- FOMC confirmed it is in no rush to ease...

- ...but that the next move remains likely to be lower...

- ...as Powell leaned against hike risk

- Quantitative tightening flows will be tapered in June

- Markets generally liked what they heard

- BoC Governor Macklem also doesn’t sound like he’s thinking of a June cut

The FOMC smartly executed an overall set of communications that struck a balance between ruling out nearer term easing, sticking to the line that the most likely next move is down, while pouring cool—not ice cold—water on the risk of rate hikes. The result was taken reasonably well by markets and broadly met my expectations for Powell & Co not sounding more hawkish than what was already priced going in. Grade ‘A’ in my view.

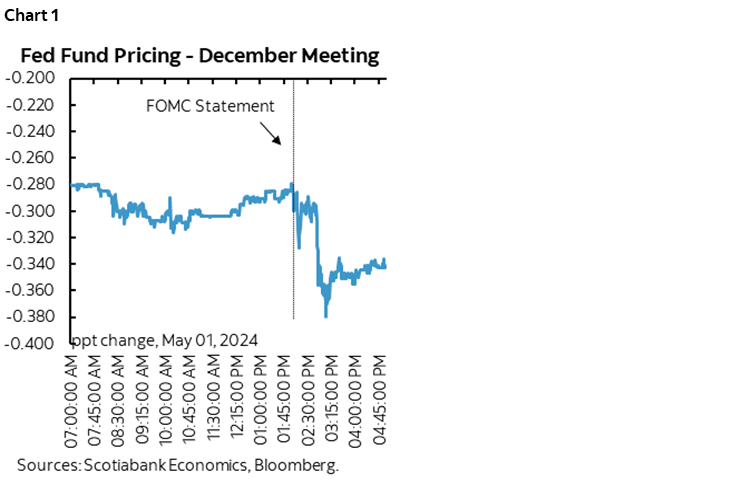

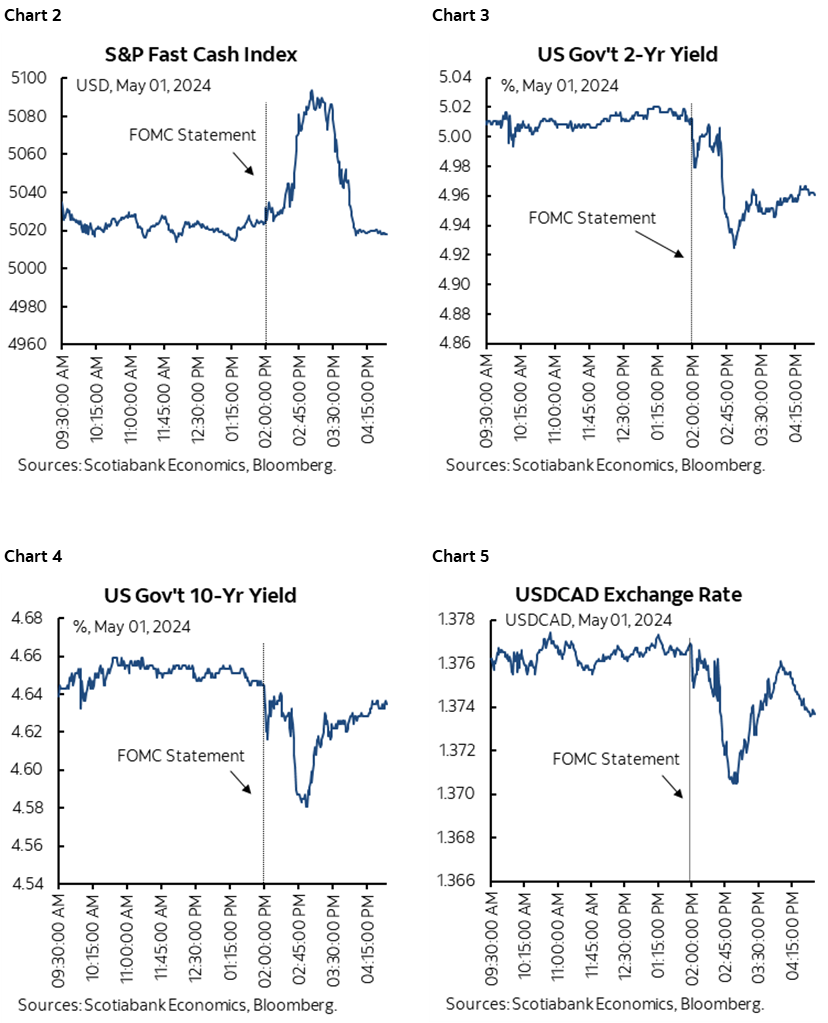

MARKETS SEE-SAWED BUT GENERALLY LIKED IT

Fed funds futures pricing for cumulative easing this year increased by a few basis points compared to just before the 2pmET statement (chart 1). Markets moved closer to being on the fence between one and two quarter point rate cuts by year-end. The S&P initially gained over 1%, 2s rallied by about 4bps, 10s rallied a touch, and the dollar weakened by about half a penny to CAD, but each of these measures gave back most of those moves into the close (charts 2–5).

OVERALL SUMMARY

Statement changes (see appendix) were devoid of hawkish signals relative to pricing and leaned in the other direction by shifting to a past tense reference to dual mandate goals that "have moved toward better balance." They announced a QT taper of the pace of roll-off of maturing securities held on their balance sheet to be implemented in June which was broadly in line with expectations. Powell's press conference laid out a baseline expectation for lower inflation over the duration of the year and that rate cuts may still be in store later in the year but that they lack the required "greater" confidence to do so in the nearer term with all meetings to evaluate incoming data. Stocks climbed by over 1%, the dollar weakened and market pricing for cumulative cuts by year-end increased by about 6–7bps to now being on the fence between one and two quarter point cuts. He also did not slam the door on hiking but generally poured cool water on it.

I think Powell also teed up a move toward projecting fewer cuts in the June dot plot. It would take only one of the 9 votes in the -75bps line in the March dot plot to move to -50bps in order to swing the median down to -50bps assuming no one else changed, just to highlight how close of a call it was even in March. It’s almost a certainty that the median projection will move lower in June. It’s unlikely they go as low as –25 which would take a lot of vote changes. It’s even more unlikely that the median drops any cuts.

Further elaboration follows.

QT PLANS—REDUCED ROLL-OFF STARTING IN JUNE

The statement and this implementation note from the New York Federal Reserve announced a tapering of quantitative tightening flows that will be implemented next month.

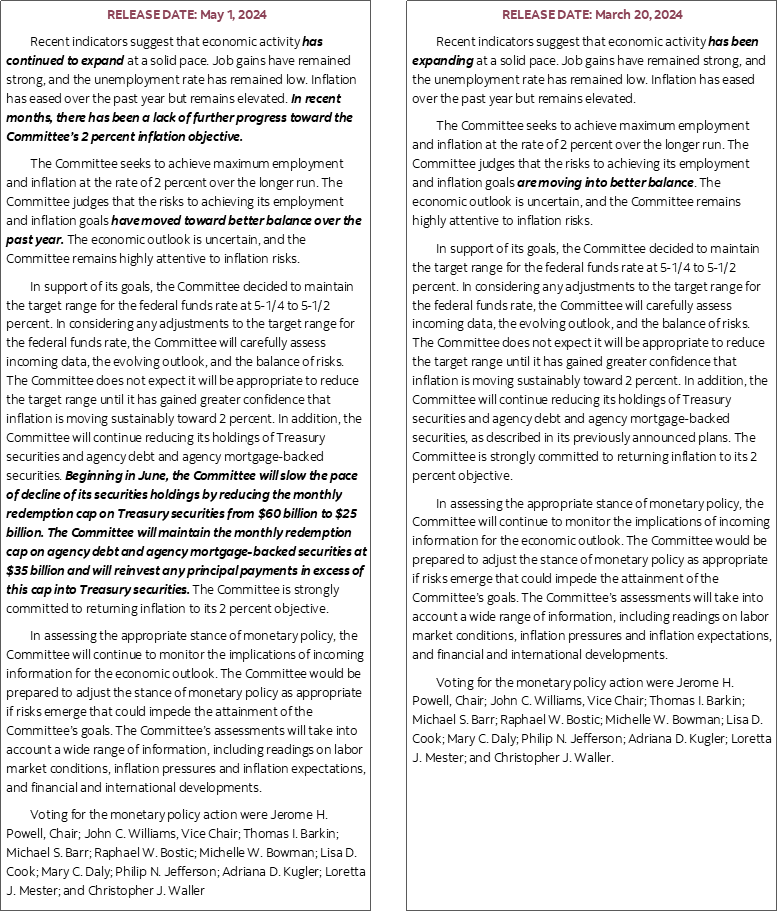

"Beginning in June, the Committee will slow the pace of decline of its securities holdings by reducing the monthly redemption cap on Treasury securities from $60 billion to $25 billion. The Committee will maintain the monthly redemption cap on agency debt and agency mortgage-backed securities at $35 billion and will reinvest any principal payments in excess of this cap into Treasury securities."

The purpose of taking this step is to not withdraw liquidity and tighten funding market conditions to the point of raising strains on the financial system as maturing bonds roll off the Fed’s balance sheet. Further important details are contained in the NY Fed’s release and the FAQs.

STATEMENT CHANGES—FEWER RISKS TO ACHIEVING GOALS

Other than the QT announcement there were a few other significant statement changes. Not that this was expected, but markets might have feared a hawkish pivot on the forward guidance that might have sounded more open to additional tightening. That was not the case.

The biggest change was the shift to this:

"The Committee judges that the risks to achieving its employment and inflation goals have moved toward better balance over the past year."

Compared to this in the March statement:

"The Committee judges that the risks to achieving its employment and inflation goals are moving into better balance."

That might seem like a subtle shift in tense, which it is, but it’s a powerful message in that the Committee is indicating more confidence that risks to the dual mandate goals of full employment and stable 2% inflation have come closer into balance. That still signals they are short of mission accomplished but to say “have” moved, instead of “are moving” is signalling that their look at the whole suite of readings has them not giving up achieving their goals and on the next rate move being down, not up.

Another key in the statement was the reference to how progress on inflation has stalled out which is their way of statement-codifying reference to not being in a rush to ease:

“In recent months, there has been a lack of further progress toward the Committee’s 2 percent inflation objective.”

The opening paragraph also shifted the tense on economic activity expanding at a solid pace.

Forward guidance was left unchanged. It remains data dependent and generic by repeating how “the Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge.”

There were no dissenters.

IN NO RUSH TO CUT

Powell’s opening comments in his press conference had him coming out swinging by noting "considerable progress" toward dual mandate goals and "that's very good news" but inflation remains too high. He continued to argue that supply and demand conditions in the labour market have come in to better balance, that there continues to be strong job growth but also strong immigration and a higher participation rate to aid a rebalancing of the labour market as wage growth has ebbed but that labour demand still exceeds supply. He also noted that longer term measures of inflation expectations remain well anchored across a broad array of measures. None of that sounded like a guy thinking of further tightening—or abandoning and hope of easing.

Chair Powell’s press conference made it clear that the Committee is in no rush to cut. He did this by saying the following:

- "so far this year the data have not given us that confidence" that dual mandate goals have been achieved.

- "it is likely that further progress will take longer than expected"

- “We've seen enough data and should take some signal and we are taking signal and the signal we are taking is that it is likely to take longer to gain confidence that we are on a sustainable path to 2% inflation.”

- he repeated that they will make decisions meeting by meeting, conditional on data

...BUT THE BASE CASE REMAINS IN FAVOUR OF LOWER EXPECTED INFLATION...

Powell made his own base case outlook very clear when he said:

"My forecast is that we will see inflation come back down over the course of the year"

He elaborated upon this by flagging the argument that lower market rent rates should show up in lower shelter inflation but with uncertain lags.

...AND AN ONGOING EASING BIAS WITH VERY LITTLE APPETITE FOR MORE HIKES

When asked during the press conference “Is the current policy rate sufficiently restrictive?” Chair Powell said:

“I do think the current policy rate is restrictive and weighing on demand. You can see that in the labour market. You saw that in the JOLTS report this morning. The same is true of quits and hiring rates that have normalized. Consumers and businesses are indicating that the supply and demand of jobs has come back down. We believe it is restrictive and over time will be sufficiently restrictive.”

"We believe our policy is in a good place. We believe it is restrictive. You see it in the labour market. You see it in interest sensitive spending."

Now while that doesn’t explicitly rule out hikes, any sensible person would have heard that it’s very unlikely.

Powell went on to state more deliberately in response to further questioning that

“It's unlikely that the next policy move will be a hike. Our policy focus is upon how long it would take to remain restrictive. We would look at the totality of the data. If we were to come to that conclusion that policy is not tight enough due to a totality of evidence then that's what it would take to take that step” [ie: hike].

Apparently that either wasn’t enough, or journalists in the presser were ticked someone else had already asked their favourite question, so they tried again by asking if he has dropped his easing bias to which he answered:

“Our decisions will depend upon incoming data, the totality of the data. We think policy is well positioned to address different paths that the economy might take. If we did have a path where inflation proves more resilient and the job market is still strong but inflation is moving strong then that would be a path to hold off on rate cuts. Inflation moving sustainably down could give us confidence to begin cutting rates. So could an unexpected weakening in the labour market. The data will have to answer the question for us in terms of peak rate.”

A better question was whether the Committee felt it still had time to cut three times this year as per the March dot plot and given the meeting calendar. Powell said:

“I don't think of it that way. We need more time. We didn't see progress in the first quarter. It's going to take longer to reach that point of confidence. I don't know how much longer it will take. When we get that confidence then rate cuts will be in scope.”

Where Powell’s delivery stumbled somewhat was in response to whether there was any discussion about a rate hike in today's meeting and whether he is satisfied with 3% for the rest of the year to which he replied:

“Of course we're not satisfied with 3% inflation. We think our policy stance is appropriate to achieve that. The policy focus has really been on holding the current level of restriction. That's where the discussion was focused."

Maybe it was dragging on and he was getting a tad frustrated with the same repeated line of inquiry, but I didn’t like the stammering and shifty body language that made Powell seem uneasy while answering that last question.

A PREDICTABLE ANSWER ON THE ELECTION’S EFFECTS

Powell was asked “Is the bar for rate changes higher closer to an election?” and his answer was delivered in a somewhat terse manner, yet a thoroughly predictable one.

“We are always going to do what we think is the right thing to do for the economy. That's hard enough to do and taking in other things reduces our chance of doing the right thing for the economy.”

When asked in another way about whether there is a difference in cutting in September versus December, he flippantly said:

“There's a significant difference between an institution that takes into account political events and one that doesn't. Read all the transcripts around past elections and you won't see any discussion around elections.”

BANK OF CANADA GOVERNOR ALSO SOUNDED IN NO RUSH TO EASE

After the dust had settled on what the Fed has done, Bank of Canada Governor Macklem and Senior Deputy Governor Rogers began testimony before a parliamentary committee. The opening statement (here) did not sound amenable to cutting the policy rate as soon as the June meeting to me. That reinforces our expectation for easing no earlier than the July or September meetings, though we are aware of the need to evaluate incoming data.

Key in this regard are the following passages toward the end:

“Overall, the data since January have increased our confidence that inflation will continue to come down gradually even as economic activity strengthens. Our key indicators of inflation have all moved in the right direction and recent data point to a pickup in economic growth.”

“I realize that what most Canadians want to know is when we will lower our policy interest rate. What do we need to see to be convinced it’s time to cut? The short answer is we are getting closer. We are seeing what we need to see, but we need to see it for longer to be confident that progress toward price stability will be sustained.”

“In the months ahead, we will be closely watching the evolution of core inflation. We remain focused on the balance between demand and supply in the economy, inflation expectations, wage growth and corporate pricing behaviour as indicators of where inflation is headed.”

“To conclude, we’ve come a long way in the fight against inflation, and recent progress is encouraging. We want to see this progress sustained.”

On timing rate cuts, key here is that “we need to see it for longer,” and “in the months ahead,” and “we want to see this progress sustained.”

We get one more inflation report before the June meeting, but the “months ahead” reference seems to me like they are setting a high bar against this being sufficient.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.