- Inflation strongly surpassed expectations as Americans move on from the pandemic

- There is very high breadth to inflationary pressure…

- ...and pressures remain hot at the margin

- Our Fed and curve views are tracking well

- BBB is dead, the US probably faces a lame duck presidency into future uncertainties

US CPI m/m %, headline / core ex-food and energy, SA, January:

Actual: 0.6 / 0.6

Scotia: 0.2 / 0.2

Consensus: 0.4 / 0.5

Prior: 0.5 / 0.6

US CPI y/y %, headline / core ex-food and energy, SA, January:

Actual: 7.5 / 6.0

Scotia: 7.0 / 5.6

Consensus: 7.3 / 5.9

Prior: 7.0 / 5.5

Here’s more evidence that Americans are shaking off the pandemic that follows the nonfarm payrolls surprise. US inflation came in well above expectations last month and at 7.5% y/y hit its highest rate since February 1982. At 6% y/y, core inflation is running hotter than at any time since August 1982.

Forty-year highs in inflation accompanied by remarkably high breadth and no signs of pressures letting up at the margin should deeply worry the FOMC. It is so far behind the inflation fight with the US at or beyond maximum employment alongside rising wage pressures that this is going to be very difficult to address with monetary policy tools absent abrupt and harsh policy movements. Persistent supply chain pressures combined with hot demand (ie: it’s both!) in a booming US economy that is entering excess aggregate demand risk unmooring wage and inflation expectations. The odds of a 50 point hike in March and roll-off commencing as soon as Q2 have gone up again. The cost to the Fed’s misreading of inflationary pressures is that the Biden administration could well be a lame duck presidency over the duration of his term which could reduce policy flexibility down the road should the economic outlook require it.

THE FED, PRESIDENT BIDEN AND MARKETS

Markets are now pricing a cumulative six hikes by the Fed this year if they go at a quarter-point drip pace. Our forecast is still 7 hikes. Odds of a 50 move in March are obviously higher after payrolls and CPI and with growing evidence that omicron is fading. There are also higher odds that they shift to roll-off starting as soon as Q2. Furthermore, this kind of heat basically kills any last chance at a scaled back Build Back Better fiscal package with Senator Manchin very likely to dig in even further. In my opinion, President Biden is in a very weak position into the mid-terms and not only because of the incumbent’s usual disadvantage during mid-term elections.

As for the rest of the curve, the US 10 year yield is flirting with ~2%. That is our forecast for the end of Q1 with 1.5 months to go and more hawkish guidance likely at the March FOMC, but with an awful lot of runway left on the year. Our US 10s forecast is 2.4% at year-end. I'd still leave it at that but have to be open to a fatter tail to the upside than downside. To adjust it at this point, however, would probably be imprudent given many risks. All of which is to say that the month-to-month swings and the volatility around the bumps and wiggles on the road are nevertheless coalescing around our curve views.

WHY THE UPSIDE SURPRISE?

Why did inflation shoot higher than just about anyone expected and particularly higher than my estimate?

One theory is that price gains were hot because behaviour has fully adapted to the pandemic. Another theory is that omicron was generally milder in terms of average severity of outcomes and so it didn't dampen high contact prices like delta and prior waves did. A third theory is that there is high damage to supply chains from omicron, yet nonfarm did not support that interpretation from a labour market standpoint.

I would lean toward the resilience angle in a breakage of the disinflationary evidence to date during past spikes in cases in that the signals that are being shed by the US economy through job gains and inflation are very much indicating that Americans are getting on with things and leaving the pandemic in the dust. That’s not equivalent to saying the pandemic is necessarily over per se.

NO LET-UP IN PRESSURES AT THE MARGIN

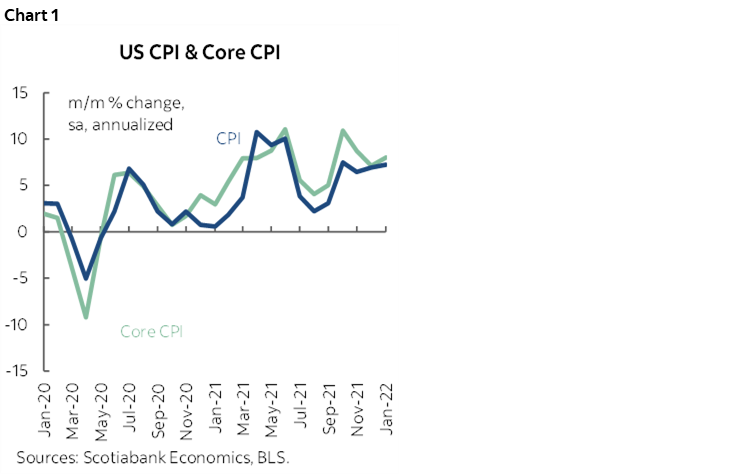

As chart 1 shows, there is no evidence that price pressures are letting up at the margin defined as the annualized month-over-month and seasonally adjusted rates of increase in headline and core CPI inflation. In fact it’s the opposite. The annualized pace of monthly CPI gains has been running between 7–11% over the past four months. The annualized pace of monthly core CPI gains has been running between about 6½ % and 7½%.

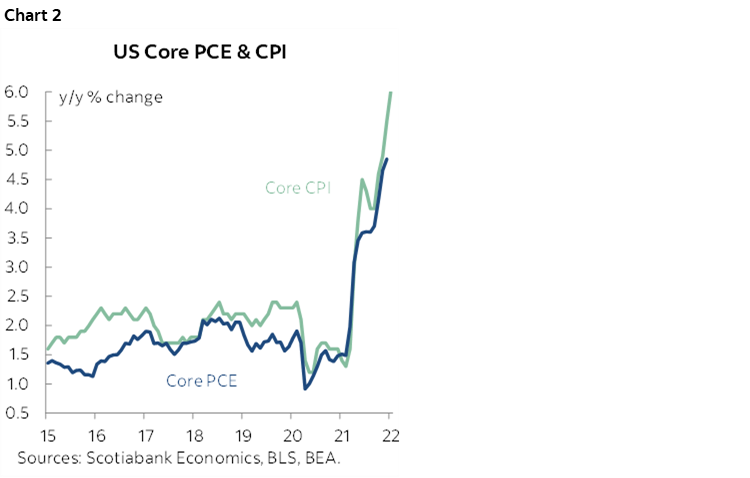

This is how central bankers should be looking at the pressures rather than talking all the time about year-over-year rates and how they are distorted when we don’t really have much comfort around that argument anyway (chart 2). As I pointed out in this morning’s note, the same central bankers who told us not to focus upon year-over-year rates throughout the pandemic to date are now telling us to focus upon how they’ll ebb going forward. I’d rather they be more circumspect toward the pressures at the margin and not so wedded to shorter-term developments by year-end or versus how price pressures could evolve over the full cycle. There is very much a live debate around that outlook which should merit not sounding overly strident that inflationary pressures will magically disappear going forward.

THE DRIVERS

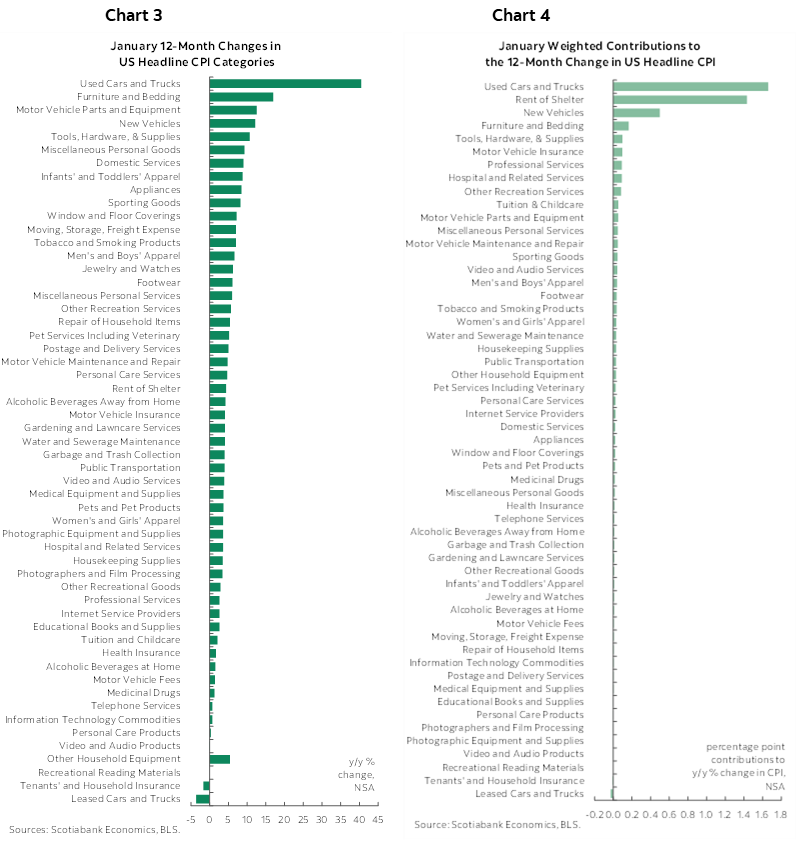

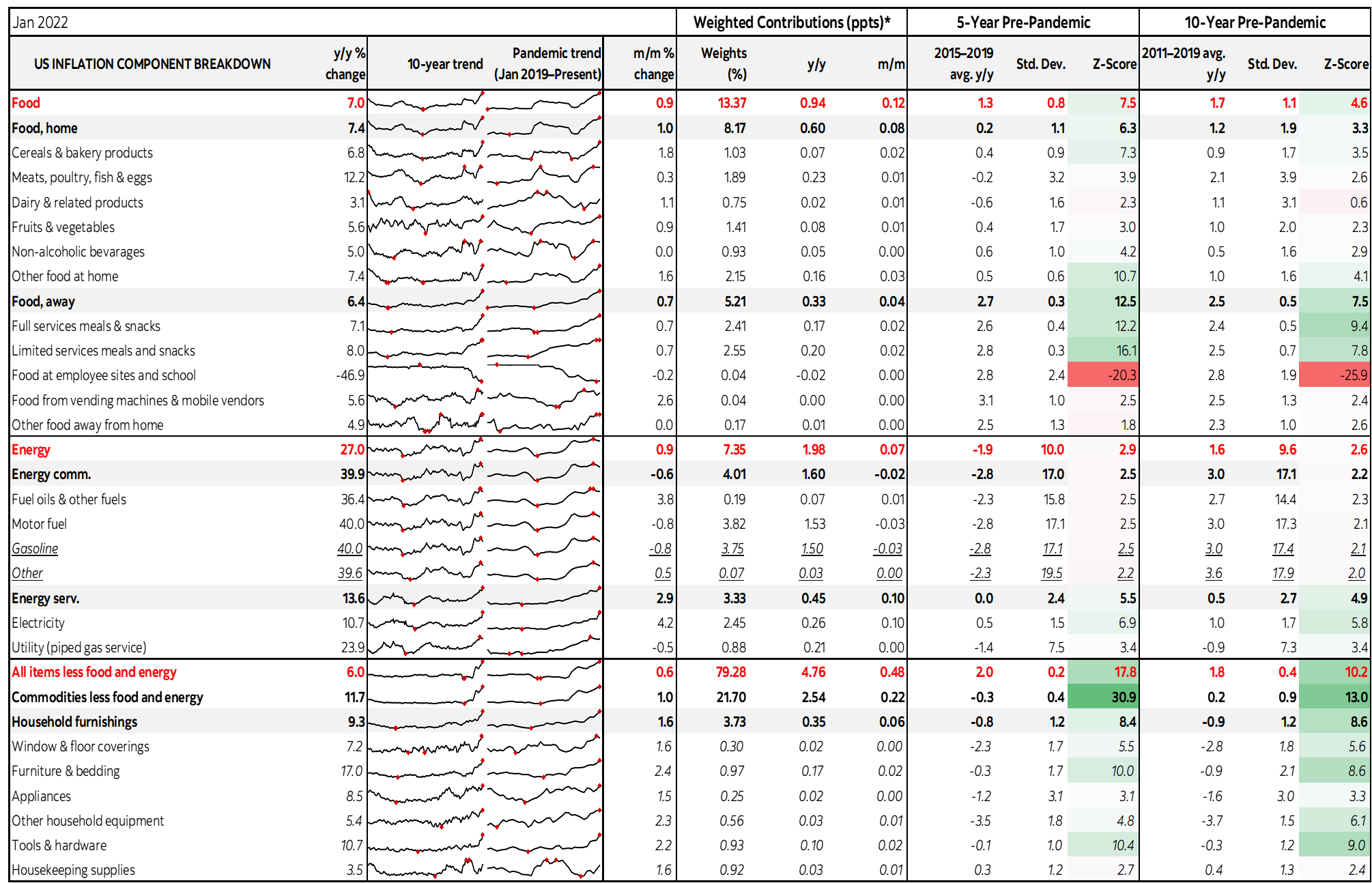

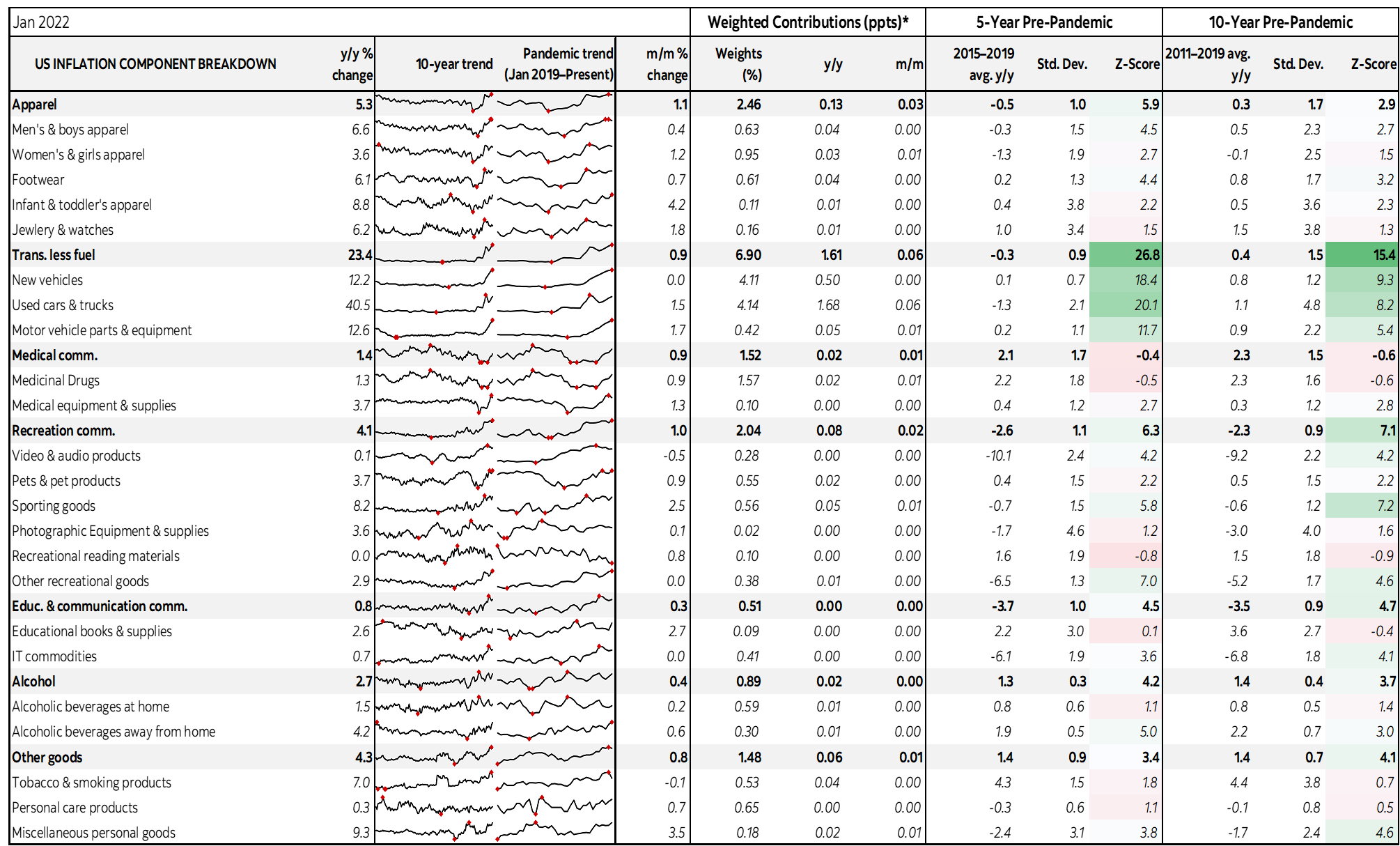

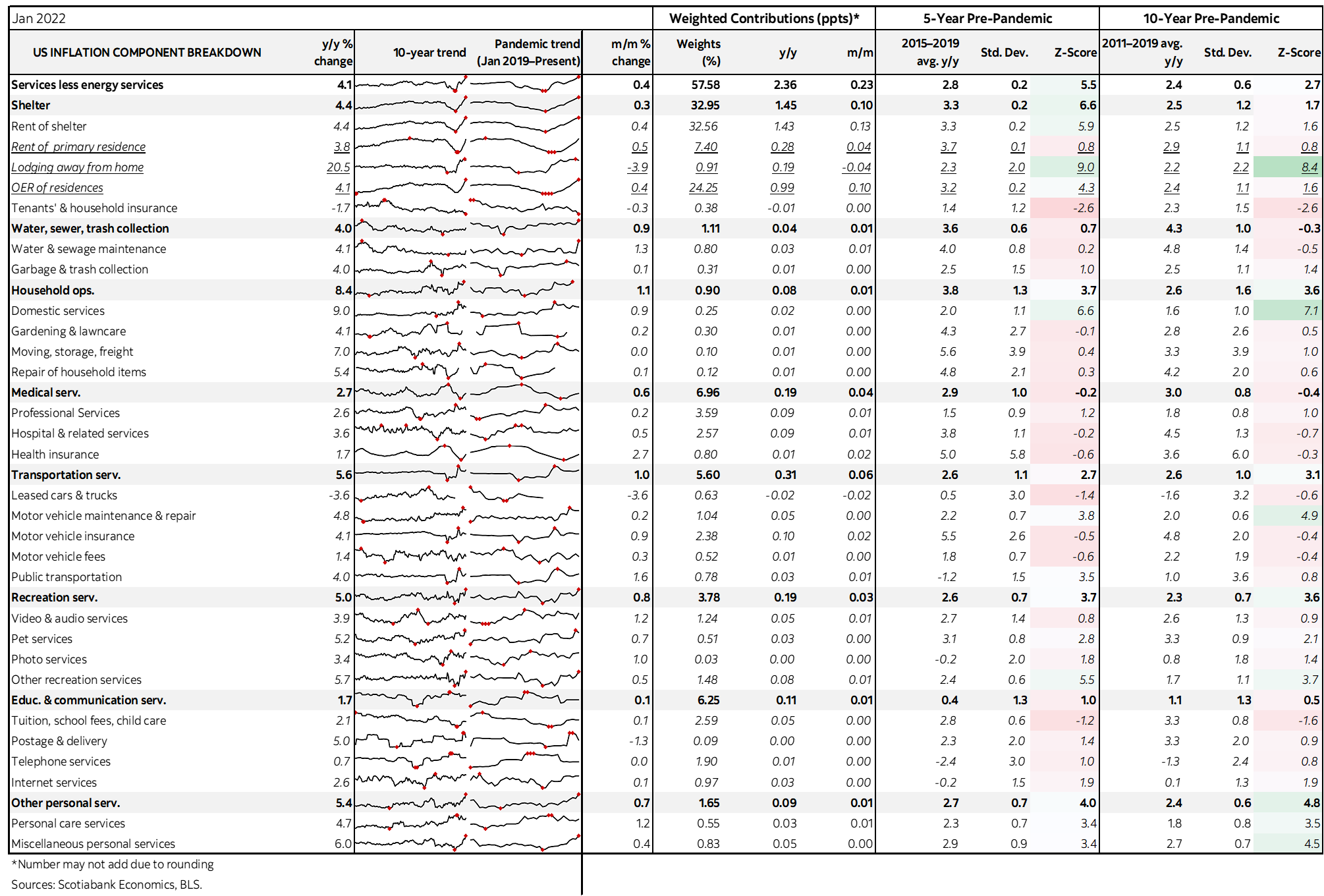

A breakdown of the CPI basket is shown in charts 3–6. Chart 3 shows the unweighted y/y changes in CPI inflation by component; 84% of the CPI basket is over 2% y/y which indicates very high breadth. This is clearly not just a relative price shock versus generalized inflation. Chart 4 does the same thing but weights the individual components in terms of their shares in the CPI basket. If you’d like to avoid inflation then don’t own a house, don’t drive a vehicle, don’t go anywhere and don’t eat.

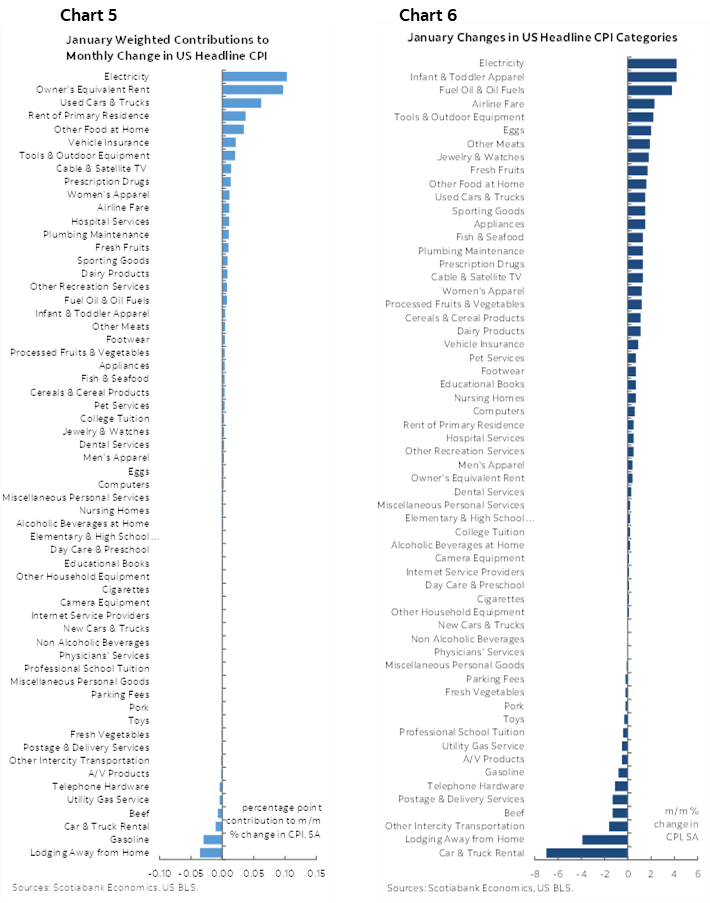

Chart 5 breaks down the basket in month-over-month unweighted terms while chart 6 does the same thing but using weighted contributions to the overall change in prices. 76% of the basket is experiencing m/m annualized price changes in excess of 2%.

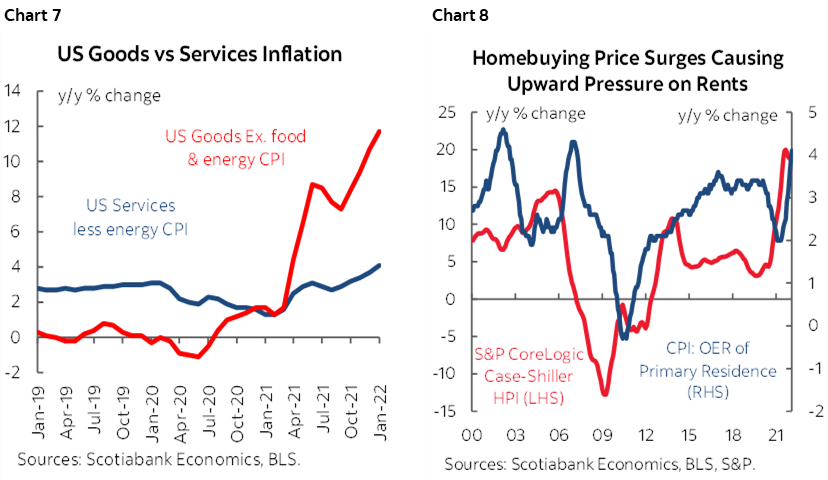

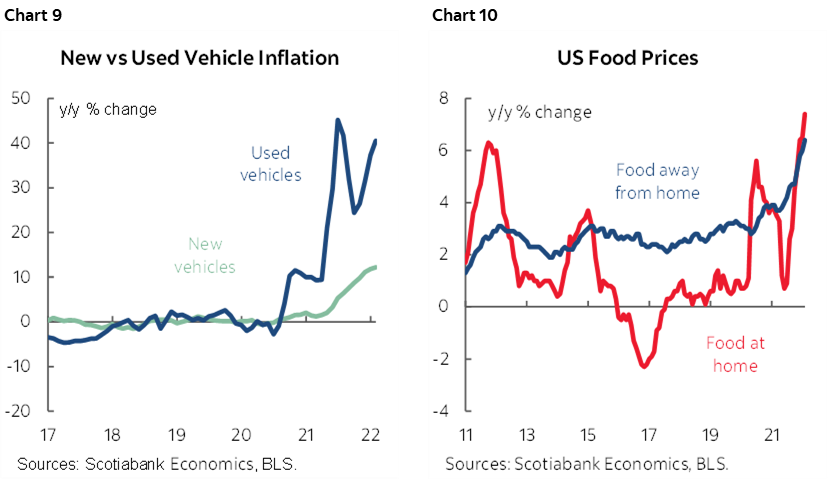

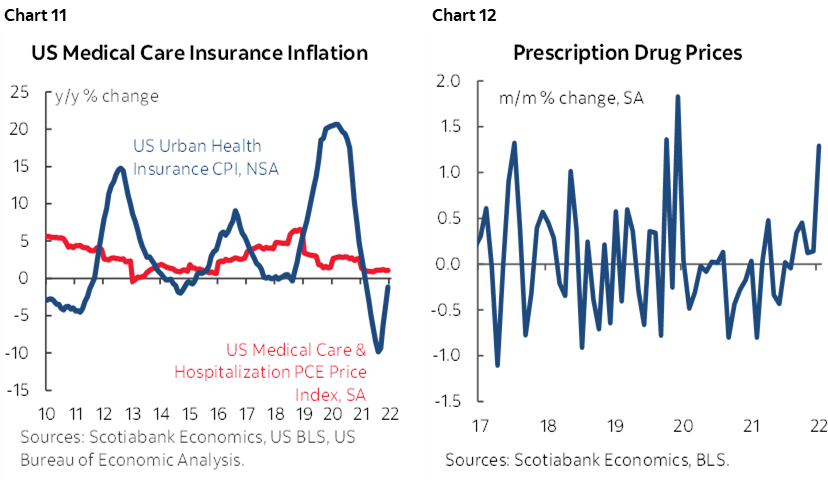

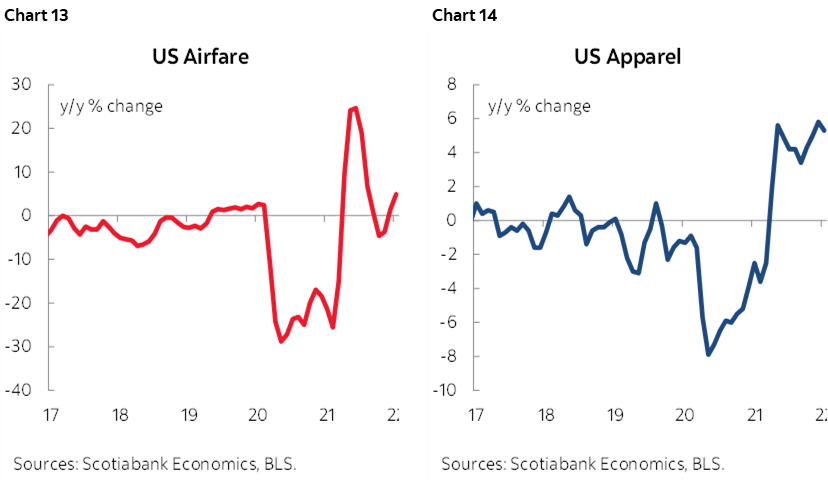

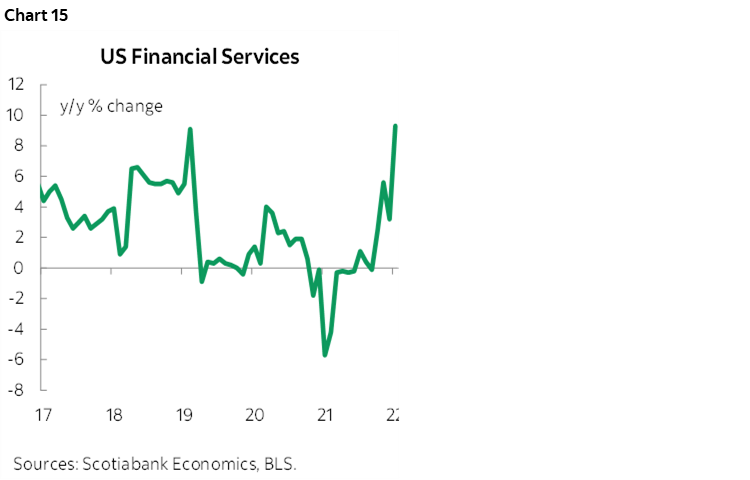

Charts 7–15 provide a breakdown of some of the categories. What I was most surprised was the paucity of evidence that high contact service price inflation ebbed. That was only true in terms of lodging that fell 3.9% m/m. Otherwise, food away from home (ie: mostly in-person dining and take-out) was up 0.7% m/m and airfare jumped 2.3% m/m higher.

Other key contributions came from housing as owners’ equivalent rent was up 0.4% m/m with rent up 0.5% m/m. Food was up by 0.9% m/m. Electricity prices jumped higher by 4.2% m/m but gasoline (-0.8%) and utility gas (-0.5%) restrained some of the overall jump in total energy prices (+0.9% m/m).

It didn’t take long after the release for Senate Manchin to chirp that the Fed has to address inflation “head on.” Strong payrolls and hot inflation are the final nail in the Build Back Better coffin. The US already has political gridlock from within the ruling Democrats who in theory hold onto the Executive and legislative assemblies. Come November, the incumbent’s historical disadvantage during mid-term elections is likely to cement gridlock over the remainder of President Biden’s term through 2024. While that may be welcome in the short-term by way of not adding further fiscal impulses to an already hot inflation picture, it could hamper the ability of the US administration to respond to future shocks especially as conditions migrate away from the relatively early growth impulses.

Please see the accompanying table with detailed charts, figures and measures of dispersion.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.