- Colombia: Inflation continued slowing down, and food prices and utilities are starting to reflect the impact of the El Niño phenomenon

COLOMBIA: INFLATION CONTINUED SLOWING DOWN, AND FOOD PRICES AND UTILITIES ARE STARTING TO REFLECT THE IMPACT OF THE EL NIÑO PHENOMENON

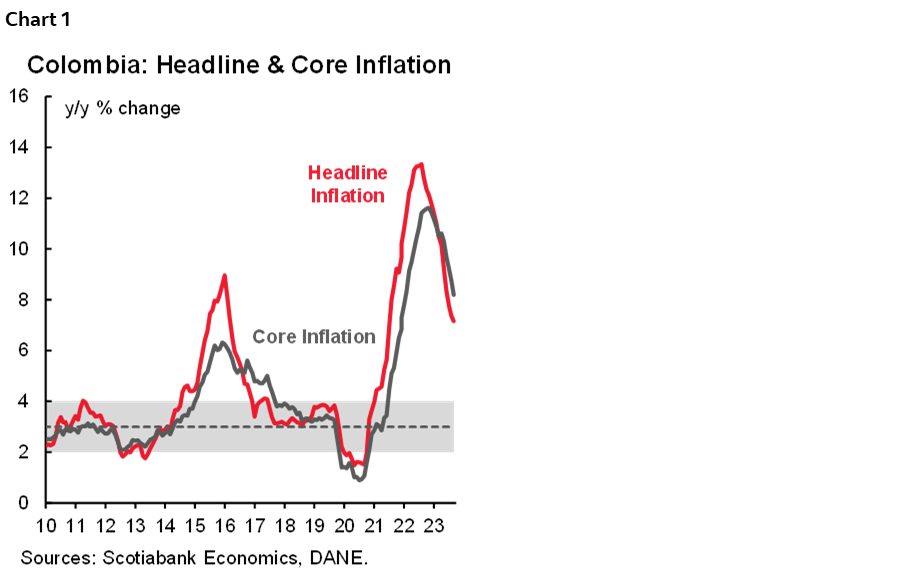

Monthly CPI inflation in Colombia stood at 0.59 % m/m in April, according to DANE data released on Wednesday, May 8th. The result was close to economists’ expectations of 0.57% m/m, according to BanRep’s survey, and aligned with Scotiabank Colpatria’s expectation. Annual headline inflation went down from 7.36% to 7.16%, the lowest level since January 2022 (chart 1), and showed a slower progress compared with Q1-2024. Core inflation (ex-food) decreased from 8.76% y/y in March 2024 to 8.19% y/y in April, while inflation excluding food and energy went down by 40bps to 6.36% y/y. Inflation progress is expected to be more moderate in forthcoming months since the statistical base effect already passed in Q1-2024; our projection for the year-end is around 5.5%.

Headline inflation has decreased by 618bps since its peak, while ex-food inflation has decreased by 322bps. The latest BanRep minutes mentioned that the board is monitoring progress in ex-ante real rate, which suggest that the main focus is on inflation expectation. Having said that, as yesterday’s data didn’t provide a significant surprise we don’t expect a material change on expectation; thus we expect BanRep will continue with cautious steps in the easing cycle, reducing the rate by 50bps at the June 28th meeting. The next most relevant milestone will be next week with the GDP data, which probably will be supportive of BanRep’s cautious approach.

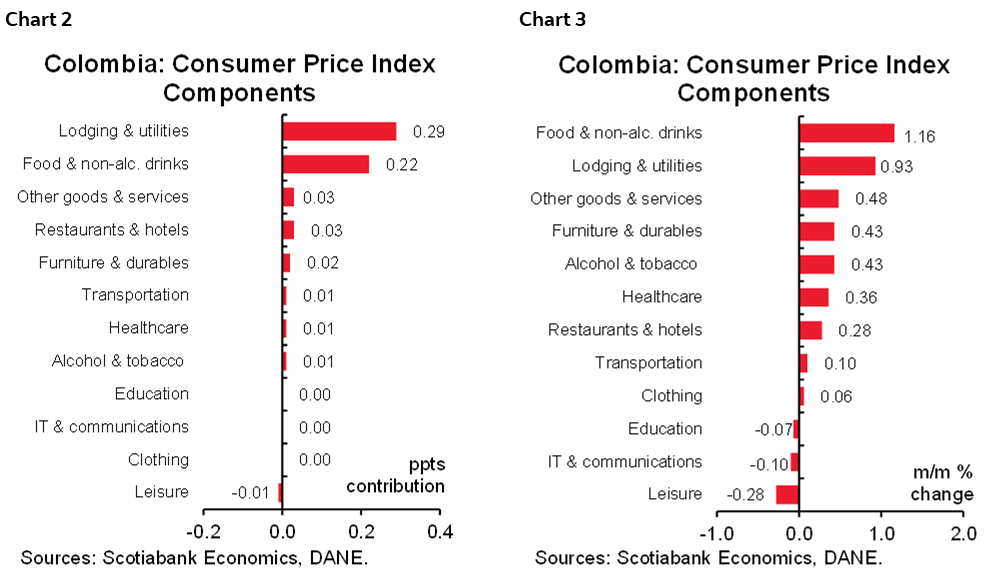

During April, two groups accounted for 86% of monthly inflation (charts 2 and 3). The lodging and utilities group is once again the main contributor, with a monthly inflation of 0.93% m/m and 29bps of contribution due to accelerating rent fee indexation. The increase in utility prices was impulsed by electricity, which, in our opinion, is reflecting the impact of the “El Niño” weather phenomenon. The second main contributor was the food group, which also accelerated, showing monthly inflation above 1% due to the impact of lower agriculture supply on prices; this is also something related to the dry weather in most of the country.

In annual terms, all groups, except for the food group, contributed to the disinflationary trend. The most significant contributor to this trend was gasoline, with its price now stabilizing after significant increases a year ago. This stability has been a key factor in the overall disinflation. However, in the case of food, the high statistical base effects that were once a tailwind are no longer in play, leading to an acceleration in April as we now replace the low statistical base effects.

The mixed picture between goods and services inflation continues. Goods-related inflation decreased from 3.08% to 2.35%, below the inflation target, but explained mainly by the disinflation of tradable goods. In the case of services, the picture is still challenging, the inflation decreased from 8.28% to 8.01%, still well above the target for the central bank but affected mainly by the indexation in key prices such as rent fees.

All in all, today’s results would not be enough to convince the cautious side of BanRep’s board. Instead, we think they will continue the easing cycle at a 50bps pace with a split vote, like in the previous couple of meetings.

Complementary highlights:

- Lodging and Utilities group contributed 29bps to the headline inflation. Rent fees accelerated in April, demonstrating that indexation is strengthening, and it could be related to supply issues amid the huge deceleration in housing construction. In the case of utility fees, this month’s electricity leads to price increases. It could be related to the impact of the “El Niño” phenomenon since now electricity generation is split between hydro and thermoelectric sources.

- Food inflation was 1.16% m/m, contributing 22bps. Monthly food inflation has accelerated, and the lack of supply due to the dry season is impacting key prices. Fresh fruits are still leading the prices increases (+5.73% m/m, +4bps contribution), followed by potatoes (+9.50% m/m), bananas (+6.48 % m/m), and vegetables and legumes (+1.98% m/m). In annual terms, the tailwind from high statistical base effects vanished. In May and June, it could become a headwind since we will release a significant negative number (0.85% m/m and -0.53% m/m), respectively. In any case, we don’t expect food inflation increases to offset the progress in other sectors; it will just slow down the headline inflation reduction.

- The rest of the groups exhibited moderate variations. On the transport side, gasoline prices were broadly stable; the uncertainty here is around diesel prices. However, the central bank has said that the potential impact of diesel prices is less aggressive compared to gasoline. In the case of restaurants, we highlight that despite increasing food prices, restaurant inflation remained low (0.29% m/m), suggesting a weak demand. Additionally, groups related to imported items such as vehicles and home appliances, among others such as clothes, are still showing negative inflation, which is a result of the FX appreciation but also of the weak domestic demand.

—Sergio Olarte, Jackeline Piraján & Daniela Silva

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.