- Mexico: Headline inflation slows in January; core hits highest level since 2001

- Peru: A new Cabinet—again; mining output down in December but up for 2021

MEXICO: HEADLINE INFLATION SLOWS IN JANUARY; CORE HITS HIGHEST LEVEL SINCE 2001

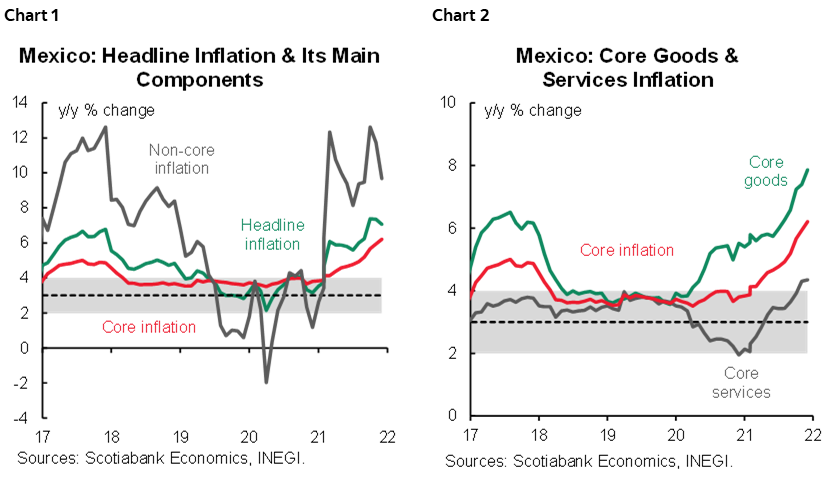

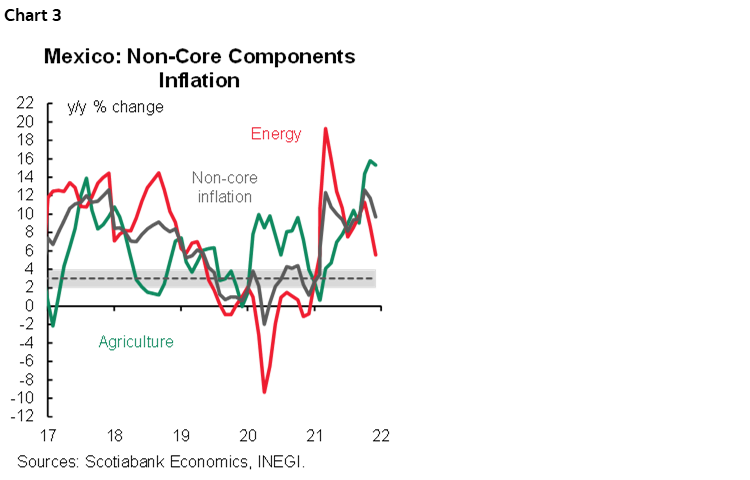

According to INEGI, headline inflation was 7.07% y/y in January, slightly above market expectations (7.01%y/y consensus) and down from last month’s 7.36% y/y (chart 1). Core inflation continued its upward trend, however, rising to 6.21% y/y (from 5.94% y/y a month earlier), the highest rate since October 2001 (chart 2).

Goods prices led January’s inflation, increasing from 7.40% y/y to 7.86% y/y, while services went from 4.30% y/y to 4.35% y/y.

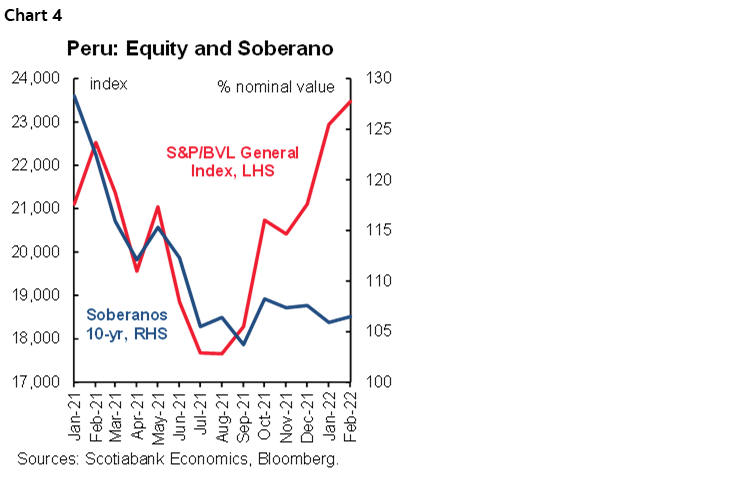

Non-core inflation moderated from 11.74% y/y to 9.68% y/y, as energy price inflation moderated (11.50% y/y versus 6.75% y/y last month) along with fruits and vegetables (21.73% y/y versus 18.44% y/y last month) (chart 3).

On a monthly basis, headline inflation rose from 0.36% m/m to 0.59% m/m (consensus 0.55% m/m). Core inflation moderated from 0.80% m/m to 0.62% m/m (consensus 0.55% m/m), with an increase from 0.91% m/m to 0.99% m/m in goods prices more than offset by a decrease in services from 0.68% m/m to 0.19% m/m. Non-core items rebounded from -0.90% m/m to 0.52% m/m, with increments in energy and government tariffs (-1.56% m/m to 0.83% m/m) and agriculture and livestock (-0.08% m/m to 0.14% m/m). Significant increases were recorded in the price of lemons (68.77% m/m), potatoes and other tubers (15.49% m/m), and bananas (12.07% m/m).

Given the price dynamics observed in January, market participants’ upward revisions to expectations for 2022 (please see our comment on Banxico’s expectations survey), and signs of persistence, we reaffirm our call for a 50 basis point hike by Banxico on February 10. The market will be watching the new Governor Rodriguez Ceja’s stance and assessing the tone of the statement with respect to inflationary pressures, growth, and the monetary stance relative to other countries.

—Luisa Valle & Miguel Saldaña

PERU: A NEW CABINET—AGAIN; MINING OUTPUT DOWN IN DECEMBER BUT UP FOR 2021

I. President Castillo appoints his fourth Cabinet

President Castillo appointed his fourth Cabinet in seven months, chaired by Anibal Torres, Minister of Justice of the previous Cabinet. Torres was part of the legal team that pursued allegations of electoral fraud against Fujimori and has been in favour of calling a referendum to change the constitution. As a minister, he has had confrontational relationships with his political opponents, so his appointment as Prime Minister was not expected and could result in continuing frictions with the Congress, which after four Cabinets seems to be the one constant of the Castillo Administration.

Although his nomination is likely to secure the required vote of confidence by Congress, it is not certain. Several members of Congress have already questioned the appointment of some ministers. In total, 12 of the 18 ministers that make up the ministerial Cabinet were ratified, with new ministers in the portfolios of Health, Environment, Justice, Energy and Mining, Agrarian Development and Women.

Another sign of friction is the replacement of ministers identified with the moderate left-wing by a greater presence of Peru Libre party in the cabinet, especially the appointment of Carlos Palacios as Minister of Energy and Mining. Palacios is a member of the Peru Libre party and oversaw the Mining Director of the Regional Government of Junin, a bastion of the Peru Libre party. President Castillo also kept Juan Silva as Minister of Transportation and Communications, with responsibilities for around 50% of the national government’s public investment budget, who had been questioned for lack of experience in public administration that could affect the pace and quality of project execution.

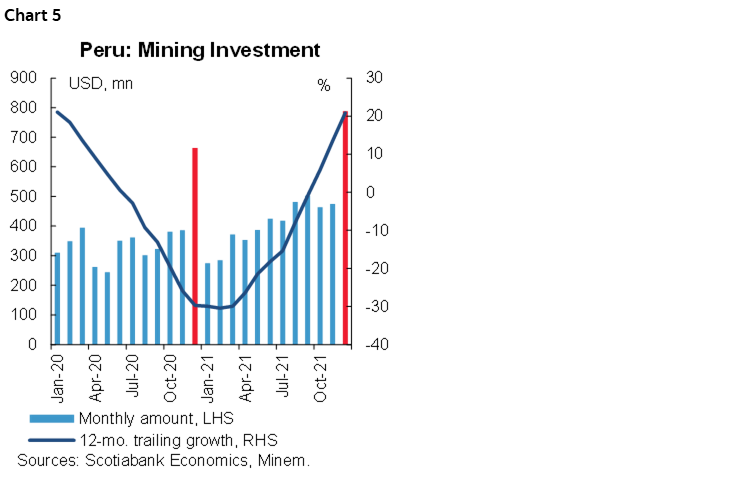

A key positive is that Oscar Graham continues as Minister of Finance. In this regard, the market reaction has been favourable, with a rise in the stock market (+1.3%, +12.6% YTD), PEN appreciation (+0.7%, +4.8% YTD), lower global bond yields (-2 bps, +43 bps YTD at 10Y), sovereign bonds (-2 bps, +19 bps YTD at 10y) and CDS (-2 bps, +14 bps YTD at 5y) (chart 4).

The new Cabinet has the challenge of calming the tense political environment and will have to deal with an agenda that includes an environmental emergency resulting from a massive oil spill, improving citizen security, continuing the vaccination program, and providing a business environment that stimulates private investment.

—Mario Guerrero

II. Mining data fell in December 2021

In a context of high global metal prices, Peru’s mining output was adversely affected by stoppages and blockades in December 2021, while year-over-year output comparisons reflect base effects. Copper production fell 5.5% y/y in December, with Minera Las Bambas reducing its production by two-thirds owing to a 12-day stoppage due to blockades by the communities. Other mining companies also reduced output, including Southern Peru (-13.2%), Chinalco (-5.3%) and Antapaccay (-11.4%). Production increased at Antamina (+6.4%), Cerro Verde (+5.9%), Hudbay (+15.1%) and El Brocal (+61.0%). Zinc production fell 5.4% y/y in December due to lower production at Antamina (-27.9%), Nexa Perú (-40.8%), Minera Los Quenuales (-77.3%) and Minera Shouxin (-52.3%). Gold production decreased 5.4% y/y in December, remaining below pre-pandemic levels owing to mine depletion, while silver production increased 1.2% y/y.

Mining output ended 2021 in positive territory on the year, however, reflecting the low base for comparison in 2020 in the wake of pandemic-related closures. Economic recovery together with the rebound in metal prices—many reaching record highs—stimulated mining output in 2021. Output increased year-on-year with respect to copper (+6.9%), gold (+9.7%), zinc (+14.8%), silver (+21.5%), lead (+9.3%), iron (+36.6%), tin (+ 30.7%) and molybdenum (+6.1%).

Mining investment increased 18.7% y/y in December, according to official data (chart 5). Investment was driven by Anglo American’s Quellaveco project and the Toromocho expansion project, which are 80% and 66% complete, respectively, with both projects expected to be completed in 2022. By category, investment was driven by “exploration” (+75.7% y/y), as companies increased exploration investment in response to high metals prices, “mining equipment” (+65.1% y/y), “development and preparation” (+53.4% y/y) and “infrastructure” (+42.6% y/y). For the year, investment increased 21.1% in 2021, still below 2019 levels (table 1).

—Katherine Salazar

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.