is a very wide range of possible outcomes to the North American trade partnership going forward, we see 3 main scenarios:

- Benign: arguably the most benign scenario, as it reduces uncertainty across the block if it is ratified in mid-year. Those who argue for this outcome state that a ratification of the agreement could help Trump in the mid-term elections as a large number of U.S. states are highly dependent on Canada and Mexico for trade. Reducing uncertainty for dependent industries could give growth, investment and employment a boost in these states, helping the Republican party ahead of the midterm elections. The issues with this view are: a) can Trump sell the status quo as a victory rather than self-inflicted harm to voters? b) this scenario does not address Trump’s agenda on migration and security. One potential solution could be to sign parallel agreements related to migration and security alongside a ratification of USMCA.

- Middle Ground: a potential middle ground scenario involves an agreement not being reached by the July 1st deadline, but an eventual ratification of the agreement with minor reviews. Some potential reviews could include tightening of rules of origin but not changing enough to require a renegotiation. In this scenario, we don’t get full renegotiation (not needing legislative approval), and the extra topics could be addressed by parallel agreements (i.e. security, migration, possible restrictions aimed at China/outside the block trade and investment). Some uncertainty lingers, but it appears increasingly likely that although Mexico and Canada could be worse off on tariffs and other issues than they were in December 2024, they both still look likely to end up better off than most countries exporting to the U.S. While the agreement is being discussed, the three countries would keep the agreement in place, with annual reviews, if necessary, until the deadline in July 2036 (at which point the agreement would expire if not ratified).

- Adverse: If a full renegotiation and legislative ratification materialize, it’s possible that the North American trade framework remains in flux beyond the end of 2026. Although a renegotiation does not necessarily mean a worse framework, it adds risks that further trade and investment barriers could emerge, it could mean additional non-trade chapters which could politicize the trade relation in the future and also suggests that uncertainty could drag on for longer. Some potential sticking points could include:

- Rules of origin: tightening of the rules of origin could be required, given that Mexico’s imports from China have increased by around 60% of the increase of Mexican exports to the U.S., which some argue is due to triangulation.

- Auto sector: Automotive trade represents almost a quarter of all trade within North America, making it one of the dominant themes in the looming discussions. As was argued by this paper by the Baker Institute, the original USMCA sought to increase the U.S. content in North American auto manufacturing (Chapter 4), but it's possible that the USTR could seek to further push for a rising U.S. share through tariffs or changes to the quotas of exempt vehicles. Another issue that could pop up in the auto chapter (and other technological sectors, such as telecoms, etc.) is national security. There are concerns that interconnected cars which use technological components produced in China could be a national security risk for the U.S. This could mean that restrictions by Mexico of Chinese components for its manufacturing sectors could face additional restrictions during the review/renegotiation processes.

- Energy Cooperation: Quoting directly from “Strategic Priorities for the 2026 USMCA Review”, by David A Gantz in the Baker Institute:

“Energy, both fossil fuels and renewables, is an area where Mexico has fallen significantly short of fulfilling its obligations under the USMCA. Mexico’s sovereignty over its energy resources was not questioned, per Chapter 8 of the USMCA. However, under Article 32.11 of the agreement, Mexico effectively agreed to a MFN clause, whereby Mexico’s actions under the USMCA may be taken “only to the extent consistent with the least restrictive measures that Mexico may adopt or maintain under the terms of applicable reservations and exceptions to parallel obligations in other trade and investment agreements that Mexico has ratified prior to entry into force of this Agreement.” The previously ratified agreement to which this article primarily refers is the Comprehensive and Progressive Trans-Pacific Partnership Agreement, particularly its Chapter 9 on investment, which details, inter alia, national treatment for foreign investors.” In particular, the 2024 reversal of the 2014 Energy Reform could end up being a sticking point in the negotiations given: a) it is frequently argued that the 2024 reform eroded the independence of autonomous regulators for the sector, b) it is also argued that the 2024 reform also affected the position of private players vis-à-vis Mexico’s public sector players.

- Regulatory Issues: This sub-topic has many layers, but some of the key ones include a) the 2024 judicial reform is often argued as eroding the independence of Mexico’s judicial system from the executing, b) the more recent limits to appeals/injunctions reduce protections enjoyed by private players when dealing with the executive—including on fiscal issues. Finally, c) the July 2025 Mexican Economic Competition legal reform also raises several issues which could complicate the USMCA review, particularly in relation to dealing with State Owned Enterprises (especially on energy), as well as potentially on the autonomy of the regulators (COFECE stops being an independent regulators, and becomes a decentralized public agency).

- Additional Chapters: We believe that including “non-trade” chapters within the USMCA is an unnecessary risk, as it risks politicizing the agreement, raising further risks to it becoming a political topic in the future. However, the possibility of adding non-trade chapters to the framework appears to be on the table, particularly with regards to migration and security. Some of Trump’s “executive order tariffs” on Mexico and Canada were established under national security arguments, and the addition of chapters on these issues appears to be a possibility. As we mentioned before, we think keeping the USMCA a pure trade treaty, with the possibility of parallel agreements on such issues is likely to protect the North American trade framework from being contaminated by such issues in the future.

At this stage, it's difficult to assign probabilities to any of these three scenarios (or others that emerge), but as we stated above, we think that a termination of the framework seems unlikely.

UNCERTAINTY AND STRUCTURAL WEAKNESS: KEY DRIVERS OF MEXICO’S LOW GROWTH

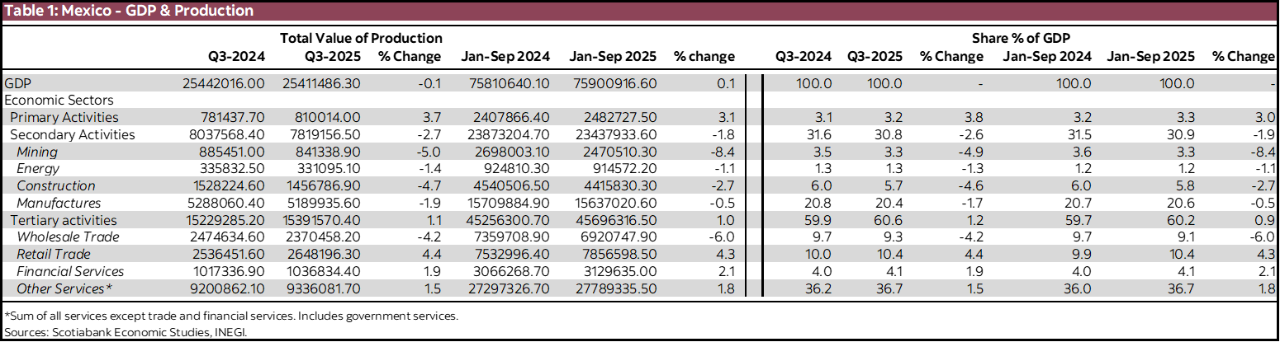

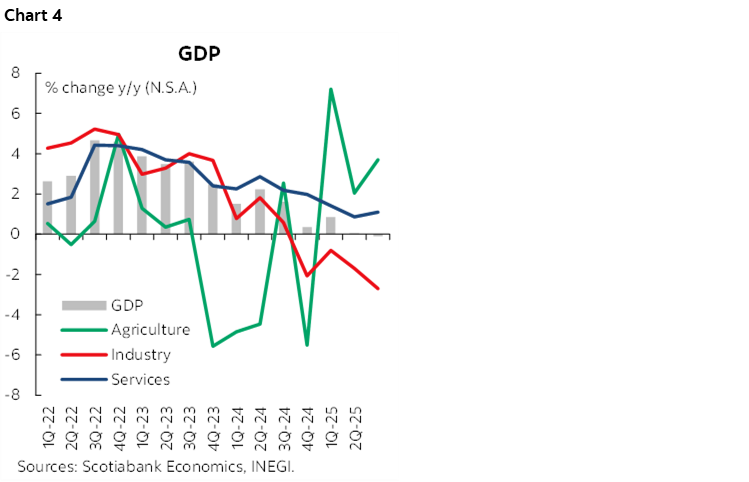

In 2025, Mexico’s economy showed a mixed picture (table 1). While some productive sectors such as agriculture and services posted growth, the industrial sector continues to show weak dynamism due to rising economic and political uncertainty in the country, as well as lack of business confidence and structural problems within the sector. This, coupled with widespread weakness in aggregate demand components, is directly reflected in GDP performance in recent quarters (chart 4). Mexico’s GDP has slowed from annual growth of 3.4% in 2023 and 1.4% in 2024 to a projection of just 0.1% in 2025. Quarterly data show marginal growth, stagnation, and declines: Q1 2025 saw a slight increase of 0.9%, followed by stagnation at 0.0% in Q2, and a marginal drop of -0.1% in Q3, with projections pointing to a year-end decline of -0.4%. Below is a description of aggregate demand behaviour and productive sectors, as well as a short-term outlook.

WEAKNESS IN AGGREGATE DEMAND COMPONENTS (INVESTMENT AND CONSUMPTION)

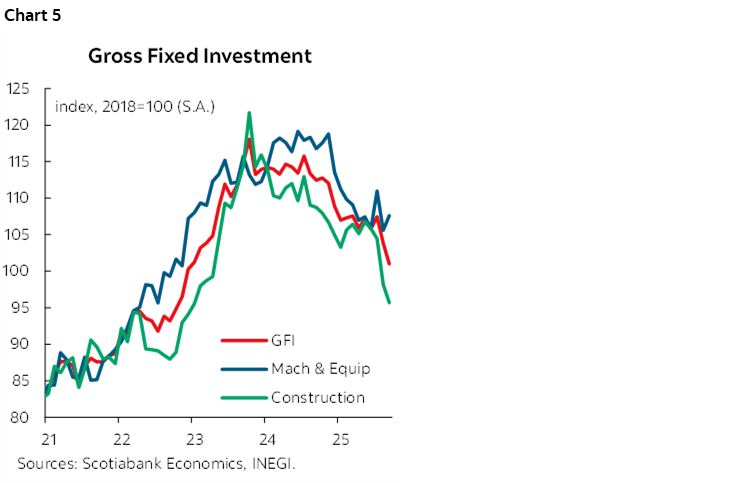

Toward the end of 2025 and into 2026, Mexico’s economy faces a challenging scenario marked by widespread weakness in demand components. Gross fixed investment has posted thirteen consecutive months of declines (chart 5), with an annual drop of -6.7% in September and a cumulative fall of -7.6% from January to September, reflecting persistent national and international uncertainty, reduced public investment, and an unfavourable security environment. This underscores how political and economic uncertainty has eroded business confidence.

Although September’s decline was smaller than in previous months, the continued deep contractions in construction, especially non-residential, and machinery indicate no signs of solid recovery in the short term. Without a secure and stable environment, it will be difficult to encourage new plant installations, infrastructure development, or expansion of productive capacity. Investment depends not only on macroeconomic stability but also on basic guarantees that allow operations without risks threatening capital, talent, and project continuity.

Private consumption, although it showed a 3.6% annual rebound in September driven by imported goods (14.8%), remains stagnant year-to-date (0.0%), affected by slow job creation, lower remittances, and weak consumer confidence. Services grew 1.5% in September but showed no change in seasonally adjusted monthly trends. The rebound observed in September is more attributable to an increase in imported goods than to improved domestic spending capacity, suggesting the boost is temporary and unsustainable. Year-to-date stagnation, combined with slow job creation and falling remittances, points to weakened domestic demand that will hardly sustain growth in the coming quarters.

LOWER DYNAMISM IN PRODUCTIVE SECTORS

Primary activities showed dynamism in the first three quarters of the year. After closing 2024 with a -5.5% decline, they rebounded in Q1 2025 with an annual variation of 7.2%. Despite a drop in Q2 to 0.9%, they recovered in Q3, growing 3.7% year-over-year and 3.1% cumulatively from January to September.

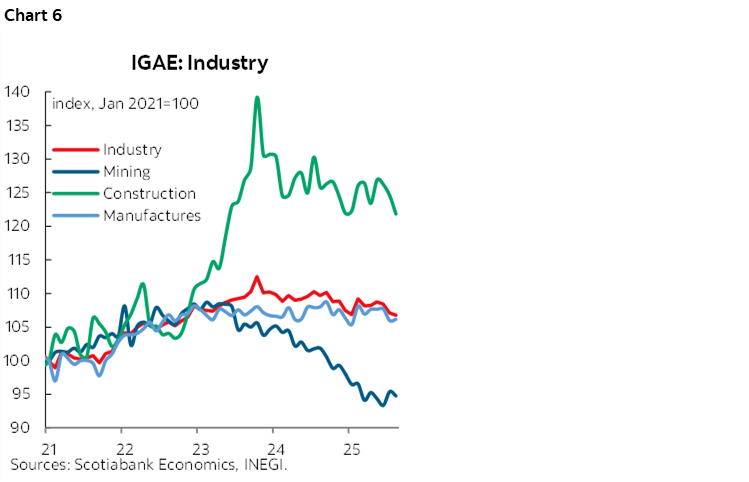

Conversely, the industrial sector continued to slow in 2025, with declines across all components (chart 6), directly linked to investment contractions—particularly in construction and machinery, as noted earlier. Breaking it down: mining contracted -5.0% in Q3 2025 and -8.4% cumulatively from January to September, accentuated by the ongoing decline in oil production despite government efforts to inject resources into the state-owned company. Public utilities contracted -1.4% in Q3, averaging -1.1% year-to-date, continuing a negative trend over the last three quarters. This reflects limited fiscal space to address these gaps and private-sector challenges from insecurity, lack of investment, and regulatory restrictions. Construction fell -4.7% in Q3 and -2.7% year-to-date, driven mainly by civil engineering works, which have posted negative figures since Q3 2024. Finally, manufacturing fell -1.9% in Q3 2025, marked by widespread declines across subsectors, with marginal gains in some industries unable to offset losses. Manufacturing weakness extends to the cumulative annual figure, with a marginal decline of -0.5% compared to the first three quarters of 2024. It is important to note that this weakness has persisted since Q3 2023—around two years—and although these declines may seem small, manufacturing accounts for 20% of Mexico’s GDP.

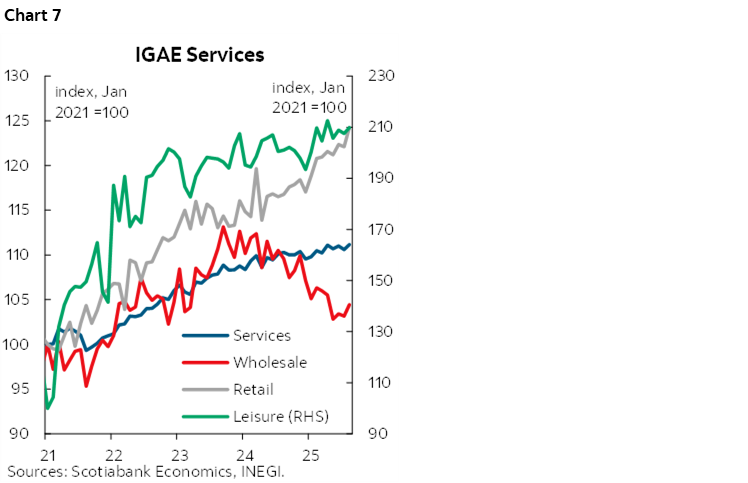

Finally, services grew 1.1% in Q3 and 1.0% year-to-date (chart 7), compared to 2.4% in 2024 and 3.4% in 2023, further highlighting the economic slowdown. Again, while these annual changes may seem marginal, the tertiary sector represented 60.2% of Mexico’s GDP year-to-date, totaling MXN 15.4 trillion in Q3 2025, which undoubtedly keeps services as the main driver of Mexico’s economy. In Q3, trade showed mixed signals: wholesale trade fell -4.2%, while retail grew 4.4%. Among the fastest-growing services in the last quarter were entertainment (13.2%), business support (10.7%), professional services (8.7%), health services (5.3%), and financial services (1.9%).

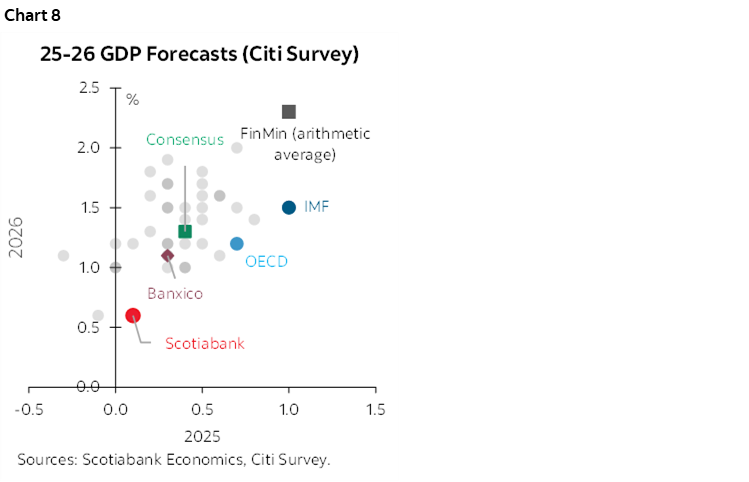

For 2025, the IMF estimates growth of 1.0%, while Citi’s economists survey median adjusted its forecast to 0.4%, down from 0.5%. Banxico maintains expectations near 0.6%, in line with other analysts (chart 8). For 2026, the IMF projects 1.5%, compared to Citi’s 1.3% and Scotiabank’s 0.6%. Globally, growth will moderate to 3.1% in 2026, with advanced economies at 1.6% and emerging markets at 4.0%, reflecting a less dynamic international environment. We believe some of these projections are overly optimistic given internal and external conditions that continue to pose significant risks to sustained recovery.

Looking to 2026, economic growth will depend on internal and external factors that could alter the current trend. Potential drivers include tourism recovery from the World Cup, accompanied by stronger lodging and entertainment services, as well as dynamism in food services. However, internal risks persist, such as political and trade uncertainty, weak investment, and slow improvement in domestic consumption, along with external risks like weaker-than-expected U.S. growth, escalating geopolitical tensions, and potential financial market instability—all of which keep the outlook highly volatile.

INCREASES IN PUBLIC EXPENDITURES AND REVENUES IN 2026

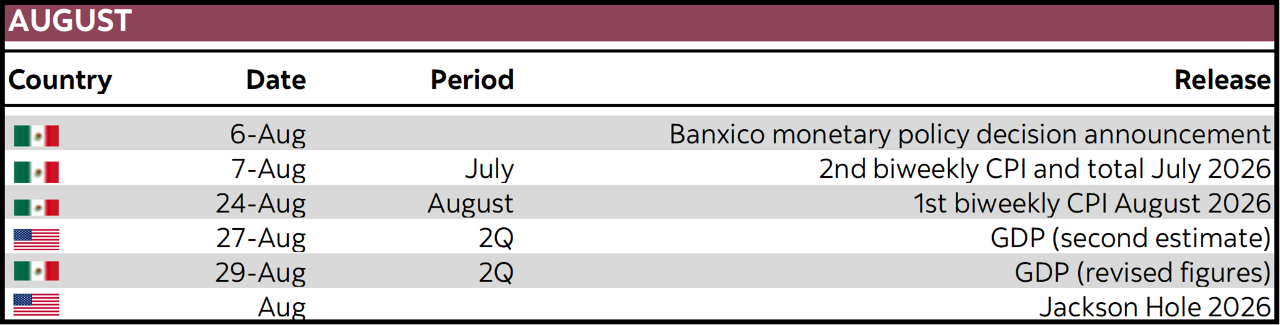

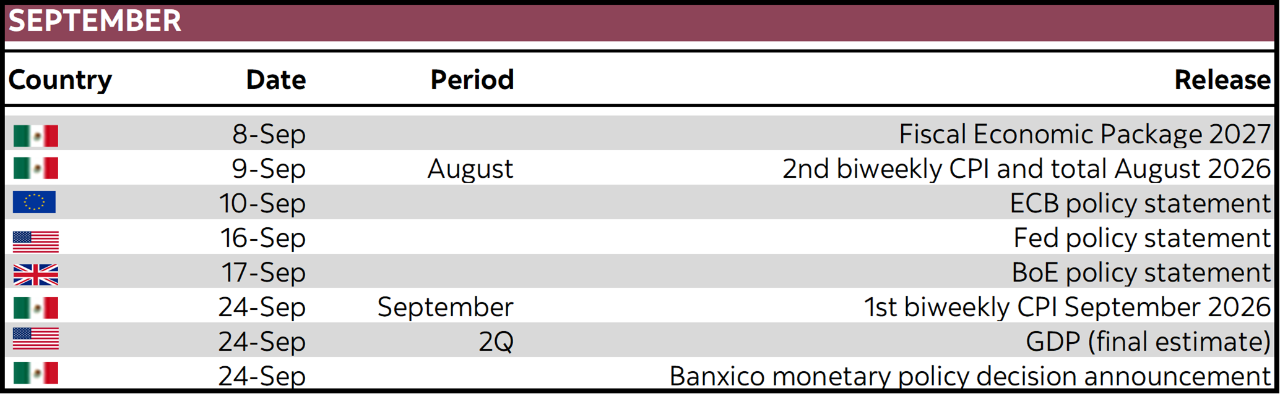

In terms of public finances, the 2025 result has been marked by three main developments: government efforts to improve tax collection efficiency without changing tax rates; contraction in public spending characterized by weak promotion of public investment and support operations for Pemex; and more optimistic estimates compared to analyst consensus. For 2026, broadly speaking, we expect the agenda to continue revolving around these three points, with some adjustments.

In September, the Ministry of Finance and Public Credit (SHCP) published the 2026 Economic Package with a macroeconomic framework that is more optimistic than market expectations. This is particularly relevant for revenue, spending, and debt estimates for the coming year. For the current year, SHCP estimated growth between 0.5% and 1.5%, above the private consensus of 0.40%, while for 2026 SHCP projects a range of 1.8% to 2.8%, compared to the consensus of 1.15%, which has been revised downward in recent updates. Regarding public finance indicators as a percentage of GDP, SHCP estimates budget revenues of 21.9% in 2025 and 22.5% in 2026, equivalent to a real annual increase of 6.3%. Notably, oil revenues are expected to grow modestly after declines of -31.0% in 2023 and -15.1% in 2024, with real annual increases of 2.7% and 3.1% in 2025 and 2026, respectively, in a context where oil production has maintained a downward trend in recent years. In this regard, Pemex’s Strategic Plan 2025–2035 includes more than 20 exploration and production projects with private participation, aiming to reach the target of 1.8 million barrels per day (mbd) of production, compared to the 1.712 mbd observed during January–October 2025.

Similarly, SHCP anticipates growth in tax revenues relative to GDP next year, explained mainly by improvements in collection but also by higher tariffs. According to the recently approved tariff law, import taxes of up to 50% will apply to goods from countries without trade agreements with Mexico, aimed primarily at countering Chinese imports in key sectors. From 2019 to 2024, tax revenues rose from 12.7% to 14.6% of GDP, while for 2025 they are estimated at 14.8%, with a further increase to 15.1% in 2026. Revenue increases can be seen in income tax (ISR), which rose from 6.7% in 2019 to an estimated 8.0% for 2025. VAT, IEPS, and non-tax revenues are expected to close the year at 4.1%, 1.9%, and 4.5% of GDP, respectively.

On the spending side, SHCP anticipates a real annual increase of 5.0%, compared to the 1.7% increase observed through October 2025. Excluding federal support for Pemex’s debt buyback of MXN 253.8 billion, the administration achieved a -1.7% contraction in cumulative spending through October 2025, mainly due to a sharp adjustment in programmable spending. Regarding this, the issuance of structured P-Caps notes maturing in 2030 to cover financial obligations and Pemex amortizations during 2025 and 2026 was positively received by rating agencies, changing the outlook for the state-owned company’s credit rating to BB+ (Fitch) and B1 (Moody’s), both with a stable outlook. Considering the slightly more than MXN 7 trillion programmed for net spending next year, SHCP estimates only a marginal real annual increase (0.5%) in pensions and retirements. However, it projects a 9.5% increase in current spending subsidies. On the positive side, the Economic Package also estimates a 10.0% increase in physical investment. However, this increase is minor in terms of GDP, as estimates show it rising only from 2.4% to 2.5% of GDP, while subsidies, pensions, and retirements would total 7.3% in 2026, compared to 7.2% in 2025, with a growing trajectory in the coming years.

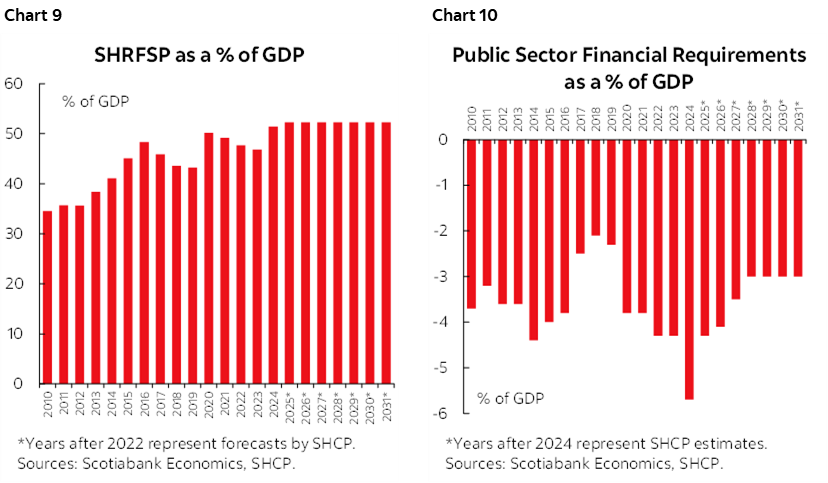

Regarding debt, for 2026, federal government estimates point to maintaining the Historical Balance of Public Sector Financial Requirements at around 52.3% of GDP (chart 9), the same as estimated for 2025—the highest level observed since 2000. Similarly, after the increase to 5.7% in the Public Sector Financial Requirements (RFSP) deficit, SHCP estimates a consolidation process starting in 2025 (chart 10), with a year-end close at 4.3%, a smaller deficit of 4.1% in 2026, and a target of 3.0% from 2028 onward. Also noteworthy is the debt portfolio profile, where SHCP plans to continue efforts toward longer maturity horizons and a greater domestic component.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.