- Mexico: GDP expectations remain weak as inflation rises in Banxico’s April Survey

- Peru: April inflation surprised on the upside, exceeding market consensus and Scotiabank’s estimate

MEXICO: GDP EXPECTATIONS REMAIN WEAK AS INFLATION RISES IN BANXICO’S APRIL SURVEY

I. GDP expectations remain weak

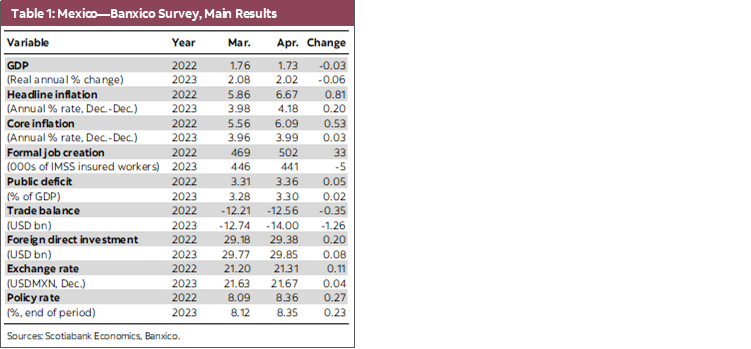

Banxico’s April Survey of Expectations confirmed expectations of higher inflation and weaker growth in 2022 and 2023 (table 1). Expected growth for 2022 moderated from 1.76% to 1.73% y/y, while the consensus for 2023 fell from 2.08% to 2.02% y/y. Revisions to expected inflation were more significant, rising from 5.86% to 6.67% y/y for 2022 and from 3.96% to 4.18% y/y in 2023. Expectations of core inflation also increased, from 5.56% to 6.09% y/y for 2022, and from 3.96% to 3.99% y/y for 2023. More analysts anticipate further interest rate hikes, with a median policy rate of 8.25% for end-2022, up from 8.00%, with the rate staying at that level through the end of next year. Despite recent exchange rate appreciation, analysts expect a slight depreciation, from USDMXN 21.20 to USDMXN 21.31 for 2022, with no change for 2023 at USDMXN 21.67. Meanwhile, the percentage of analysts who consider that now is a good time to invest remained practically unchanged at 8%, while 59% think it’s a bad time, and 32% said they were unsure. Finally, analysts assess inflationary pressures (16% of responses), domestic political uncertainty (11%); public insecurity problems (11%); weakness in the domestic market (8%); and higher input and raw materials prices (8%) as the leading factors hindering growth in the next six months.

II. GDP flash estimate for Q1-2022 shows an uneven recovery

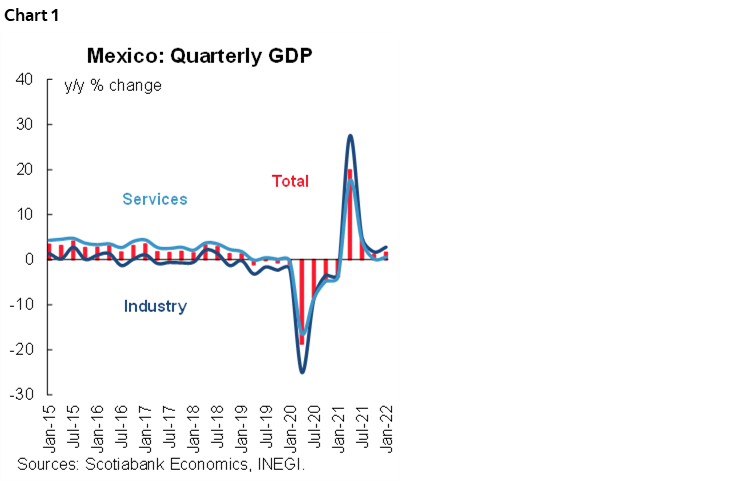

The flash estimate for Q1-2022 GDP released by INEGI on Friday, April 29 met market expectations at 1.6% y/y, up from 1.1% y/y in Q4-2021 (chart 1). Primary activities increased 2.1%, secondary activities 2.8%, and tertiary activities 0.6%. On a quarterly basis, GDP grew 0.9% q/q (0.0% previously, 1.1% expected), with primary activities falling -1.9%, which was more than offset by secondary and tertiary activities, both of which accelerated by 1.1%, respectively. These preliminary results show the uneven recovery across sectors, which remain below pre-pandemic levels. Looking ahead, we expect the war in Ukraine and inflationary pressures will continue to affect economic activity, exacerbating the trend weak investment, which started to fall in 2018 and has stagnated below pre-pandemic levels.

—Miguel Saldaña

PERU: APRIL INFLATION SURPRISED ON THE UPSIDE, EXCEEDING MARKET CONSENSUS AND SCOTIABANK’S ESTIMATE

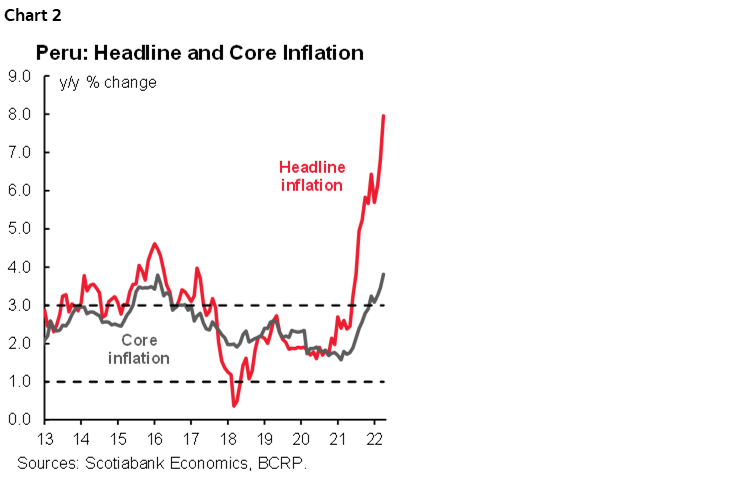

In April, inflation again surprised on the upside, reaching 0.96% m/m, the highest m/m rate in 27 years for the month since 1995, when it reached 0.98%, exceeding the estimate by the market consensus (0.63% according to the Bloomberg survey) and our own forecast of 0.7%. Year-on-year inflation accelerated from 6.8% y/y to 8.0% y/y (chart 2). April marks the 11th consecutive month that inflation exceeded the upper limit of the central bank’s target range (between 1% and 3%). And with price pressures showing no signs of abating, April’s result will continue to put pressure on the central bank, which we expect will continue to raise its benchmark rate in May.

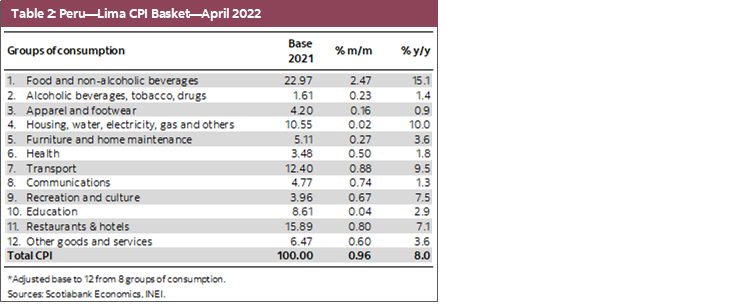

Price pressures were broadly based in April. Of the 586 products that make up the consumer basket (base 2021), 453 (77%) rose, 67 (11%) fell, and 66 (11%) remained unchanged (table 2). Core inflation went from 3.5% y/y in March to 3.8% y/y in April, above the upper limit of the target range (3%) for the fifth consecutive month. Moreover, the increase in prices occurred despite the government’s temporary reduction of the excise tax (ISC) on gasoline and its inclusion in the Fuel Price Stabilization Fund, though these measures were reflected in a reduction in the price of oil diesel (-8.1%) and vehicular liquefied petroleum gas (-2.2%).

Wholesale inflation, linked to production costs, jumped from 11.6% in March to 13.1% in April, the highest rate so far this year. The USDPEN exchange rate, which appreciated 1.8% y/y in March, depreciated 1.9% y/y in April, contributing to the rise in the prices of imported products.

For May, we expect inflation between 8% y/y and 9% y/y, driven by a low base of comparison, given that May 2021 inflation was 0.27% m/m, and continuing high commodity prices for key products, such as oil, grains, and fertilizers. The government has announced a temporary reduction of the VAT for a set of products such as chicken, eggs, milk, meat, wheat, pasta, and sugar starting in May, although business associations question the effectiveness of this measure. The government also announced a 10% increase in the minimum monthly wage, from PEN 930 to PEN 1,025 (USD 267), to compensate for the loss of purchasing power from higher inflation, although the scope of this measure is also limited (covering just 12% of the formal labour market). The estimated fiscal cost of the measures is close to 0.3% GDP, the same as the average for comparable measures in Latin America, according to the IMF.

In our Latam Weekly of April 29, 2022, we revised our inflation forecast for 2023 from 3.0% to 4.0%, with the message that we see inflation as more persistent and therefore less likely to return to the target range next year. The central bank estimates that inflation will return to the target range by the second half of 2023, but its chairman, Julio Velarde, recently warned that there is a risk that inflation will persist in the longest period outside the target range. From 2000 until now, the longest period with inflation above 3% was 21 months (between October 2007 and June 2009). With April’s result, there have now been 11 consecutive months in which inflation exceeded 3%.

For 2022, our inflation forecast of 6.4% maintains an upward bias given the April results and the analysis of the effects of the Russia-Ukraine conflict on the prices of raw materials and the problems in China over supply chains.

Over the past nine months, the central bank has raised its benchmark rate by 425 basis points to 4.50% and increased reserve requirements three times. We believe further increases in the policy rate are necessary to prevent further slippages in inflation expectations (4.39% over 12 months according to the BCRP March survey, the highest level since October 2008) away from the target range. Accordingly, we expect a rise of 50 bps in its meeting on Thursday, May 12.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.