- Chile: Imacec expanded 10.1% in December (-0.4% m/m)

- Colombia: 2021 employment closed 5.1% below pre-pandemic levels; active population lowest since 2013

- Mexico: Technical recession looming as credit contraction slows

- Peru: New political tension culminates in change of Cabinet, again

CHILE: IMACEC EXPANDED 10.1% IN DECEMBER (-0.4% M/M)

GDP likely grew 12% in 2021, supporting solid growth for 2022.

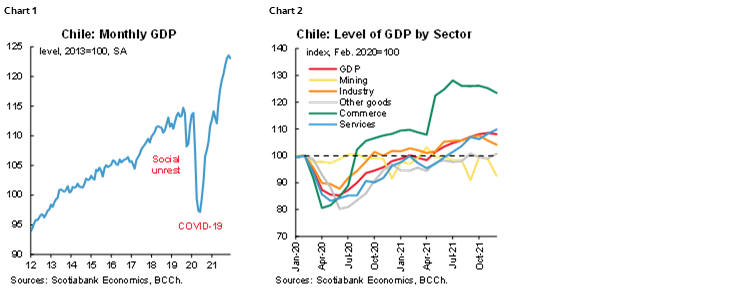

On Tuesday, February 1, the central bank published December’s Imacec index of economic activity, which grew 10.1% y/y, slightly below market expectations (Bloomberg: 10.3%) and Scotiabank’s estimate of 10.5%. Services (business and health) and trade largely explained the y/y economic growth. Goods production also contributed positively to the y/y increase, highlighting the performance of construction.

On a m/m basis, however, goods production and trade showed weakness in December. The Imacec fell 0.4% m/m (chart 1), mainly explained by the negative performance of mining (-6.2% m/m). The Imacec of the manufacturing industry fell 1.4% m/m, registering its second consecutive fall after six months of expansion (chart 2). Trade fell 1.4% m/m, continuing the slowdown that has been dragging on for a few months, after the high level it reached in the middle of the year fueled by fiscal transfers and pension fund withdrawals.

Based on high-frequency data on debit card purchases, January retail sales remain at historically high levels, reaffirming that the slowdown in retail growth is likely to be very gradual. Additionally, we estimate that the approval of the Universal Guaranteed Pension (PGU) will have a positive impact on GDP in 2022 of between 0.2 and 0.3 percentage points, mainly thanks to the positive effect it will have on private consumption.

All in all, GDP is likely to have grown 12% in 2021, in the upper part of the range of the central bank’s projection made in December. And while GDP contracted in December in seasonally adjusted terms, we consider that the high level with which it began the year provides solid growth support for 2022, which is likely to see an expansion of 3.5%. As we pointed out earlier, consumption has slowed gradually, and will continue to soften during, at least, the first part of the year, despite the support provided by the abundant liquidity in debit and checking accounts, as well as the resources that the PGU will contribute this year. We estimate that investment will grow in 2022, as new large-scale projects identified at the end of last year and the beginning of this year are incorporated into the project pipeline.

Public spending continued to grow strongly in December, with a real expansion of 41.3% y/y. According to the Budget Office, total spending grew by 33.3% in 2021, with an expansion of 36.3% in current spending, owing to the extraordinary aid provided by the government last year. For 2022, the Budget Law contemplates a drop in spending close to 22%, which we believe could be mitigated by the increased fiscal space that the next government will have from higher GDP growth in 2021 compared to what was expected a few months ago. This spending capacity will also provide some flexibility to the new authorities to support economic activity this year, without neglecting the structural deficit commitment set for this 2022.

—Jorge Selaive, Anibal Alarcón, & Waldo Riveras

COLOMBIA: 2021 EMPLOYMENT CLOSED 5.1% BELOW PRE-PANDEMIC LEVELS; ACTIVE POPULATION LOWEST SINCE 2013

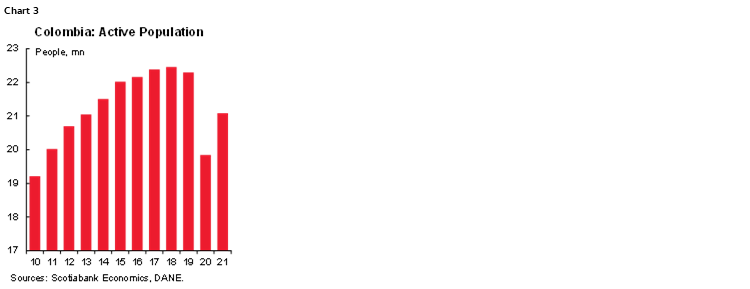

Employment data for December 2021, released on Monday, January 31, show that the jobs recovery stagnated by the end of the year, despite the relaxation of restrictions. Employment contracted by 123 thousand m/m in December, with roughly 80% of job losses in rural areas, while urban jobs contracted by 22 thousand m/m. The employed population was 21.08 million on average in 2021, the lowest since 2013 and 5.1% below the pre-pandemic level (chart 3). The unemployed population fell by 10.8% y/y, but is still 28.2% higher than in 2019, while inactivity remained high at about 16.55 million people, well above the 14.5 million of the pre-pandemic average, with the elder and younger populations most affected.

Nationwide unemployment came in at 11.0% in December, while urban unemployment (major 13 cities) was 11.6%. In seasonally adjusted terms, the nationwide unemployment rate was 12.3% in December, decreasing slightly from 12.6% in November, and 12.7% in urban areas as compared to 13.9% in November (chart 4). On average, 2021 nationwide unemployment rate stood at 13.7% and 15.3% for urban areas, decreasing from the previous year’s figures of 15.9% and 18.2%, respectively, but still above of 2019 (pre-pandemic) number of 10.5% and 11.2%, respectively.

Colombia continued to operate without significant restrictions in December, with job gains concentrated in sectors such as transport-related services (+181 thousand), construction (+150 thousand), and professional and technical activities (+137 thousand). In 2021, overall job gains were 1.24 million, mainly in sectors such as commerce (+334 thousand), construction (+157 thousand), and hotels & restaurants (+153 thousand), showing the effect of the reopening. Sectors lagging from pre-pandemic (2019) levels include the leisure sector (-298 thousand), manufacturing (-236 thousand), and public administration, education, and health services (-232 thousand).

Some improvements were made regarding gender gaps in 2021, though progress stalled in the last quarter of the year. The nationwide female unemployment rate was 18.1% and the male rate was 10.6% on average in 2021. In urban areas female unemployment was 18%, while the male rate was 13.1%, pointing out that main gaps are concentrated in rural areas.

Regarding jobs quality, in 2021 around 57.6% of job creation was in the informal sector. However, it is worth noting that this ratio improved by the end of the year as around 48.7% of job gains were in the informal sector in the fourth quarter. That said, in December informality stood at 47.7% in the urban area (13 major cities) and at 48.8% in the 23 main cities, improving from previous year’s numbers of 48.6% and 49.5%, respectively, but still are high.

Summing up, December’s employment data continue to show positive results from services-related and formal sectors in urban areas. That said, concerns regarding the labour market remain. Rural and agricultural jobs continued to decrease, while the data also show that inactivity remains high. In 2022, as the economic recovery consolidates without restrictions better dynamics in terms of job creation is expected.

—Sergio Olarte & Jackeline Piraján

MEXICO: TECHNICAL RECESSION LOOMING AS CREDIT CONTRACTION SLOWS

I. Fourth quarter 2021 GDP contracted q/q for a second consecutive quarter

According to INEGI’s preliminary estimate, fourth quarter 2021 GDP came in at 1% y/y, below market expectation of 1.5% y/y (chart 5). For the year as a whole, GDP grew by 5%. On a quarterly basis, Q4 marks the second consecutive decline, -0.1% q/q (-0.4% q/q previously), which would put Mexico in a technical recession if confirmed by the final estimate.

Industry increased marginally, 0.4% q/q, with tepid growth largely due to the downward trends in both construction and utilities as well as the continuing logistical challenges in manufacturing posed by supply chain bottlenecks. Despite a relaxation of public health restrictions, services remained subdued, falling for a second consecutive quarter -0.7% q/q (-0.9% q/q previously), mostly owing to the outcomes on the labour market from the outsourcing bill. Primary activities rose marginally by 0.3% q/q from 0.7% q/q the previous quarter.

Looking ahead, we expect the negative effects of the outsourcing bill will fade over time. Nevertheless, the recent increase in infection rates will delay the full recovery in services. Meanwhile, the effects of low investment and value chain disruptions are likely to hinder industry’s upsurge in the short run, although we expect activity to start normalizing by the second half of the year. Additional downside risks include stickiness in inflation (mainly in the core component), a more restrictive monetary policy stance coming out of the February decision, uncertainty surrounding local economic policies, and volatility in international financial markets.

II. Declines in outstanding credit indicators attenuated amid recovery in the real sector

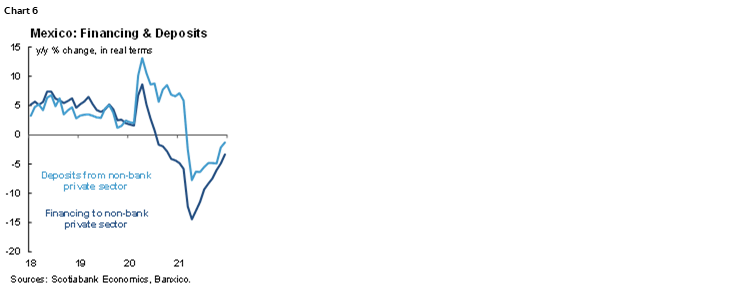

According to Banxico, the decline in bank deposits slowed in real terms from -2.2% y/y in November to -1.3% y/y in December (2021 average -2.8%), as term deposits contracted –8.9% y/y from -10.3% y/y, while demand deposits increased from 2.4% y/y to 2.8% y/y (chart 6). During 2021, deposits were affected by a higher base of comparison and an increase in household spending triggered by an easing of pandemic constraints. However, the recovery in income, supported by remittances (at record highs), attenuated the decline in bank deposits.

Total bank financing fell -4.8% y/y, marking ten months in negative territory. Financing to the Federal Public Sector continued to contract, after double-digit increases during 2020 and through the first half of 2021. Financing to the private sector, though still in negative territory at -3.3% y/y, shows signs of stabilizing. Similarly, declines in consumer and corporate credit slowed to -4.3% y/y and -4.6% y/y, respectively. Meanwhile, housing loan growth has remained positive and stable during the pandemic.

The total non-performing loan ratio decreased marginally to 1.96% from 2.06%. By component, the rate of non-performing corporate loans was 1.73%, housing 3.39% and consumer 3.91%, with all three components very close to their annual average (1.99%, 3.39%, 3.91%, respectively).

Going forward, we expect that bank deposits and financing will resume an upward trend, reflecting recovery in the real and services sectors.

—Luisa Valle & Miguel Saldaña

PERU: NEW POLITICAL TENSION CULMINATES IN CHANGE OF CABINET, AGAIN

A new episode of political tension within the Peruvian government itself culminated in the announcement by President Castillo of his intention to form a new team. The latest Cabinet change was triggered by the resignation of Avelino Guillén—the third Interior Minister of Castillo’s Administration—over a dispute regarding the promotion of senior police officers.

The Cabinet chaired by Mirtha Vasquez lasted only four months, from October 2021 to January 2022, with a moderate profile focused on economic stability, progress in the vaccination process, and the management of social conflicts through dialogue. Vasquez had managed to reduce political tensions with Congress and even de-escalate social protests, though without reaching definitive solutions, but the frictions within the government continued.

Vasquez backed Guillén and his resignation led to the Cabinet change. The episode is relevant in that it could reflect a breaking point in the support that the government had been receiving from Verónica Mendoza’s team, the moderate left-wing profile.

Support for President Castillo has been weakening in the first six months of his government. Despite the respite in political uncertainty under Vasquez, the President’s disapproval was on the rise (64% in January 2022) according to an IEP poll. A recent poll showed that Castillo’s disapproval rating rose to 61.5% in January.

The agenda facing the new Cabinet, which is yet to be appointed, includes key issues such as the tax treatment of mining, the development and distribution of gas, the deterioration in the technical quality of key government positions, and appointments to key regulatory bodies. In addition, sub-national government elections are scheduled for October 2, 2022.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.