- BoC held the policy rate at 2¼% as universally expected

- Forward guidance continued to point to a long hold

- The script broadly met expectations not to rock the boat…

- ...but the street should challenge the BoC’s fading of recent developments

- Macklem dodged a golden opportunity to lean against hike pricing

- Canadian & US rates rallying roughly in tandem, CAD firmer, FOMC up next

The Bank of Canada kept its policy rate unchanged at 2.25% as universally expected and left guidance intact that it is on a prolonged hold while emphasizing uncertainty. That shouldn’t have surprised anyone in a don’t-rock-the-boat before the holiday season sense and with the long gap before the next decision seven weeks from now.

That’s not the same as saying their stance is beyond reproach. The BoC conveniently looked through most of the key developments and I’ll return to explaining this after recapping what they said. For now, the short and cautious message drove some positioning covering in the Canadian rates curve and a small decline in yields that consolidates only a modest portion of the rate hike pricing for later next year.

UNCHANGED LONG PAUSE GUIDANCE

Forward rate guidance was left unchanged as follows

“If inflation and economic activity evolve broadly in line with the October projection, Governing Council sees the current policy rate at about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment.”

To which they added “Uncertainty remains elevated.” Indeed. That’s new in that part of the statement, but not new elsewhere in the statement as they emphasized that “uncertainty is still higher than normal” in the prior statement.

A VERY SHORT STATEMENT

Please see the appendix for a comparison of today’s statement and the October version. What should jump out is the brevity. It’s just over half the length. Part of that is because this was a non-MPR meeting. Part of it is because they don’t want to rock the boat.

I’ll go over some of the key takeaways from the statement next.

HERE COME THE YEAH, BUTS

My overall takeaway here is that the BoC bought time until it does a proper job at the end of January with more information. For now, they put on horse blinders and heavily faded developments in ways I think went too far. There are three main examples.

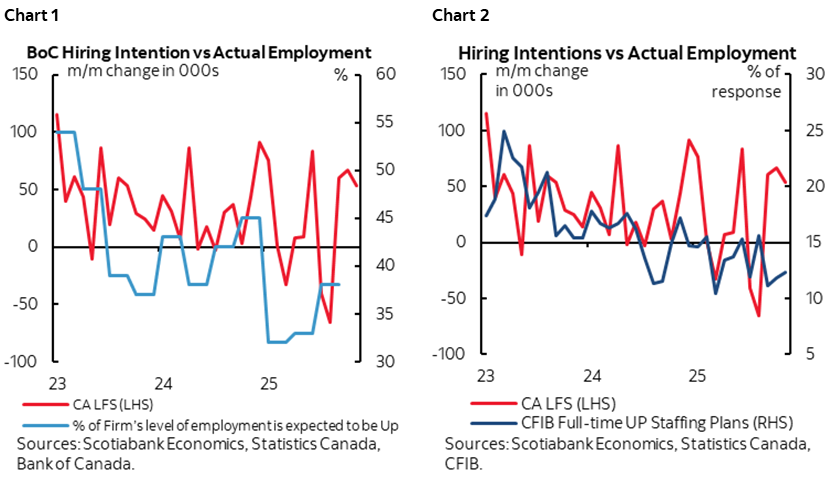

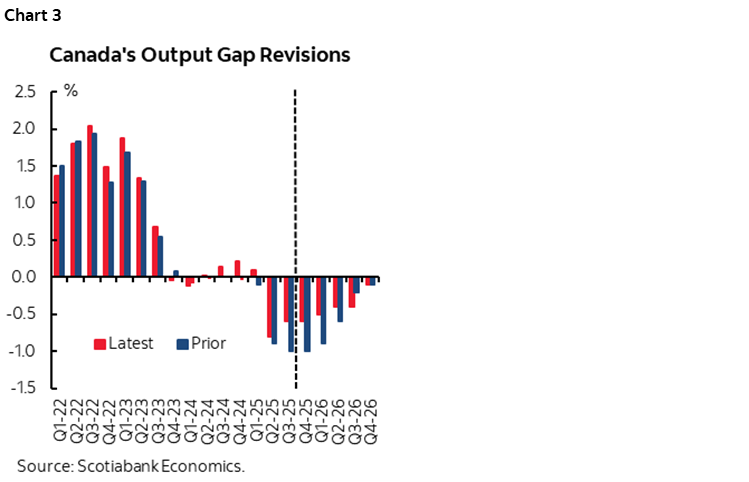

Jobs ripping? Yeah but look at the soft hiring intentions data was the message here. The counter to this stance from the BoC is that intentions data is largely useless as a guide to actual hiring decision so why emphasize it? Doing so is a vain attempt at ignoring the fact the job markets has blown away their expectations—and everyone else’s. Charts 1–2 show the BoC’s business survey measure of hiring intentions that has been bleak all year and the CFIB’s small business measure of hiring intentions that has been bleak since last year, versus the often high and generally robust trend in hiring figures.

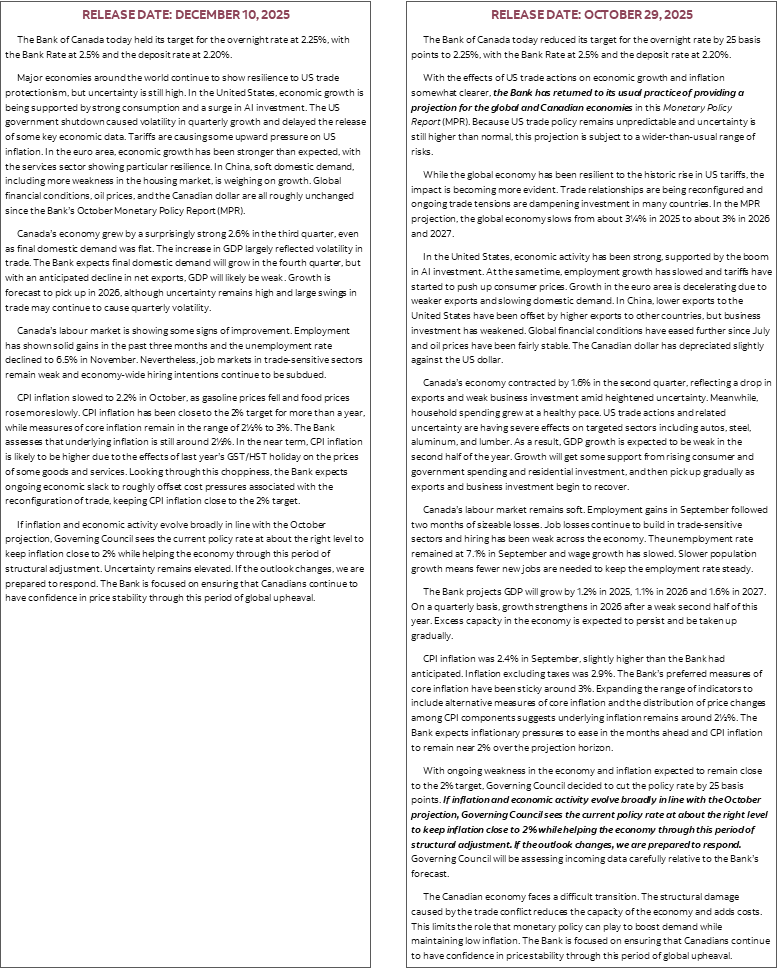

GDP revisions and impacts on slack? Yeah but we don't have any numbers for you now [of course they do] but we’re told they “roughly” balance out in supply and demand implications for the amount of slack. Define ‘roughly’ is my counter. We think the new data cut the estimated amount of slack in the economy ‘roughly’ in half as at Q3 compared to previously and did so by looking at the same set of numbers the BoC does (chart 3). From –1.1% to around –0.6% or so is reasonable. If the BoC is going to fade all of that by staying at –1.1% then I’d like to see their math while bearing in mind that they’ve (in my opinion) invoked some pretty arbitrary assumptions on potential GDP and hence the supply side in the past.

What about the fiscal policy effects on the outlook? Dunno, haven’t really estimated that, but there are supply and demand effects from the federal budget. Of course they’ve looked at the effects. But just wait until the next forecasts before the BoC unveils the estimated impact as they see it.

SO WHY'D THEY DO IT?

There are several possible reasons. One is that it’s somewhat prudent not to overreact to recent developments, and one example is that it’s highly unlikely that the job growth trend of the past three months is sustainable at such rates although it’s unclear if it just slows or sustainably craters.

On the flip side, I also worry about a central bank that fades or undermines them.

Two is that there are many uncertainties going forward and it's premature to rock the boat. That's not the same as saying that the street shouldn't rock the boat on these developments. And uncertainties can turn out better or worse as opposed to viewing them as meaning only bad outcomes. CUSMA, for instance, could go off the rails. Or the pattern to date to respect it outside of steel and aluminum and parts of autos (ie: most of the economy that is not in those sectors) could be a sign of action versus rhetoric in Washington. Tear it up into midterm when you’re already polling poorly? I’ll take the other side of that one.

In all, this was the expected denial report. Don't rock the boat, see you in seven weeks when we have full forecasts and some actual data on what’s going on in the US. But don't be lulled into putting on horse blinders yourselves.

MACKLEM PASSED ON AN OPPORTUNITY TO FADE HIKE PRICING

And yet, Governor Macklem was given a golden opportunity to lean against market pricing for rate hikes as soon as late next summer into Fall and he passed. Totally whiffed. Ninth inning, bases loaded, winning run at the plate, and whoooof.

See the exchange in Q#4 of the press conference recapped below. Macklem could be reasonably expected not to lean one way or the other that far out amidst the uncertainty. But if he had a strong opinion and wanted to control the path forward then he could have done so with a word or two and he did not.

He also noted that “so far, the economy is proving resilient overall” which is the same messaging you are hearing from the ECB, BoJ, Fed, and Antipodeans. These central bankers are herd bound and generally tend to move together.

PRESS CONFERENCE RECAP

What follows is an attempt at a recap of the Q&A portion of the press conference after Macklem was done reading his opening remarks. Any omissions or errors and to be blamed on my typing but I think it’s broadly representative of the discussion. A full official transcript would be helpful!

Q1. You are downplaying three strong job markets. How are you thinking about them?

10:42:35 A1. Hiring in services has been resilient. Overall employment has moved up. That is encouraging. There is some resilience in the economy. Looking forward, it hasn't fundamentally changed our view. The Canadian economy is going through a structural adjustment. Companies are cautious about their investment and hiring plans. Going forward we continue to expect fairly modest growth.

Q2. What is the source of this resilience?

A2. It's hard to give a super precise answer. We got revisions to 2022, 2023, 2024 that showed stronger consumption and investment and productivity growth was still weak but went from zero to about 0.5. Both demand and supply were stronger. The economy was stronger than expected and that may explain some of the resilience in the data. Secondly, there are steep tariffs on some sectors like steel, aluminum, but outside of those sectors if you are compliant with those sectors then Canada's average US tariff rate is one of the lowest in the world. We haven't seen big spillovers to the rest of the economy.

Q3. How did the federal budget and provincial updates impact your outlook?

A3. What you see in the budget is increases in government spending particularly on defence that will support demand. Targeted measures including those announced before the budget will support hard hit sectors to help them pivot to other exports and domestic sources of demand. There is also a lot of focus on investment. We're still working through the macroeconomic implications. It will take some time for the macroeconomic impact to show up in the economy. That will build up over time but it's not like there is a big hit right away. The impacts will depend importantly on the speed and success of execution and how the private reacts and we'll have to come up with some forecasts for these things. The budget will add demand and supply and is not adding a lot of additional inflationary pressures.

Q4. Are traders getting ahead of pricing hikes next year?

A4. I'm going to let traders decide what to price. We've been very clear. Given how we see things right now, we think the policy rate is about right. At the lower end of the neutral range it is providing a bit of support to help the economy work through. That's how we see things now. How we see things going forward is a more difficult question and I'm not going to put our policy on a timeline. Markets can expect our decisions on a meeting by meeting basis and as conditions evolve we will update our communications. We'll be assessing developments in relation to our outlook. If developments move in one way or the other to that outlook then we are prepared to respond.

Q5. In reference to data lags and US shutdowns, if you're not getting a full picture of growth until after the fact then how does this impact your ability to conduct policy?

A5. There are a number of important bits of data Statcan gets from the US like trade. With the shutdown, the data on exports is not as good as normal [ed nor imports] but yes in the fullness of time there is a prospect of larger than normal revisions when the data comes in.

Q6. The BoC speaks about inflation returning to target but Canadians focus on costs and prices. What do you say to Canadians about affordability?

A6. Generic political answer acknowledging many Canadians are impacted by affordability but it emphasizes the important of keeping inflation low so incomes can catch up. The other thing I would stress is we're not trying to push overall prices down as that would cause a recession.

Q7. Do you think there is less slack than you anticipated in October and do you see the output gap narrowing over your projection period?

A7. We don't have a new projection. The recent data is showing some improvement and that is welcome news. That has not changed our view the economy is still in excess supply and we continue to expect modest growth going forward. New revisions for the last 3 years showed GDP quite a bit higher because of both demand (consumption) and supply (investment) drivers. I would not interpret higher GDP as purely a signal of higher demand, there are both supply and demand drivers. Before we get to January MPR we'll have to evaluate more fully. Secondly, Q3 GDP was a lot stronger than expected which mechanically would narrow slack, but the details don't look like demand was stronger as final domestic demand was slack. We expect Q4 FDD to pick up while trade weakens. The resilience we're seeing in the economy has been welcome news but it hasn't changed our views because there is still excess supply and growth is still modest.

Q8. How may tariff shocks and threats influence you next year?

A8. Through spring and summer people were talking recession and we published scenarios in the mPR that could have pushed the economy into recession. The 'r' word people are talking about now is resilience. We're ending the year in a better place than it looked in the middle of the year. But there is still a significant adjustment to work through. We're going to be assessing the impact of the budget and new data in the next MPR.

Q9. You had estimated the TMX pipeline would add 0.25% to the economy. What could be the impact of another new pipeline?

A9. I'm not going to comment on the impact at this point. We do need to diversify our trade. The TMX pipeline has been an important example that has allowed us to increase our exports to non-US markets. It's not a huge shift but on the margin it's helping us get more oil to other countries. It's also helping us getting more value out of what we export because it has narrowed the WTI-WCS spread.

Q10. Are we many months away from the need to adjust the policy rate higher?

A10. I don't have much more to add. We think the policy rate is in the right place right now.

Q11. In 2024 you said Canadians can breathe a sigh of relief that inflation has come down. There is still high uncertainty and affordability concerns. What's your message into 2025?

A11. There is a feeling of uneasiness or uncertainty overhanging Canadians right now. Our focus is inflation to provide stability to an uncertain picture.

Q12. Is it the Bank's probability to warn people of the material probability of rates going up to ward off what's happened in the past on mortgage patterns?

A12. Our responsibility is to discuss the outlook and probabilities. We put that out because monetary policy has to be forward looking. We're going to be assessing that data in relation to our outlook. If you see the data before us then you know before we adjust that our views are likely to evolve. It's our job to be really clear about where we see the economy going and it's the job of mortgage advisers etc to advise clients.

Q13. Where do you see shelter costs and the final wave of mortgage renewals going?

A13. Overall activity looks better balanced but there are many regional markets. We don't expect another surge in house prices. We expect a continued correction in some higher priced markets. Both interest rates and supply conditions are helping to improve affordability but there is a structural issue on the supply side.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.