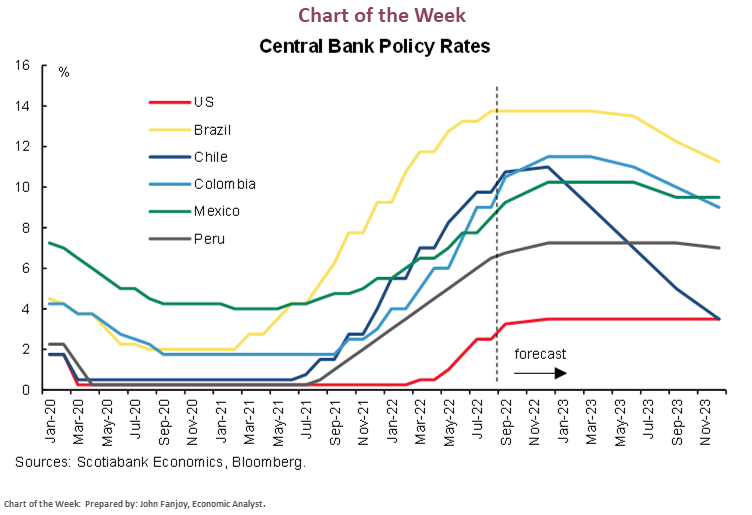

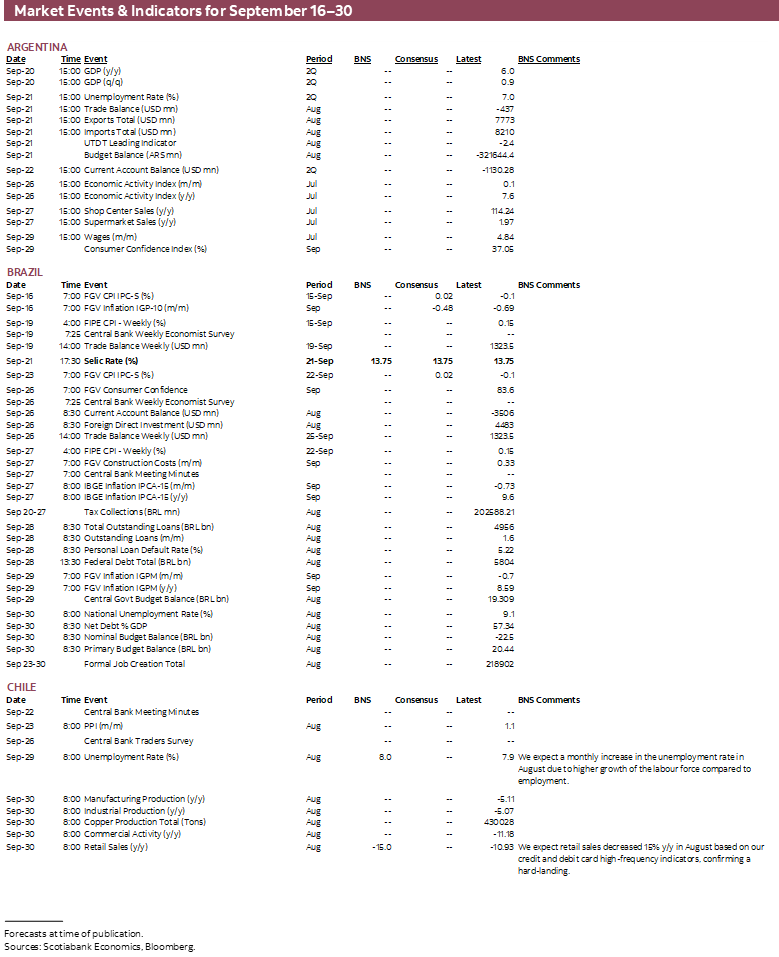

- The Fed’s policy decision next Wednesday will take centre stage, with a hawkish 75bps hike overshadowing a (likely) unchanged Selic rate in Brazil on the same day and projected policy rate reductions in Latam next year.

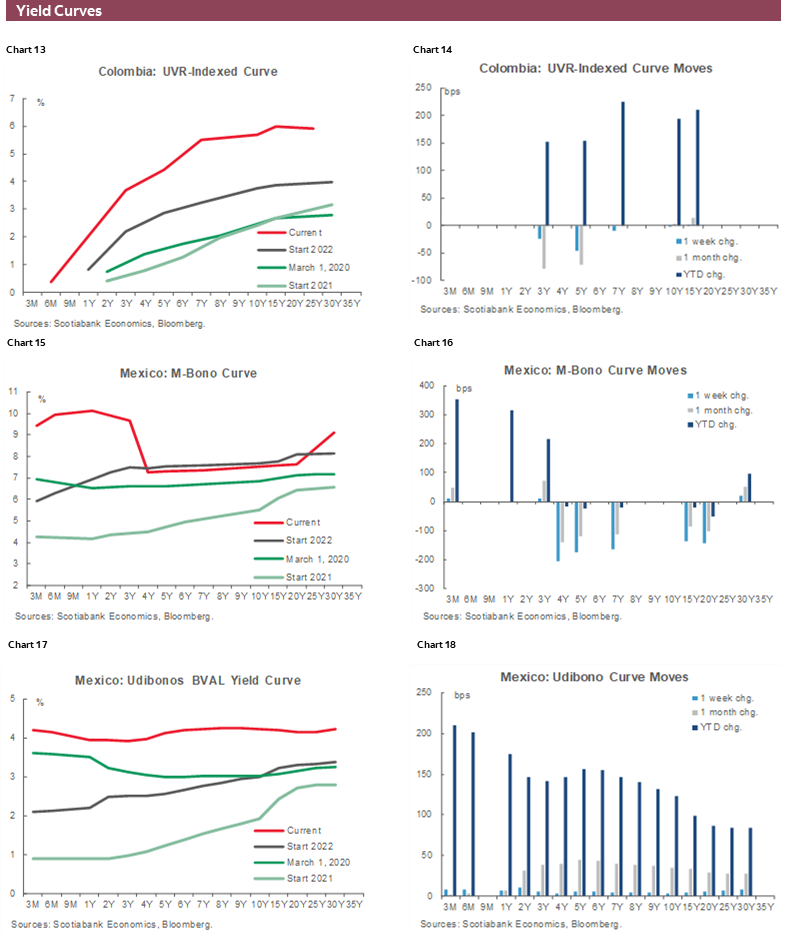

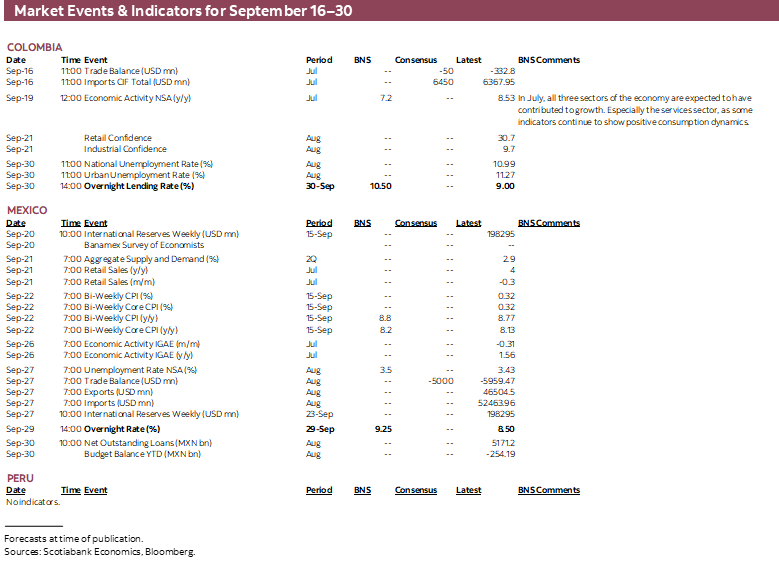

- Mexican H1-Sept CPI data is unlikely to change Banxico’s mind ahead of its late-month meeting, where we forecast a 75bps hike, but it may challenge its expectation that inflation peaked in Q3.

Latam assets took a hit this week amid the sharp risk-off reaction in markets after surprisingly strong US inflation data (core, in particular). The data have prompted some economists to project a giant 100bps hike from the Federal Reserve at its policy decision next Wednesday, while our call remains a (still sizable) 75bps increase accompanied by hawkish guidance.

In the Pacific Alliance, domestic developments could not compete to drive attention away from the data-motivated sell-off, and next week’s regional calendar may again not offer enough to take the spotlight away from the Fed.

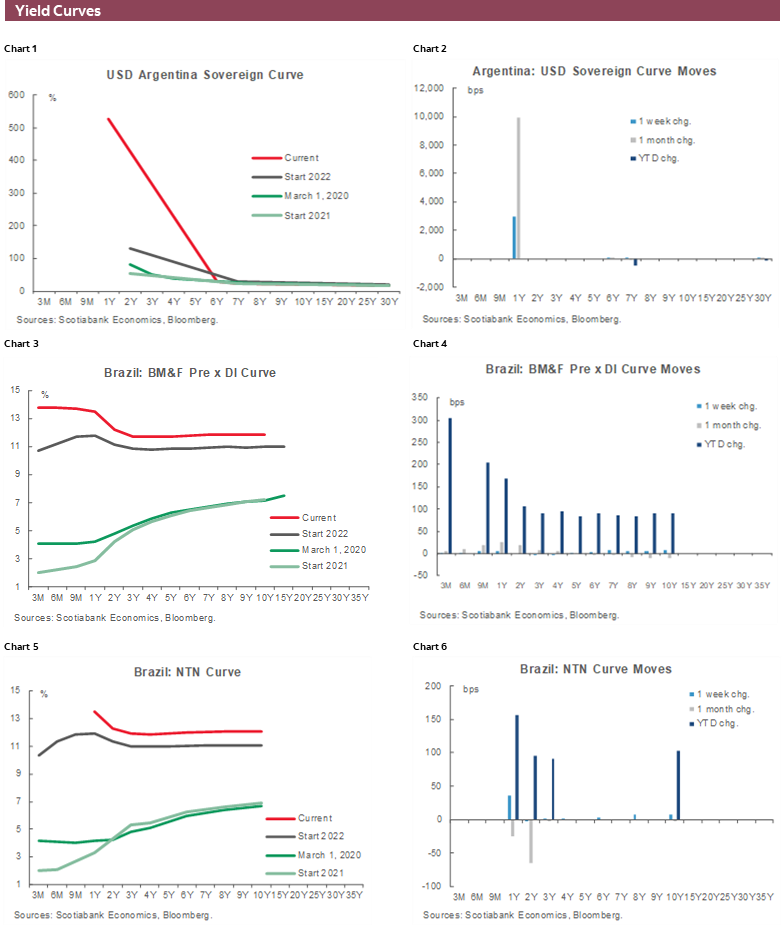

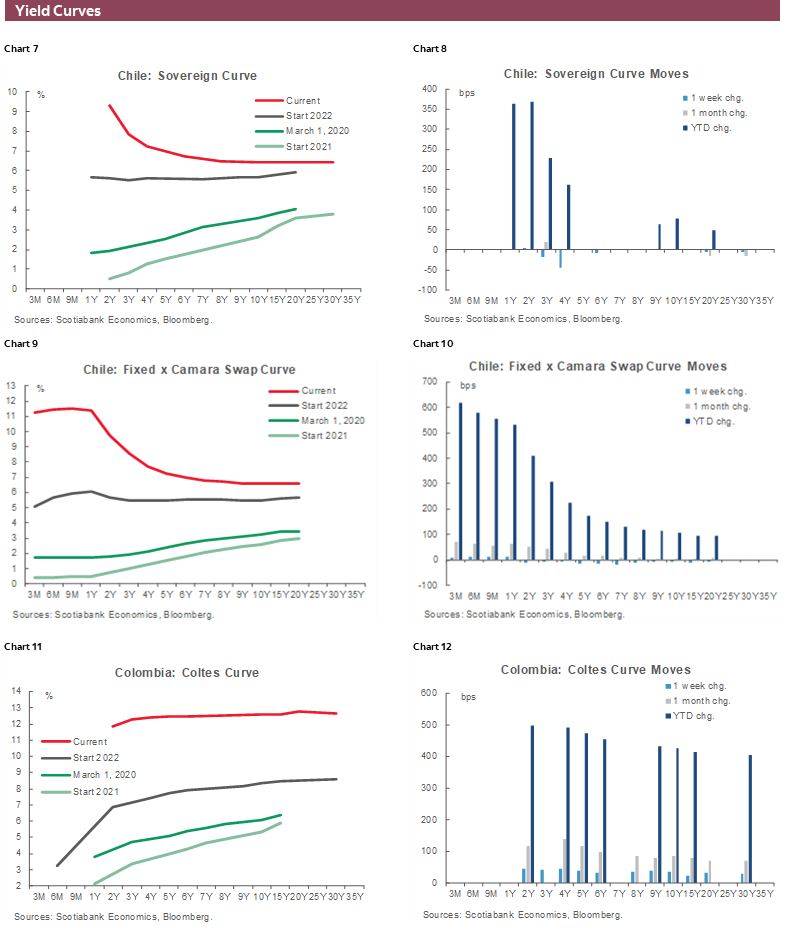

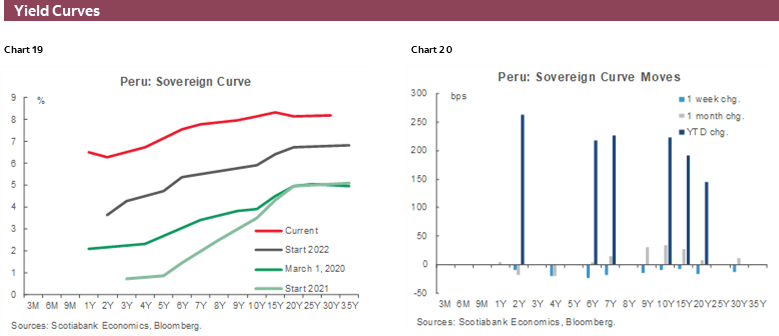

The parallel shift upwards in expectations for Fed rates pulled regional yield curves higher, but nowhere is this clearer than in the case of Mexico, where Banxico has tied its rates policy to moves north of the border. Year-ahead Banxico policy rate expectations have climbed by around 40bps since Friday’s close, roughly equivalent to the increase seen in Fed rate expectations.

Next week’s release of bi-weekly Mexican CPI for H1-Sept is unlikely to result in Banxico deviating from a 75bps increase, our expectation for the September 29 policy announcement. A surprise 100bps increase from the Fed could certainly open the door for renewed hawkishness in Banxico’s stance, more than a stronger than expected bi-weekly inflation print could. Having said that, September’s CPI data will challenge Banxico’s latest inflation projections where it sees headline and underlying inflation peaking in Q3-22. With merchandise and food prices soaring, core inflation shows no signs of receding soon.

The US’s economic resilience with stubbornly tight labour markets and no obvious signs of cresting core inflation will keep the Fed at the forefront of hawkish monetary policy among the G10 that Latin American officials may be unable to match—risking downside for the regional currencies, or at least limiting upside.

In our latest forecast update published this week, we foresee cuts by all the Pacific Alliance plus Brazil central banks through 2023 compared to steady rates in the US (and perhaps early-year hikes, see chart of the week). Continued Fed hawkishness could see officials in the Americas postpone the rate cuts leg of their policy cycles to insulate their economies from exchange-rate-related inflation and limit investor outflows towards the appeal of higher US rates.

Brazil’s central bank is expected to hold its Selic policy rate unchanged at 13.75% next Wednesday, bringing its 1,175bps hiking cycle since March 2021 to an end. Petrobras’s cuts to fuel prices, coupled with the government’s country-wide cap on state taxes on fuel, has resulted in a slowdown in year-on-year headline inflation, with inflation expectations following it lower. Beneath declines in headline CPI, however, core price pressures remain well entrenched, which may see the BCB roll out “a residual adjustment” (as indicated in its August decision) of 25bps.

Mexican retail sales and Colombian economic activity figures for July round out the week on the data front while we continue to monitor discussions in Chile on the process of rewriting the constitution after Chileans firmly rejected the constitutional assembly’s proposal in early-September. In Colombia, Congress will begin debate on tax reform that is projected to boost public coffers by COP 25 tn according to the 2023 budget approved earlier this week (see our Bogota team’s first impressions here).

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.