- Chile: Unemployment rate higher as labour force participation rises; industrial production points to strong growth

CHILE: UNEMPLOYMENT RATE HIGHER AS LABOUR FORCE PARTICIPATION RISES; INDUSTRIAL PRODUCTION POINTS TO STRONG GROWTH

I. Positive labour market outcomes, despite higher unemployment rate

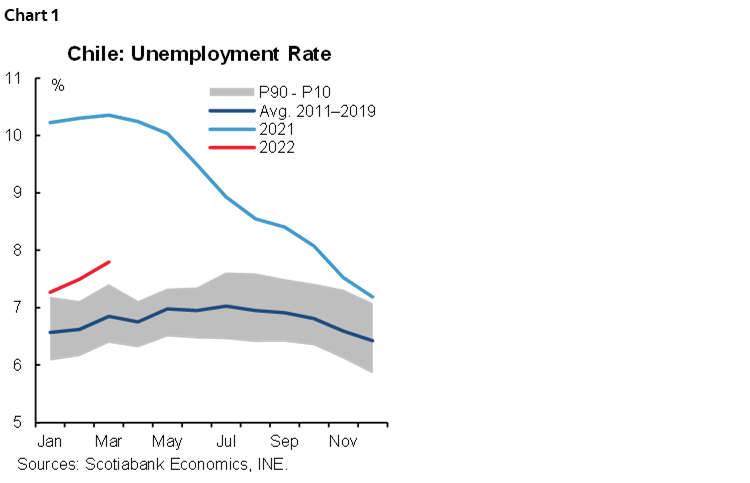

On Thursday, April 28, the statistical agency (INE) released the unemployment rate for the quarter ending in March, which rose to 7.8%, in line with our expectation, again owing to higher labour force growth (0.7% m/m) compared to that of employment (0.3% m/m). Given that dynamic, and the impact of seasonal factors, it should come as no surprise that the unemployment rate has risen (chart 1) as labour market participation continues to recover in-line with the increased openness of the economy.

Job creation, while continuing, has not kept pace with the recovery of the labour force. In this sense, we consider that there is no deterioration in the labour market, since the low unemployment rate in the second half of last year reflected obstacles to participation in the labour market linked to mobility restrictions, as well as the effects of fiscal transfers and pension withdrawals.

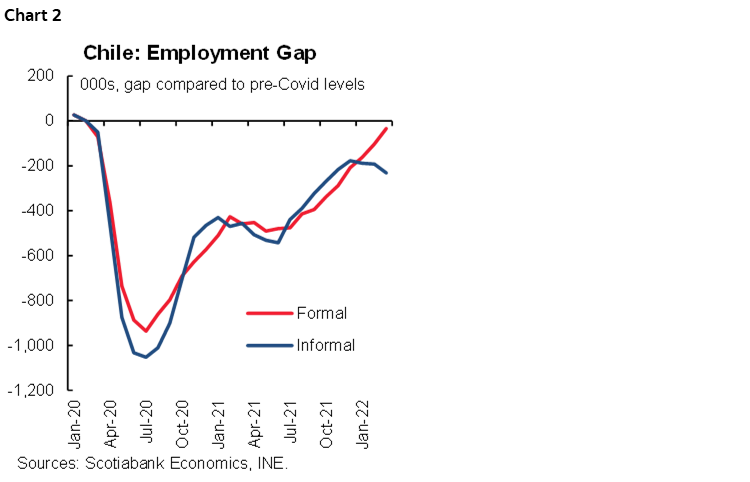

There are still 266k jobs to recover compared to the level of employment prior to COVID-19. In the quarter ending in March, 29k jobs were created (22k men and 7k women). This pace was higher than that observed in seasonally adjusted data for March and is attributable to the strong increase in private salaried employment, especially in services and mining. However, there is still a long way to go to return to the pre-pandemic employment rate, which stood at 54.9% in March, well below the 58% forecast for this month in a typical year. Under this metric, there are around 480k jobs to be created to return to expected employment levels for the size of the Chilean labour market.

Once again, the strong creation of formal jobs in the quarter ending in March stands out (69k), compared to the loss of informal jobs (40k) (chart 2). By economic sector, formal job creation was concentrated in accommodation (18k), health (14k), professional activities (12k), and administrative services (12k). The same sectors also account for smaller decreases in informal employment, which could be indicative of a process of re-composition in jobs, from informal to formal, possibly encouraged by the labour subsidy (IFE laboral) provided by the government.

II. Monthly GDP would expand 7.0% y/y in March

On Friday April 29, statistical agency (INE) released the industrial production index for March, which expanded 0.8% y/y, above market expectations (Bloomberg: -3.9% y/y). The figure is explained by a superb performance of the manufacturing production, which grew 3.3% y/y (+2.9% m/m), surpassing market expectations (Bloomberg: -3.0% y/y), and the rebound in mining production (-2.2% y/y). According to INE, retail sales increased in March by 11.3% y/y, in line with our projection. In our view, these indicators support a monthly GDP expansion of 7% y/y in March, which is consistent with a Q1-2022 GDP growth of 7.8% y/y (-0.7% q/q).

—Jorge Selaive, Anibal Alarcón, & Waldo Riveras

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.