- The BoC’s favoured core measures were soft again in March

- Other core measures not so much

- This is encouraging, but still just three months of softness...

- ...with a lot of ground to cover before the June meeting

- What was hot and what was not

- BoC’s Macklem to speak shortly

- CPI m/m NSA / y/y %, March:

- Actual: 0.6 / 2.9

- Scotia: 0.7 / 3.0

- Consensus: 0.7 / 2.9

- Prior: 0.3 / 2.8

- Average of trimmed mean and weighted median CPI, March: 1.25% m/m SAAR

Make that three in a row!

The Bank of Canada’s preferred core inflation gauges were soft again in the month of March. At the margin, that slightly added to June cut pricing. That’s welcome news after all that Canadians have been through. But we still need much more evidence. The core question of whether this is a durable soft patch remains open in my opinion.

There is a lot of ground to cover yet between now and the June meeting and I’ll give reasons for why I’m not prepared to fundamentally pivot to June. On balance, the high resilience in core services pricing and ongoing suspect disinflation on the goods side of the picture makes me cautious toward declaring victory over inflation especially since it’s just three months of evidence with Spring data pending.

Market Reaction—June Probability Up, Modest Cuts for the Year

CAD depreciated by about half a penny or so versus the USD post-CPI. The Canada two-year yield fell by about 10bps post-data and is outperforming the US front-end.

OIS pricing for the June meeting added another 5bps and is currently sitting at about 19bps of a quarter point cut. The rest of the year’s pricing moved closer to our forecast for 75bps of total cuts by year-end at just under 70bps priced. Thus, markets rare leaning toward an earlier start to cutting than our present forecast but a similar end for the year.

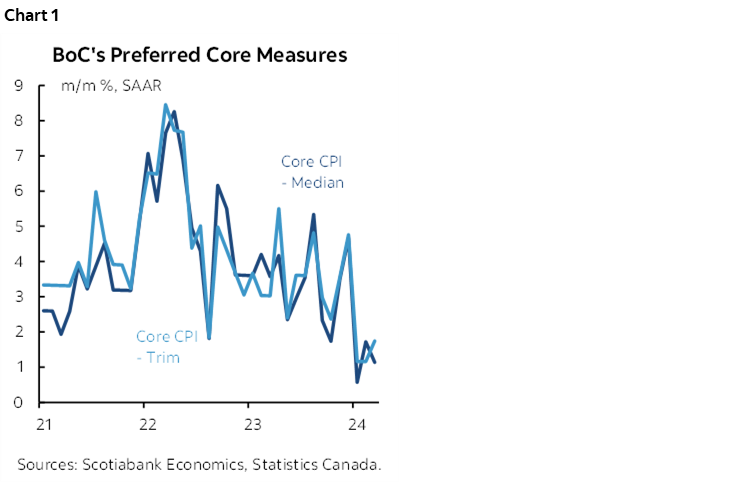

Core Measures Were (Mostly) Soft

The BoC’s preferred core inflation measures were soft. Trimmed mean CPI was up by just 1.75% m/m SAAR and weighted median CPI was up by just 1.15% m/m SAAR (chart 1). Those figures dropped the three-month moving averages to 1.4%% m/m SAAR for trimmed mean and 1.2% for weighted median.

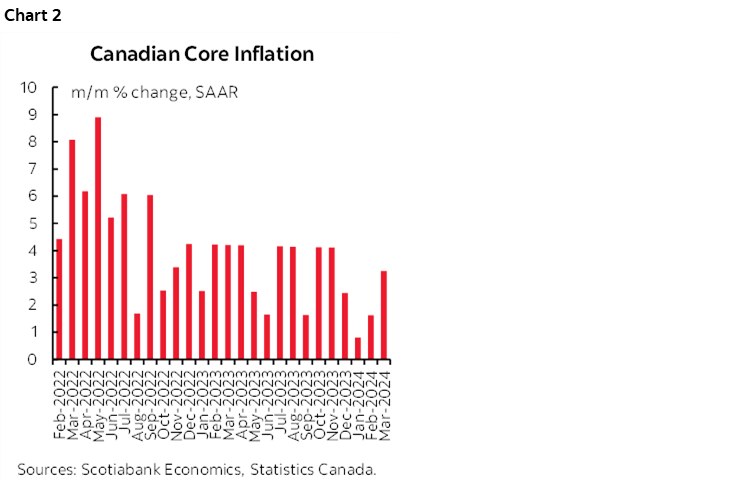

Other core measures were less cooperative but likely to play second fiddle in the BoC’s way of looking at inflation. Traditional CPI ex-food and energy was up by 3.3% m/m SAAR (chart 2) and the three-month moving average is now at 1.9% m/m SAAR. CPI excluding the eight most volatile items and indirect taxes was up by 2.4% m/m SAAR.

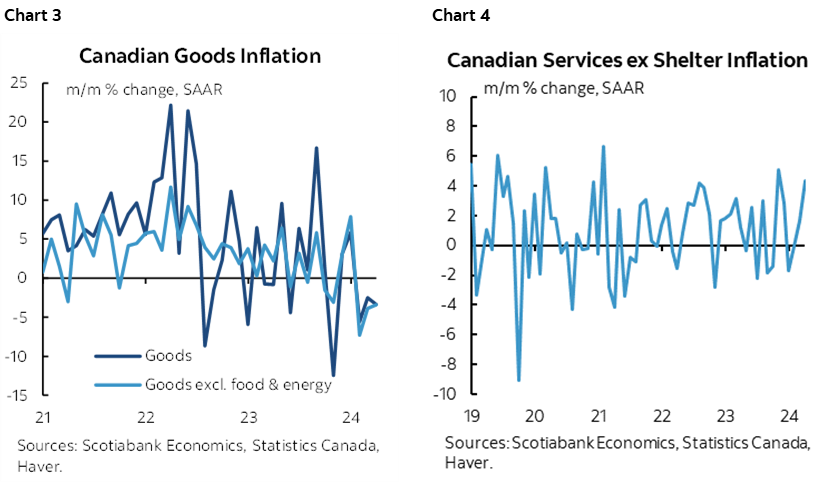

Resilient Services, Goods Disinflation

All of the weakness we’re getting remains on the goods side of the picture (chart 3) while core services inflation ex-housing jumped higher (chart 4).

Goods CPI was down –0.3% m/m SA and so was core goods CPI ex-food and energy. Core services ex-shelter was up by 0.3% m/m SA.

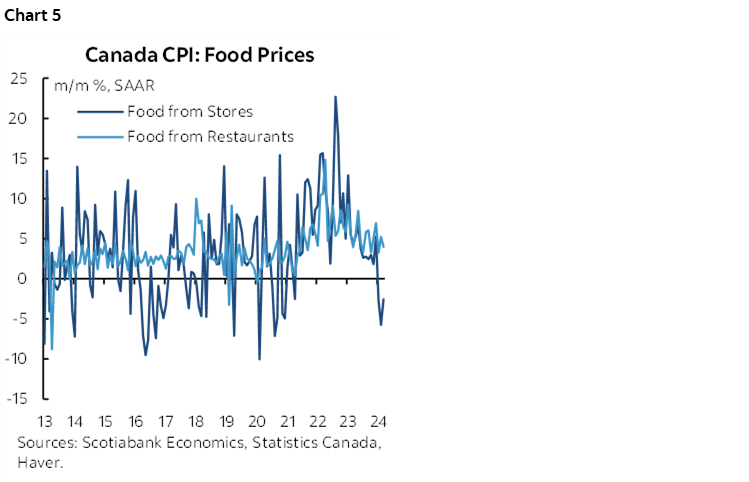

Headline Weighed Down by Food and Gas

Headline CPI was up by 0.3% m/m SA. Cool food prices (+0.1% m/m SA) weighed on the headline reading as grocers continued to cut prices while restaurant inflation remains hot (chart 5).

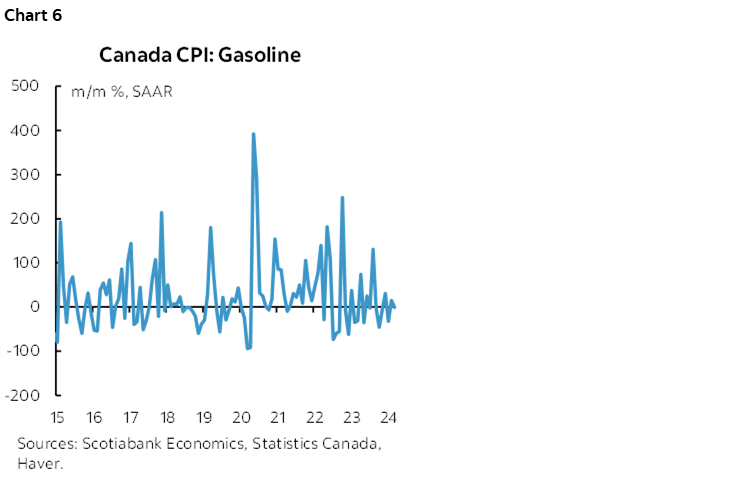

Gasoline prices slipped by –0.1% m/m SA as the 4.9% m/m NSA rise was roughly in line with longer-term seasonal norms and little changed in m/m annualized terms (chart 6).

What Was Hot...

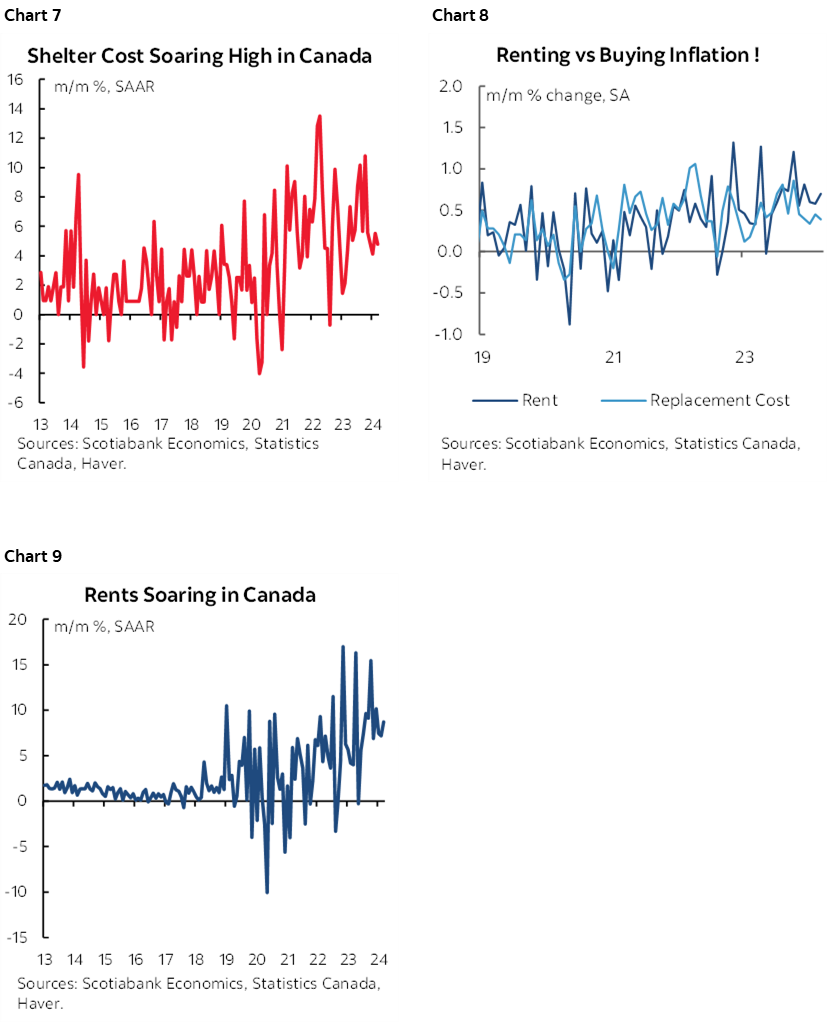

Shelter inflation remains very hot (chart 7). Rent inflation remains elevated (charts 8, 9).

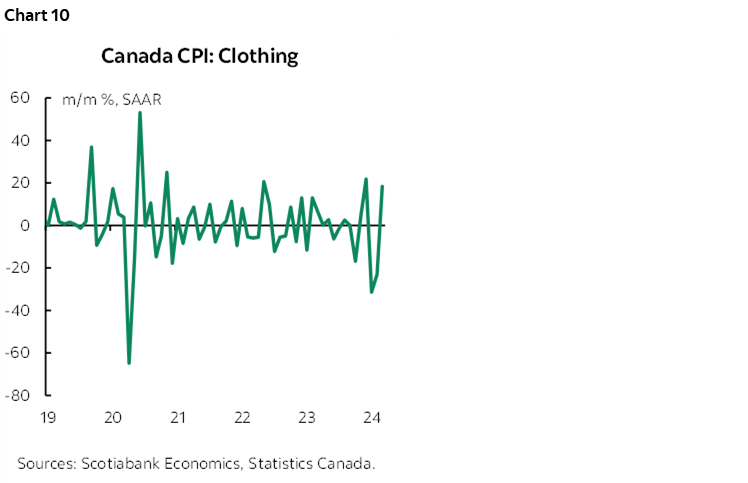

Clothing prices rebounded sharply in March as discounting subsided and gave way to the introduction of new Spring lines at higher prices (chart 10).

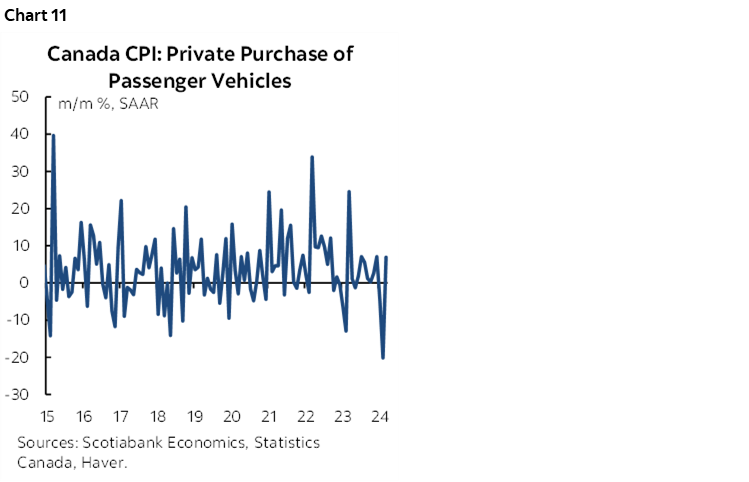

There was also a rebound in vehicle prices that were up by about 7% m/m SAAR (chart 11).

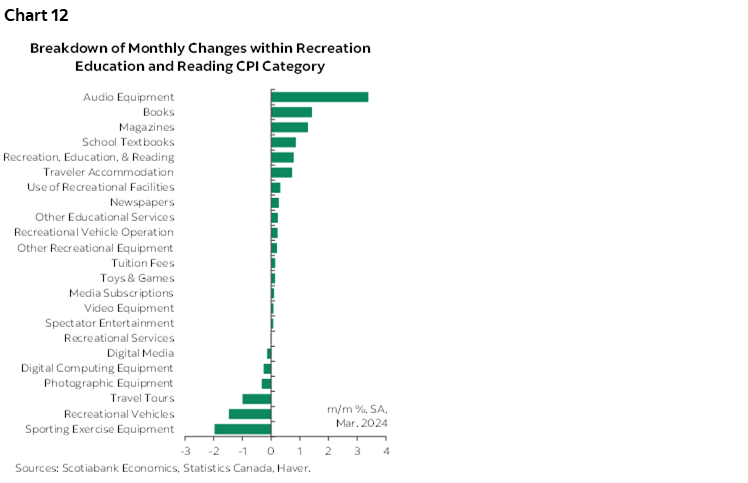

The recreation, reading and education category was up by 0.6% m/m SA. Chart 12 shows a break down of that category.

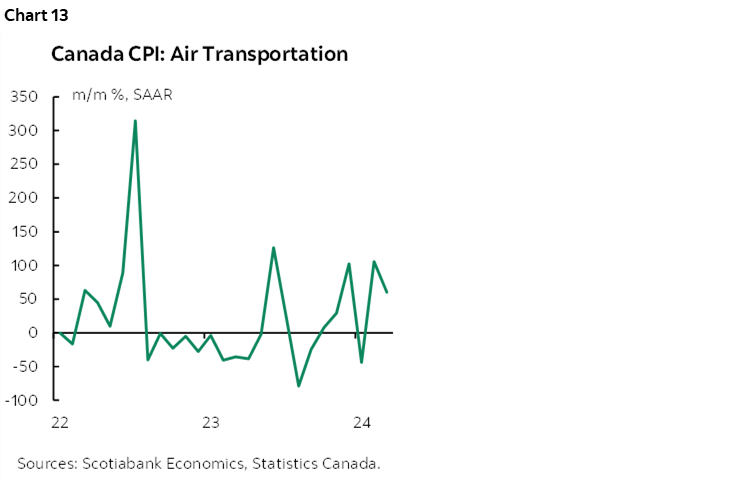

Air transportation was sharply higher in March (chart 13).

...And What Was Not

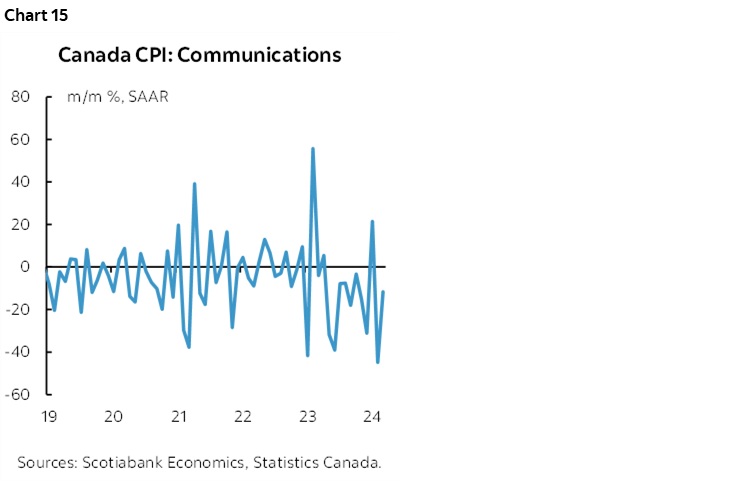

Communications prices fell again (chart 14). There were smaller declines in March over February than the prior month, but still, cell service pricing fell another 1.6% m/m NSA (-25% m/m in February). Internet service prices fell another 2.1% m/m NSA (-13.7% m/m NSA in February)

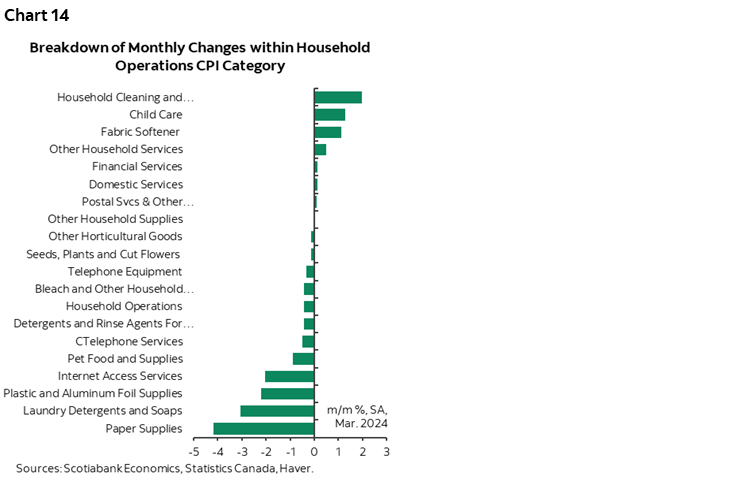

Chart 15 provides a break down of the whole household operations category.

Further Details

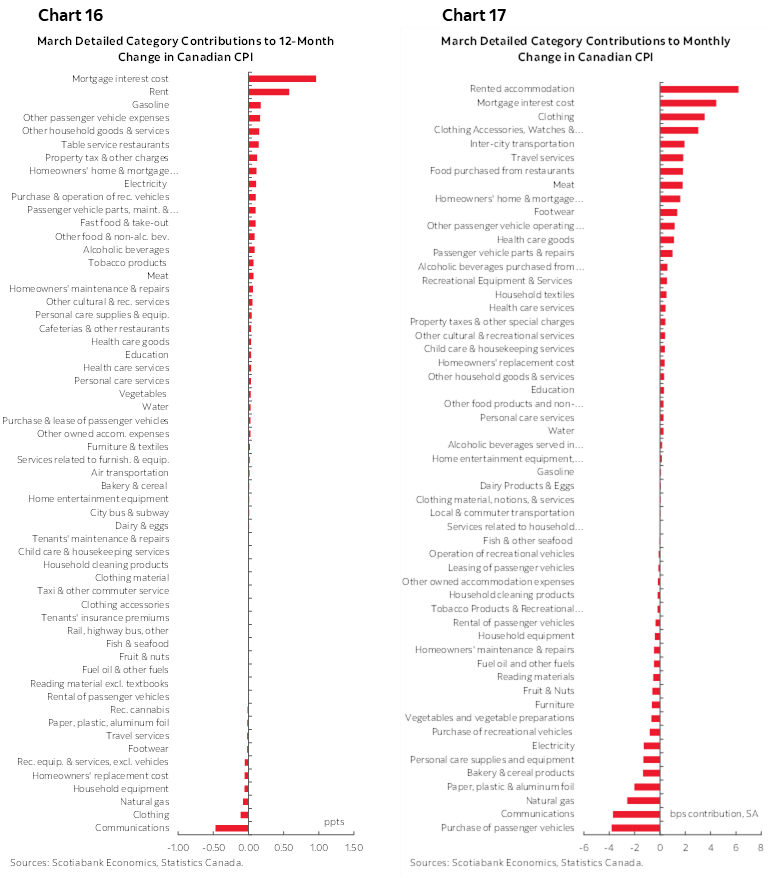

Please see breakdowns of the CPI basket in terms of weighted contributions to y/y inflation (chart 16) and weighted contributions to month-over-month seasonally adjusted inflation (chart 17).

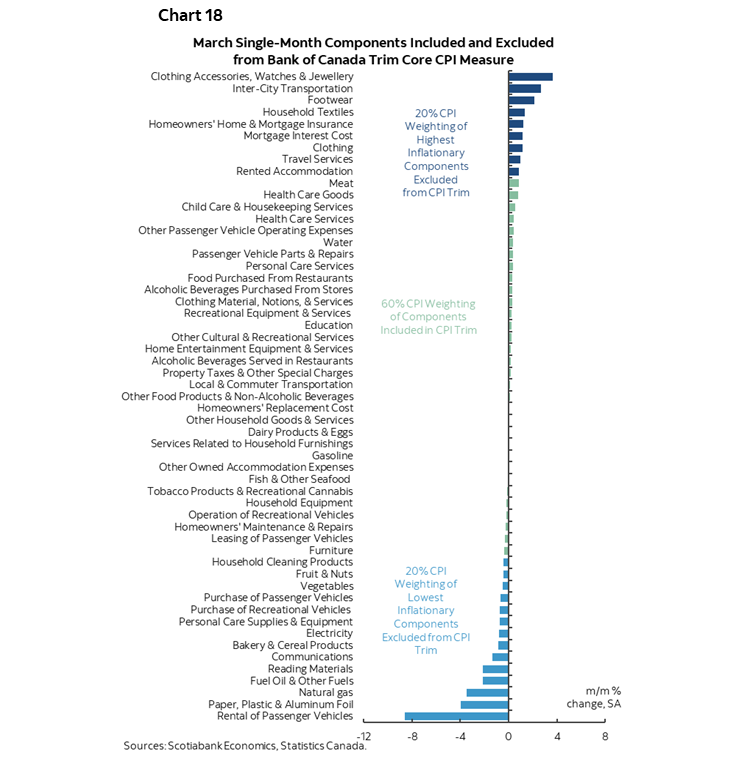

Chart 18 shows a breakdown of what was included in trimmed mean CPI last month.

Year-to-Date Tracking

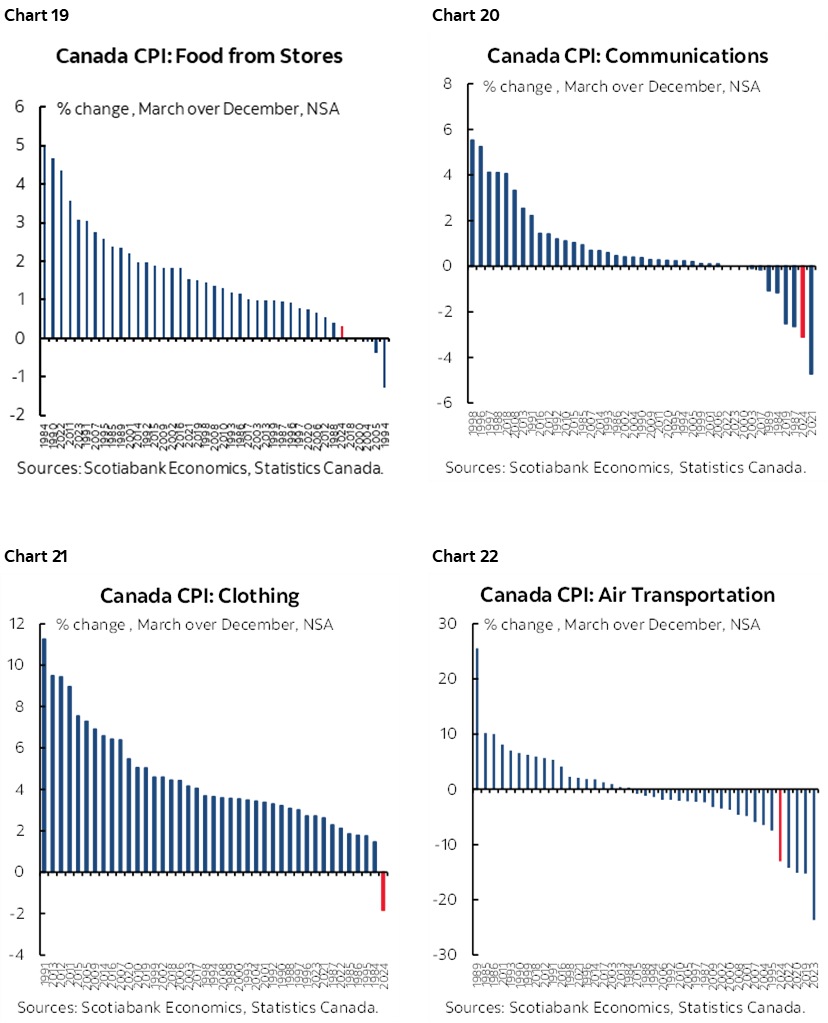

There remains ongoing unusual softness in several categories including ones affected by seasonal changes and regulatory pressure. Charts 19–22 provide depictions in addition to the earlier chart for grocery prices.

BoC Implications

Governor Macklem speaks at 1:15pmET today on a panel alongside Fed Chair Powell. Watch for his reaction if asked by the moderator, former Finance Minister Morneau, what he thinks. There will be no audience Q&A or press conference.

To begin easing and embolden markets to price more must have more data and developments to support it in the wake of how central banks massively misjudged inflation over recent years. If a cut follows such a soft patch then it will be very revealing of the BoC’s bias to look through inflation risk at the beginning and cut at the first whiff of softening pressures.

There is still a lot of ground to cover until the June 5th BoC meeting. April CPI arrives on May 21st and the odds of a rebound from the forces driving goods disinflation are rising at the same time that carbon taxes will factor in with implications for headline CPI and any pass through.

Q1 GDP lands on May 31st. There may be upside risk to the BoC’s forecast with growth tracking north of 3% q/q SAAR.

The Federal government’s budget that lands later today will have to be incorporated into the BoC’s forecasts at least partially before June and fully in the July MPR forecast update.

The Federal Reserve’s cuts keep getting pushed down and out. At over 1.38 to the USD the currency has lost about three cents in a week. Emboldening cuts would strongly risk CAD punching through 1.40 and stoking more import price inflation.

All the while Canadian productivity, wages and unit labour costs continue to combine to drive inflation risk.

Now bring on the Spring housing market over April–June.

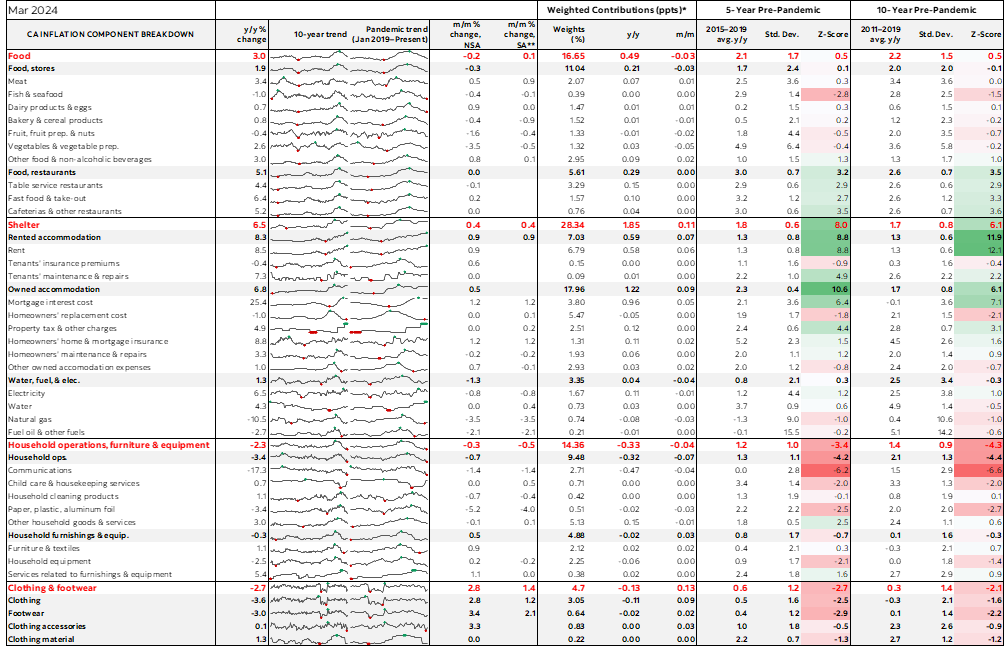

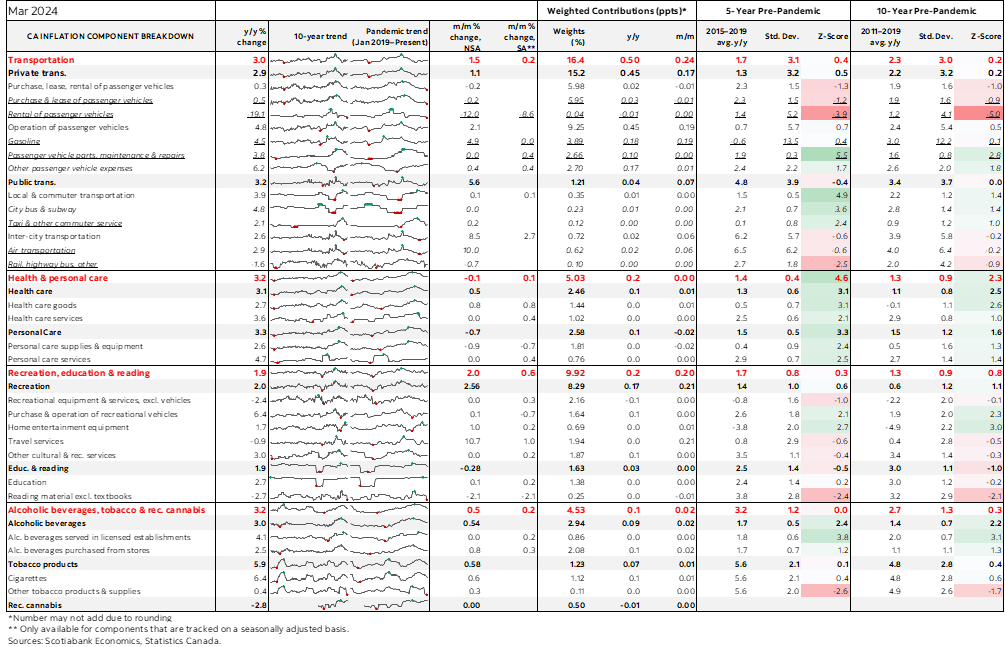

Lastly, please see the accompanying table at the back of this publication for further details on the components including micro charts and z-score measures of deviations from trends.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.