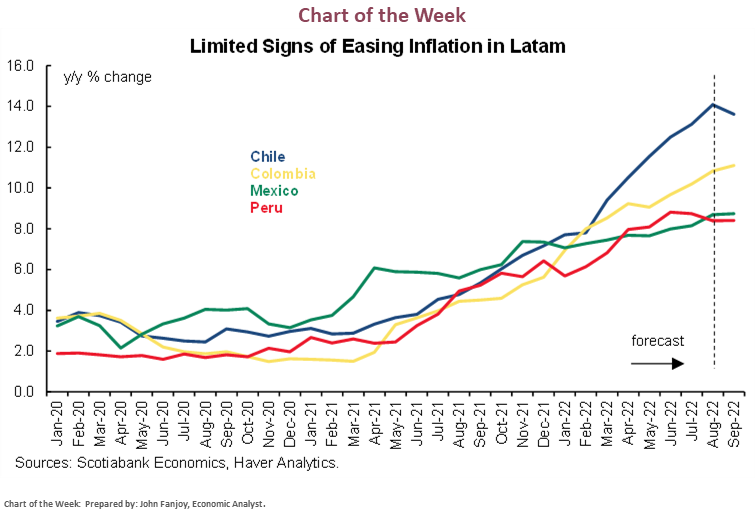

- Pacific Alliance countries publish inflation figures for September next week. In Colombia, our economists anticipate a further pickup in year-in-year inflation compared to relatively flat readings out of Mexico and Peru and a slight deceleration in Chile.

- Peru’s BCRP is expected to hike by 25bps next Thursday as it nears the end of its hiking cycle, a view supported by Chairman Velarde in recent comments.

- Mexico’s AMLO will announce additional measures as part of his anti-inflation plan on Monday but we expect limited impact on core prices.

- Lula’s lead over Bolsonaro widens in polls ahead of Sunday’s elections, but a second-round showdown in late-October remains the most likely scenario.

Pacific Alliance countries will publish September inflation data this week, with key implications for policymakers in the region that are looking (or hoping) to bring their hiking cycles to an end soon (see chart below).

In Colombia, our economists expect an increase in headline inflation to 11%+, supporting BanRep’s aggressive pace of rate increases. The projected 11.16% y/y gain (vs. 10.84% last month) follows from elevated food prices as well as continuously elevated input prices and the tailwind of higher education-related prices. Core inflation is forecast to climb by a similar margin (see Colombia section below).

Mexican inflation is showing no clear signs of decelerating, with H1-Sep CPI data showing only a marginal decline in headline prices growth. Our Mexico City team sees gains in both headline and core readings (see Mexico section below), while lingering price pressures should result in upward revisions to economists’ forecasts in the upcoming Banxico survey. AMLO’s anti-inflation plan, with supplementary measures to be announced on Monday, has had limited impact on the core goods basket.

As for Peruvian inflation, our economists anticipate a roughly unchanged pace of annual prices growth in September while in Chile they see a slight deceleration from 14%+.

Brazilians take to the polls on Sunday for the first-round presidential election, with Lula leading Bolsonaro by double-digits in recent polls. The former president will likely fall short of an outright majority, however. Votes will also be cast for congress, and state governorships and assemblies, among others. Though he may not claim a majority of votes this weekend, Lula is heavily favoured in a runoff election in about a month’s time. Markets have adjusted to highly-defined odds of a Lula victory (whether it’s in the first- or second-round), so near-term gains in Brazilian assets may be limited—if only thanks to political clarity—with domestic developments ceding greater influence to the global market mood.

—Juan Manuel Herrera

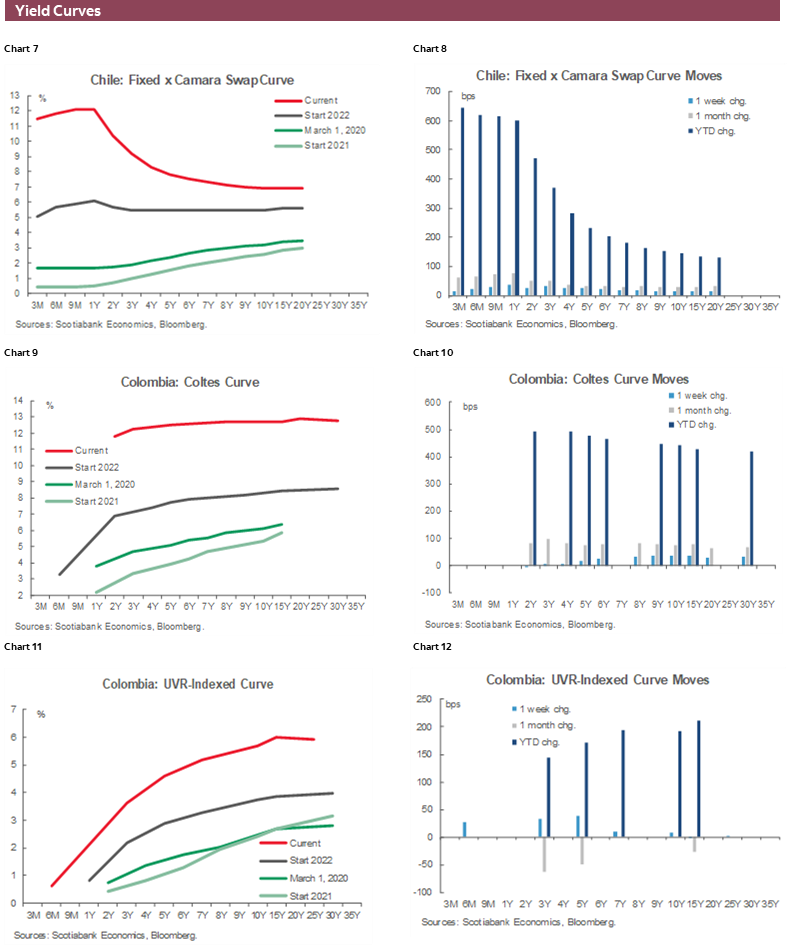

CHILE: FISCAL CONSOLIDATION IN PROCESS, MINOR SLOWDOWN IN INFLATION

Modest expansion in the public spending next year. The Government sent the Fiscal Budget bill to Congress, who will have 60 days to discuss and approve the initiative. As expected, fiscal spending will grow at a moderate pace; while the public debt will increase by USD12bn in 2023 (see our Latam Insights).

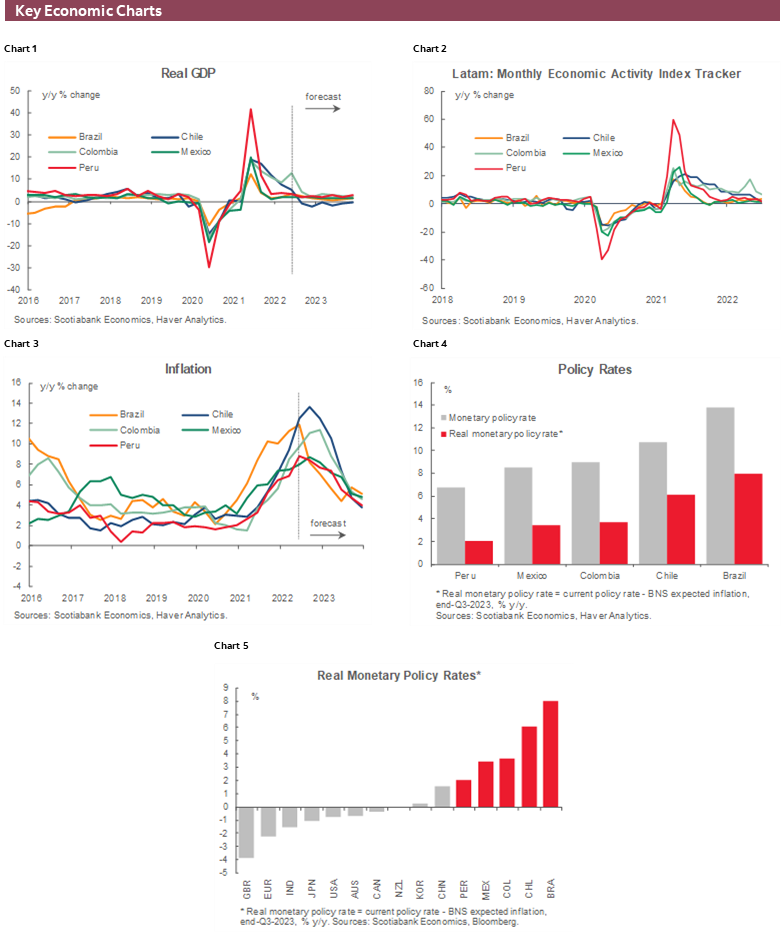

Economic activity is projected to have decreased 1.8% y/y in August (-0.7% m/m). On Monday, October 3, the Central Bank will release August economic activity (Imacec) data, for which we forecast a new drop in y/y terms. With respect to the previous month, we expect a 0.7% contraction (seasonally adjusted), mainly due to a decrease in non-mining GDP. Taking into account the above, we maintain our projection of 2.1% GDP growth for 2022 and a 0.9% contraction for 2023.

The statistical agency (INE) will publish September CPI figures on Friday, October 7. We forecast September inflation at 0.9% m/m, below market expectations at 1% m/m, mainly due to decreases in prices for air transportation and tourist packages. Overall, the main drivers behind inflation in September will be food and transportation. In the case of food, we estimate increases in meats, vegetables and non-perishables. Transportation prices gains are explained by rises in gasolines, new cars and interurban bus fares. Within this division, we anticipate a relevant drop in air transportation fares. Overall, we estimate a large number of items with monthly increases within the basket (inflationary diffusion), representing around 69% of the basket (August: 69%). With this, annual inflation would show a deceleration from 14.1% in August to 13.8% in September.

—Aníbal Alarcón

COLOMBIA: INFLATION TO REMAIN ON UPWARD TREND

We expect prices to remain on an uptrend in September CPI data due on Wednesday, with particular strength in food prices, as inflation continues to reflect higher input prices. Education-related prices should act as an additional tailwind to inflation. Our forecast calls for an 11.16% y/y increase in headline CPI from 10.84% y/y in August with a similar acceleration in core inflation to 8.06% y/y (from 7.83%). However, the market is more skewed to the upside (expectation of +0.75% m/m and 11.24% y/y).

In data for August, we expect industrial production to continue to show some deceleration due to persistent pressures in the prices of inputs and raw materials. Retail sales are expected to continue with a trend of moderation due to the effects of inflation that have limited household disposable income. This is in addition to the fact that in the reference month there are no events that can cause an upward bias.

—Sergio Olarte, María (Tatiana) Mejía & Jackeline Piraján

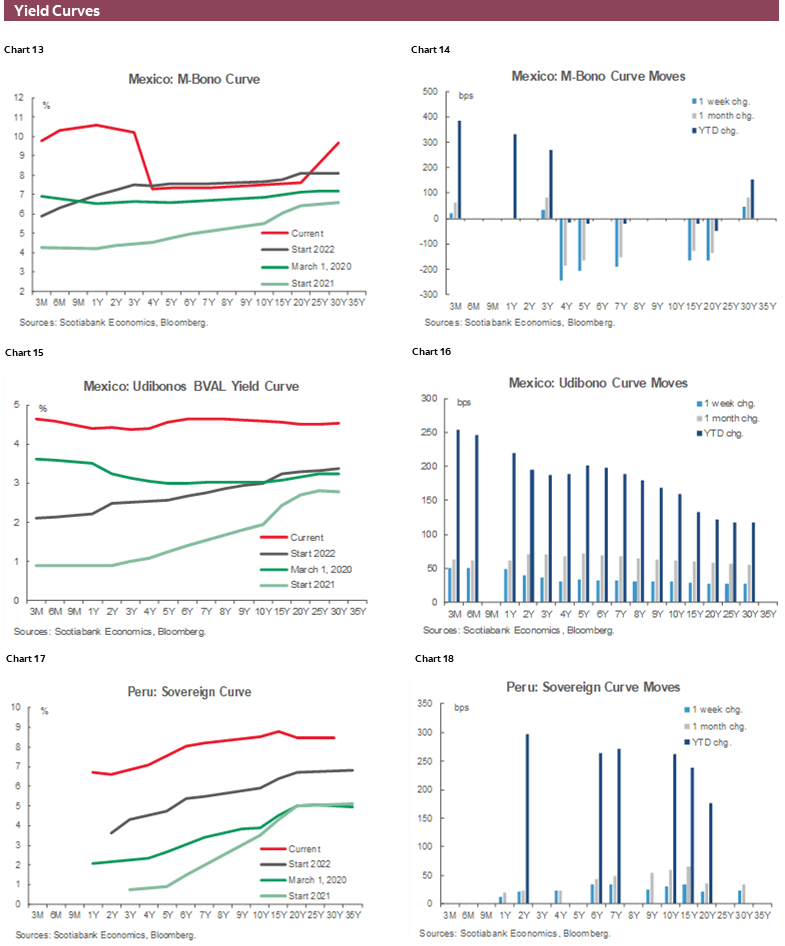

MEXICO: INFLATION CLIMB MAY HAVE CONTINUED IN SEPTEMBER, AS COULD YEAR-END EXPECTATIONS

Unlike in the US and Canada, we see no signs of Mexican headline inflation decelerating in September. In fact, in the first fortnight of the month, inflation again exceeded expectations, showing only a marginal break in its upward trajectory (8.76% vs 8.77% previous and 8.71% consensus). In the Citibanamex survey, analysts expect a 0.63% m/m CPI increase in September, which would translate to 8.71% y/y or practically no change from the 8.70% print from August. In turn, core inflation remains in an upward trajectory; as in the first half of September it rose from 8.13% to 8.27%, with no expectation of cooling over the totality of the month.

With this in mind, we consider the 8.71% to be slightly skewed to the downside, and our expectation is that both headline and core inflation continued their ascent in September. Banxico’s economists survey for September out on Monday will most likely show upward revisions to inflation and interest rate forecasts. In the August release, participants’ inflation forecasts averaged 8.15% for Dec-2022, while the median Banxico rate projection for year-end stood at 9.50%. Amid the most recent Fed and Banxico hikes, analysts have also likely lifted their policy rate expectations. Next week’s Banxico survey results should see a higher number of respondents expecting an interest rate at least at 10.25% by the end of 2022.

Is also important to highlight that president AMLO will release an update to the anti-inflation plan on Monday, with a focus on items impacting the basic consumption basket, which mostly corresponds to non-core goods (agriculture and energy, which rose 10.65% y/y in August). However, while the plan has resulted in more muted increases in energy prices, it has had practically no impact on the price of other goods—and we wouldn’t expect this to change.

Recently, GDP growth forecasts for 2022 have also been revised higher. In the August Banxico Survey, analysts projected a 1.93% expansion in 2022, followed by 1.31% in 2023—below the 2.0% long term average. However, consumer confidence points to a moderation in spending during the second half of the year. Thus, we expect private consumption to continue to expand at only a modest pace in data for July out on Thursday. As for fixed investment figures out on Thursday as well, we expect no significant monthly advances as construction activity remains depressed well below pre-pandemic levels, yet the year-on-year pace in gross fixed investment will be supported by low-base effects.

—Miguel Saldaña

PERU: PAUSE IN INFLATION DOWNTREND IS LIKELY IN SEPTEMBER. WE CONTINUE TO EXPECT A 25BPS HIKE IN THE REFERENCE RATE NEXT WEEK

The key prices that we are monitoring in September point to a monthly inflation reading of around 0.4% m/m, similar to September 2021. This is in line with the view voiced by BCRP Chairman Julio Velarde that inflation would likely be between 0.4% and 0.5% m/m. If so, 12-month inflation would hold at 8.4%, as it was in August—resulting in a pause in the decelerating trajectory of inflation. This is in line with our inflation forecast of 7.7% for 2022.

In this scenario, the BCRP will likely continue in its normalization of monetary policy. Yesterday, Velarde noted that it’s likely the bank won’t have to raise the key policy rate much more. This suggests that the BCRP is winding down its rate hiking cycle, while it simultaneously continues to consider an increase in the short term.

We expect the BCRP to raise the reference rate at their meeting on Thursday, October 6, likely by 25bps, as they did September, to 7.00%. However, the end of the cycle is near, in line with our baseline scenario. The key variable going forward will continue to be inflation expectations. We believe that there is a good chance that after three months of marginal declines, inflation expectations will stop falling in the very short term, perhaps even at the next reading, for October. Inflation expectations (12-months out) have fallen from 5.3% in July to 5.1% in September, which is not much of a decline. With much of the market (as well as the BCRP) now expecting inflation to decline at a slower pace, this could actually result in a minor rise in inflation expectations, as forecasts for the decline in inflation are stretched over a longer period. The BCRP’s actions in October and November will depend crucially on this variable.

—Mario Guerrero

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.