- In a split decision, BanRep hiked its policy rate 100 bps, to 6.0%, as expected. Four Board members voted for the 100 bps increase, with three members voting for a 150 bps rise.

- We retain our call for BanRep to keep hiking 100 bps over its next two meetings, leading to a terminal rate for this tightening cycle of 8.0%.

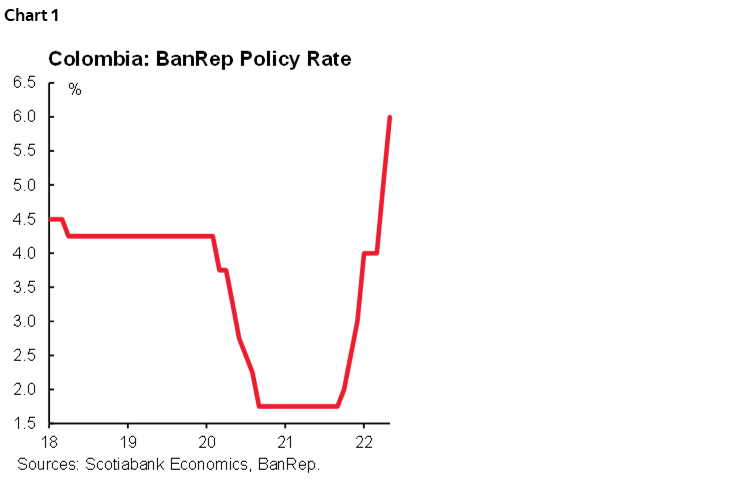

Today, April 29, in a split decision, the Board of Colombia’s central bank (BanRep) increased the monetary policy rate 100 bps to 6.0% (chart 1), as expected by market consensus and Scotiabank Economics. Four board members voted for the 100 bps hike, while three members wanted a more hawkish stance, voting for a 150 bps hike. Despite the split decision, the Board is unanimous in its intention to normalize monetary policy. BanRep’s staff again increased its GDP growth forecast for 2022, this time from 4.7% to 5.0%. The communique was unusually short, though it recognized the high uncertainty with respect to inflation.

Key features of the decision include:

- The split vote shows that increasing inflationary risks have led to shift in the balance on the Board. For now, we affirm our expectation of 100 bps moves in the future, but the Minutes (to be released on Tuesday, May 3) will be relevant to make a balance ahead of forthcoming meetings.

- The Board received an update on the macroeconomic forecast, but Governor Villar provided few details in the press conference. Having said that, the governor acknowledged that the new forecast incorporates further inflationary risks, but still projects a gradual convergence to the target range in the medium term.

- Governor Villar also highlighted that a neutral rate is not the final target in the current hiking cycle and that depending on the inflation measure used (spot, 1-y expectations, or 2-y expectations) the real policy rate could currently be close to neutral, or even contractionary. Either way, Villar said the Board remains data-dependent.

- In the same vein, Villar highlighted that the main challenge for monetary policy is to ensure domestic demand is compatible with productive capacity. He emphasized that, while current inflationary pressures are partly attributable to supply shocks, strong demand explains why the central bank is continuing to increase the policy rate.

- Villar also noted that the IMF renewed the two-year Flexible Credit Line of USD 9.8 bn for Colombia. The MoF has said that the Government is not considering using this line and that the FCL will be treated as part of higher international reserves and is considered as a precautionary buffer.

As expected, BanRep hiked 100 bps, with one more Board member joining the hawkish side. Looking ahead, it will be important to monitor the balance of opinion for future meetings; in this regard, the Minutes will provide further details about the discussion and the arguments cited in support of different positions.

For now, we keep our call of further 100 bps hikes in each of the next two meetings, leading to a terminal rate of 8% for this tightening cycle. This projection is subject to inflation developments, however, and the staff's updated macroeconomic scenario, which will be released on Monday, May 2. This scenario will be key to assessing possible changes to the terminal rate. The press conference with the staff will be on Wednesday, May 4.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.