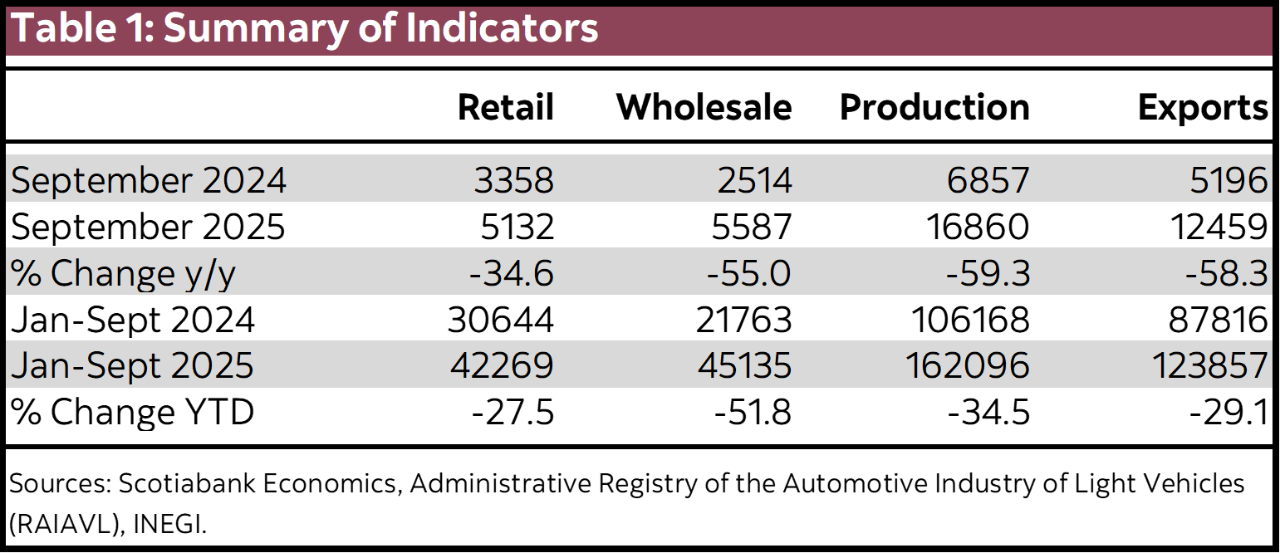

- Domestic sales of light vehicles showed a slight rebound in September but accumulate a fall of -0.6% for the year. Domestic demand for heavy vehicles has plummeted, with contractions of up to -55% in wholesale sales.

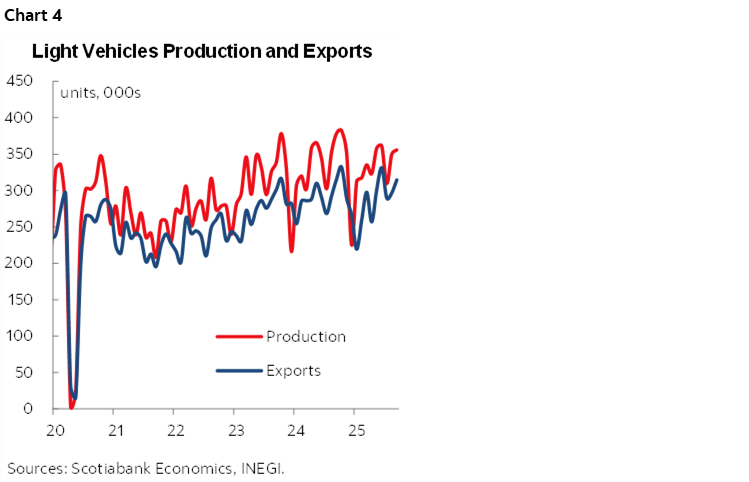

- Exports and production of light vehicles fell back into negative territory, with cumulative declines of -0.9% and -0.3%, respectively.

- Internal factors such as stagnation in formal job creation, lower remittances and low investment are putting downward pressure on automotive demand. Changes in market share reflect a decline in Chinese brands and a partial recovery in Nissan, Toyota and Kia.

- Trade tensions, the imposition of tariffs and uncertainty over the USMCA review next year could limit the trajectory of production and exports in the coming months.

DOMESTIC DEMAND: SALES IN DECLINE AFTER REBOUND IN JULY AND STEADYING IN AUGUST

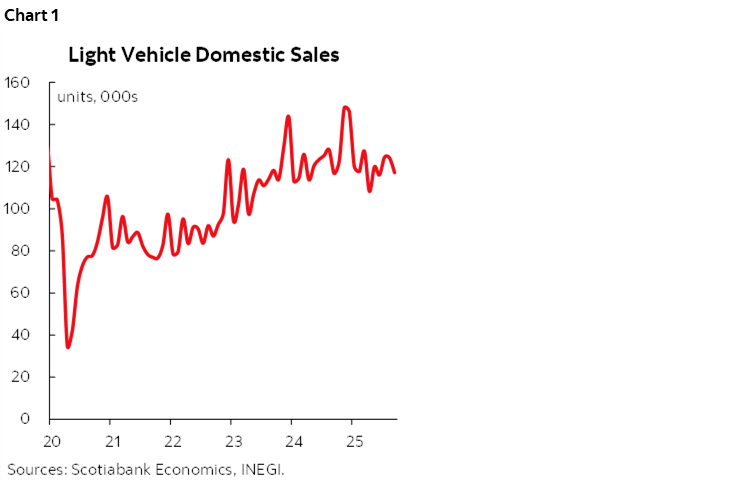

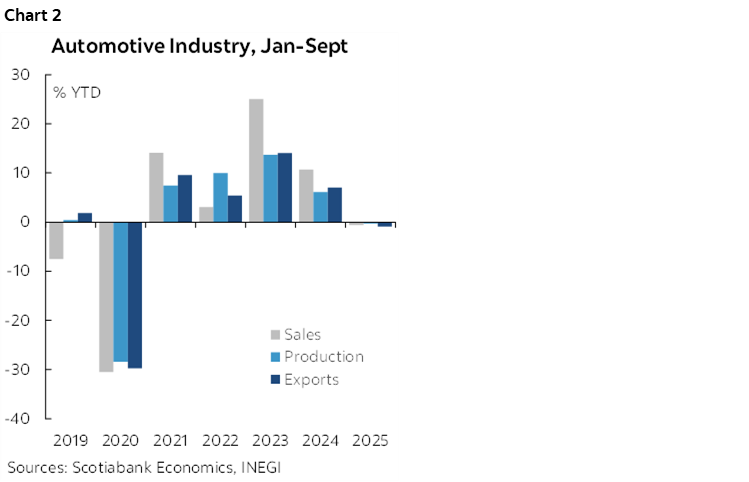

In September, domestic sales of light vehicles had a mixed behaviour. Although they climbed back into positive territory in year-on-year terms in September, breaking a streak of y/y declines since April, they fell by -5.6% m/m to follow the –0.2% drop in August and the 7.3% jump in July (chart 1 and table 1). The advance was also only modest at 0.3% y/y, totaling 117,181 units. With this, cumulative sales over the first three quarters of 2025 are tracking an annual contraction of -0.6% compared to the same period last year, equivalent to 1,075,187 vehicles (chart 2).

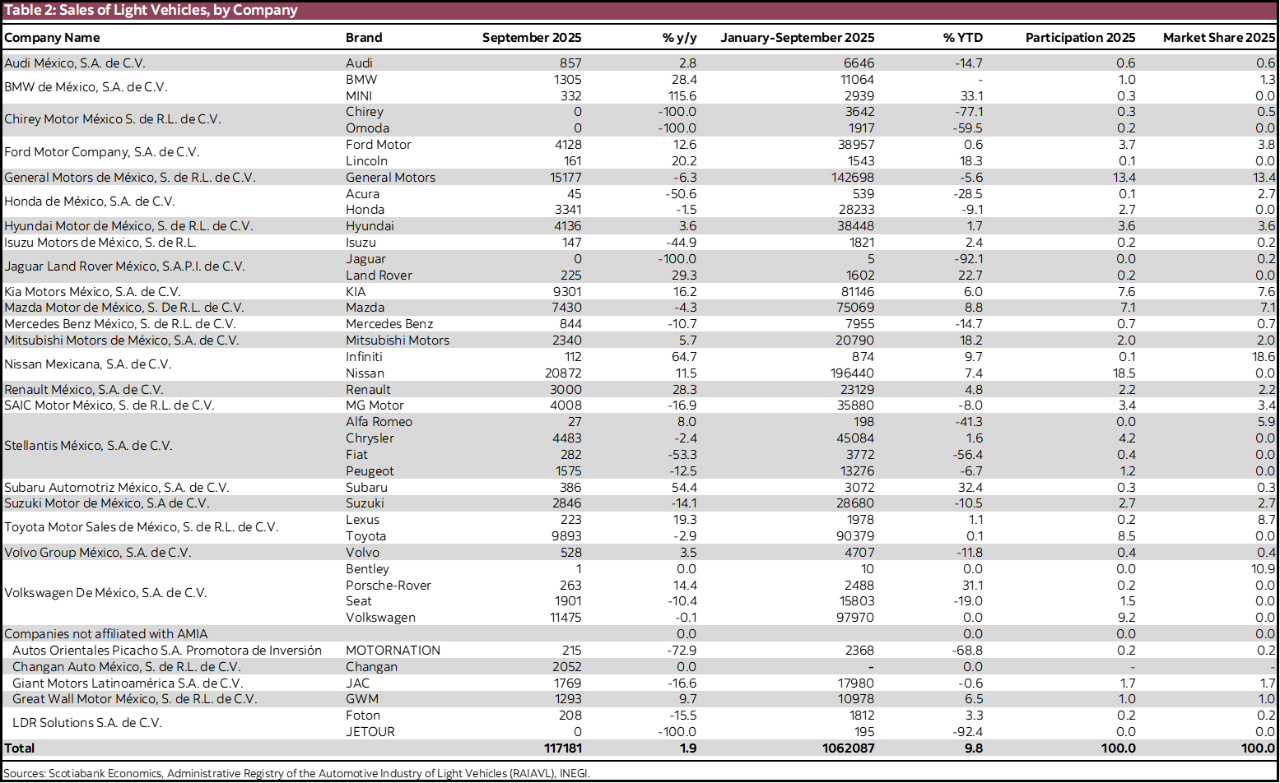

By brands (table 2), there is a drop in the share of new competitors (Motornation, JAC, Changan, Jetour) in light vehicle sales, which had gained ground in previous years to reach 9.7% of total sales in 2023, 9.5% in 2024, and 8.2% so far this year. In contrast, within the largest participants, some brands have rebounded, gaining market share, such as Nissan (18.3%), Toyota (8.4%), and Kia (7.5%), while other brands have decreased their market share, such as General Motors (13.3%), Volkswagen (9.1%), and Stellantis (5.9%).

This drop may partly owe to the fact that new competitors, mostly of Chinese origin, that has stimulated demand in previous years have lost ground so far this year. In addition, the initiative of the 2026 Revenue Law, which contemplates higher tariffs for imported vehicles of Asian origin, represents a downside risk for their domestic sales starting next year.

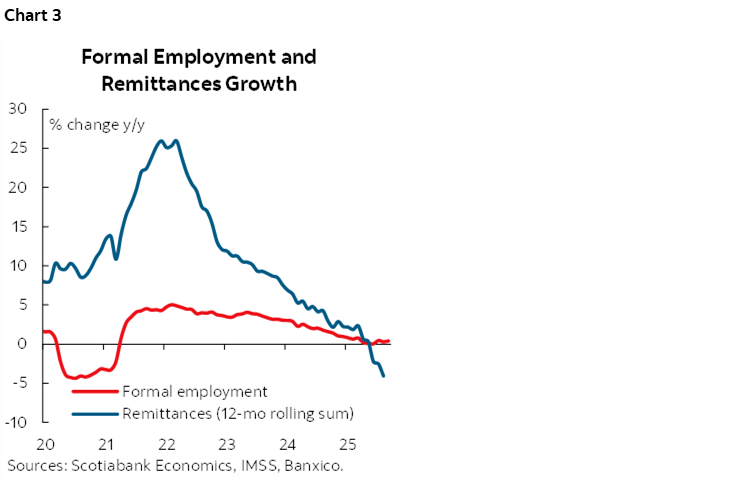

Another reason why these falls are observed is the weakness that the domestic environment continues to show. Sales are in a slump, possibly because consumption has been stagnant since September last year. It remained negative until June, with a real annual variation of 1.6% y/y, but is showing stagnation trends, with just 0.1% y/y growth in July. In addition to this, formal job creation remains weak with an annual advance of only 0.4% as of September, without considering the regularization of digital applications workers. In addition, remittances observed a 4.1% y/y drop on the aggregate of the past twelve months (chart 3), while consumer confidence has remained with minor changes in contraction territory, which suggests that domestic sales could continue their downtrend in the following months.

PRODUCTION AND EXPORT OF LIGHT VEHICLES

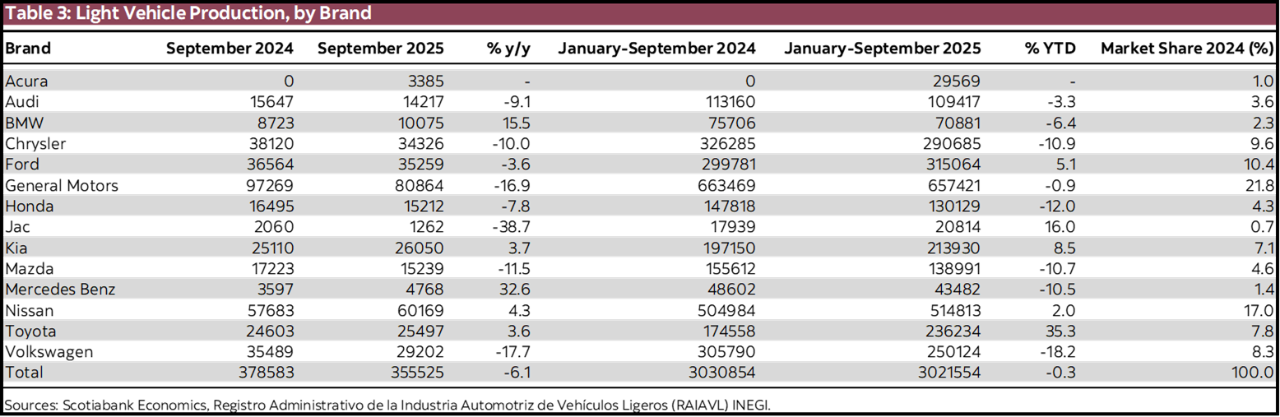

In September, the production of light vehicles registered an annual drop of 6.1% y/y, totaling 355,525 units (chart 4). This drop was reflected in the cumulative annual variation, showing a slight decline of -0.3% YTD compared to the same period of the previous year, in contrast to August, when a growth of 0.5% was observed. At the brand level, General Motors continues as the leader with the highest production in Mexico (table 3), although it presented a 16.9% drop compared to last year. The brands that have also presented declines are Ford Motor, Honda, Audi, Chrysler, Mazda, Volkswagen and JAC with the largest drop in production, -38.7%. Meanwhile, Mercedes-Benz had the highest year-over-year growth during the month, at 32.6%, along with Toyota (3.6%), Kia (3.7%), Nissan (4.3%) and BMW (15.5%).

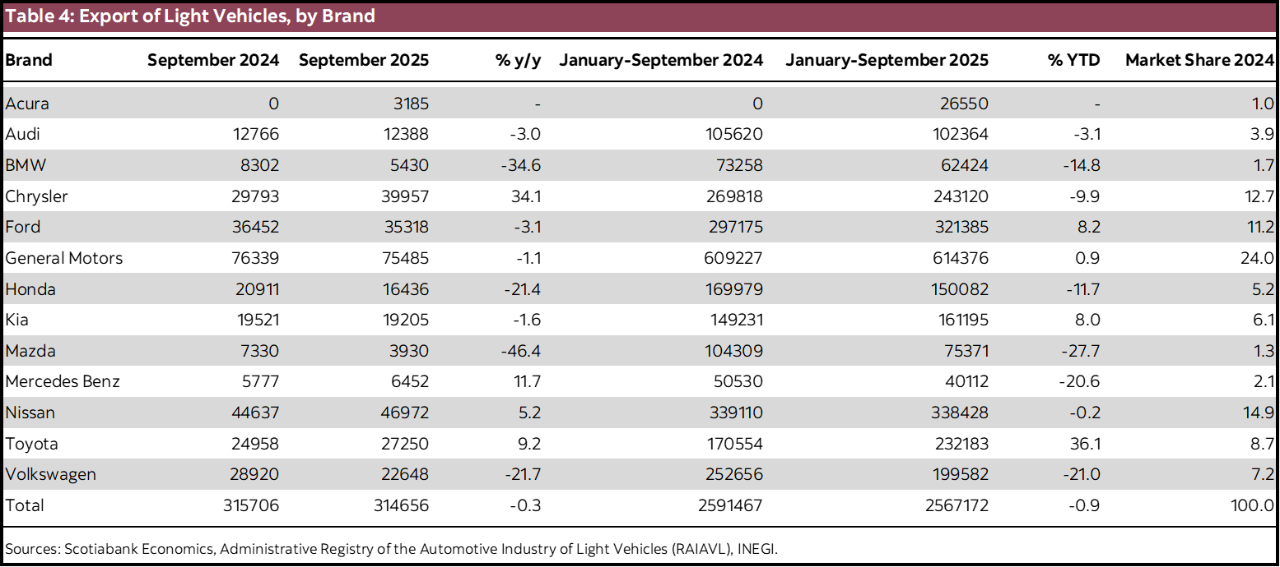

Exports also decreased slightly, falling -0.3% year-over-year, with 314,565 units, after four months of increases. Due to the sharp falls observed in the first half of the year, in the sum of the first quarters of the year, vehicle exports totaled 2.5 million units exported, equivalent to a fall of -0.9% y/y (table 4). By brands, those that have suffered the greatest contraction during the year are Mazda (-27.7%), Volkswagen (-21.0%), and Mercedes Benz (-20.6%), while Toyota and Ford have increased their shipments by 36.1% and 8.2%, respectively, and GM have remained practically stable, with an increase of just 0.9%.

The automotive industry represents 31.3% of the exports of the manufacturing sector, which shows its weight within the country's industrial activity. This link is reflected in the behaviour of manufacturing production, which has stagnated since April. The slowdown in automotive exports may have contributed to this performance, since external demand for vehicles directly influences the production levels of assembly plants and auto parts suppliers, thus affecting the manufacturing sector.

HEAVY VEHICLES: WIDESPREAD DETERIORATION

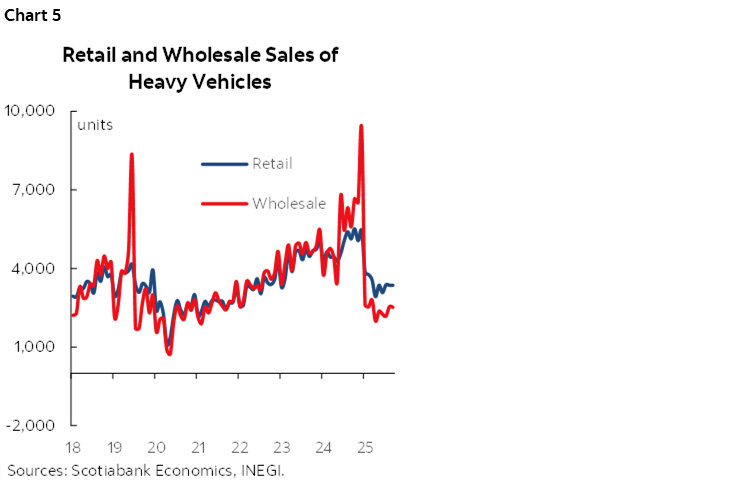

The slump in the heavy-duty vehicle industry from January to September remains pronounced, marking a stagnation of about a third below the levels of the same period a year earlier (chart 5). On the domestic demand side, sales of heavy vehicles presented an annual contraction of -34.6% y/y in retail transactions in September, while wholesale sales have a -55.0% y/y drop compared to the same month a year earlier. In the accumulated sum of the first three quarters of the year, retail sales total 30,644 units, while wholesale sales accumulate 21,763, equivalent to contractions of -27.5% YTD and -51.8% YTD, respectively. This weakness in domestic demand, especially in wholesale sales, is related to the stagnation of investment and business confidence, affected both by the international environment and by internal factors, such as uncertainty around judicial reform and more adverse security conditions.

External demand for heavy-duty vehicles is also affected by weaker prospects, although to a lesser extent than changes in domestic demand. In September, exports of heavy vehicles fell by -21.3% year-on-year, while in the cumulative January–September, the fall was -29.1% YTD, equivalent to 87,816 units. Even though export variations are lower than those observed in domestic sales, they face additional downside risks due to the announcement of tariffs in the United States on truck imports, despite the U.S. economy holding to expectations of moderate growth, which together with reindustrialization efforts in key areas represents a relevant support for truck exports.

In this context, the new 25% tariffs imposed by the U.S. on heavy vehicles from Mexico—justified by national security reasons—will significantly raise the cost of exporting, affecting the competitiveness of Mexican automakers. Although the USMCA grants tariff preferences to products that comply with rules of origin, the application of these tariffs has generated tensions since many Mexican vehicles do comply with the treaty (91% according to AMIA). However, the lack of clarity on exemptions and political pressure from the U.S. have called into question the effectiveness of the USMCA as a trade shield. In addition, Mexico has responded with measures such as proposals for 50% tariffs on Chinese vehicles, seeking to align itself with the U.S. and strengthen the North American bloc, which could be a strategic card in the next review of the treaty in 2026.

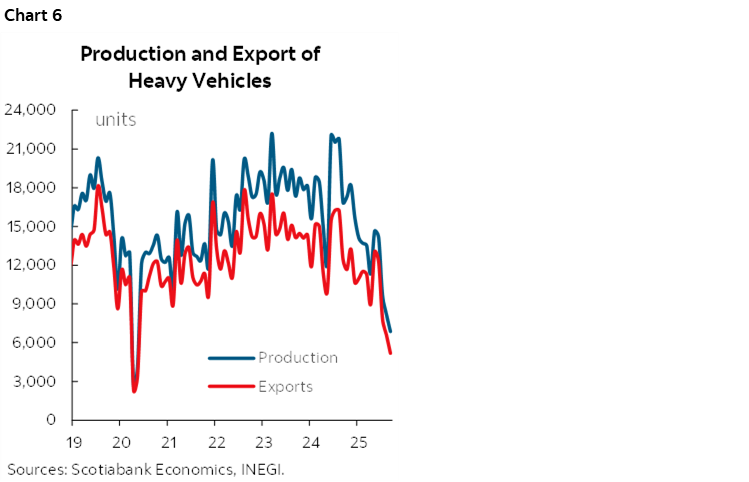

Finally, the production of heavy vehicles presents a greater deterioration, falling by -59.3% y/y during September (chart 6), while in the accumulated of the first nine months, the decline is -34.5% YTD. In this sense, the adverse domestic environment, together with the expectation of a more complicated trade relationship with the U.S. are key factors for supply prospects in the medium term, although industrial relocation efforts represent an upside risk for the industry.

IN CONCLUSION

The Mexican automotive industry faced a negative environment in the first three quarters of 2025. There is a stagnation in the production, export and sales of light vehicles, as well as a general deterioration in the heavy vehicles sector. The weakness of the domestic market reflects the persistent effects of national and international economic and political uncertainty, which have been accumulating since previous quarters. The industry is expected to be affected by U.S. trade policy announcements, particularly the imposition of new tariffs that raise the effective export rate, reducing the competitiveness of Mexican products in the U.S. market. In the domestic sector, the imposition of tariffs on vehicles also represents a downside risk to vehicle sales. In this context, the sector's recovery will depend largely on the evolution of the macroeconomic environment, regulatory certainty and investment conditions, both internal and external, in the coming months.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.