- Stronger-than-expected growth led to better fiscal outcomes in 2021, with the deficit and debt-to-GDP ratio lower.

- The improved fiscal performance implies that financing needs in 2022 will be lower than previously estimated.

STRONGER ECONOMY IMPROVES FISCAL RESULTS AND OUTLOOK

On Friday, February 4, the Ministry of Finance (MoF) released the 2022 Financing Plan and preliminary fiscal results for 2021. Stronger economic activity led to improved fiscal results in 2021 that, if sustained, would put finances ahead of key 2022 milestones. Debt stabilization and lower financing needs in 2022 are the main takeaways of the publication. In our view, the macro assumptions in the plan are realistic and reflect a commitment to fiscal sustainability.

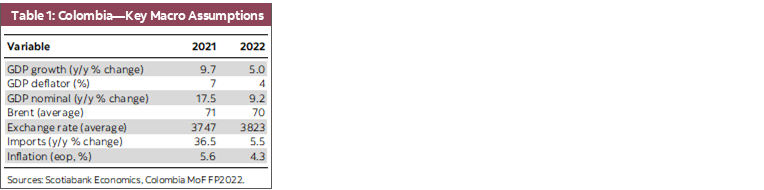

MACRO ASSUMPTIONS

- The government expects GDP growth to close 2021 at 9.7%, well above the 6.0% estimate in the 2021 MTFF, which contributed to higher tax collections of COP 11 tn (~1% of GDP).

- Economic growth of 5.0% (table 1) is expected for 2022, which is slightly above the market consensus (4.50%). This projection is achievable if Colombia continues towards the “new normal,” with the MoF expecting a rebound in the services sector and manufacturing. On the demand side, the MoF projects higher investment, which would offset the expected deacceleration in consumption, resulting in a higher external deficit.

In terms of risks to the outlook, the MoF said that higher-than-expected inflation, long-lasting effects from the bottlenecks in mining and construction, and restrictions due to the pandemic would have negative effects on economic growth. On the positive side, higher oil production and a more robust labour market recovery would boost growth.

- Regarding other key variables, the MoF expects a conservative average in oil prices and a depreciation in the average USDCOP. Inflation is expected to close 2022 at 4.3%, the same projection as the central bank.

2021 FISCAL RESULTS

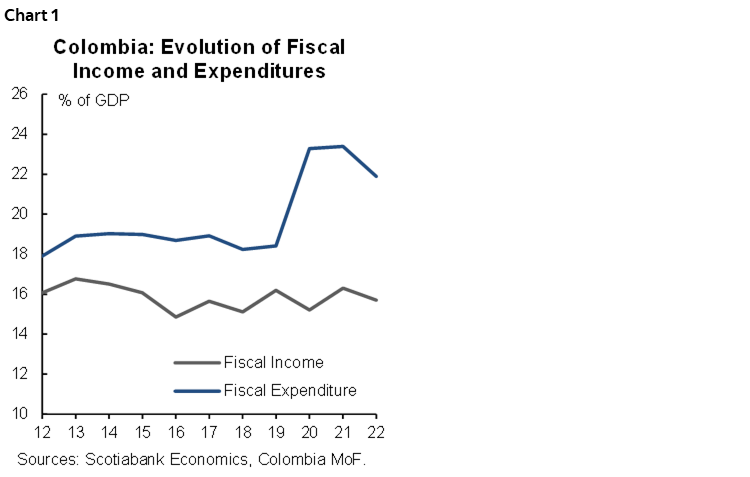

As a result of stronger-than-expected economic growth, tax collections in 2011 were better than expected by COP 11.1 tn (1% of GDP), especially import tariffs which contributed 60% of the overall increase (table 2). At the same time, there was an under execution of fiscal expenditures of COP 2.7 tn (0.2% of GDP) in 2021 (chart 1). Higher tax revenues and lower expenditures led to an estimated improvement of 1.5% of GDP in total and primary fiscal deficits, which would imply a total deficit for 2021 of 7.1% of GDP (well below the forecast of 8.6% of GDP made a year ago).

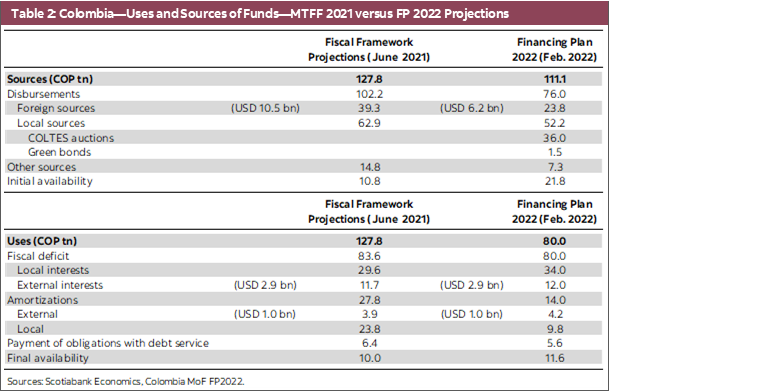

Stronger fiscal performance resulted in a higher cash buffer at end-2021, which stood at COP 21.8 tn (2.1% of GDP), well above the estimate made at the beginning of the year of COP 10.8 tn (1% of GDP). Accordingly, the MoF starts 2022 with a strong cash position that will be reflected in lower financing needs.

2022 FINANCING PLAN

The MoF’s main assumption is that continued healthy economic growth in 2022 will be translated into solid tax revenue. In fact, for 2022, tax collections are estimated at 15.7% of GDP, close to the pre-pandemic average (15.6% of GDP). On the other side of the income statement, expenditures were estimated at 21.9% of GDP, still well above of pre-pandemic average of 18.6% of GDP, but lower than those observed in the worst of the pandemic (23.4% of GDP in 2020 and 2021). All in all, the expected fiscal deficit for 2022 was revised from 7.0% of GDP to 6.2% of GDP, which in our opinion is an even stronger positive effect than the 2021 fiscal deficit reduction.

The improvement in 2022 is not the result of expected one-off transactions, which is a positive change from previous fiscal projections.

Our take is that the above-the-line projections are positive. The government is making realistic assumptions regarding economic growth and tax collections, close to the pre-pandemic average. However, expenditures remain high as a percentage of the GDP and, depending on the recovery, we would expect an under execution on spending and a potential new surprise by the end of 2022.

Positive news on tax collections translated in higher cash buffers, but, more important, is also reflected in lower financing needs. This will contribute to moderate negative supply effects along the COLTES curve in 2022.

Total financing needs represent 8.6% of GDP (COP 111.15 tn), well below the 2021 level of 11.2% and close to the pre-pandemic level (8% of GDP). Issuances are lower-than-expected in the MTFF-2021. Domestic sources of funds will be COP 10.7 tn lower, while foreign sources will be COP 15.6 tn lower, and short-term operations will be COP 5.3 tn lower.

The main source of financing is local debt issues (71%), while 19% is expected to come from external sources, a different composition from that observed in 2021 (61% in local sources).

External sources are expected to cover USD 6.22 bn of total financing needs (below the projection in the MTFF-2021 of USD 10.5 bn), with the MoF expecting half coming from bonds and half through the multilateral institutions. This implies that in 2022 the MoF will reduce its sales of dollar liquidity.

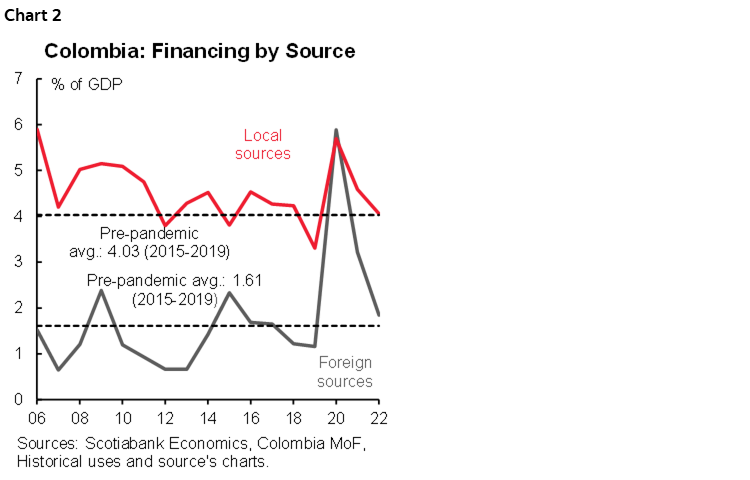

Local sources account for COP 52.23 tn (4.1% of GDP), slightly above the pre-pandemic of 3.77% of GDP in 2019 (chart 2). Auctions are expected to raise COP 36 tn, with COP 1.5 tn of additional issuance in green bonds. COP 14 tn will be through direct issuance with public institutions, though part of that will be allocated to create the public debt fund, about which detailed information is to be provided in the near future.

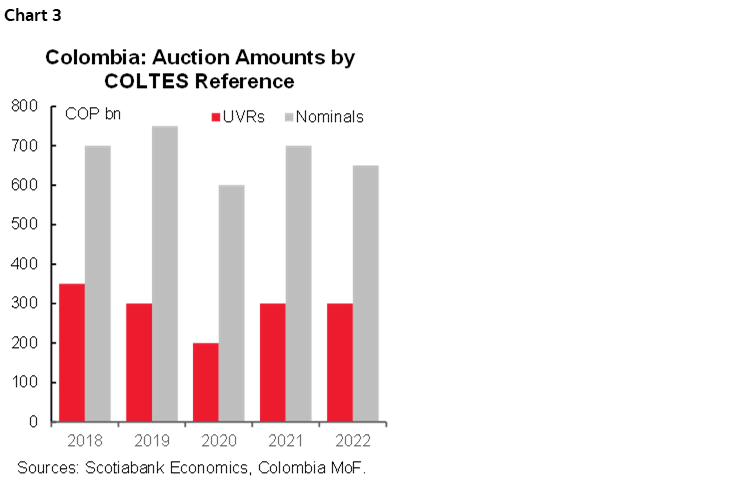

The MoF will issue around COP 300 bn in UVRs and COP 650 bn in nominals in local markets on a biweekly basis. Nominals auction are set to moderate, while UVRs auctions will remain at 2021 levels (chart 3).

Our take is positive, as the MoF is mobilizing higher tax collection to reduce financing pressures. Additionally, FP-2022 conveys a strong message of fiscal responsibility, consistent with reduced supply pressures in the yield curve ahead of the Fed’s hiking cycle.

DEBT DYNAMICS AND THE SOVEREIGN CREDIT RATING

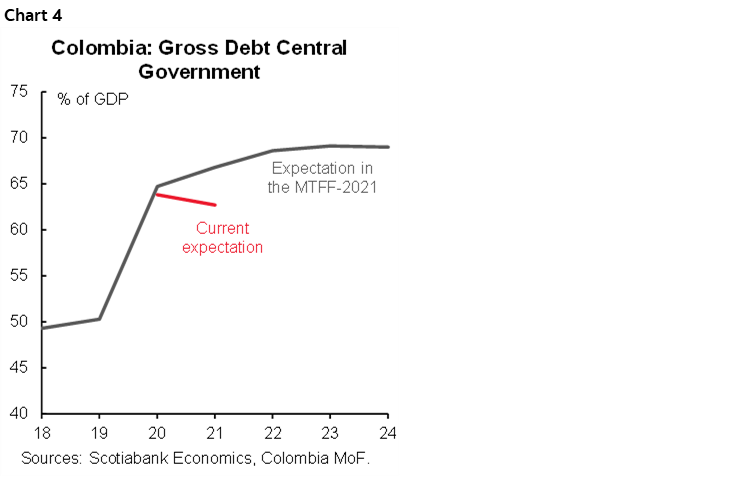

The gross debt-to-GDP ratio for the Central Government is projected to decrease from 63.8% of GDP in 2021 to 62.7% of GDP in 2022, reaching the debt target for 2032 earlier than expected (chart 4). In terms of net debt, the level will decrease from 60.9% of GDP to 60.5% of GDP.

All in all, the Financial Plan came with strong positive news. Results for 2021 were better-than-expected and the macro base case scenario assumptions ahead of 2022 are realistic. The positive outcomes are reflected in lower financing pressures, which still entail high expenditure needs. Our overall take of the 2022 plan is positive and it is likely to be viewed as such by the credit rating agencies. However, it is too early to anticipate an upgrade in the sovereign credit rating by Fitch and S&P.

That said, the fiscal front probably won’t be the main issue for Colombia in 2022. The bad news is that previous positive fiscal takes have been offset by uncertainty regarding the monetary policy locally and abroad, and by political uncertainty regarding presidential elections.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.