- External (tariffs) and domestic (fiscal) developments were key risks going into 2025 for Peru, but have had limited impact on the country’s economic performance as very favourable terms of trade and firm domestic demand tee up another 3%+ expansion this year.

- We expect a similar rate of growth in 2026, helped by solid macroeconomic fundamentals (employment and inflation) and a spending boost from another round of pension withdrawals. Elections in 2026 and political and trade uncertainty remain significant risks, however.

TERMS OF TRADE IMPROVEMENT WAS A KEY FACTOR FOR 2025

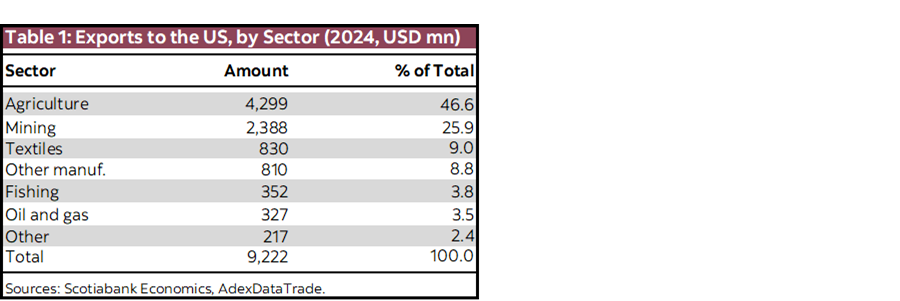

The current year began with two major external risks for the economy. The first was, and continues to be, an uncertain international environment due to U.S. government policy, particularly tariff hikes. The tariff imposed by U.S. imports from Peru sits the U.S.’s 10% lower bound for global tariffs. In addition, the U.S. imposed a 50% tariff on certain copper products, although not on concentrates, which is what Peru exports the most. It does not appear that the U.S. has finished considering tariffs, so the risk of a larger effect in the future remains (table 1). At the same time, however, the data does not show evidence, so far, of a significant negative impact of the U.S. tariff policy on the Peruvian economy.

The other important, and recurrent, risk for Peru has to do with the electoral cycle. In the past, pre- and post-election uncertainty has often had a significant impact on the country’s economy.

Furthermore, and as additional testament to how unstable politics can be in Peru, on October 10th Congress impeached President Dina Boluarte, and replaced her with José Jerí, a member of Congress. José Jerí is the seventh president in seven years. Of these seven presidents, only two were elected as such, Pedro Pablo Kuzcynski in 2016, and Pedro Castillo in 2021. So the regime change reflects a greater weakness overriding Peru’s day-to-day politics, which is the country’s weak political institutionality.

At the time of this writing, the markets have reacted to the new Jerí regime with benevolence, and a new cabinet was appointed that appears to be primarily pro-business. There is some risk of political turbulence going forward, however.

Both factors, external and domestic, generate a significant level of uncertainty. For this reason, it is surprising how little this dual risk environment has been affecting the economy. Rather, 2025 has been an unexpectedly favourable year for the Peruvian economy. Growth has been moderate, although led by robust domestic demand; macroeconomic balances, already firm, have improved even more; accompanied by monetary stability alongside low inflation during the year, with the benchmark interest rate reduced from 5.00% at the beginning of the year to 4.25% in September, as well as an exceptionally strong exchange rate.

LOOKING AHEAD TO 2026

Although the uncertainty generated by U.S. policies did not affect Peru in 2025, there is a risk that its impact will materialize later. Similarly, the electoral uncertainty that did not affect economic data during 2025 remains a risk for 2026.

It is difficult to predict the magnitude of the impact that these two potential sources of risk may have in the future, given the same uncertainty they generate. What can be said is that, so far, the international context is having a more favourable than unfavourable effect on the country’s economy. The main reason is the significant boom in metal prices. In addition, the prices of many important imported goods such as crude oil, wheat and corn have fallen. As a result, Peru’s terms of trade are currently at record levels. Historically, there is some favourable correlation between high terms of trade and growth in GDP and private investment.

Our expectation is that terms of trade will stabilize in 2026. We expect metal prices to rise slightly on average versus 2025, even if that implies a correction from currently high levels. We also expect an upward correction in import prices of key products (wheat, corn, soybeans, oil), as they are currently at unsustainably low levels.

Given the present weakness of political institutions in Peru, elections represent an additional source of uncertainty. It is difficult to predict the outcome of the presidential and parliamentary elections to then determine an eventual economic impact. Our assumption is that, under the next government, the Ministry of Economy and Finance (MEF) will maintain fiscal policy more or less within the channels in which it has been in the last 15 years. Another assumption is that the country’s general institutionality does not continue to erode.

Peru has been able to grow despite the political turbulence of the last eight years largely thanks to the strength of economic institutions, such as the Central Reserve Bank (BCRP), the Superintendence of Banking, Insurance and AFPs (SBS) and the National Superintendence of Tax Administration (Sunat). This institutionality has been decisive in maintaining the soundness of the economic accounts. In 2026, the BCRP’s board of directors will be renewed, as with every change of government. Much of the country’s economic future will depend on the decision that will be made in this regard.

In summary, a series of risks are foreseen for 2026, but the year will kick off from an economically solid position, with strong external accounts, manageable fiscal accounts, moderate GDP growth, and price stability from consumer prices and interest rates, to key import prices and the exchange rate.

GDP GROWTH

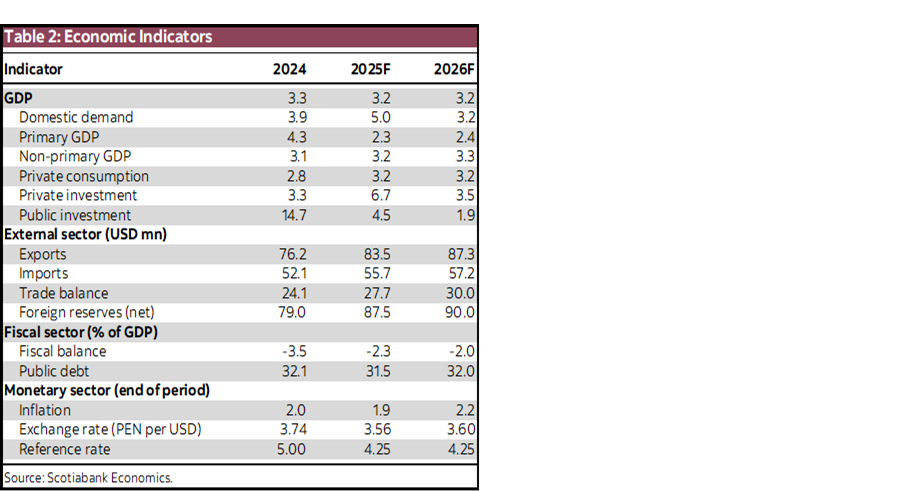

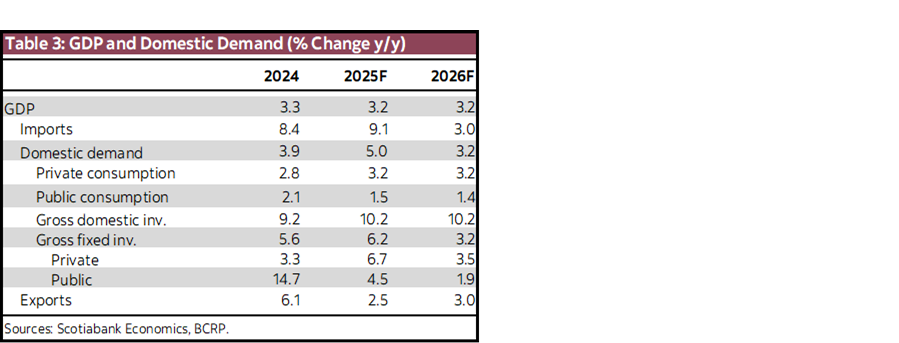

We project that GDP will grow 3.2% in 2026, matching the pace that we estimate for 2025 (tables 2 and 3). Our projection balances positive and negative factors. There are factors that limit growth in 2026, including the fact that GDP will grow from a higher comparative base than in 2025. It will also face the ups and downs of an election year. Finally, the government is seeking to slow public spending to meet fiscal targets. Along these lines, the MEF published a budget proposal that establishes an increase in public spending of only 2.2% in 2026.

Among the positive factors for growth are: the economy is ending 2025 with a solid labour market, low inflation and an increase in the incomes of some Peruvians thanks to the eighth withdrawal of pension funds (AFP); the first round of withdrawals should take place in the second half of November, although the bulk of the impact on consumption will occur in 2026. All this will contribute to private consumption growing 3.2% in 2026.

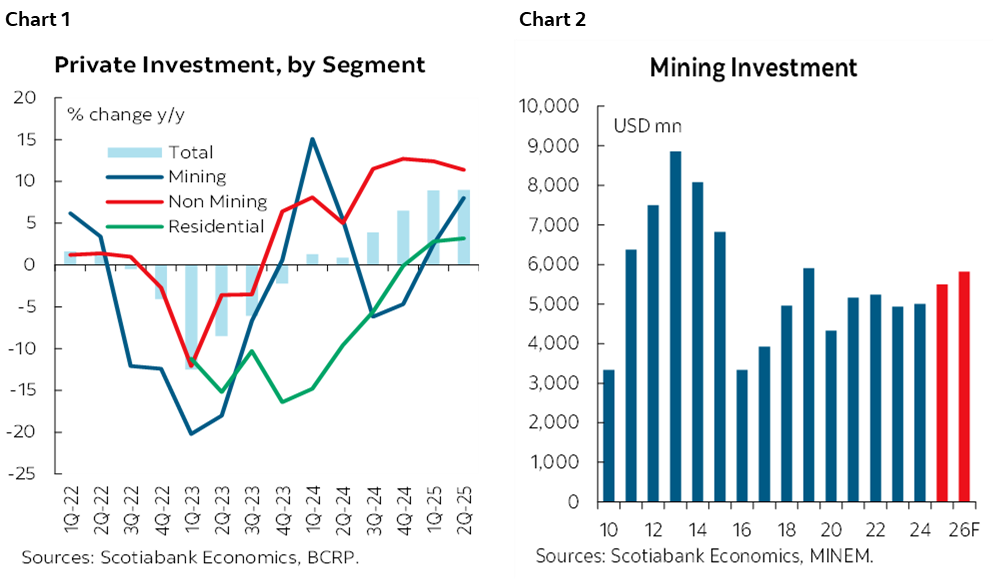

Private investment growth is usually more difficult to project (charts 1 and 2). Typically, private investment is more cautious in an election year. Not always. In the 2006 elections, private investment grew 20.1% despite the uncertainty in business confidence faced with an election between Alan García and Ollanta Humala. What happened in 2006 was that electoral uncertainty was offset by a boom in metal prices. One can argue that we are going through a similar situation today. Recall, however, that given the uncertainty regarding U.S. tariff and global policy, the external context also comes with an unusual degree of risk. Given this dual uncertainty, we prefer to remain cautious.

What the government has been aggressive in is promoting private investment via infrastructure works through tenders within the scheme of public-private partnerships and, to a lesser extent, works for taxes. These tenders will have a greater impact in terms of execution from 2027, although they have already been contributing to domestic demand incrementally in 2025 and 2026.

The government’s announcement that it will seek to comply with the fiscal rule that establishes that the fiscal deficit should not exceed 1.8% of GDP next year implies that it will try to control spending. This and the change of government that will occur in 2026 are behind our relatively low projections for public consumption and investment, 1.4% and 1.9%, respectively.

Finally, and somewhat unfortunately, we need to admit that the expansion of illegal mining has also been contributing to GDP growth in the last decade. There are incipient signs that a certain permissive attitude by authorities towards illegal mining is changing. Although illegal mining is also production and economic income that contributes to domestic demand, it brings with it a series of collateral effects that negatively affect the well-being of society.

GDP BY SECTOR

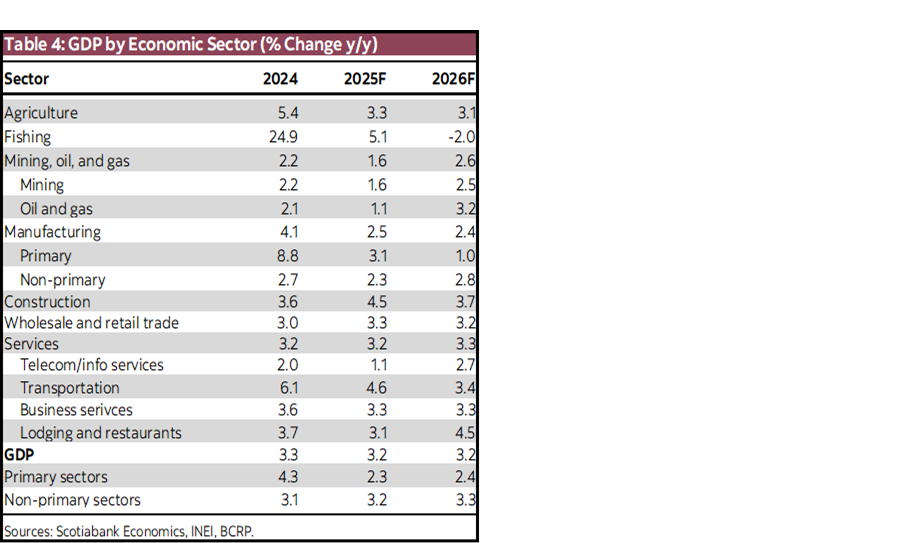

We project that GDP will grow 3.2% in 2026, similar to 2025. These figures consider the impact of the eighth withdrawal from pension funds (AFPs). Based on priors, we expect that around 20% of the nearly S/27,000 million of resources that would be withdrawn would be directed to private consumption. Given that the funds would begin to enter the economy in the second half of November, there will be some impact towards the end of 2025, but the main impact will be in the first half of 2026, contributing about 0.1 percentage points (ppts) to growth in 2025 and 0.3 ppts to the expansion of 2026. This would reinforce our expectation that sectors linked to domestic demand such as trade and services will continue to lead GDP growth (table 4).

Trade: Growth of 3.2% would be similar to that of the economy as a whole. Initially, we expected a slowdown in the sector as a result of a high base of comparison and since the election period generally generates caution in consumer spending—especially in the demand for durable consumer goods such as vehicles and household appliances. However, the injection of funds from the withdrawal of the AFPs would compensate for this usual moderation in spending, especially considering that the injection of resources would impact the first half of the year, the period in which the elections will be held. In addition, employment growth (in line with private investment momentum), the improvement in the purchasing power of the population (associated with low inflation rates), and an improvement in credit conditions (thanks to BCRP rate cuts) would contribute to support retail sales.

Services: We project an expansion of 3.3% similar to 2025. All segments would grow, although at different speeds. Among the stand outs would be transportation (thanks to the greater movement of cargo and people in line with the expansion of domestic demand), personal services and business services (thanks to the momentum in private consumption and private investment, respectively), and accommodation and restaurants (which by end-2026 would recover to pre-pandemic levels). On the other hand, we foresee a slowdown in government services, in line with the moderation of public spending budgeted for 2026, and in telecommunications, in view of the high level of penetration that exists in mobile telephony and fixed and mobile internet.

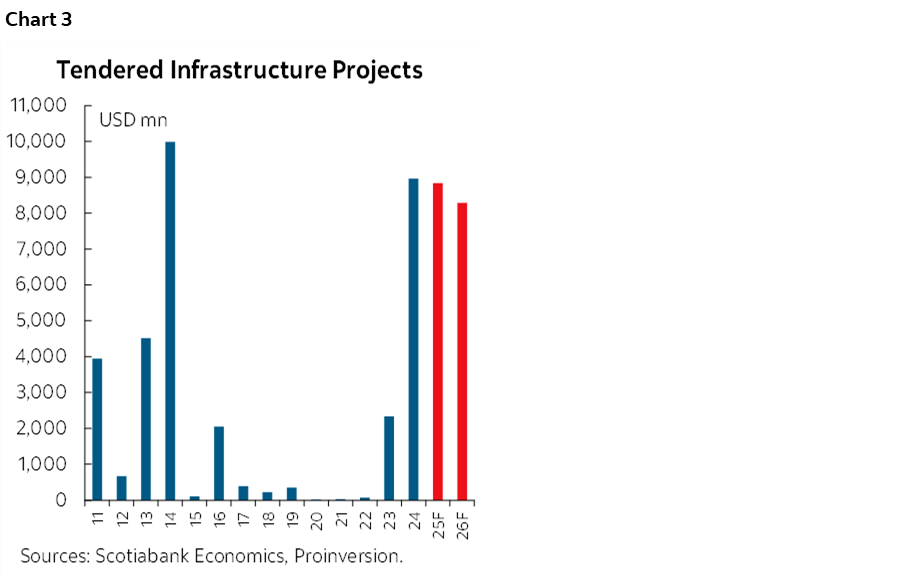

Construction: We expect growth of 3.7%, driven by the uptrend in private investment. Despite the caution of the electoral cycle, private investment has shown a notable recovery during the first half of 2025 and would continue with all engines running in 2026. High metal prices will motivate growth in mining investment, while residential investment will continue to be driven by the improvement in the population’s incomes—especially self-construction—and lower interest rates on mortgage loans. Finally, investment in infrastructure projects tendered under the Public-Private Partnership (PPP) modality is becoming an engine of growth in the medium and long term. Projects have been tendered for almost US$9,000 million in each year between 2024 and (we project) 2026 (chart 3). In contrast, the execution of public works would slow down in line with a more austere public budget in 2026 and due to the learning curve of a new national government that takes office on July 28th.

Manufacturing: The growth of 2.3% that we project would be led by non-primary manufacturing, in turn driven by the production of capital goods in line with the expansion of private investment, consumer goods in the face of the sustained evolution of private consumption and, to a lesser extent, intermediate goods. The lower growth of manufacturing, 2.3%, with respect to the economy as a whole, 3.2%, reflects, in part, a growing consumption of imported goods, in a context of reorientation of products—mainly from Asia—to other markets in response to the new tariff policy in the U.S., and in part to a greater share of services in household spending.

We expect that primary sectors will grow at a similar rate to 2025, assuming normal weather conditions for the agriculture and fisheries sectors, and in the absence of the entry into operation of large projects that impact the production of the mining sector.

Agriculture: We project that it will expand 3.1% in 2026, a rate similar to that of 2025. After the impact of the El Niño Phenomenon (FEN) in 2023, and its aftermath that lasted until mid-2024, agricultural production has resumed its usual growth trend. Several agro-export crops, including blueberries, grapes, and avocados, are still in the upward phase of their yield curve, so they have room to continue growing. In addition, the recent approval of a new agrarian law—which restores tax benefits to the sector—could promote a new wave of investments that increase production in the medium term.

Fishing: The slight drop of 2% that we expect in 2026 would be due to a base effect given the high level of anchovy catch that would be reached in 2025, which would be around 5 million tons, its highest level since 2021. By 2026 we assume a catch level of 4.7 million tons, which although it would be above the average of 4.2 million of the last ten years, would be lower than what was recorded in 2025. On the side of Direct Human Consumption (DHC) fishing, we expect a moderation in its rate of expansion given the significant recovery of the squid catch this year.

Mining: We expect the sector to expand 2.5% in 2026, more than in 2025. This growth would be led by gold since it will be the first full year of operations of the San Gabriel project (Moquegua) whose start of operations is scheduled for November 2025, and which would contribute about 150 thousand ounces per year. This is in addition to the recovery of iron ore production, which was affected in 2Q25 by logistical problems at Shougang Hierro Peru, the acceleration of copper output—Antamina would increase its copper production after having mined areas with higher zinc content during 2025—and the start of operations of the Romina zinc project—scheduled for the end of 2Q26 and which would provide about 50,000 FMT of zinc per year.

MACROECONOMIC BALANCES

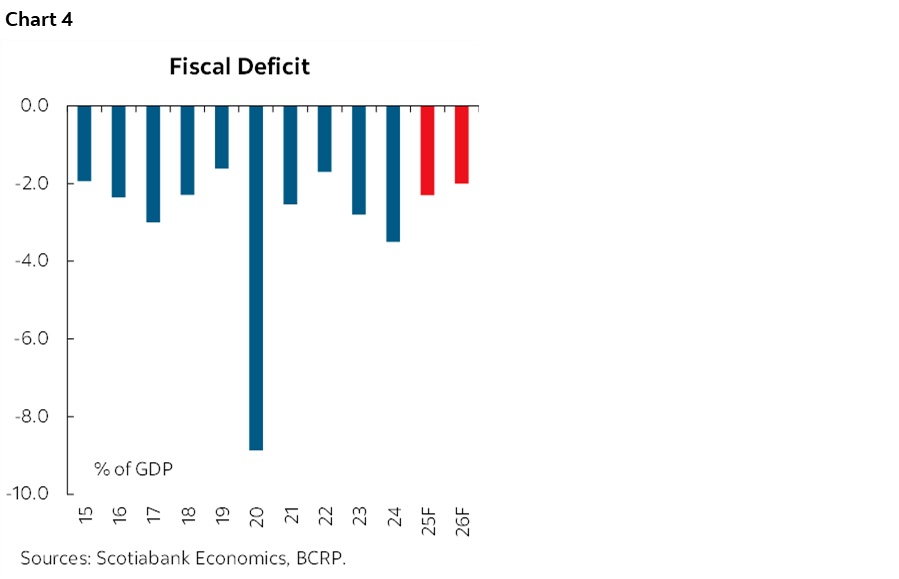

Fiscal balance: The fiscal deficit fell from its peak of 4.0% of GDP in September 2024, to a 2.3% level estimated for September 2025. The main factor behind this improvement has been the increase in tax collection, by 15% in this period, compared to rise in expenditure of 8%. This higher collection has been largely due to high metal prices, although the rise in General Sales Tax (IGV) revenues due to the growth in domestic demand also had a positive impact. While the environment of high metal prices makes it feasible to achieve the fiscal target of 2.2% of GDP in 2025, it is also true that fiscal spending typically increases due to seasonal factors in the fourth quarter of each year. Given this, our expectation is that the fiscal deficit will stabilize at 2.3% of GDP by the end of 2025 (chart 4).

The country’s fiscal situation will remain comfortable as long as high metal prices persist on the one hand, and domestic growth continues on the other. The public sector budget for 2026 has been increased by only 2.2% in nominal terms. Our projections of public consumption and investment, of less than 2% in real terms in both cases, are in line with this figure. The budget still needs to be approved by Congress, which could increase spending, but probably not in a materially significant way. Even so, achieving a fiscal deficit of 1.8% of GDP in 2026 will not be easy. Our projection is that the fiscal deficit will fall modestly to 2.0% of GDP. Although it is above the fiscal rule, it is a level that is manageable and sustainable over time.

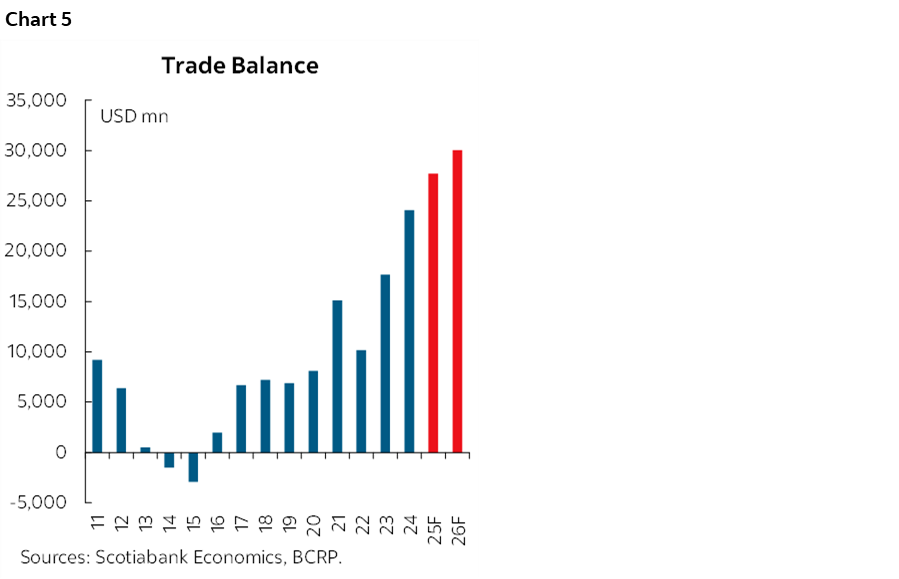

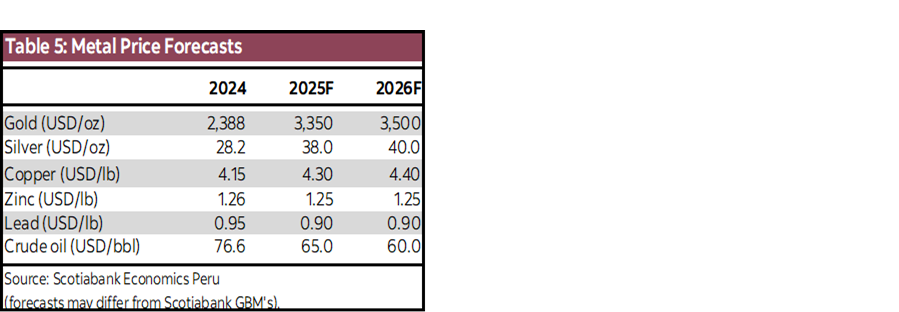

External accounts: The high international prices of metals in 2025 have helped Peru reach a historically high trade balance surplus (chart 5). We estimate that gold will end 2025 with an average price around 40% higher than in 2024, and copper close to a 4% average increase.

We did not expect such high metal prices at the beginning of 2025. The complicated global tariff context seemed rather risky for industrial metals. This risk has not materialized. On the other hand, the unusual, and unexpected, weakening of the dollar at the global level, as a result of the distrust generated by the economic and global policy of the Trump White House, has helped support metal prices, both industrial and precious, measured in dollars.

The global environment has had a particularly important impact on precious metal prices. This environment includes not only the uncertainty generated by monetary and economic policy in general in the U.S., but also the difficult global geopolitical situation. This is an environment that could continue into the future.

In the case of copper, the energy transformation towards renewable energy seems to be contributing more than expected as a price tailwind. If so, copper could continue to face high demand for years to come. In 2025, these energy transition combined as a price support with the partial interruption of production at the Freeport copper mine in Indonesia, which represents about 4% of global copper supply. According to the company, production will not return to normal levels until 2027, applying additional upside pressure copper prices.

While there are fundamentals behind the rise in metal prices, it is also true that these prices have risen a lot and seem ready for a correction. This is particularly true for gold and silver. As for industrial metals such as copper and zinc, there is a risk that tariffs and geopolitical complications will impact the world economy with a lag, leading to a global slowdown in 2026. Given this contrast between fundamentals and risks, on balance we expect metal prices in 2026 to be below their current levels (table 5), but to be somewhat higher in terms of annual average (note that Scotiabank Peru’s estimates may differ from forecasts by Scotiabank Global Banking and Markets).

On the other hand, the fall in the prices of imported goods that occurred in 2025, including key prices such as crude oil, corn, wheat and soybeans, is unlikely to be repeated in 2026. Several of these prices are at unsustainably low levels.

Therefore, for 2026 we expect a slight deterioration compared to the historically strong terms of trade of 2025, although the higher volumes exported would allow a higher trade surplus than the previous year. We expect the value of exports to rise by about 5% in 2026, compared to an estimated 10% in 2025, and the value of imports to increase by 3% in 2026, versus an estimated 7% in 2025.

ANOTHER YEAR OF STABLE PRICES AND LOW INFLATION

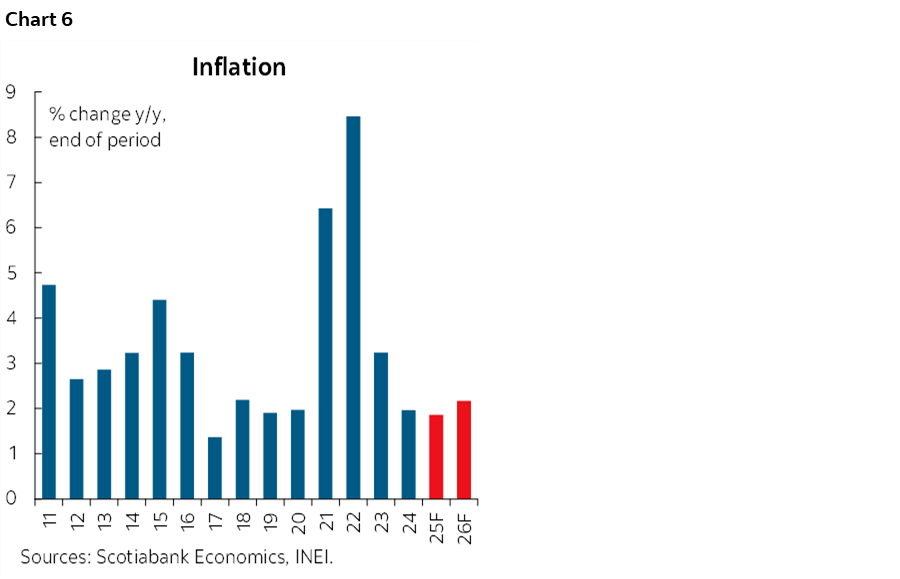

Inflation and reference rate: Inflation is firmly within the BCRP’s target range of 1% to 3% since April 2024. There are no inflationary pressures on the part of the domestic demand in the country, nor, at least for now, is there any contagion of global inflation. In particular, although there are incipient signs of mild global inflation due to the effect of tariffs in the U.S., no impact on prices has materialized in Peru. Therefore, we expect inflation at 1.9% at end-2025 and 2.2% at end-2026 (chart 6).

The risk of imported inflation due to the effect of tariffs on prices in the U.S. is much lower than when the war in Ukraine began in 2022. The beginning of the latter conflict had a direct impact on key prices for Peru, particularly crude oil and agricultural commodities. On the other hand, the current global environment has been putting downward pressure on these same prices. The prices that could be affected are prices of manufactured goods from the U.S., but these are more easily substitutable, and in general have a much smaller impact on inflation.

With inflation under control and the economy growing adequately, the benchmark rate of 4.25% seems to be close to the BCRP’s comfort level. The BCRP has determined that the neutral interest rate is 2.0% in real terms. Given inflationary expectations of around 2.2%, the nominal rate equivalent to the neutral rate would be 4.20%, close to the current 4.25%.

There is room for inflation expectations to fall to 2.0%, which would open room for further reduction. If the U.S. Federal Reserve is aggressive in lowering their own policy rate, it would increase the probability of one more BCRP cut to 4.0%. Our expectation is that this would happen sometime in the last quarter of 2025 or the first quarter of 2026.

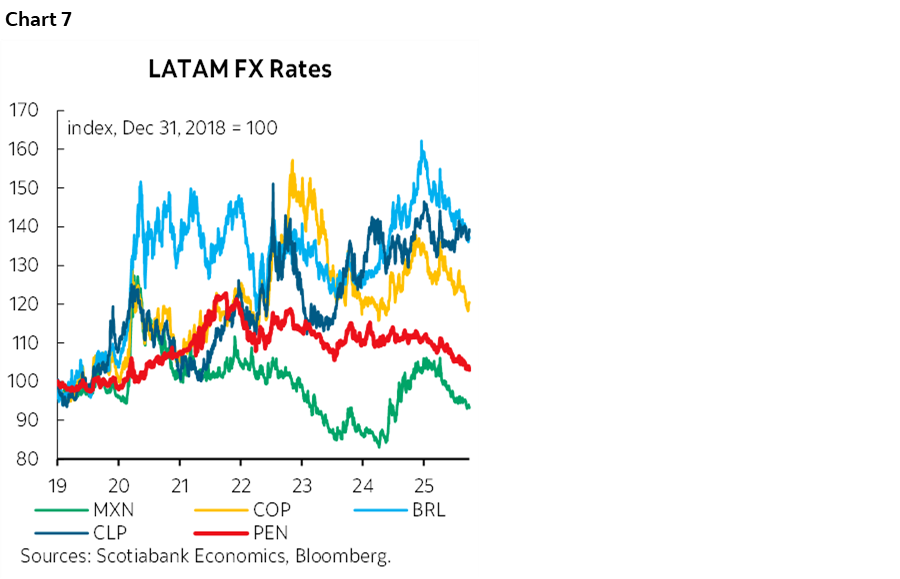

The exchange rate: The national currency, the sol, or PEN as it is known in the foreign exchange market, has shown a surprising combination of strength and stability in 2025. Strength since it appreciated 7.6% in the year to September (we estimate a final appreciation of 5.2% for the year, with the year-end exchange rate at S/ 3.56), and stability against other peer currencies in the region that have also appreciated, in general, but with a much more volatile trajectory over time (chart 7).

The main factor behind the appreciation of the PEN is the weakness of the dollar at the global level. Given the magnitude and duration of the dollar’s weakness, it is unclear how long this will continue. There is debate among analysts about the causes of the weak dollar, and whether it reflects a change in the dollar’s role as a global currency.

The second factor behind the appreciation of the PEN has been the very favourable fundamentals behind it, given the strength of Peru's external accounts, especially in terms of goods and services, to which is added a context of positive capital flows.

Many of these factors will continue into 2026. However, there will be elections with a high degree of uncertainty and, according to precedent, the exchange rate usually rises (the PEN depreciates) in the months prior to an electoral process. This is why we expect the exchange rate to rise towards the end of 2025 and into 2026. Once the elections are held, the exchange rate will continue to rise or correct depending on the election results, making it more difficult to predict what will happen. Our projection of S/3.60 by the end of 2026 is merely indicative. On the other hand, although history indicates a negative electoral impact on the exchange rate, it is also true that there have never been elections with external accounts as strong as they are now, which could moderate the pre- and post-electoral impact.

THE MARGINS OF ERROR FOR 2026

Economic predictions are always more difficult when it comes to election years. The possibilities are often dichotomous. If the resulting government is perceived as serious, responsible, and with the capacity for state management, economic prospects could become very favourable. If, on the other hand, the resulting government is perceived as anti-market, populist, linked to interested groups and with a questionable capacity for state management, the projections would have to be much more conservative and cautious. For 2026, risks and biases exist for both sides.

The global context will continue to provide support. The country's favourable terms of trade could greatly boost the economy in the event of the most positive scenario, and could limit the detrimental impact of a more harmful scenario.

Our projections for 2026 do not seem too different from those estimated for 2025. What must be remembered, however, is that, given the dichotomy of post-electoral possibilities, the margins of error in economic projections are wider than usual. For the time being, our projections reflect the assumption, inevitably tempered, of an intermediate point in our post-electoral consideration, with an economy benefiting from global metal prices and price stability internally, but growing at a speed below its possibilities.

These challenges remain: how to strengthen institutions, how to promote investment and expand productive infrastructure, how to ensure continuity in economic policy, how to detach the political class from lobbying interests, how to absorb and formalize the illegal economy, particularly mining, separating it from associations with criminality. In short, how to amplify and intensify the improvement in the well-being of the population through economic policy.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.