- Accurately predicting recessions is notoriously difficult. In part, this reflects an ongoing debate over whether most expansions “die of old age,” or prematurely end because of excessively aggressive monetary tightening by central banks concerned with rising inflation.

- There is evidence that Latam recoveries are morphing into expansions, as output returns to pre-pandemic levels. And while there is little reason to think that nascent expansions are at risk of dying of old age, the risks of recession may be rising.

- But if the expansions are at risk of an untimely demise, the blame, arguably, should be put on central banks in the advanced countries, not their Latam peers.

There is an ongoing debate in economics whether expansions “die of old age” or are “murdered,” as former Fed Chair Ben Bernanke once quipped. The debate revolves around the factors that transform economic expansion into recession—the effects of excessive debt accumulation and highly levered household and business balance sheets, coupled with increased risk-taking, on the one hand, or excessively aggressive monetary tightening by central banks that overshoot policy settings as they struggle to contain inflation, on the other hand. In a week that saw the Federal Reserve hike its key policy rate 50 basis points and bring forward plans to shrink the size of its balance sheet in a double-barrelled barrage to reduce inflation, the debate is of interest for more than merely theoretical reasons.

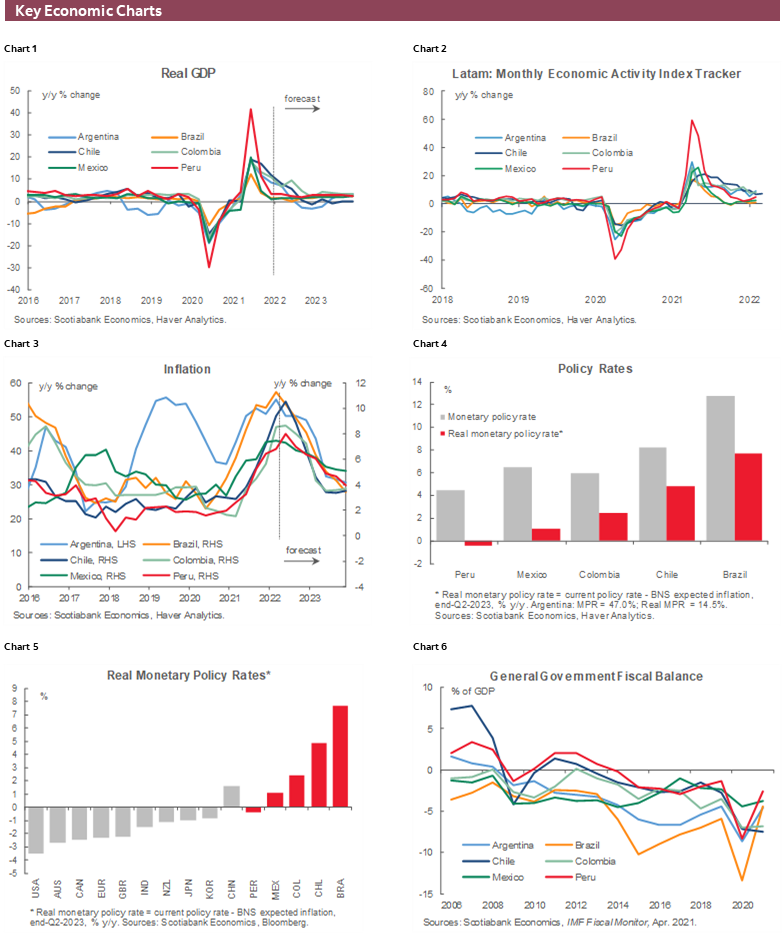

For the avoidance of doubt, there are few, if any, grounds to conclude that the economic expansions underway across the Latam region are at immediate risk of dying of old age. After all, it is just over two years since the pandemic shock, when activity seized up as public health mandates to restrict the spread of the virus were put in place. And while output has returned to its pre-pandemic level in most Latam countries, reaching that milestone can hardly be considered an indication of geriatric expansion. The fact that employment has generally lagged the recovery of output, with employment still below pre-pandemic levels, should dispel that contention.

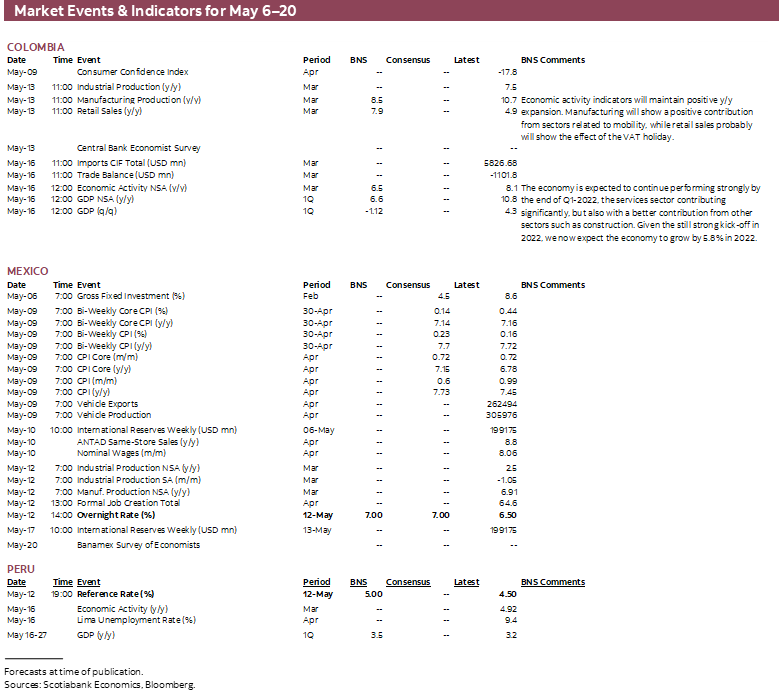

But there are signs that recoveries across the region are maturing. Strong growth in 2021 reflected the “dead cat bounce” from pandemic-induced contractions in 2020: given low bases for comparison, the re-opening of economies, as mobility restrictions were relaxed, was bound to generate high growth rates. These adolescent growth spurts are making way for slower growth, a characteristic of more mature expansions. For instance, Scotiabank’s team in Santiago notes that, while Chile’s monthly GDP data for March came in above market expectations at 7.2% y/y, the q/q contraction reflects convergence towards trend GDP. Similarly, our experts in Lima have pointed out that, with m/m growth flat, February GDP growth of 4.9% y/y may not be as strong as it appears. In Mexico, Scotiabank’s team recently highlighted the results of Banxico’s expectations survey, which shows slightly weaker growth (and higher inflation). The message here is that slowing growth does not necessarily presage issues of grave concern, even if there is a possibility, as in Chile, of a mild technical recession, as growth transitions to a more sustainable rate. Meanwhile, Colombia has closed the output gap between potential output and actual output, completing the transition from recovery to expansion.

Signs of maturing recovery are also found in labour markets across the region. In Peru, for example, employment stagnated in March while the three-month moving average unemployment rate for Lima increased again. Likewise, Chile’s unemployment rate for the first quarter of 2022 increased as labour force growth outpaced job gains. And in Colombia, employment contracted on a seasonally-adjusted basis in March. Yet, despite these setbacks, there are positive signals coming from labour markets. Most important is the evolving composition of job gains, as formal jobs continue to increase while informal jobs decrease and gaps between male and female participation rates close.

In short, recent labour market trends may be consistent with sustained expansion. This is because early in a recovery firms may be uncertain about the durability of the expansion—particularly so with the threat of another COVID-19 wave looming over the outlook. In such circumstances, they are more likely to meet demand by re-employing less-skilled contingent workers who can easily be laid off if the recovery proves false. More formal employment, which typically involves skilled workers, entails higher costs of both hiring (to ensure the right job-skills match) and firing (separation payments).

At some point, however, as recovery becomes expansion, productivity and profitability can be enhanced by retaining more skilled workers. Moreover, unskilled workers can morph into skilled workers as they gain firm-specific human capital and move up the firm’s internal labour market promotion ladder. In this perspective, stagnating employment reflecting higher formal job creation that fails to keep pace with the loss of informal jobs could be a favourable development if it reflects these human capital investments.

In normal circumstances, recent developments would be unlikely to raise alarms that an expansion is nearing its expected lifespan—except current circumstances are anything but normal. As noted in the last edition of the Latam Weekly, we are emerging from a once-in-a-century pandemic while fighting the economic collateral damage from Russia’s war on Ukraine.

These twin gales of economic destruction have propagated a series of supply-side and commodity price shocks that have pushed global inflation higher, well above central banks’ inflation targets. These price pressures do not ineluctably imply we are on the cusp of a new age of inflation. However, they do challenge central bank price stability commitments and threaten to unleash expectations of inflation going forward. Central banks must therefore act with determined resolve to keep expectations well anchored; in this respect, the current conjuncture undoubtedly explains the Fed’s more hawkish stance compared to just a few weeks ago.

The danger now is central banks having to move more aggressively to avoid expectations becoming unmoored. And given the uncertainty that pervades the outlook, such a response entails an increased risk of overshooting, as central banks mis-calibrate the degree of restraint required to achieve the fine balance needed to both anchor expectations and support sustained growth. Inflation that erodes purchasing power through the real balance effect is one source of possible miscalibration.

Moreover, it might be the case that the only way to return inflation expectations to central banks’ target range is through a deliberate effort to choke demand to such an extent that excess supply puts downward pressure on prices and thus expected inflation. It is inconceivable this could be achieved without a recession or, equivalently, a sustained period of below-potential growth.

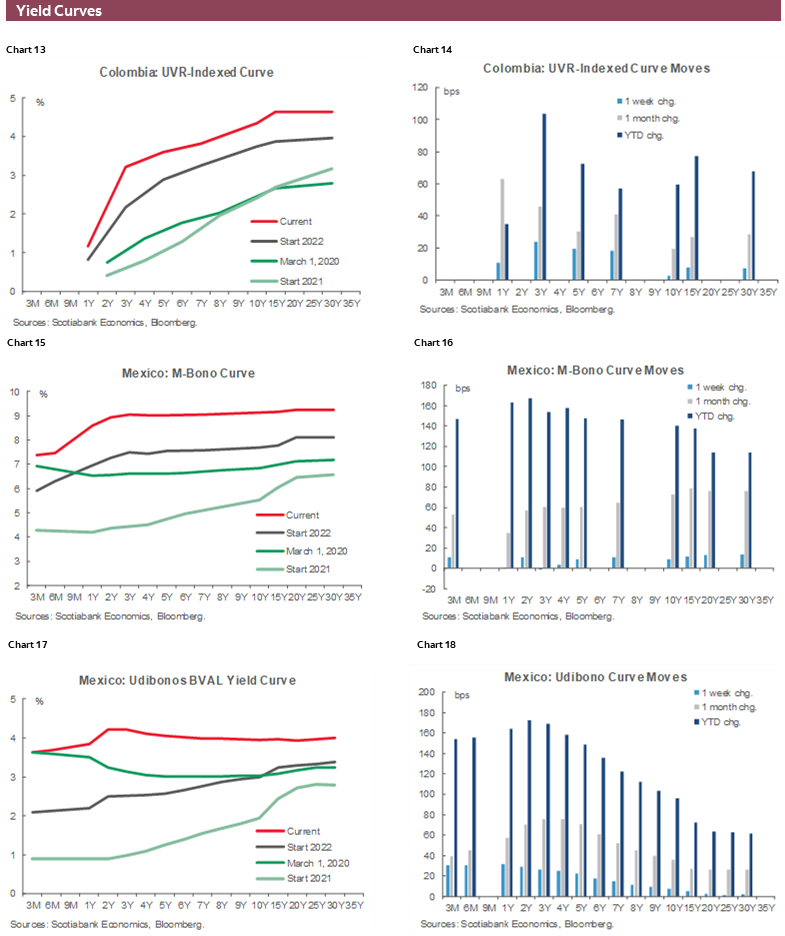

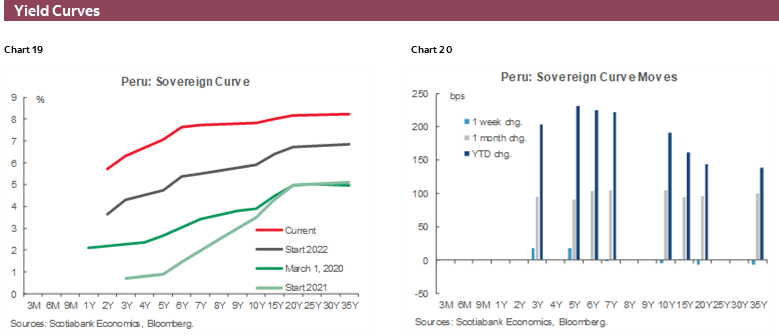

The inescapable conclusion is that, while the risk of economic expansions dying from old age seems remote, the possibility of an unnatural death is rising. But if expansions in the Latam region are murdered, to use Bernanke’s phrase, it may not be local central banks, which have been proactively rebalancing monetary conditions over the past year, that are culpable. In just the last week, Colombia’s BanRep raised its reference rate 100 bps in a more hawkish split vote while Chile's BCCh hiked its policy rate 125 bps today in a unanimous decision. Scotiabank economists across the region expect additional increases in the weeks ahead.

Rather than Latam central banks, those responsible for the potential untimely and premature death of economic expansions around the globe may well be advanced country central banks that failed to act with comparable prescience, temporizing with growing inflationary pressures, and those whose war to overturn the international order unleashed a gale of higher commodity prices.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.