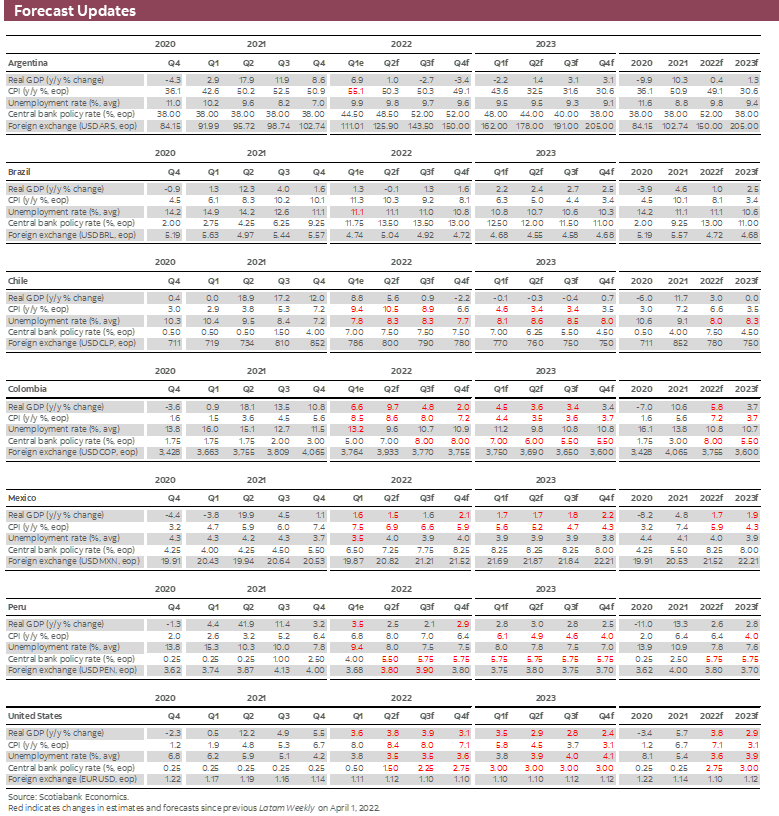

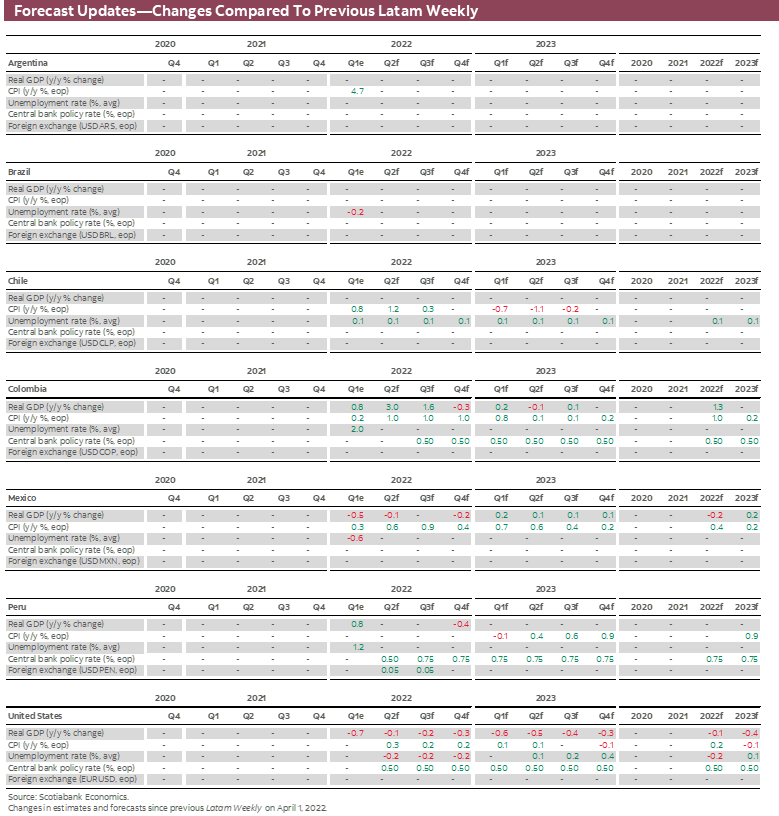

FORECAST UPDATES

- Higher commodity prices resulting from Russia’s war on Ukraine have fueled global inflation and led to increased volatility in financial markets. With inflationary pressures threatening price stability commitments, Latam central banks have accelerated policy tightening with implications for growth. See the latest forecast revisions made by Scotiabank’s economists in the region in the table below.

ECONOMIC OVERVIEW

- The war on Ukraine has also unleashed a gale of destruction, measured both in terms of lives lost and economic losses. Moreover, there is a risk—admittedly undefined—that the global trading system could become collateral damage.

- Coming in the wake of the economic dislocation caused by the global COVID-19 pandemic, which has led to severe supply side shocks, Russia’s war could trigger a shift in global trade patterns as sanctions, counter sanctions, and secondary sanctions animate a geopolitical bifurcation of world trade.

- For the Latam region, the potential consequences of this scenario could be enormous. Sound policy is needed to transform a storm of dislocation into a gale of creative destruction.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico, and Peru.

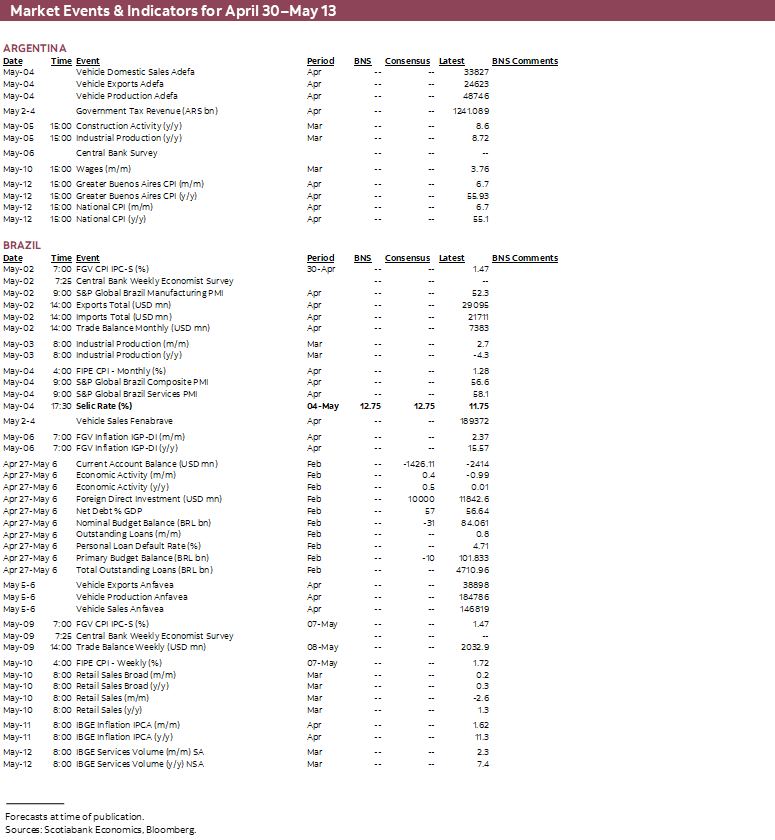

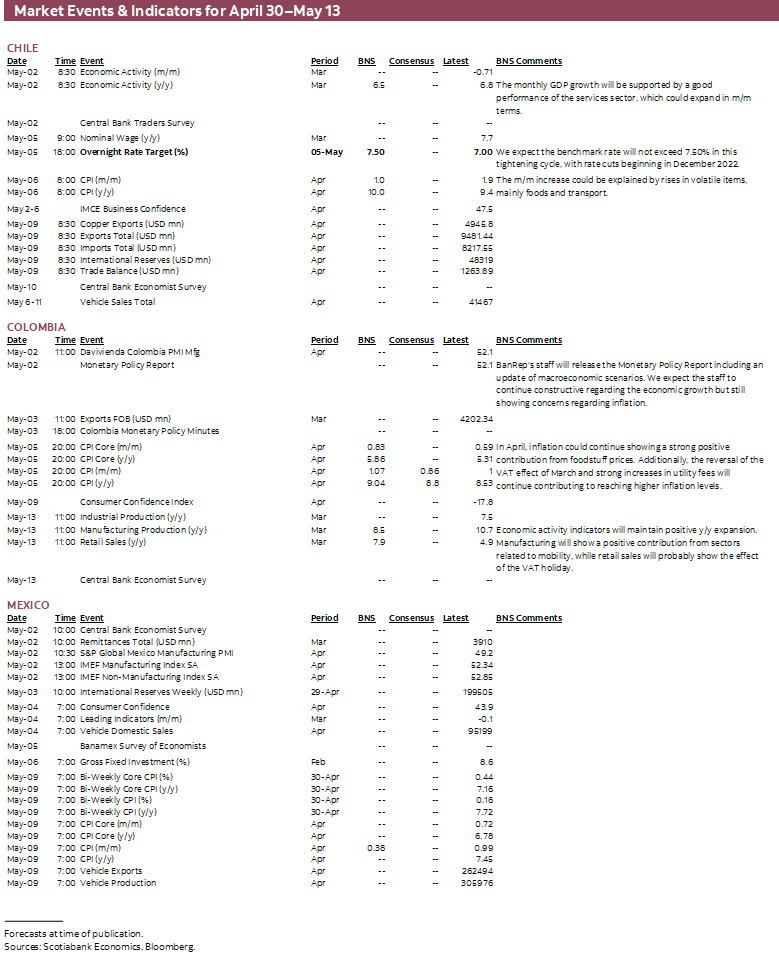

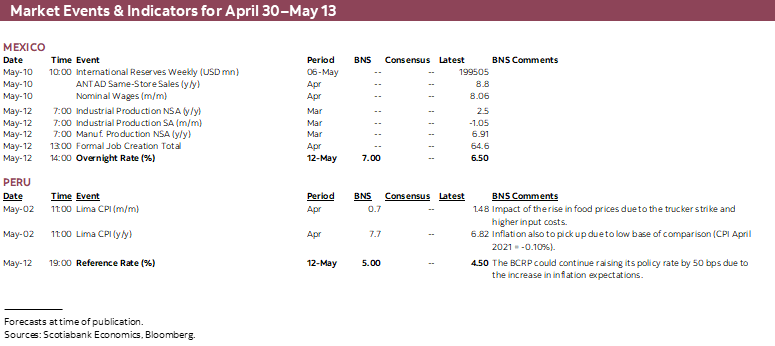

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period April 30–May 13 across the Pacific Alliance countries, plus their regional neighbours Argentina and Brazil.

Economic Overview: Gales of Creative Destruction?

James Haley, Special Advisor

416.607.0058

Scotiabank Economics

jim.haley@scotiabank.com

- The longer that Russia’s war on Ukraine continues, the greater the risk that the global trading system becomes collateral damage as sanctions, counter sanctions, and secondary sanctions lead to a geopolitical bifurcation of trade.

- This effect would come on top of pandemic-induced supply chain disruptions that may lead firms to reconsider the highly-disarticulated supply chains that have figured so prominently in global production.

- The Latam region has seen a huge shift in trade patterns over the past 30 years with the progressive integration of China into the global economy. Large changes to trade patterns, however uncertain, could entail considerable dislocation. Policies that expand trade infrastructure and remove distortions to intra-regional trade would protect the region from the gales of war.

GLOBAL TRADE AS COLLATERAL DAMAGE

Economic ideas are often adopted, amended and, sometimes, distorted to fit a particular narrative. The notion of “creative destruction” is one such idea. Simply put, this is the proposition advanced by the late Joseph Schumpeter that, in market economies, the economic disruption associated with restructuring inevitably leads to the more efficient use of resources, higher productivity, and (by definition) an increase in output. He coined the phrase “gales of creative destruction” to describe the beneficial process by which product and process innovation leads new firms to replace outdated ones. The process can be likened to windstorms that clear out the deadwood in the economic forest, making way for new growth.

Over the past two years, the global economy has been subjected to a (hopefully) once-in-a-century gale, as a global pandemic spread from country to country. The disruption wrought by COVID-19 is measured in the lives lost and those disrupted, the output forgone, and the loss of “relationship capital”—the value of idiosyncratic firm-specific human capital, as workers are separated from their employers, and firms’ relationships with suppliers and customers are disrupted. Moreover, the effects of the pandemic are long-lasting as supply chain disruptions propagate persistently higher inflation.

Russia’s invasion of Ukraine, now in its third month, has unleashed another destructive storm. Commodity prices have spiked higher, fueling inflationary pressures already primed by pandemic. And the spectre of widespread food shortages looms menacingly over the global economy, as Ukrainian agricultural exports are blocked, and Russia threatens to use food as a strategic weapon. Should the Kremlin follow through on its threats, the costs would fall disproportionately on the world’s poorest, likely resulting in an uptick in sovereign debt defaults that would send a temper through global financial markets. As Scotiabank’s team in Bogota note below (see Country Update), financial markets have already been subjected to heightened volatility because of rising geopolitical tensions.

In this respect, while the economic and human destruction resulting from these gales is readily apparent, it is far from clear that they represent a creative process. Far from it.

The process of restructuring that Schumpeter had in mind when developing his thesis is most aptly thought of in terms of technological innovation that gives one firm a competitive advantage over its rivals. The innovator can’t exploit its advantage, however, if it is unable to secure the resources—the labour, working capital, and inputs—needed to expand production. That won’t happen if existing firms continue to produce, hoarding these resources. The clear implication is that incumbent firms using the now outdated technology must fail to create the space for more efficient production process. Innovating firms drive incumbents from the market by reducing prices, benefiting consumers. This is the basis of the “creative” destruction hypothesis.

There is nothing about the dislocation of the pandemic or the wholly unwarranted destruction of Russia’s war that is remotely creative. But that likely won’t stop some from misappropriating the concept.

True, the Latam region could benefit from the positive terms-of-trade shock that higher commodity prices offer. Since the start of 2022, Latam currencies have generally outperformed emerging peers by holding their own, or even appreciating, against a surging US dollar. That performance partly reflects the expectation of a positive terms-of-trade shock from higher commodity prices. But these benefits can be fickle, as recent volatility from a pull-back in global commodity prices illustrates. And those terms-of-trade benefits could prove illusionary if high commodity prices push the global economy into recession, destroying external demand. We are far from that point. Yet, as noted in the last edition of the Latam Charts, the IMF has alerted its members to this risk.

Against those uncertain and possibly transitory benefits, is a far greater potential cost to the Latam region from the destructive gales still buffeting the global economy. This is the possible decoupling of economies from the global trading system, as companies rethink global supply chains, and the bifurcation of the globe on ideological or pragmatic grounds. Some “re-shoring” of supply is likely both inevitable and warranted—to the extent that the ever-finer division of production (labour) into ever-more-granulized components was based on the untested assumption that supply disruptions are unlikely. (The paradox here is that the finer the specialization of input sourcing, requiring idiosyncratic investments in production process, the greater the costs of any disruptions that do occur from the absence of alternative sources from which to secure critical inputs.)

The effects of this supply-chain “re-think” are likely to be limited and, admittedly, could provide opportunities for domestic firms that forge missing links in re-shored supply chains. Though some firms stand to gain in this scenario, these gains do not necessarily lead to generalized benefits; as such, it does not constitute “creative” destruction.

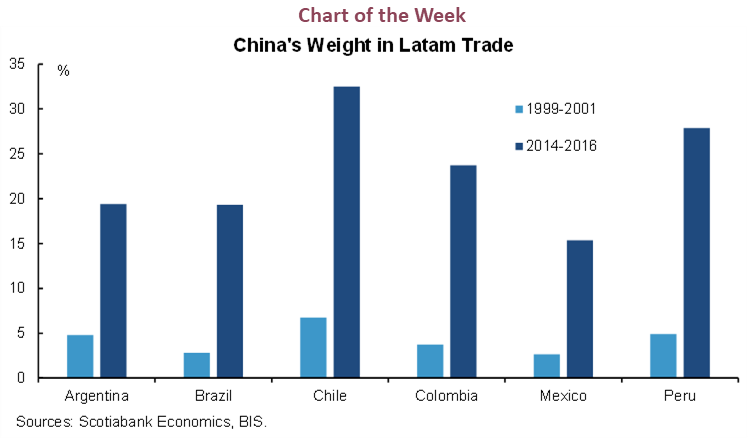

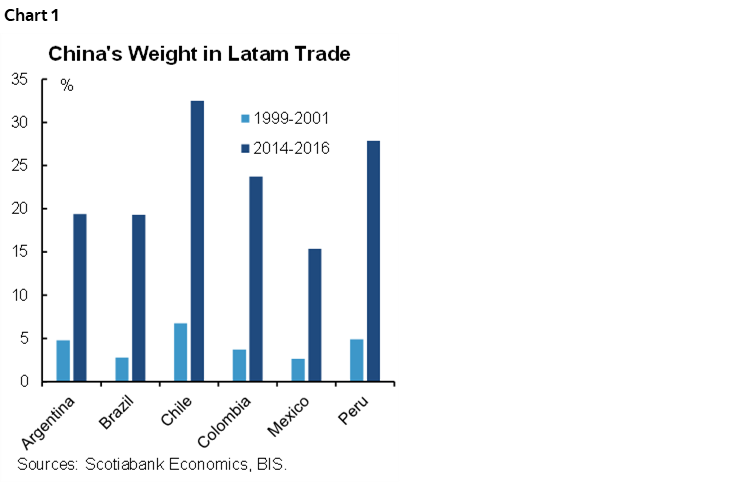

Far more worrisome is the potential for a major realignment of global trading patterns because of geopolitical factors. It is not an exaggeration to say that the integration of China into the global economy has led to a revolution in international trade. This is certainly the case with respect to the Latam region. Arguably, no region has been more affected. Over the past three decades, the share of China in the region’s trade weights (as calculated by the BIS) has risen dramatically (chart 1). China now represents a major buyer of the region’s natural resources, an important source of finance to develop and exploit these resources, and supplier of consumer goods.

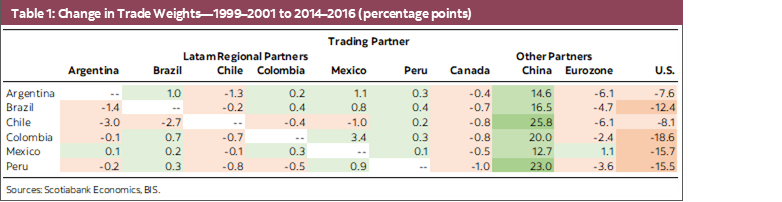

Breaking down the shifts in trade weights (table 1) yields two noteworthy observations. The first, clearly, is that China’s increased weight as a regional trade player has come at the expense of traditional partners, especially the US. Canada’s share in the region’s trade weights has likewise fallen, though these declines may have been limited by free trade agreements with the Pacific Alliance countries.

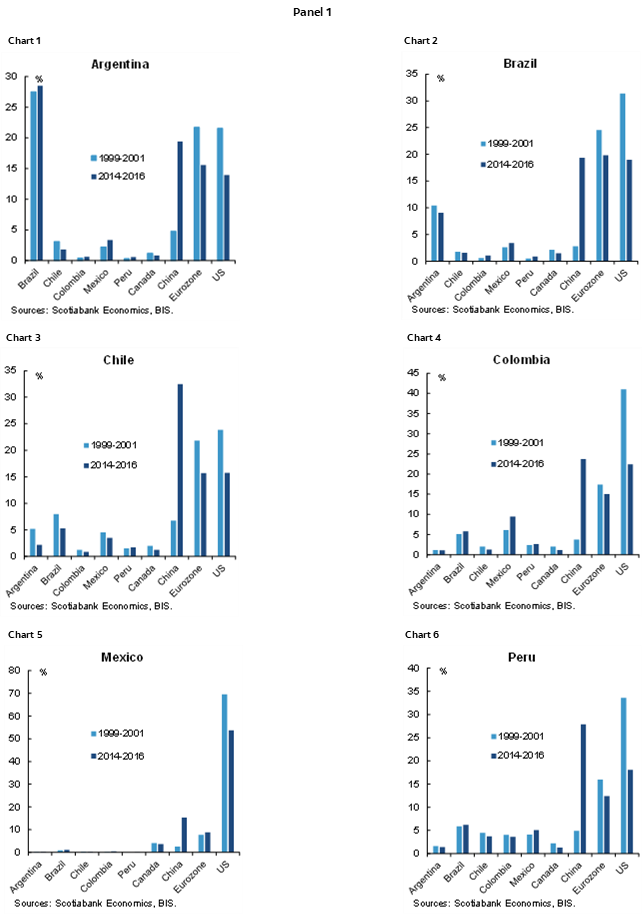

The second observation concerns intra-regional trade. It is a long-standing “stylized fact” that Latam countries trade more with countries outside the region than with their regional partners. This is illustrated by the various individual country trade weights (panel 1). The relative unimportance of intra-regional trade stands out. Moreover, with some exceptions, intra-regional trade weights have fallen over time.

Now, to be sure, there are good reasons for the low trade weights between Latam countries. Two countries with similar proportional endowments of capital, labour, and natural resources would have similar factor price ratios and thus export similar products under the Hechsher-Ohlin hypothesis. And two countries sharing access to similar technologies would likewise have identical Ricardian comparative advantages. In both cases, countries might be expected to trade more with third parties than between with each other.

But those “traditional” trade theories have been eclipsed by “new” approaches—though this description is somewhat misleading given that they were developed 30 or more years ago—based on product differentiation, imperfect competition, and increasing returns to scale. In this respect, geographic barriers that raise transportation costs and policy barriers also likely play a role in stifling intra-regional trade. The good news is that geographic barriers can be assuaged by infrastructure investments that both reduce production costs and link neighbouring countries, leading to higher trade and better jobs. And policies that artificially distort trade flows to create opportunities for domestic firms, but which end up protecting inefficient incumbents with higher costs to consumers, thereby thwarting the process of creative destruction Schumpeter described, can be changed.

Making the necessary investments and changing policies to facilitate greater regional integration would not be easy; it would take political capital. However, the longer the war in Ukraine continues, the greater the likelihood that the global trading system could become collateral damage as sanctions, counter sanctions, and secondary sanctions lead to an increasingly fragmented world. This could entail considerable dislocation for the Latam region. In such circumstances, the option of inaction becomes increasingly costly. In contrast, responding to challenges is the hallmark of leadership and is critical to crafting creative opportunities from destruction.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—High Inflation Leads the Government to Support Households with Targeted Fiscal Transfers

Jorge Selaive, Head Economist, Chile

+56.2.2619.5435 (Chile)

jorge.selaive@scotiabank.cl

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

Waldo Riveras, Senior Economist

+56.2.2619.5465 (Chile)

waldo.riveras@scotiabank.cl

GOVERNMENT UPDATES “STEP BY STEP” PLAN

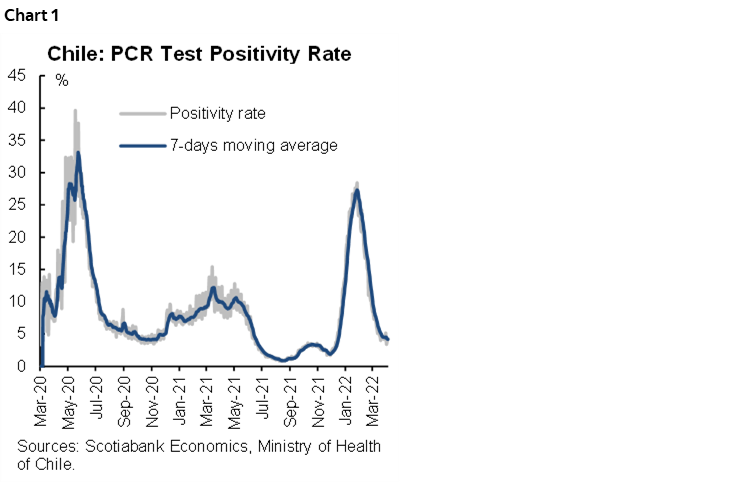

The daily number of confirmed COVID-19 cases has continued to slow in recent weeks. The test positivity rate fell to 4.3% (chart 1). Occupancy rates of ICU beds and COVID-19-related death rates are also decreasing. Meanwhile, the vaccination campaign has reached 94.4% of the eligible population. The rollout of booster (third) doses continues—reaching 13.9 million people—and the new booster dose (fourth) is in progress—with 3.1 million people covered. Overall, mobility has continued to increase in April, which will support the economic activity, mainly services.

In light of these figures, the government announced changes in the “step by step” plan, considering three types of health impact phases: low, medium and high. In addition, restrictions on the opening of borders have been relaxed. The new plan started on April 14.

CENTRAL BANK COULD MOVE FASTER AFTER UPWARD SURPRISE IN MARCH INFLATION

On Friday, April 8, the statistical agency (INE) released the March CPI, which surprised upward both market expectations and ours. The CPI increased 1.9% m/m (9.4% y/y), reflecting a general increase in prices across volatile items, such as food and energy as well as at the core level.

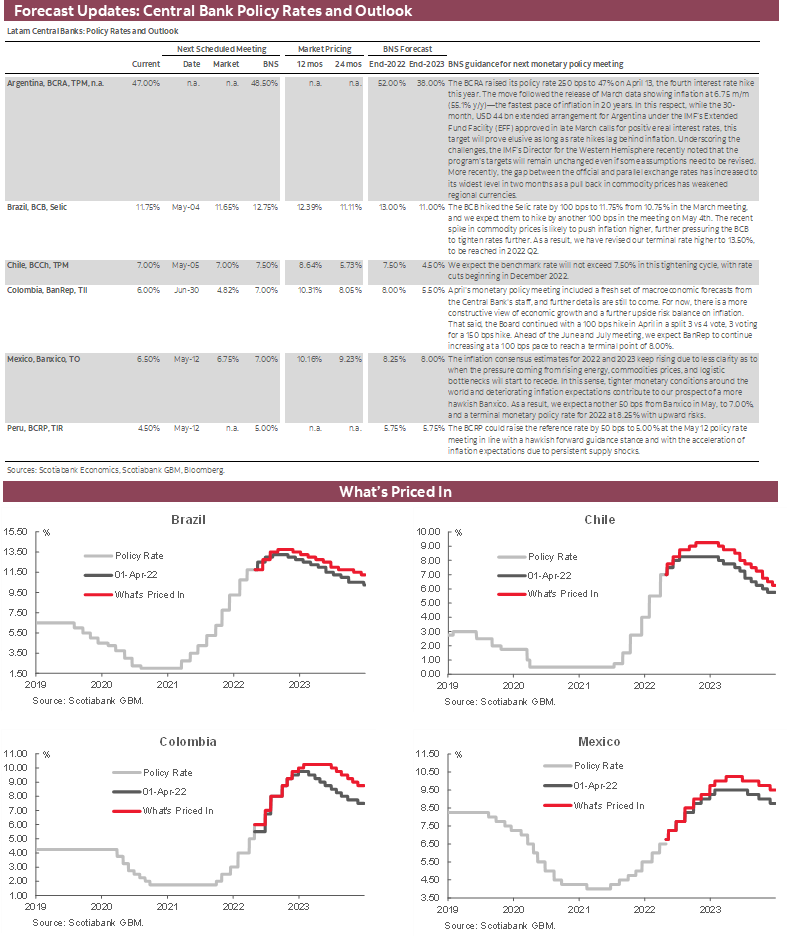

The March outcome, which we consider may be a “one-off” surprise to the central bank’s baseline scenario, could motivate the BCCh to accelerate the pace at which it moves the monetary policy rate to the centre of its desired policy rate corridor. This would allow the BCCh to wait for more information and possible changes to its forward guidance at the June meeting.

Accordingly, we have revised up our expectation of the monetary policy rate hike in May, from 25 bps to 50 bps. At the same time, we now consider the March Monetary Policy Report projection of annual inflation of 5.6% out of range, while our forecast of 6.6% is more likely.

HIGHER UNEMPLOYMENT RATE REFLECTS LABOUR FORCE GROWTH

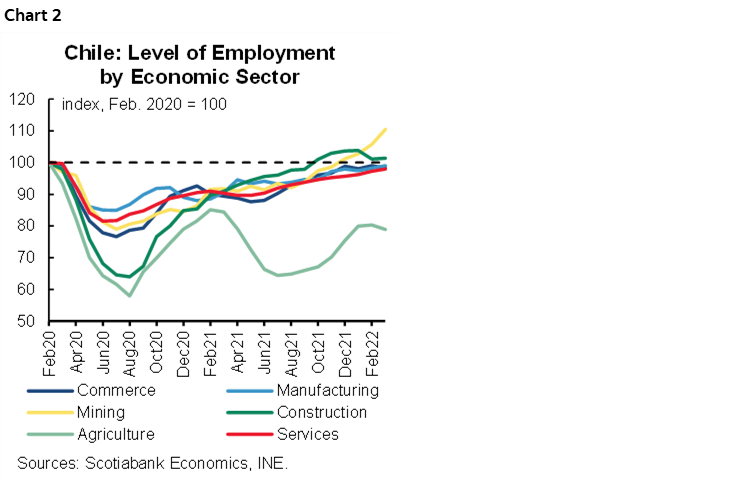

Meanwhile, on Thursday April 28, the statistical agency (INE) released the unemployment rate for the quarter ending in March, which rose to 7.8% again owing to higher labour force growth (0.7% m/m) as compared to that of employment (0.3% m/m). The increase in the unemployment rate in recent months is explained by the re-incorporation of men and women into the labour market at a rate that has outstripped job growth. Specifically, employment in services continues to grow (chart 2), which should support to economic activity going forward. In this sense, we do not think that there has been a deterioration in the labour market, since the low unemployment rate in the second half of last year reflected the obstacles to labour market participation posed by health restrictions as well as transfers and pension withdrawals.

GOVERNMENT SUPPORTS HOUSEHOLDS AFFECTED BY INFLATION

In the political arena, the government announced that will provide direct fiscal transfers between May and December 2022 to protect households against recent inflation. Fiscal transfers will be equivalent to the increase in the value of the basic basket of foods over the last 12 months. At the same time, the Ministry of Finance also announced that it will present a bill to Congress for a 14% increase in the minimum monthly wage, from CLP 350,000 (USD 414) to CLP 400,000 (USD 473), starting in August. It should be noted that this announcement was already incorporated in the baseline scenario of the central bank, with only a limited impact on inflation.

Overall, the fiscal cost of both measures is estimated in USD 850 mn and will not entail further sovereign debt issuance or affect the fiscal deficit as it will be financed with resources coming from the existing emergency transitory fund.

A LOOK AHEAD

Lastly, in the fortnight ahead, central bank will release the monthly GDP growth (Imacec) of March, on Monday May 2, and will hold its monetary policy meeting, on Thursday May 5. For its part, INE will publish the April’s CPI on Friday, May 6.

Colombia—Resilience in an Uncertain Environment

Sergio Olarte, Head Economist, Colombia

+57.1.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Maria Mejía, Economist

+57.1.745.6300 (Colombia)

maria1.mejia@scotiabankcolpatria.com

Jackeline Piraján, Senior Economist

+57.1.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

This year has been a roller-coaster for markets around the world; volatility is all that markets talk about. A range of shocks have shifted international risk appetite and expectations of growth. Higher and more persistent worldwide inflation has triggered more hawkish central banks responses, while the Russia-Ukraine war and China’s zero-COVID-19 policy have led markets to consider the possibility of a stagflation-type event. The news has not been all bad, however. Higher commodity prices have helped Pacific Alliance countries to maintain positive momentum in the real sector. Nevertheless, the economic and financial environment remains uncertain. Colombia, for instance, has seen an increase of around 180 bps along the yield curve owing to higher international and domestic rates in a very volatile environment, while the COP has fluctuated almost 10% in the year-to-date (ranging between USDCOP 4,080 and USDCOP 3,707) under a risk-off environment, even while benefiting from higher-than-expected oil prices.

The real sector is a very different story. Economic activity has shown considerable resilience in the face of the inflationary shock and heightened market volatility. In fact, economic activity has grown an impressive 7.9% y/y through February, while leading indicators for March, such as energy demand and tax collections, suggest that GDP increased more than 6% in Q1-2022. In 2021, the economy grew by 10.6% despite social unrest that started in March 2021. And in June 2021 the country began a massive re-opening policy that remains in effect today. The private sector—especially services-related activities—led the recovery, with a contribution of 7 ppts in the overall 2021 growth, and a recovery of around 800 thousand jobs.

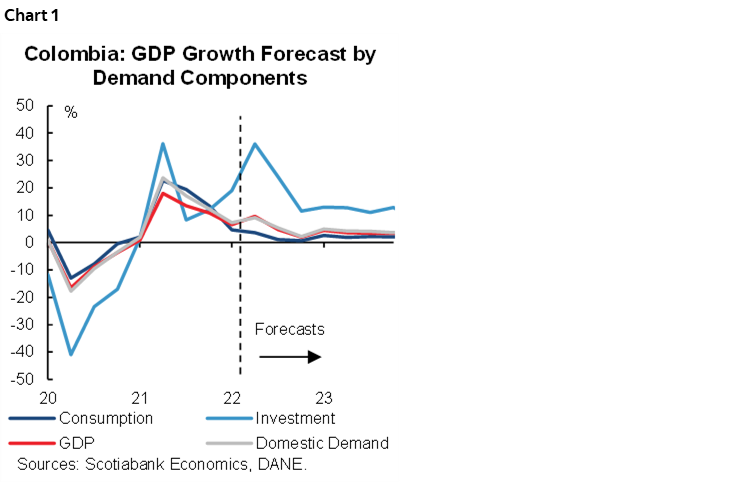

Re-opening will continue to contribute to better economic performance in H1-2022, leading us to raise our economic growth forecast for 2022 from 4.5% to 5.8%. While we expect some slowing of consumption, this is likely to be balanced against a larger contribution to growth from investment (chart 1). That said, there are several risks to watch in H2-2022: i) the reaction to presidential elections results, especially on fiscal guidance which could impact capital investment inflows, ii) the effect of inflation on domestic consumption from the erosion in disposable income, iii) the impact of the bottlenecks in global supply chains on the domestic manufacturing sector, iv) the impact of the Russia-Ukraine conflict, and v) the transition to higher rates in the developed world. As a result of these risks, we remain cautious and bias our GDP projection to the downside.

Inflation reached the highest level since the last significant shock in 2014–2016; and, as the outlook remains clouded, an upside bias remains. In this respect, while our current CPI inflation forecast for the end of 2022 is 7.25%, it doesn’t include potential new upside pressures on agricultural input prices and possible increases in fuel prices, which combined would increase the persistence of current inflationary shocks beyond what had initially been expected and further delay the return to BanRep’s target range (between 2%–4%).

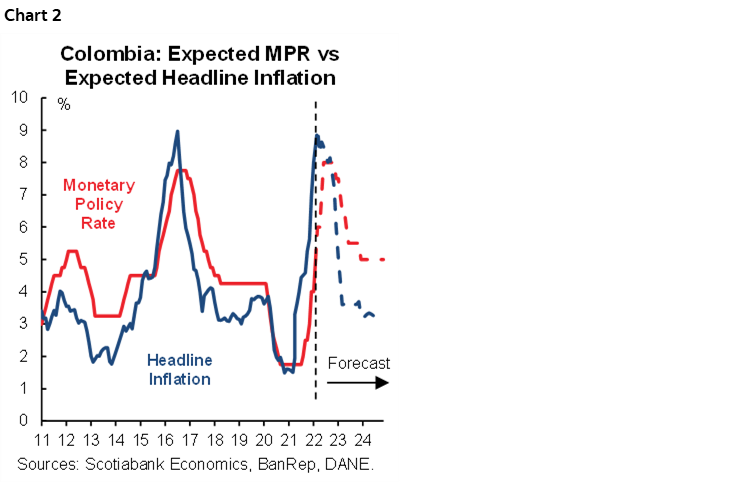

In this environment, with an encouraging economic growth outlook and upside risk on inflation, we expect the monetary policy rate to reach 8% (chart 2) by June—a level that would be contractionary, but which we expect to be temporary (prevailing for around six months). Although it remains to be seen how long current inflationary shocks will be sustained, prices would fall materially if these shocks dissipate and no additional shocks are experienced.

The external deficit is expected to continue to widen in nominal terms, with a current account deficit of around USD 17 bn. However, as economic activity improves the current account deficit would decrease as a share of GDP from the 5.7% in 2021 to 5.0% in 2022. In terms of financing, FDI will be increasingly important, with higher inflows in the mining sector but also the possibility of flows to other sectors. That said, the exchange rate will continue facing headwinds in returning to pre-COVID-19 levels. Still, we think that the USDCOP could close the year around 3,750, showing the positives of higher commodity prices notwithstanding a risk premium from anxiety about the future president’s economic policy, especially on the fiscal front.

All in all, the Colombian economy continues to turn in a strong economic performance, though negative risks remain, and political uncertainty could contribute to even higher volatility in the forthcoming months. The central bank will continue navigating these troubled waters even as international development add new challenges.

Mexico—Public Finances are Well Positioned for Rates Shock, Despite Long-Term Challenges

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

As we have long argued, there are important challenges facing Mexico’s public finances stemming from a weak structural economic growth outlook. Mexican growth averaged just over 2% over the past two decades but looks likely to drop to around 1.5% going forward. We believe that recent shocks to private sector confidence could lead to a decline in investment as a share of GDP from an average level of around 23% to closer to 20%. With lower investment, formal job creation would also see a proportional drop. These factors, combined with the jump in public debt/GDP in the pandemic (public debt is now close to 60% of GDP) and likely higher interest rates going forward, mean that debt levels may be less well anchored—with lower investment, the debt-servicing capacity of the economy, and thus its ability to sustain higher levels of government debt, is reduced. This is a long-term challenge, however, and using the benchmarks of the joint IMF-WB debt sustainability framework, Mexico’s public debt falls within the medium risk range.

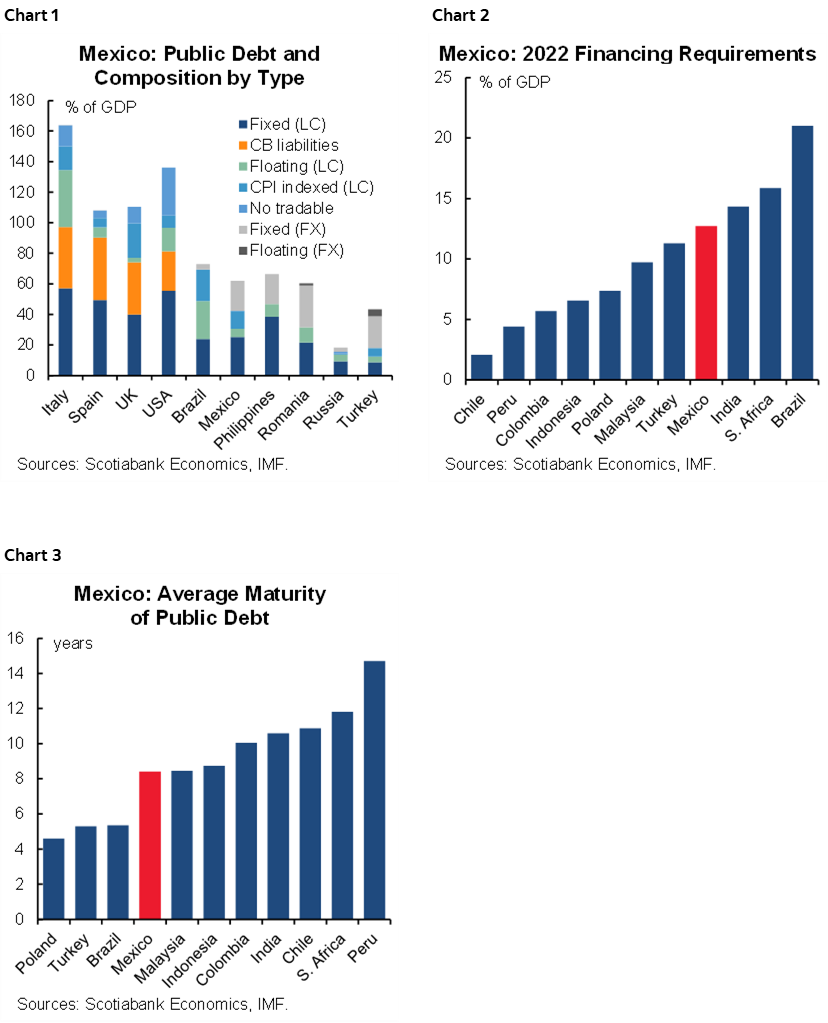

Despite these long-term challenges, Mexican debt is relatively well positioned to absorb the current global shock in which global inflation is driving domestic and foreign interest rates higher. Financing requirements for 2022 are around 13% of GDP (chart 1), which are manageable. The bulk of Mexico’s public debt is local currency-denominated carrying a fixed interest rate (chart 2), while the average maturity of public debt is relatively long (chart 3), at 8.4 years—meaning rates will reset over a longer period, giving the government time to adjust. Foreign currency debt represents 16% of GDP, of which roughly half is owed by state-owned enterprises, and with the bulk of Pemex’s revenues being USD-denominated, the government’s capacity to deal with potential FX volatility is relatively strong.

There are potential pitfalls, however. Rising US yields, alongside a wider Mexico-US spread, represent a challenge in terms of stabilizing long-term debt dynamics. But with a relatively long average debt maturity, the impact of those higher rates will accrue only gradually. In this regard, the Mexico-US spread, which had been close to 400 bps, has consistently widened by around 150–200 bps over the past three years. Interestingly, this widening Mexico-US spread does not appear to be driven by perceived higher credit risks, with only about one-fifth of the total widening explained by wider credit default swaps (CDS). This suggests that the bulk of the higher rates is explained by an FX/inflation premium, which in turn suggests Banxico has lost some credibility.

The conclusion seems to be that, while near-term risks to debt sustainability are low, the authorities have no reason for complacency. In particular, an erosion of central bank credibility could lead to a diminished capacity to issue domestic currency debt, especially in periods of shifting global risk appetite. The return of Original Sin could, in turn, increase debt sustainability risks in response to future fiscal shocks.

Peru—Raising our BCRP Policy Rate Forecast; Constitutional Assembly: Much ado about Something

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

Mario Guerrero, Deputy Head Economist

+51.1.211.6000 Ext. 16557 (Peru)

mario.guerrero@scotiabank.com.pe

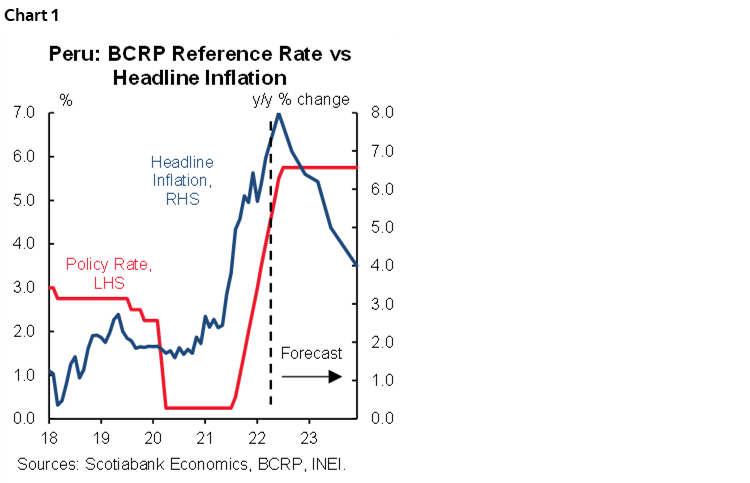

We are increasing our forecast of the terminal level of the BCRP reference rate from 5.0% to 5.75%. We believe that the central bank will increase the policy rate to 5.75%, from its current level of 4.50%, over the next three or four months, at which point it will keep the rate stable (chart 1).

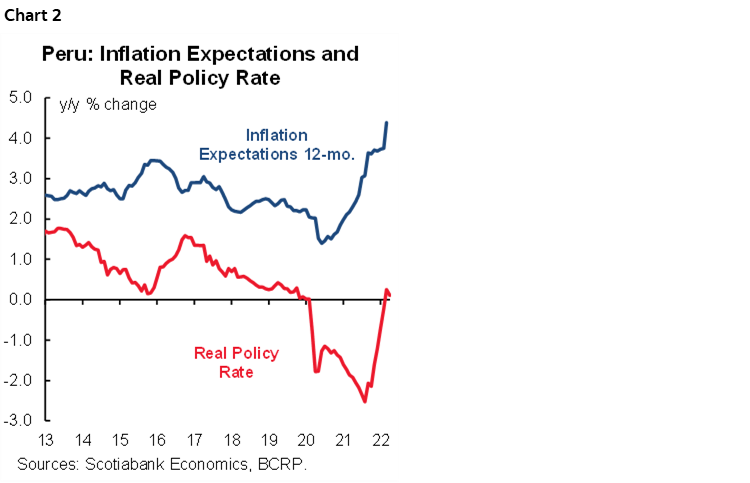

This recalibration does not reflect a change to our forecast of 2022 inflation of 6.4%. Rather, it incorporates the BCRP’s view of the current conjuncture, which puts considerable weight on inflation expectations. The BCRP has reported, for example, that inflation expectations rose sharply in March to 4.4%, up from 3.7% two months ago (chart 2). And in our view, expectations have not peaked. Meanwhile, in its recent policy statement, the BCRP eliminated references to inflation being “temporary” and extended the timeframe for inflation to return to the policy range (1% to 3%), to mid-2023. To us, this suggests increased concern over inflation at the BCRP.

Furthermore, twelve-month inflation to March was 6.8%, and we expect it to rise to 7.6% in April, on its way to surpassing 8%, most probably, before stabilizing. This will affect inflation expectations further and put additional pressure on the BCRP to raise rates.

As noted above, once the reference rate reaches 5.75%, we expect the BCRP to pause into 2023. This level is consistent with a neutral real rate of 1.5% and inflation expectations at 4.25%. That said, the real rate will likely remain below the neutral rate for as long as inflation—and inflation expectations—continue to rise, but then converge towards the neutral rate in 2023.

While we are keeping our inflation forecast for 2022, we are raising our forecast for 2023 from 3.0% to 4.0%. At the same time, we see several risks to our 2022 projection. For one, our forecasts assume that global energy and soft commodities prices stabilize in mid-2022 which, in turn, depends on the duration of the Russia/Ukraine conflict. Another risk is domestic demand/supply imbalances. Although there are no indications such factors are behind inflation at this time, this may change at some point given signs that small domestic farmers are reducing their use of fertilizer owing to its increase in price, thereby potentially affecting output.

The BCRP will also be looking at economic activity. February GDP growth came in at 4.9% y/y. This is a robust figure, at first blush. However, it reflects base level effects, as mobility restrictions were in place at this time in 2021. In month-on-month terms, aggregate GDP growth was flat and sectoral growth was mixed.

We expect growth in March to come in around 3.0%. One positive indicator is that cement sales finally rose in March, up 9% y/y. Growth after March is likely to slow, however, as the low comparison base disappears, inflation begins to bite into consumption, and the general political uncertainty (see below) stifles investment.

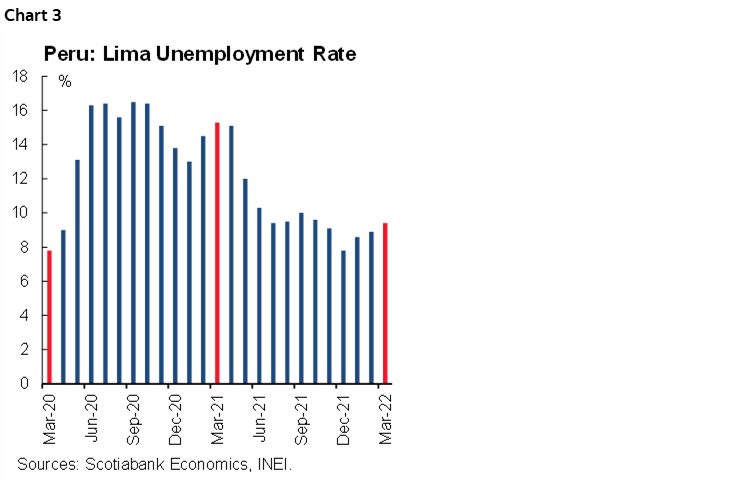

Employment may be showing some initial effects of this uncertainty. The unemployment rate rose in Lima for a fourth consecutive month, from a low of 7.8% in December 2021 to 9.4% in March 2022 (chart 3). In December (Q4-2021), unemployment had briefly touched on pre-COVID-19 levels, but this recovery was fleeting. The number of jobs in Lima has remained stagnant at 4.9 mn since December. The silver lining here is that adequate jobs have risen from 40% below pre-COVID-19 levels, to 16% below.

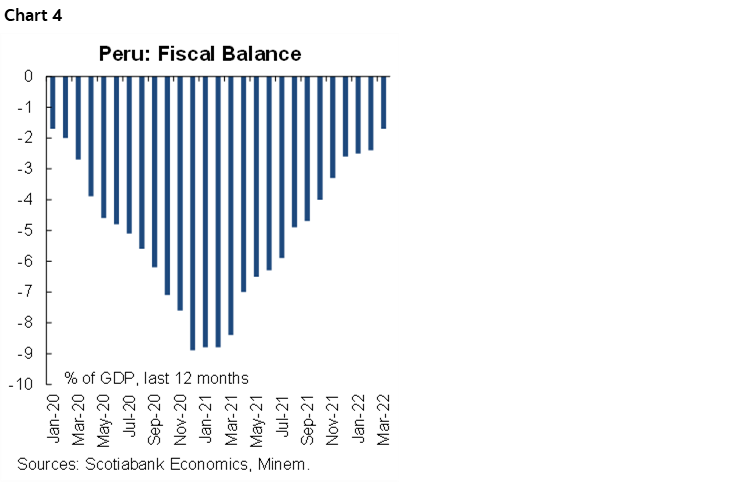

In contrast, the fiscal accounts continue to improve (chart 4). The 12-month fiscal deficit plunged from 2.4% of GDP in February, to 1.7% in March. Income tax revenue rose a huge 47% y/y in Q1-2022, whereas government spending declined marginally. Current expenditure was flat and public investment was down 8%. The fiscal deficit is likely to increase slightly after the March–April tax season ends, and end 2022 within the 2.0% to 2.5% of GDP range. The outlook is unclear, however, due to several recent tax benefits for fuel and key food staples which, so far, account for approximately 0.3% of GDP in lower tax revenue, but which may also presage additional measures that may be in the offing.

Politics have been particularly volatile recently, with potential repercussions on institutional strength and independence. In an unexpected and controversial move, the elections board (Jurado Nacional de Elecciones) dismissed the mayor of Lima on April 27, accusing him of “double dipping” early in his mandate by drawing a state salary as a member of the board of directors of the Lima water company in addition to his mayoral salary. This has added to the perception of institutional instability in general.

Meanwhile, tensions flared up yet again between the Executive and Congress after President Castillo submitted a proposed law to Congress on April 25 to hold a referendum on the election of a Constitutional Assembly with the mandate to draw up a new Constitution. The initiative is unlikely to get the votes it needs. However, the possibility of a Constitutional Assembly had been off the table, and its resurrection by the government is disappointing in that it adds another source of political uncertainty.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.