ECONOMIC OVERVIEW

- After a benign Fed decision and an as-expected 50bps rate cut by BanRep, we now have what should be unsurprising rate cuts by the BCRP and the BCB, and a rate hold by Banxico. The same cannot be said for guidance, however, especially in Brazil and Mexico where the rate path is clouded by inflation and Fed risks. RBA and BoE announcements should also be placeholders ahead of eventual first cuts.

- In today’s Weekly, our teams in the Pacific Alliance preview next week’s CPI releases from Chile, Mexico, and Colombia, as well as Banxico’s and the BCRP’s rate announcements. In Colombia, our economists also do a deep dive into pension reform plans as the June 20th deadline for legislation quickly nears.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico and Peru.

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period May 4th–17th across the Pacific Alliance countries and Brazil.

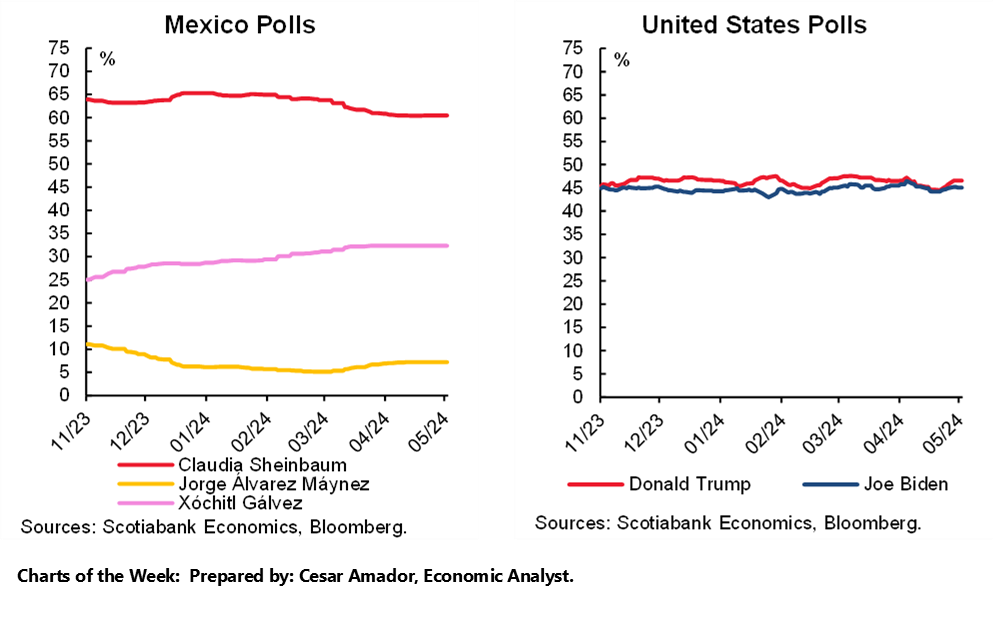

Charts of the Week

ECONOMIC OVERVIEW: BANXICO, BCRP, REGIONAL CPI, AND COLOMBIA POLITICS

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- After a benign Fed decision and an as-expected 50bps rate cut by BanRep, we now have what should be unsurprising rate cuts by the BCRP and the BCB, and a rate hold by Banxico. The same cannot be said for guidance, however, especially in Brazil and Mexico where the rate path is clouded by inflation and Fed risks. RBA and BoE announcements should also be placeholders ahead of eventual first cuts.

- In today’s Weekly, our teams in the Pacific Alliance preview CPI releases from Chile, Mexico, and Colombia, as well as Banxico’s and the BCRP’s rate announcements. In Colombia, our economists also do a deep dive into pension reform plans as the June 20th deadline for legislation quickly nears.

We find ourselves in a busy period of key macroeconomic releases and central bank decisions around the globe. However, as it concerns the latter and thankfully for beaten markets, there hasn’t been major surprises. The BoJ did not hike unexpectedly, nor did the Fed or Chairman Powell give serious thought to the remote possibility of increasing rates. We also don’t think the RBA or BoE will deliver unexpected rate changes. With the Fed decision behind us, maybe rates markets could enjoy a partial retracement of sharp losses since the start of the year, while remaining apprehensive on US rate cuts, and Latam currencies could take off some of the weight of attractive US yields.

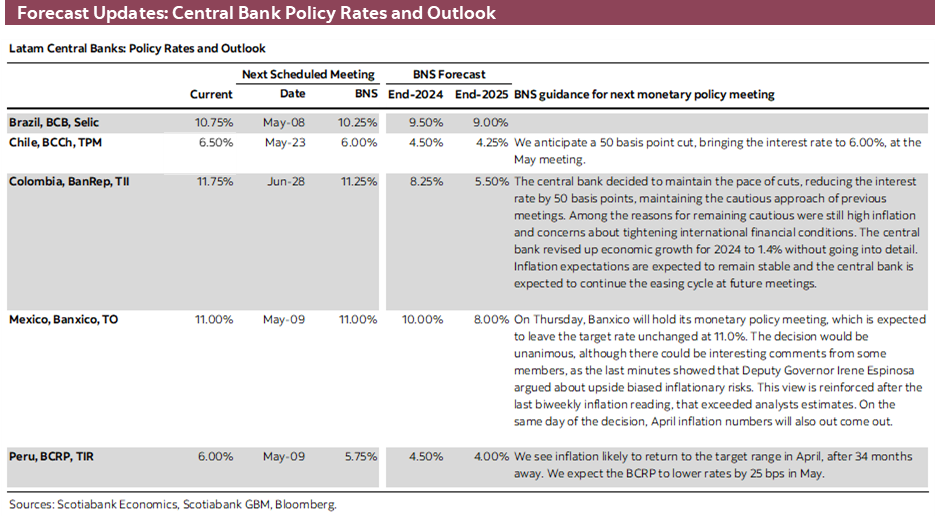

In Latam, BanRep delivered a universally anticipated 50bps cut in a split vote at its April 30th decision (see our team’s recap here) and reaffirmed its cautious stance—much to the chagrin of super dove Fin Min Bonilla. We’ll get a bit more colour from local officials at the Monetary Policy Report press conference on Tuesday, with a focus on their assessment of external risks (namely, rising US yields) impacting domestic inflation balanced against a weak economic backdrop. Monday’s April meeting minutes are also worth a look.

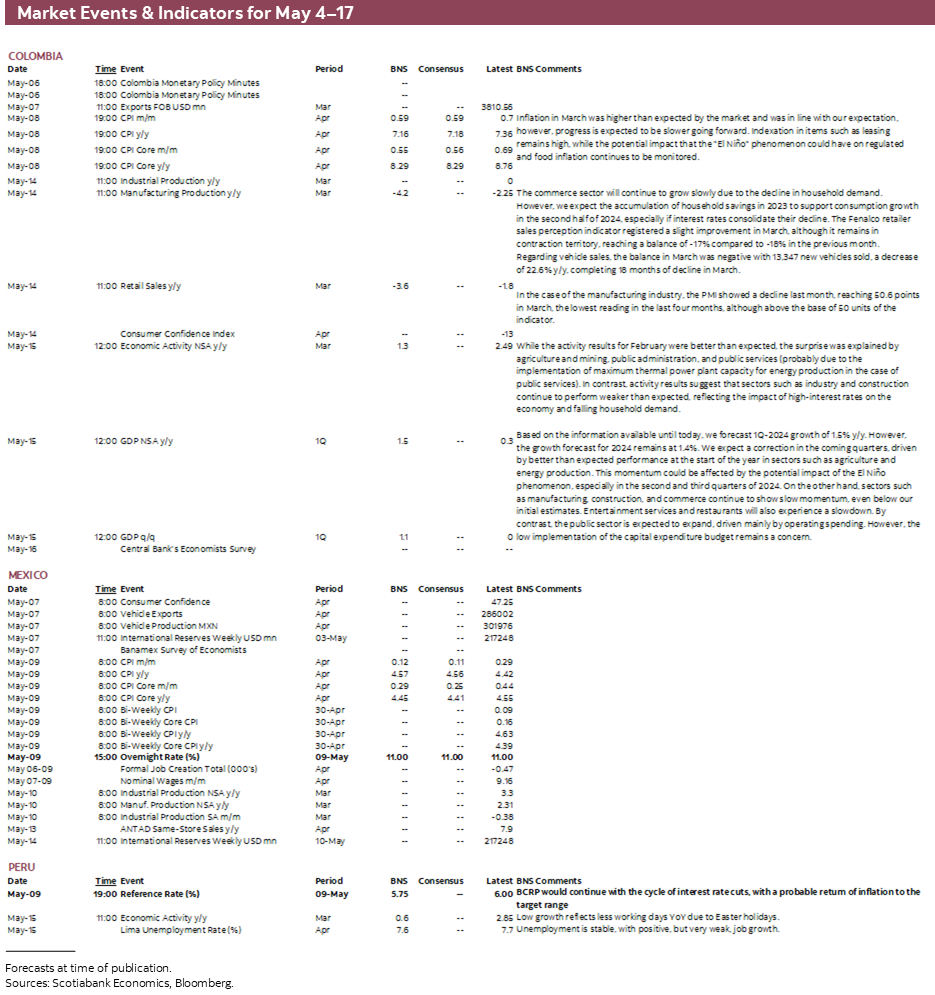

BanRep communications will be important to follow, but the highlight of Colombia’s week ahead will be Thursday’s after-market release of April CPI and also developments on the political front. Starting with inflation data, next week’s print may be somewhat disappointing for officials as indexation practices hold core and headline inflation at elevated levels; we still expect decelerations in April, but core inflation should still come in above 8% y/y. As for politics, our Bogota team discuss pension reform developments as the government faces a time crunch to the June 20th deadline to legislate the proposal. In parallel, Petro’s team is expected to present to Congress an economy recovery/support package in coming days, where the biggest risk is the possibility of changes to the fiscal rule.

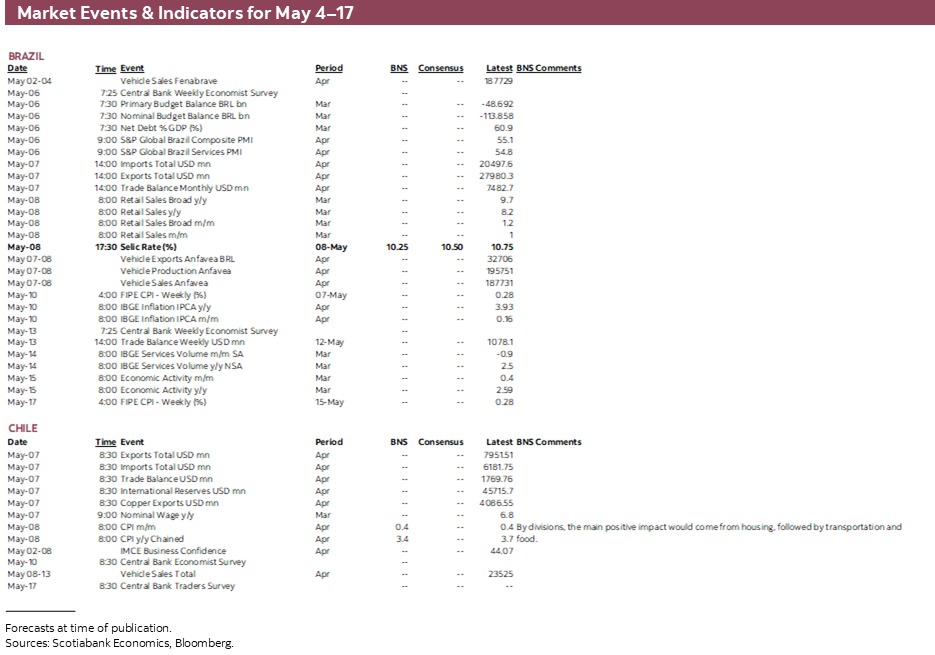

Mexico’s and Brazil’s calendars look about the same. Both countries release CPI data for April, and in both countries we get central bank announcements. But, as far as the data and the actual rate decisions go, there is no major dispersion in views. Mexico and Brazil publish mid-month inflation figures that intimate the bulk of the full-month readings. The BCB is widely expected to cut 25bps after six consecutive and well-telegraphed 50bps moves. Now, the focus shifts to guidance as markets and economists have turned much more uncertain about how much more policy loosening is in store.

From Banxico, after a cautious rate cut in March, now a rate hold is universally expected as policymakers take their time amid stubbornly-high core inflation and upside pressures on non-core prices; setting aside a recent slowing of the economy. Fed guidance has also been an important influence on Banxico policy rate expectations. Our Mexico team go over their expectations for next week’s CPI data and Banxico’s decision in today’s report, outlining that inflation may evolve in a way that may only see two more 25bps cuts delivered instead of our current forecast of four more cuts by year-end. Continue to watch election polls, too, as Sunday marks the start of a four-week countdown to the June 2nd vote.

Peru’s central bank is also scheduled to deliver a policy announcement next Thursday, and theirs also looks like a done deal with a 25bps rate cut to 5.75% on tap. We already thought the bank would opt to cut again as it has in seven of its last eight decisions—only surprising with a hold in March—and this view was reinforced by Wednesday’s miss and sharp deceleration in headline inflation to 2.4% that leaves the BCRP with little reason to hold. In today’s Weekly, our economists in Lima discuss the recent prices data, highlighting a large m/m decline in food prices that is welcome news, yet driven by poultry and fish prices and not agricultural prices that have yet to normalise from El Niño shocks.

Finally, Chile’s INE releases the first of next week’s April prices data on Wednesday. The team in Chile projects a steady pace of monthly inflation at 0.4% m/m, a still-too-high number that would result in a 3.4% y/y reading. However, as they outline in today’s report, roughly half of this overall prices increase will owe to energy/fuels prices , and they also projected that inflation ex. volatiles will make a strong move lower towards target; from 3.7% to 3.3% y/y thanks to easing services inflation. All in all, data are evolving in the right direction for the BCCh, but external factors remain a worrying factor as even BCCh Pres Costa has highlighted; data and markets dependence is well entrenched.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—We Project April CPI of 0.4% m/m (3.4% y/y)

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

- Half would be explained by fuel hikes

We project April CPI of 0.4% m/m (3.4% y/y), above market expectations in forwards (0.34%) and surveys (Economists and Traders’ Survey: 0.3%). Likewise, we project that the ex-volatile CPI would increase 0.4% m/m (3.3% y/y), mainly due to the contribution of goods, reflecting part of the effects of the exchange rate increase observed in the last few months. On the other hand, services would increase by 0.3% m/m, leaving behind the indexation and second-round effects observed in the Q1-2024.

By divisions, the main positive impact would come from housing, followed by transportation and food. In the first two divisions mentioned, the increase in fuel prices stands out, which would be reflected through increases in the price of LPG, kerosene, diesel and gasoline. With respect to the latter, we project a pause in price increases in the coming weeks. However, the positive impact of gasoline on the CPI will still be present in May’s CPI (+0.1 ppts), although it could disappear as of June. In total, the impact of the aforementioned fuels would be 0.2 ppts in April, half of the CPI forecast for the month. As for food, the main positive impacts we project would come from non-perishables and dairy.

Core inflation is rapidly approaching 3%. CPI ex-volatiles would fall from 3.7% to 3.3% y/y, mainly due to lower services inflation and a stabilization of goods inflation. Similarly, CPI inflation less food and energy would fall from 2.6% to 2.5% y/y, also due to lower services inflation.

Colombia—Pension Reform: Against the Clock to Get the Final Approval

Jackeline Piraján, Senior Economist

+57.601.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Daniela Silva, Junior Economist

+57.601.745.6300 (Colombia)

daniela1.silva@scotiabankcolpatria.com

Despite this year being especially challenging for government reforms, the Pension Reform had a stunning advance in recent weeks, ending with the approval of the Senate Plenary, the second out of the four debates the reform must pass before becoming a law. The government, however, is running against the clock to clean all the processes to have the final approval. The schedule is very tight; either way, if the reform passes, the most important discussion will be around the regulation of the law, which could take even longer to be completely known.

How has the Pension Reform process been?

The government presented the Pension Reform bill on March 22nd, 2023. The proposal is looking to change the current pension scheme, which is composed of two competing sub-systems: the public (pay-as-you-go/defined benefit) and the private (defined contribution scheme) to a pillar scheme of four groups. The first group, the solidarity pillar, guarantees a subsidy for those older adults who are in a situation of vulnerability. The second is the semi-contributory pillar, which provides a life annuity for those who contributed but did not meet the minimum number of weeks required for a pension. The third is the contributory pillar, in which there is a mandatory contribution from all the formal employees in Colombia. The idea is to create a fund that guarantees a high replacement rate; however, limits the benefit up to 2.3 minimum wages (which is currently around USD 767), that means that contribution to this pillar can be over a minimum salary and limited up to 2.3 minimum salaries. The fourth pillar is individual savings, which will be managed by existing private pension funds with contributions above the threshold of 2.3 minimum wage threshold.

On June 14th, 2023, the reform was approved in the first debate in the Senate Commission VII, where some propositions were approved, such as reducing the number of weeks of contribution to access a pension in the contributory pillar and to whom the transition regime would apply, which means that more people will not be affected by the reform. During the second half of 2023, the project did not make any progress because the government had its eyes set on health reform which failed to get approved.

At the beginning of 2024, opposition parties tried to delay the Pension Reform discussion, breaking the quorum in the initial sessions. However, the government reached some consensus with the Liberal Party, which helped the project pass the second debate. In the second debate, relevant agreements were reached, such as reducing the contribution threshold of the contributory pillar from the original proposal of 3 to 2.3 minimum wages and ensuring that this fund will be managed by BanRep and not by Colpensiones as originally proposed.

Now, the bill is getting ready to be debated in the House of Representatives, where additional modifications could be made, such as the bill’s entry into force, which so far would be in July 2025 according to what was approved by the Senate Plenary, and some discussions on the threshold of the contributory pillar since the government has recently insisted that it should be 4 minimum wages.

With only seven weeks remaining for the project’s approval, the path to success lies in the consensus and fluid discussions with other parties. These factors will prove crucial in navigating the remaining uncertainties and ensuring the reform’s effectiveness.

What are the critical points of the Pension Reform discussion?

In our opinion, Pension Reform has positives and uncertainties. On the positive side is the proposed transition from a competing sub-system characterized by arbitrage and the fact that very wealthy people have high pension subsidies to one scheme in which subsidies are limited and coverage increases to those people who, during their lives, lived in informality without the possibility of having a pension.

On the uncertain side is how the new scheme of pillars will be managed, especially the sovereign reserve pension fund. Under the current scheme, private pension funds have AUM equivalent to 30% of GDP. With the reform, the stock will remain under private pension funds management. However, around 85% of forthcoming contributions will go to the new reserve pension fund, and this raises two significant questions:

1) How could the regulation for private pension funds change?

2) Who will manage the fund, and how will the public pension reserve fund be managed?

Regarding the first question, private pension funds will maintain their current AUMs and will manage contributions above the threshold of 2.3 minimum wages. Pension funds currently charge affiliates fees on the contributions; however, with the reform, the management fees are proposed to be 0.7% on AUMs. In our opinion, it is still important to see how further regulation could change and if the final framework could modify competition incentives across private pension fund systems.

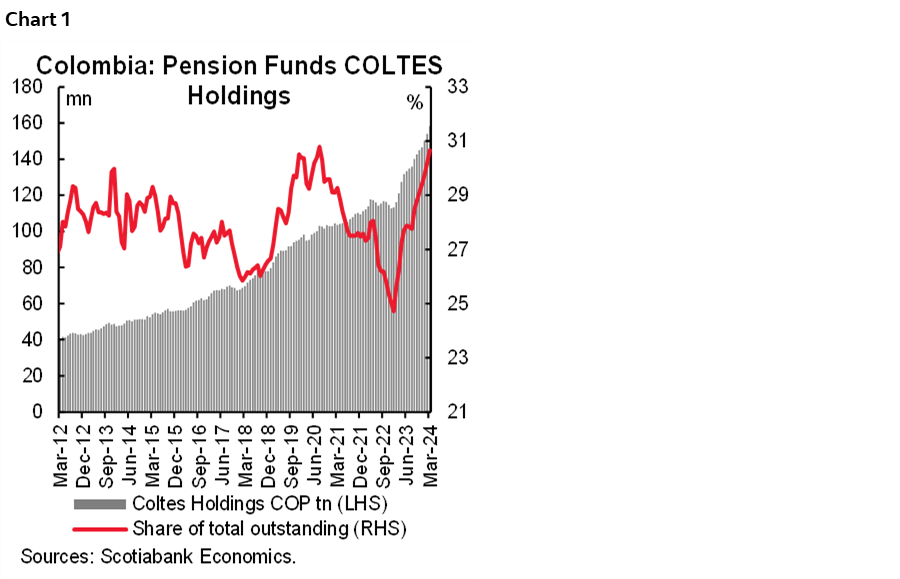

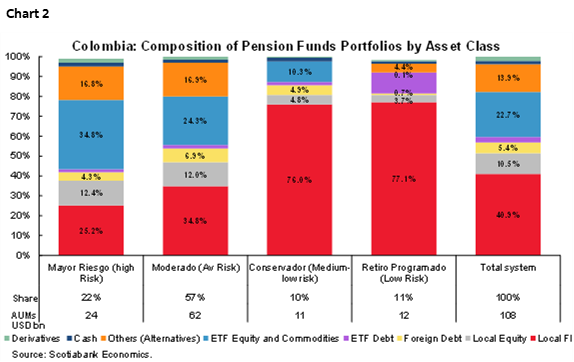

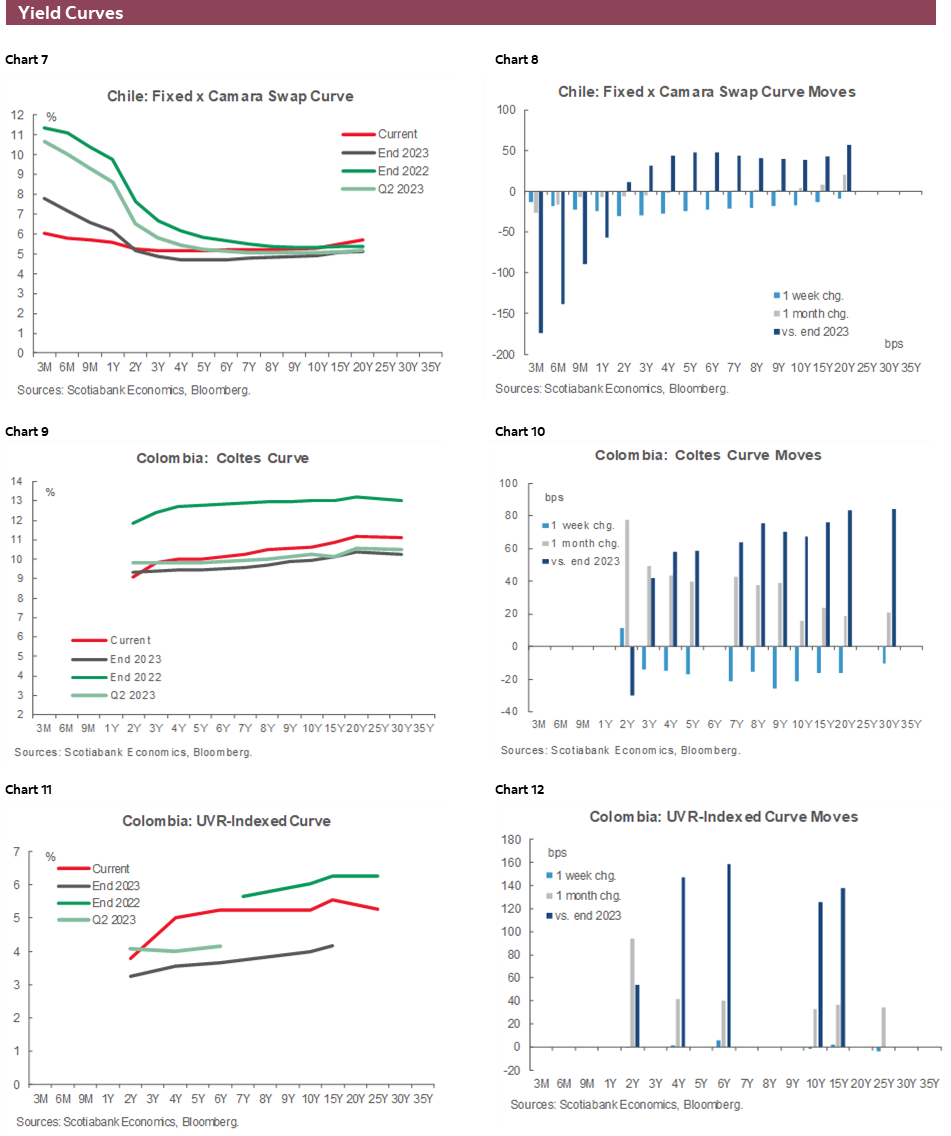

The pension fund currently has around 30% of COLTES outstanding (chart 1), and investments are split all across the yield curve. In the current scheme, private pension funds have four portfolios, and the decumulation fund and the conservative fund concentrate the major positioning in COLTES (chart 2). We see a danger if regulation fails to incentivize competition for profitability since it will, in turn, impact the dynamism of the COLTES markets.

Regarding the second question, the Senate Plenary proposed Banco de la República as responsible for managing the pension fund, which, in our opinion, is a strong confidence vote. However, on this point, the issue is also about regulation. Under the current constitutional framework, the central bank doesn’t have enough clarity on the scope of the responsibility of managing pension savings. In our opinion, the positive side of the situation is the fact that Congress wants to protect pension savings, and the uncertainty is what the mandate of the institution that will be responsible for the investment of those savings will be.

All in all, there are two conclusions. The first one is that the schedule to get the approval is very tight, and the second one is that the final regulation is critical. However, this goes beyond the scope of Congress and will only be known during the transition of the potential implementation of the reform. That said, it is very early to anticipate a final output.

What’s next?

The Seventh Commission of the House of Representatives is expected to start to work on the Pension Reform on May 9th, and it should not spend more than two weeks deciding on the approval. If everything is okay, the Plenary of the House of Representatives will be on June 1st, having only two weeks to approve, and on June 20th, the date of the official deadline, the conciliation should take place. That said, the Pension Reform is at the edge of the knife between the success.

Regarding regulation, the broad lines of functioning will be established by Congress, such as the possibility of BanRep managing the pension fund. However, the details about benchmarks and competition, among other relevant issues, won’t be defined sooner. Having those elements in mind, it is very early to anticipate a final impact on financial markets. However, we highlight that Congress is pushing to protect pension savings, which at least lets us think that pension savings will continue to be a relevant actor in the COLTES market.

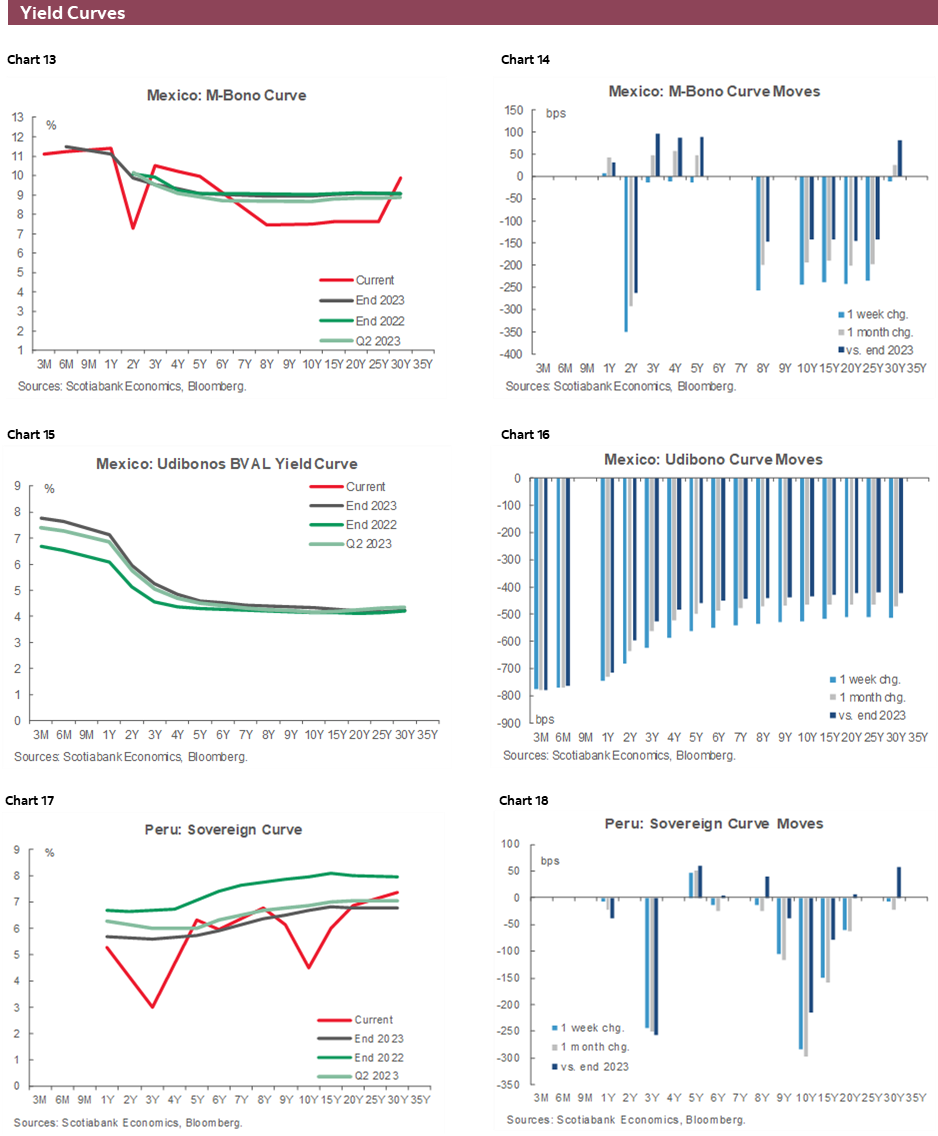

Mexico—Possible Year-End Rate Scenarios for Banxico

Brian Pérez, Quant Analyst

+52.55.5123.1221 (Mexico)

bperezgu@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

On Thursday of next week, Banxico will hold its monetary policy meeting, which is expected to leave the target rate unchanged at 11.00%. The decision would be unanimous, although there could be interesting comments from some members, as the last minutes showed that Deputy Governor Irene Espinosa argued about upside biased inflationary risks. This view is reinforced after the last bi-weekly inflation reading, that exceeded analysts’ estimates (4.63% y/y, 4.48% consensus), due to the increase in the non-core component (+5.38%), affected by agriculture and livestock. Meanwhile, in core inflation, services remained flat (+5.21%), maintaining a significant upside risk derived from wage cost pressures and a strong labour market. On the same day of the decision, April inflation numbers will also come out, which we expect to increase in line with the bi-weekly data, this time to 4.57 y/y (vs. 4.42% in March), and core inflation to continue falling to 4.45% y/y (vs. 4.55% previously). Thus, we believe that the rebound will come this time from the more volatile non-core part, specifically from agricultural items.

We believe Banxico has room to make four additional rate cuts this year, arguing that the real rate would remain restrictive and high enough to at least bring inflation down to 4.0% (in Q1-2025). However, we also see a strong scenario in which there could be only two cuts during the year if the inflation data forces the board to have doubts about reaching the target over the forecast horizon (3.1% in 2025). On the other hand, although it is not the central bank’s objective to maintain the rate spread, we expect it to remain close to 550bps, taking into account that the current market scenario now expects only one cut this year by the Fed, since the FOMC indicated that the probability of a new increase is low and J. Powell’s statements indicated that the following movements would be downward, but over a longer period of time.

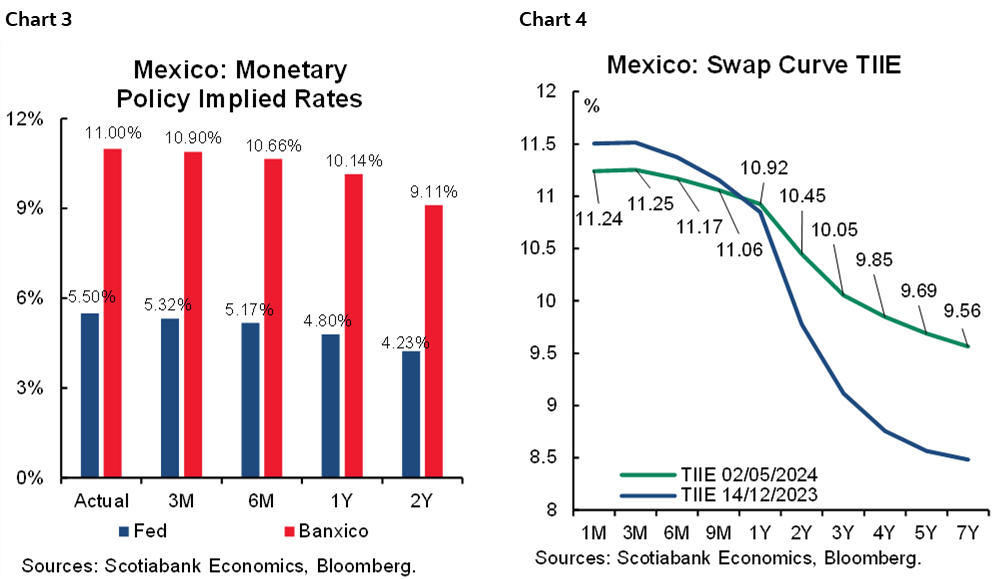

Implied rates point to a rate of 10.66% in six months, that is, the market is slightly undecided on whether there may be one or two cuts for the rest of the year, while, for the Fed, they stand at 5.17%, having the same problem of one or two cuts (chart 3). However, if we compare the current TIIE swap curve with the one observed in December 2023, we can see that the short term of the curve has had a reduction of approximately 26bps, in line with Banxico’s cut, while in the longer term nodes it has had the opposite effect, with an increase of approximately 100bps, so the market expects rates to be high for longer (chart 4).

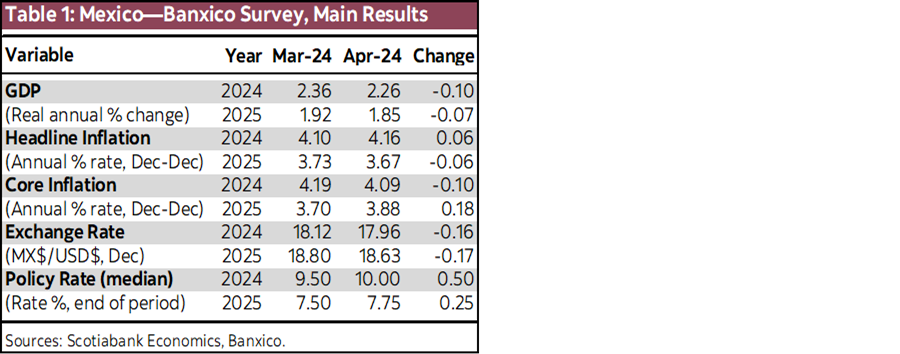

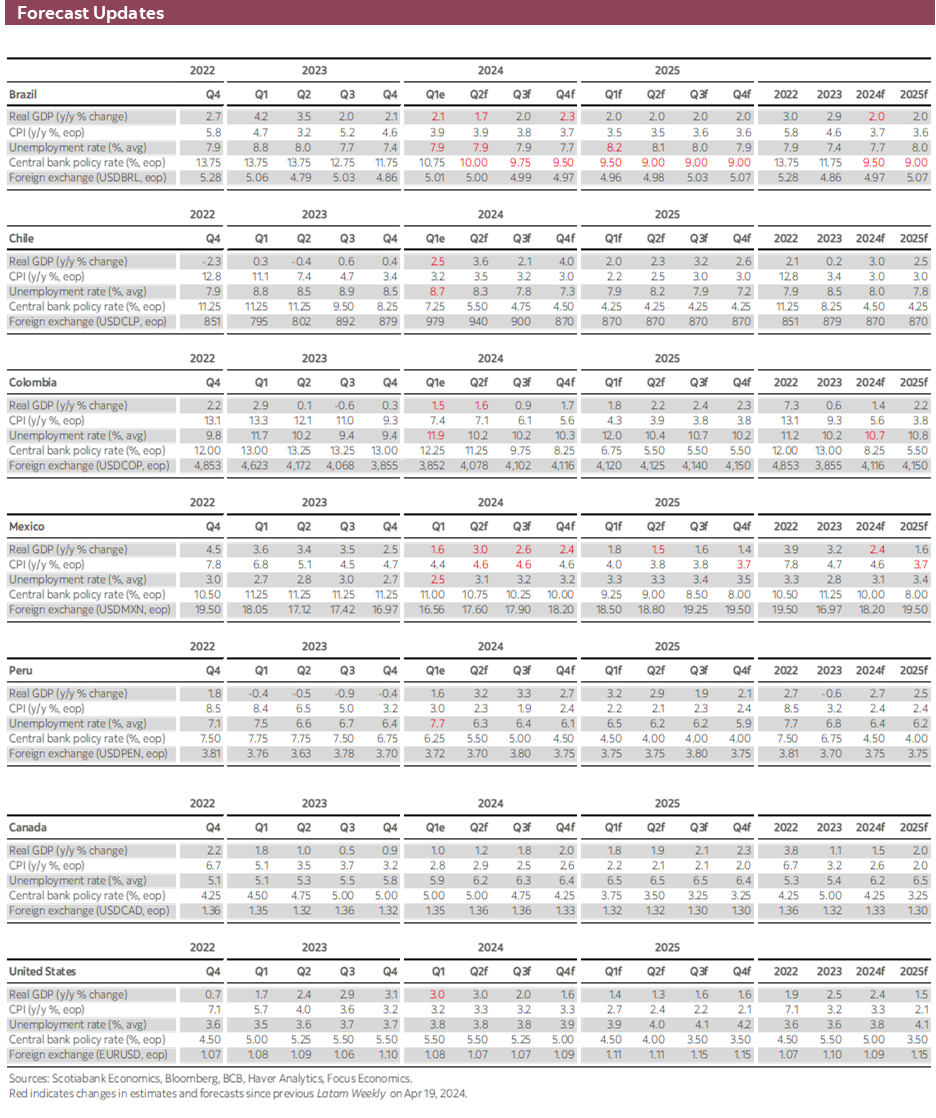

In the Banxico survey, the median of analysts’ responses increased and now forecasts a year-end rate at 10.0% (9.50% previously), in line with our outlook, although with several possible scenarios in a range of 8.75%–10.50%, and at 7.75% in 2025 (7.50% previously). Inflation for year-end rose to 4.16% (4.10%), and for 2025 it remained at 3.73%. As for GDP growth, it was revised slightly downward to 2.26% (2.36% previously), and for next year, consensus forecast slowed to 1.85% (1.92% previously), see table 1.

Peru—Low Inflation Puts BCRP Under Further Pressure to Lower its Policy Rate

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

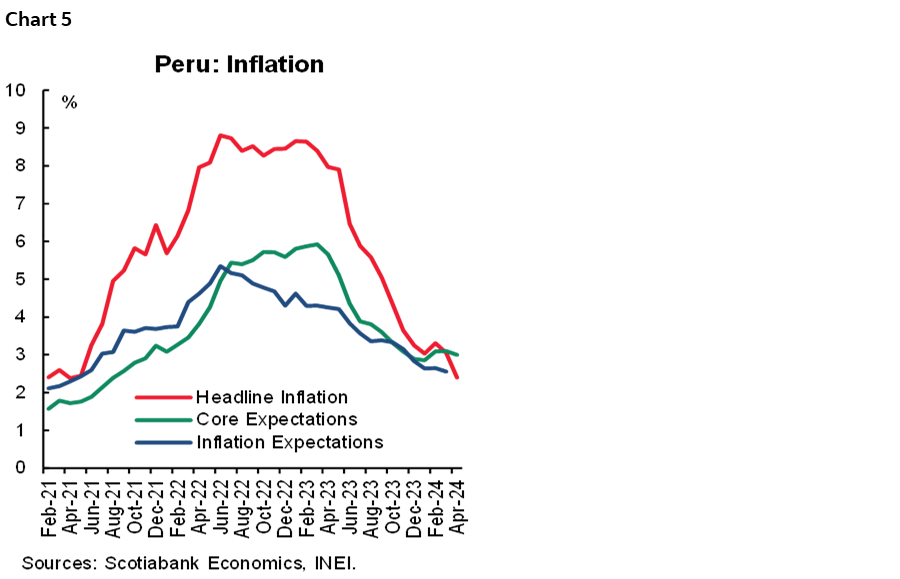

Next week’s calendar in Peru is all about the BCRP policy rate decision. We expect the BCRP to lower the rate from 6.00% currently, to 5.75%. This appears to be the more rational choice, after the surprisingly great decline in April yearly inflation, from 3.0% a month earlier to 2.4%, and considering that monthly inflation in April was negative, -0.05%. To round out the downward-pointing data, core inflation fell from 3.1% to 3.0%, which isn’t much of an improvement, admittedly, but is in the right direction.

Equally significant, if not more, inflation expectations fell from 2.65% to 2.56%. The real reference rate now stands at 3.19%, and would fall to 2.94% with another 25bps cut, so there is still space before the BCRP real rate reaches the 2.0% neutral rate. What’s more, given the 2.4% inflation level currently, together with the magnitude of the drop in April, it is quite likely that inflation expectations for May will fall even further, giving the BCRP even greater room to reduce rates. All in all, it’s hard to envision the BCRP at its May 9th meeting ignoring so much data pointing in the direction of a lower reference rate.

Note that headline inflation fell more than core inflation in April. Food prices fell 0.9%, whereas other prices were more stable. It’s tempting to see this as an early indication that the impact of low agriculture output (due to last year’s El Niño weather event) on agriculture prices was waning, but this is not quite the case yet. The prices that declined in April were related to the disappearance of El Niño, but due to a sharp drop in fish and poultry prices, not agricultural prices. The impact of a return to normal agricultural output on prices is yet to come.

On May 15th, March GDP figures will be released. Three figures have already been released, however: mining, oil & gas, and fishing. Mining GDP rose 4.0% YoY. Although this was robust, it was still below what we were expecting stronger growth. Oil & gas fell 5.3% YoY, and fishing was down 32%. All three figures disappointed. All three disappointments suggest that our aggregate GDP growth forecast of 0.6% YoY for March will not be attained.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.