- Recent speeches by central bankers have reviewed the lessons learned in dealing with inflation. Most important is the risk of easing restrictive stances in response to early signs of lower inflation, which can lead to a higher cost in terms of output and unemployment.

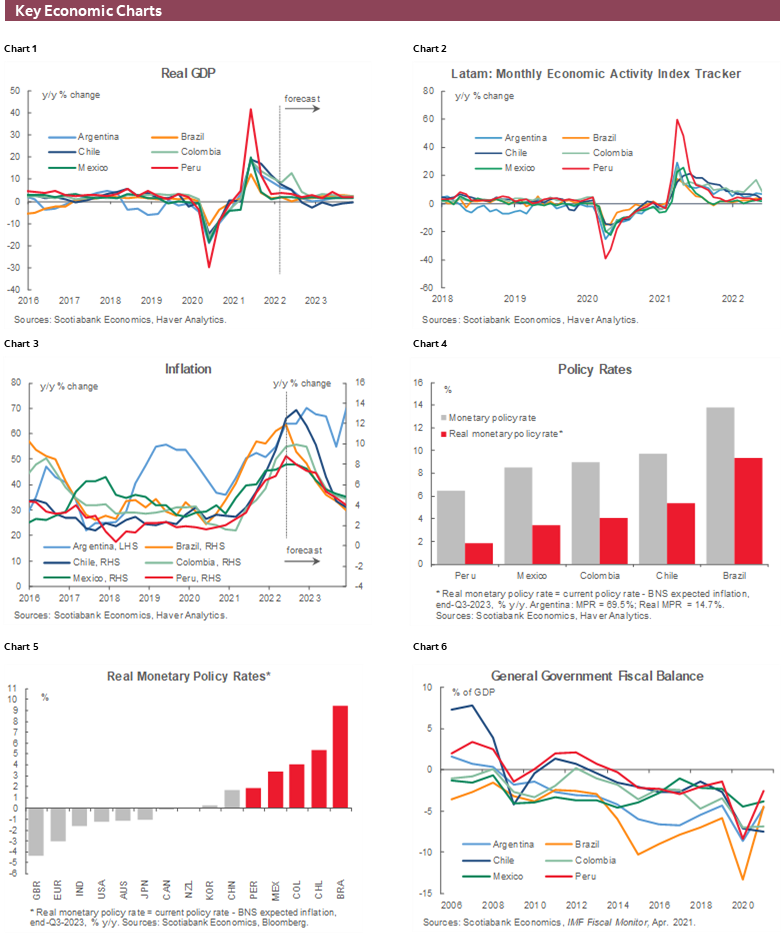

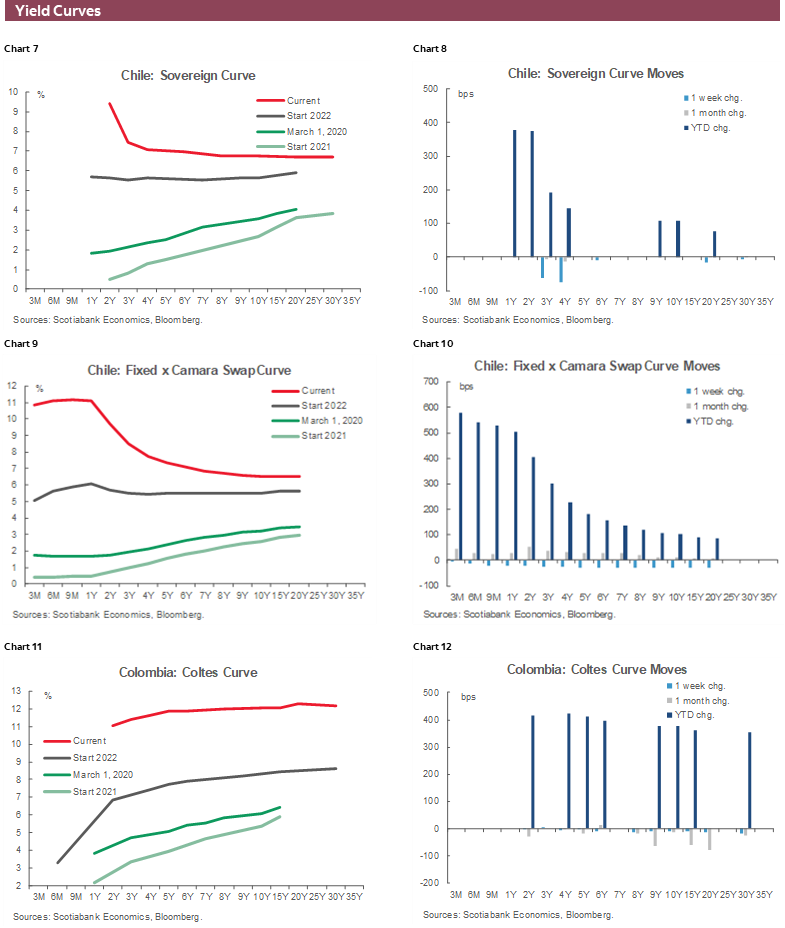

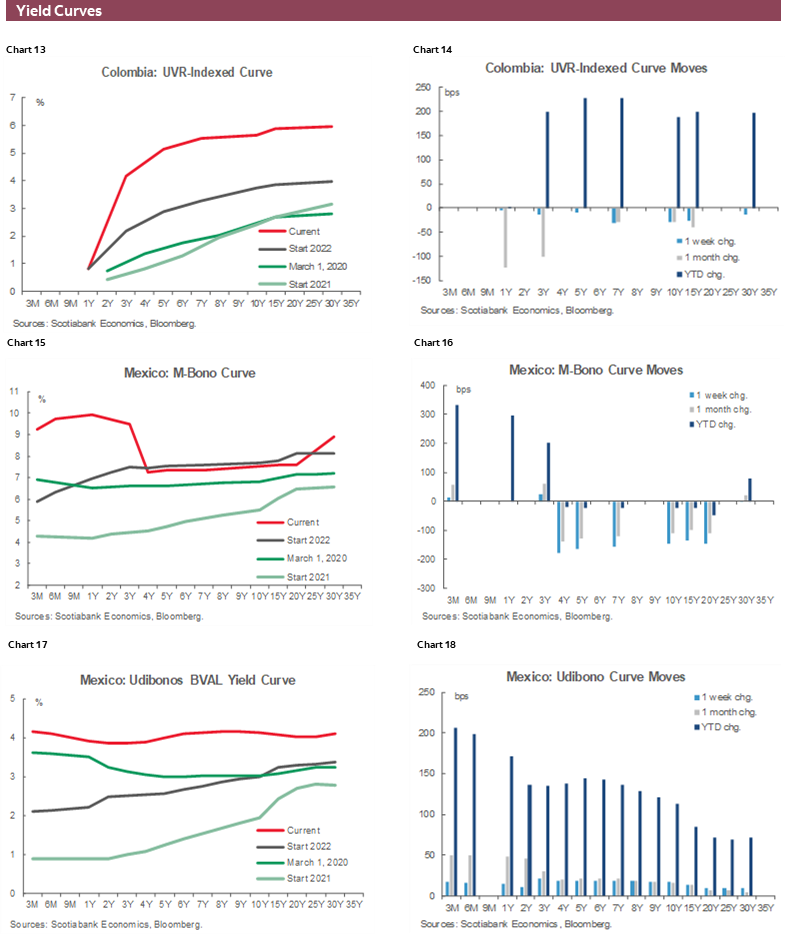

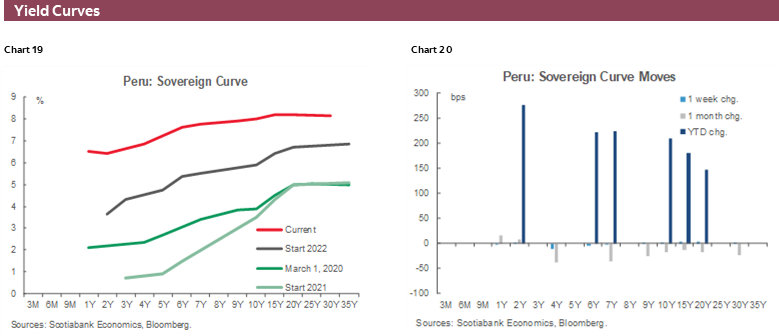

- Most Latam central bankers appear to have heeded this lesson, raising real (inflation-adjusted) policy rates to contain inflationary pressures, thereby anchoring longer-term inflation expectations and reducing one source of uncertainty for local financial markets.

In the Northern Hemisphere, the start of September marks the end of summer holidays and the return to school. At the recent annual Jackson Hole conference of central bankers, Fed chair, Jerome Powell, adopted a professorial tone, lecturing on the lessons learned from past inflationary episodes. His message: central banks that temporize with inflation, relaxing their restrictive stance at the first signs of abating pressures, ultimately pay a higher price in terms of inflation-output trade-offs. Other central bankers, notably from the ECB, followed Powell's lesson plan.

Central bankers' schooling of markets in the dangers of relaxing vigilance in the fight against inflation should disabuse those anticipating early rate cuts on lower inflation numbers. The Fed and other central banks are now clearly concerned that expectations of higher inflation are at risk of becoming embedded in decision-making. If that scenario were to unfold, the costs of bringing inflation down, measured in terms of output losses and higher unemployment, would increase. And that is what Powell and his colleagues want to avoid.

There are two corollaries to this thesis. The first is that nobody should expect cuts to monetary policy rates anytime soon. Central banks will not ease until price pressures have been purged from the economy and inflation expectations firmly returned to target on a durable basis. The second corollary is that recession risks have likely increased, albeit more so for Europe, which is faced with severe supply side shocks from higher energy prices. In that event, however, negative output gaps should accelerate the moderation of inflation expectations, bringing forward a shift in the stance of monetary policy.

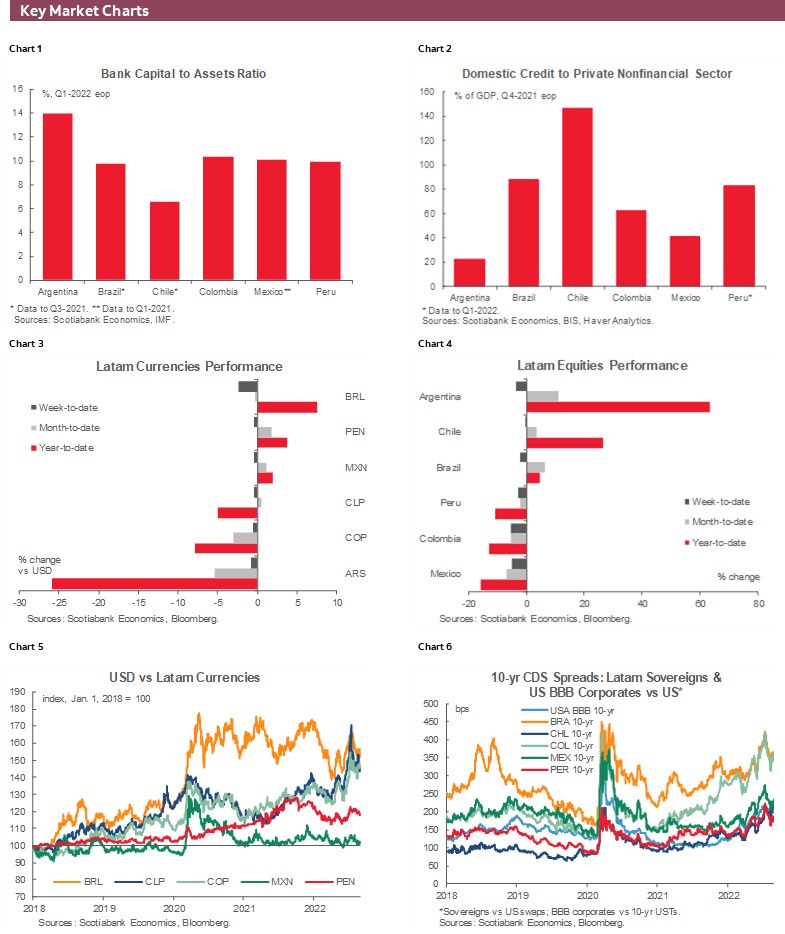

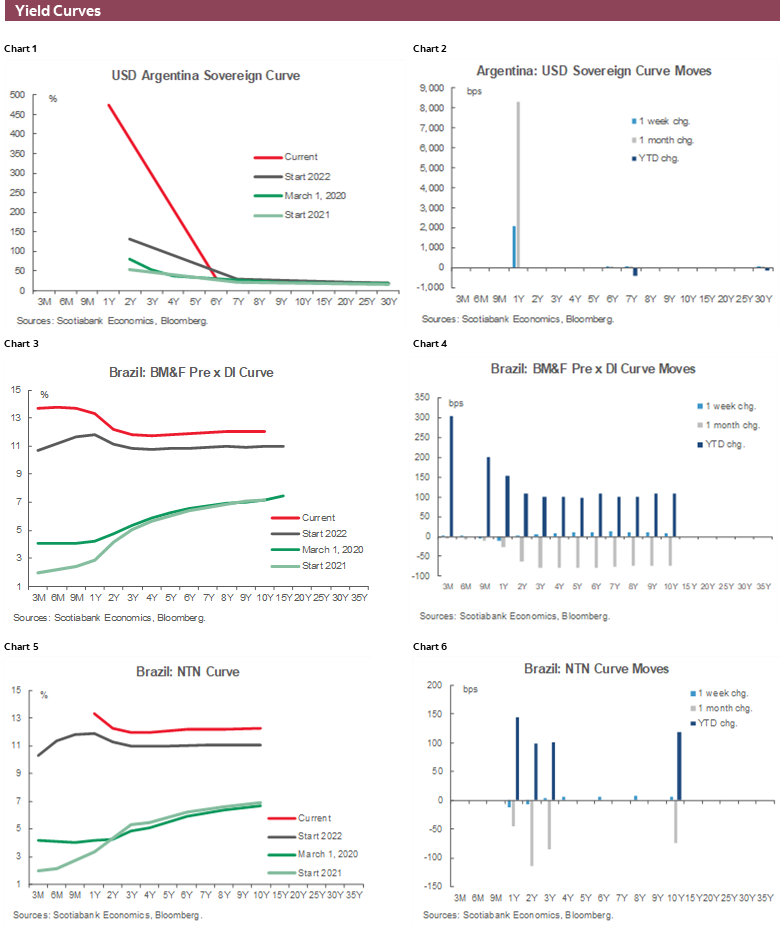

Both of these effects have been priced into markets in recent days, with equity prices selling off sharply. And for the Latam region, global financial conditions remain challenging. Nevertheless, with the US dollar appreciating against most currencies around the globe, stoking inflationary pressures through exchange rate pass-through effects, several of the region's currencies have held their own. (Argentina's peso, in contrast, has depreciated sharply, reflecting the pervasive uncertainty there with respect to macroeconomic policy management and the risk of financial instability.)

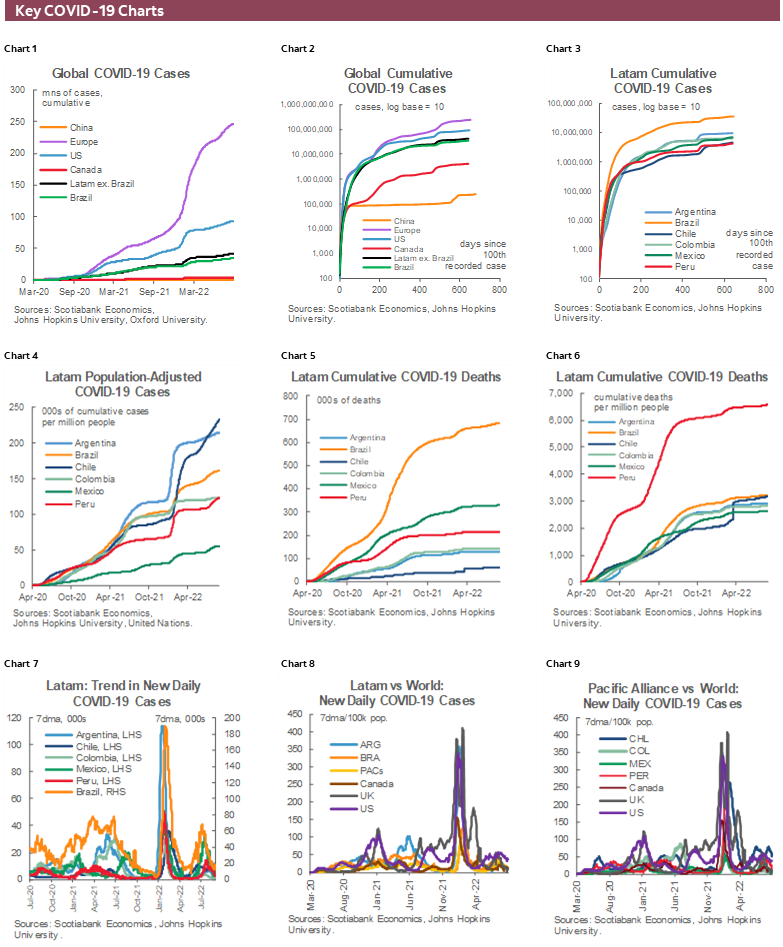

For the most part, despite recent financial turbulence, economic recoveries in the region remain on track as growth adjusts from the post-pandemic rebound to more sustainable longer-term rates. This process could be uneven, and Scotiabank's experts in Santiago point out that the Chilean economy is likely to contract over the next several quarters. Continued growth, meanwhile, would sustain job creation, which has begun to flag, and close remaining gaps with pre-pandemic employment levels.

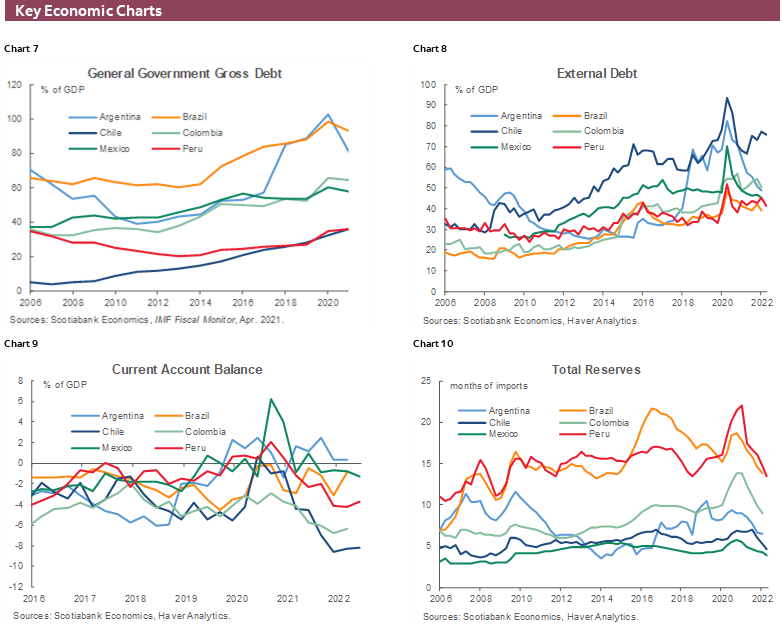

Slower growth should relieve some price pressures where unsustainably strong consumer demand has exacerbated supply-side shocks. Scotiabank's Latam economists anticipate inflation will decline over time, with inflation-targeting central banks in the region focused on returning inflation to target ranges over the medium term. Central banks across the region now lead their global peers in terms of raising their real, or inflation-adjusted, policy rates. At the same time, the transition to more sustainable levels of consumer demand would also help reduce large current account deficits, notably in Chile and Colombia.

Longer-term inflation anchored by credible, independent central banks reduces one source of uncertainty for financial markets and supports growth and asset valuations. That said, in the current conjuncture, considerable uncertainty remains, including that coming from the political sphere. Markets will continue to closely watch the new presidential administration in Colombia, which has thus far adopted a cautious and conciliatory approach. And there are also encouraging signs that Peru's new Finance Minister is seeking to impose some order on what has been a chaotic policy-making environment. In addition, the results of Chile's plebiscite on the draft new constitution Sunday, which recent polls suggest will be rejected, could likewise be a source of political uncertainty depending on how the government responds. As our team in Santiago point out , while the prospect of rejection has boosted local asset valuations, the durability of those gains may depend on the government laying out a clear roadmap on next steps and how to address outstanding contentious issues.

The key lesson from all this is that, while governments may be unable to control or prevent external shocks, they should do their homework to ensure that their economies are insulated from them. And while it is too early to give Latam governments a final grade on their performance in the current cycle, it would appear that most have absorbed that lesson from their own past experiences with high inflation.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.