- Colombia: Economic activity signals continued expansion, with construction improving while inflation begins to affect other sectors

- Peru: February GDP growth of 4.9% is not quite as strong as it looks

COLOMBIA: ECONOMIC ACTIVITY SIGNALS CONTINUED EXPANSION, WITH CONSTRUCTION IMPROVING WHILE INFLATION BEGINS TO AFFECT OTHER SECTORS

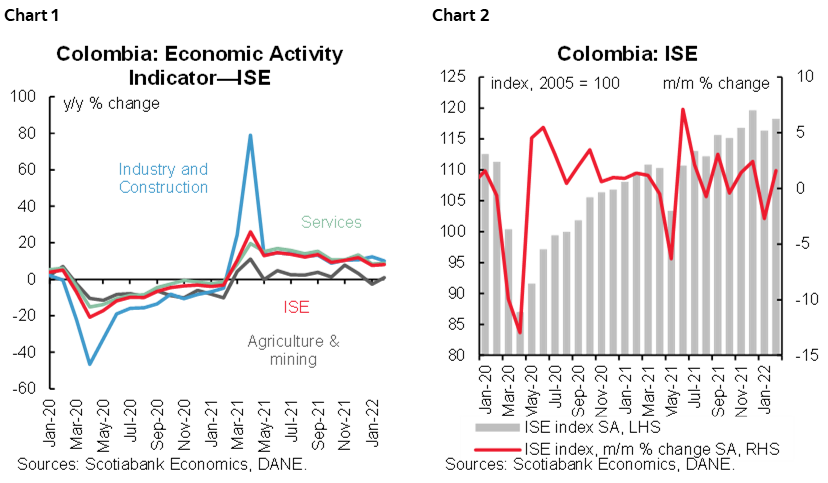

On Monday, April 18, the Colombian Statistical Agency (DANE) released the February 2022 Economic Activity Indicator (ISE), the main proxy for GDP, which expanded by 8.1% y/y, well above the Bloomberg market consensus of 7.2% y/y. Activity increased across all sectors of the economy, with the secondary and services sectors boosted by a monthly base effect in the financial sector reflecting a large one-time payment by an insurance company in January (chart 1). On a monthly basis, economic activity expanded 1.6% m/m (chart 2), comparable to the pace in the last quarter of 2021. Compared to its pre-pandemic level (February 2020), the activity indicator showed growth of 5.6%.

February’s ISE results showed positive signals:

- Primary activities (13% of the economy) expanded by +0.9% y/y and 4.3% m/m (seasonally adjusted) in February. The agricultural sector was up 1.2% y/y, while mining and oil production only rose 0.3% y/y, showing that mining and oil continue to lag the recovery. Agriculture output is likely affected by higher production costs, while lower oil production is partially offsetting the positive terms-of-trade effects from high international prices.

- Secondary sectors (17% of the economy) rose 10.1% y/y and expanded 1.0% m/m. Manufacturing production continues to be strong in areas affected by the reopening and increased mobility, growing 9.2% y/y. Likewise, construction is performing better as it increased 12.4% y/y consistent with stronger economic growth.

- Service-related activities (70% of the economy) were up 8.9% y/y, and increased 0.7% m/m as compared to a contraction of -3.8% m/m in January, which reflected an insurance payment for the Hidroituango case. However, other services sectors, such as commerce, transportation and hotels, and restaurants, contracted -0.3% m/m, possibly pointing to the effect of inflation on consumption as households feel the effects of higher food prices on their disposable income and are reducing non-essential consumption.

February’s result showed a positive outcome in the consolidation of economic activity growth, offsetting the negative effect of the previous month. However, there were also signals pointing to inflation weighing on some activities that should be monitored in the months ahead.

Overall, we highlight the recovery in the construction sector, which continued to reduce the gap with pre-pandemic levels of activity. In addition, there was a boost in terms of employment growth, with employment now just 2.73% below the pre-pandemic level. Meanwhile, economic activity is 8.02% above its pre-pandemic level. These results support our forecast of GDP growth of 4.5% in 2022.

—Sergio Olarte, Maria Mejía, & Jackeline Piraján

PERU: FEBRUARY GDP GROWTH OF 4.9% IS NOT QUITE AS STRONG AS IT LOOKS

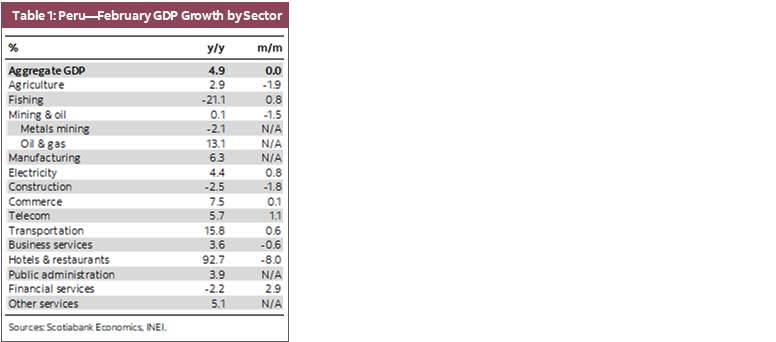

February GDP growth came in at 4.9%, y/y (chart 3), according to data released on April 15 by the National Statistics Institute, INEI. On the face of it, the number seems strong, and it is the highest rate of growth rate in five months. However, looking at the figure in more depth shows a slightly different picture. February’s y/y growth was off a low comparison period, as February 2021 was a period of COVID-19-related mobility restrictions (chart 4). Unsurprisingly, the sectors with the greatest growth this year were those most affected by the restrictions last year (table 1). These sectors include hotels & restaurants, up 93% y/y in February, transportation (15.8% y/y), and, to a lesser extent, commerce (7.5%), telecom (5.7%), electricity (4.4%), and manufacturing (6.3%).

In month-on-month terms, things were less exciting. Aggregate GDP growth was flat, m/m, and sector growth rates were mixed. Outside of fishing, electricity, telecom, financial services and transportation, each of which rose a robust 0.6% to 1.1% in month-on-month terms, all other sectors showed low or negative growth compared to January, the month before.

On the plus side, oil & gas growth of 13% y/y was led by a nearly 41% increase in oil output. This increase is not a temporary effect, as it largely is the result of operations that had been down due to maintenance and repairs coming back on stream.

Of particular concern is construction GDP, which declined 2.5% y/y, falling for a fifth consecutive month. This is in line with an 18% y/y decline in public investment, and probably also reflects low private investment, both in infrastructure projects and in residential construction.

Another sector to keep an eye on is metals mining. The decline in February was mainly in zinc-lead-silver mines, whereas copper output was down only 0.9%. Note, however, that we expect the impact of unrest on copper output to be much larger in March.

The upshot is that the nearly 5% y/y growth that took place in February is likely not sustainable. March will be the last month with a favorable comparison base, although less so than in February because mobility restrictions were in place only for half of March in 2021. Education also came back in force in March–April 2022, whereas schools were still shut in 2021. This should add to growth. At the same time, March 2022 was fraught with social unrest, including nearly a week of blocked roads, and a one-day lockdown decreed by the government to cool down protests. Also of significance, operations at the Cuajone mine (Southern Peru), which represents 7% of Peru’s copper production, were halted throughout the month of March this year. Finally, public investment fell 7%, y/y, in March.

It’s hard to gauge just how much these issues will compensate the favorable base, but the likely balance should put GDP growth in March in the vicinity of 2% to 3%, y/y.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.