FORECAST UPDATES

- New data on inflation, activity and output continue to challenge short-term projections. See the table below for our country teams’ latest forecasts and their notes on risks to the projections.

ECONOMIC OVERVIEW

- Inflation remains the biggest challenge facing Latam economies. But even as central banks mobilize to contain price pressures and return inflation to target, risks to growth remain.

- These risks come from two sources: continuing large relative price shocks that can introduce an inflationary impulse that could lead to output losses; and increased uncertainty with respect to underlying relative prices that distort investment decisions.

- Lower investment could set back efforts across the Latam region to reduce the informal sector, which is characterized by low productivity and low wages, thereby impeding development.

- These effects underscore the importance of the inflation, relative prices, and growth nexus.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico, and Peru.

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period February 19–March 4 across the Pacific Alliance countries, plus their regional neighbours Argentina and Brazil.

Economic Overview: Inflation, Relative Prices, and Growth

James Haley, Special Advisor

416.607.0058

Scotiabank Economics

jim.haley@scotiabank.com

- Sustained, high inflation in the Latam region would pose a threat to growth and development more broadly. Relative prices play a role in two key respects.

- First, if prices are “sticky” downwards, large shifts in relative prices—like those seen in the pandemic—can impart an inflationary impulse that, if incorporated into expectations, could lead to (higher) output losses as central banks return inflation to target.

- Second, if inflation goes unchecked, changes in relative prices could become masked by generalized price adjustments. The resulting uncertainty with respect to relative prices may distort investment decisions—leading to unproductive investments or a lower level of investment in aggregate.

- Less investment in physical capital would impede efforts to bring workers from the informal sector to more productive activities, setting back economic and social development.

THE GREAT INFLATION REDUX?

Recent editions of the Latam Weekly have focused on—some might say “obsessed over”—the importance of raising long-term growth rates. Given the seriousness of the inflation problem now confronting the Latam region, many readers might argue this emphasis is misplaced. They would certainly be right to warn about high inflation and the risk that inflation expectations become unmoored from inflation-target anchors.

Each new week brings more data points that underscore the persistence of what had been expected to be a “temporary” inflation problem. In Colombia, January inflation came in at the highest level since September 2016. And even where headline inflation moderated somewhat in January, as in Mexico and Peru, inflation expectations continue to be ratcheted higher. In Chile, meanwhile, an expected moderation of inflation in January did not materialize.

In short, the “temporary” inflation of mid-2021 clearly shows no sign of abating. However, the current inflationary episode may yet prove transitory in a longer-term perspective given the inflation-targeting frameworks by which most central banks operate. To put it bluntly, this is not the mid-1970s, when central banks’ nominal anchors were slipping or largely non-existent. In the economic literature, that period has become known as the “Great Inflation.” And while there may be some similarities between then and now, the fundamental lesson of that time has not been forgotten; those who predict a Great Inflation Redux may end up fighting the Fed.

But it is precisely because of the risks posed by continuing high inflation that efforts to raise potential growth are so important. To state the obvious: a central bank actively fighting inflation does not have the luxury of worrying about stabilization policy. That is, stabilizing output around its potential level. The hierarchy of goals in such cases is clear—even for central banks with formal or, what is more generally the case, informal price stability and full employment dual mandates. The first order of business is to contain inflation. Moreover, when inflation is at least partially driven by supply shocks, the capacity of central banks to raise output is at best limited; at worst counterproductive.

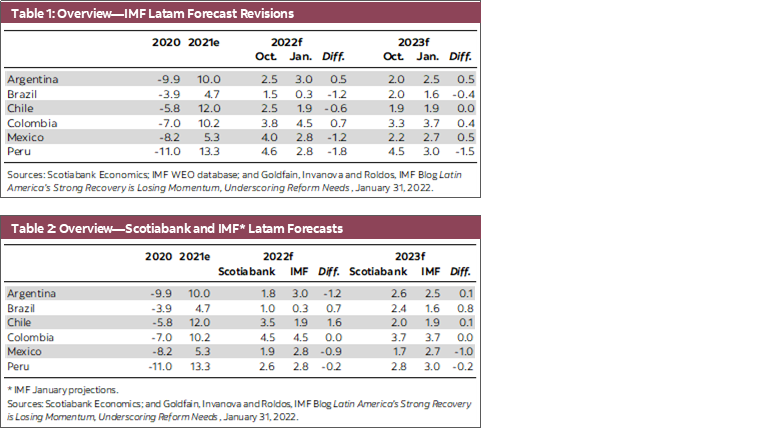

At the same time, longer-term economic performance may suffer, as high inflation masks relative prices in the economy, and incentives to save and invest are distorted. Such effects are not merely hypothetical. In fact, they may already be reflected in recent IMF forecasts, which have been marked down, significantly so in some cases, in just the past few months (table 1). These downward revisions could be a mid-course correction, as the Fund staff lowered what might have been overly optimistic projections based on the very rapid recovery in the Latam region earlier in 2021. A comparison of the latest IMF forecasts to the projections of Scotiabank’s country teams suggests that is the case (table 2). Nevertheless, the Fund staff clearly see cause for concern with respect to longer-term growth. Their policy prescription is reforms to raise potential growth.

Relative price effects are central to growth for two reasons. First, a spike in the price of durables, say, relative to the price of services can exert an inflationary impulse. This is because prices are generally considered to be “sticky” downwards; that is, prices are far more flexible in terms of going up in response to excess demand but decline more slowly and often require a condition of persistent excess supply to adjust down.

Downward rigidity clearly violates the economist’s ideal of perfectly flexible prices, and the degree to which markets are characterized by it may wax and wane according to changes in the structure of a market, such as degree of competitive pressures, the variability of underlying demand, and even social norms. Regardless, a steep increase in the price of durable goods and decline in the demand for services, like that which occurred in the pandemic, will have an appreciable impact on the price level as durables increase in price while the price of services remains fixed.

In theory, the effects of the resulting shift in relative prices would dissipate over time, with little lasting impact on inflation, as service prices fall (or rise by less than the pre-shock trend). And if the central bank holds fast to its nominal anchor, there should be no permanent inflationary effects. But as noted above, the danger lies in the initial inflation shock becoming embedded in inflation expectations such that it becomes more difficult for the central bank to return inflation to its pre-shock path without engendering a larger-than-expected output loss—in other words, without triggering a recession.

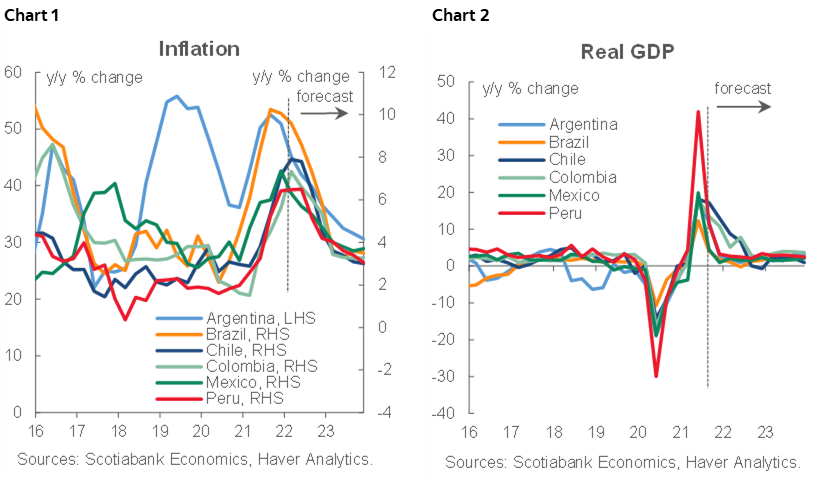

Provided the central bank’s commitment to price stability is secure, the risks to growth from this relative price inflation may be well contained. However, the longer that successive relative price shocks—augmented by generalized excess demand pressures—push some prices higher, the greater the likelihood that these expectations shift higher. In this respect, central banks cannot rely solely on their credibility; to retain that credibility, they must demonstrate they are prepared to act to preserve price stability. Arguably, that is why Latam central banks have acted more proactively than their peers elsewhere: with less experience with inflation-targeting and facing a wider range of potential shocks, central banks in the region may have less leeway. Their challenge is finding the sweet spot in terms of monetary tightening, tightening sufficiently to keep expectations anchored, so that inflation returns to target (chart 1), but not so much as to engineer an unnecessary drop in output (chart 2). The forecasts of Scotiabank experts in the region assume that central banks succeed in this quest.

The second reason why relative price effects are important to growth is that, in practice, shifts in relative prices are the signal by which resources are allocated in a well-functioning market economy. Inflation has a pernicious effect in this respect because it introduces increased uncertainty with respect to relative prices. In an environment of high inflation, changes in relative prices are masked by a confusing cloud of generalized price adjustments.

The danger in this situation is that investment decisions are distorted or delayed, with adverse effects for growth and development more broadly. It is possible, for example, that scarce capital is channeled into areas that seemingly offer high returns in terms of output gains, but which turn out to be unproductive when the veil of inflation is removed. Or productive investment could be delayed if inflation introduces sufficient uncertainty with respect to relative prices and the returns from physical investment: firms may simply exercise the option value of waiting until such time as the expected long-term returns from expanding capacity are clearer. In the limit, under conditions of extreme inflation, productive investment may cease, as investors seek to preserve capital value from the corrosive effect of inflation, opting for the security of inflation hedges, rather than take the risk of investing in plant and equipment.

Of course, political uncertainty, such as that which has prevailed in Peru (see the country notes below prepared by our country team in Lima) and policy-induced uncertainty about which Scotiabank’s experts in Mexico City have written in past editions of the Latam Weekly, also discourage investment. In this respect, with the added risk to growth from inflation, the potential costs of these effects are even higher so that it is incumbent on governments to contain such uncertainty going forward.

Saving is also affected by inflation. Unexpected inflation can drive the real returns on savings down (or negative if the inflation shock is sufficiently large). In such circumstances, individuals may choose to increase consumption rather than suffer the loss in real wealth. This may generate a transitory bump in activity, but at the cost of reducing long-term growth.

These effects could have particularly serious impacts on the Latam region. In the first instance, this is because they would impair efforts to reduce the informal sector, which is characterized by low-productivity, labour-intensive activities. As Scotiabank’s team in Bogota highlight in the country notes below, the informal sector accounts for more than half of Colombia’s economy. Moving workers from these low-paying jobs into more capital-intensive employment represents the most direct path to economic development because productivity and wages are tied to the capital-labour ratio. But if inflation distorts and reduces investment, this capital-deepening effect is delayed.

This is why understanding the nexus between relative prices, inflation and growth is so important.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—Constitutional Assembly Drafting New Constitution

Jorge Selaive, Head Economist, Chile

+56.2.2619.5435 (Chile)

jorge.selaive@scotiabank.cl

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

Waldo Riveras, Senior Economist

+56.2.2619.5465 (Chile)

waldo.riveras@scotiabank.cl

Owing to the advance of the omicron variant, the daily number of confirmed COVID-19 cases has continued to increase sharply in recent days, reaching its highest level since the beginning of the pandemic. The test positivity rate rose to 28%. The occupancy rate of ICU beds is increasing, while the COVID-19-related death rate rose to its highest level since July 2021. Meanwhile, the vaccination campaign reached 93% of the eligible population. The rollout of booster (third) doses continues—reaching 12.2 million people—and the new booster dose (fourth) is in progress.

On Tuesday, February 8, the statistical agency (INE) released the CPI for January, which rose 1.2% m/m (7.7% y/y), above both market consensus and our expectations. Along with the January CPI reading, the index that excludes volatile elements also increased 1.2% m/m—the second highest reading in the last 25 years, surpassed only in March 2008. Such increases were last recorded in the mid-1990s. The most volatile items, such as food and energy, continued to fuel inflation, with increases of 1.6% m/m and 0.8% m/m, respectively.

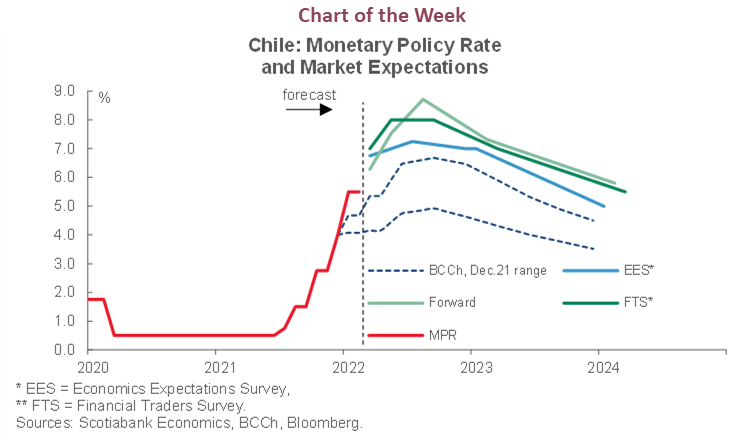

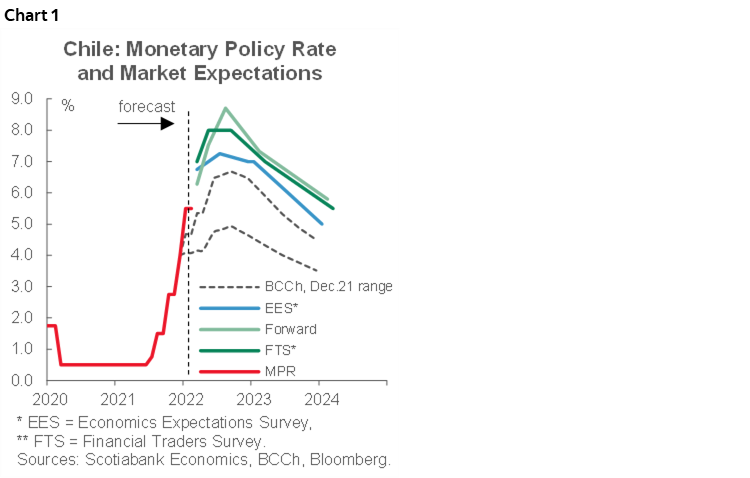

In our view, this reading further complicates the inflationary situation observed over the last year, exacerbating the already worrying de-anchoring of inflation expectations. Given this, in its next Monetary Policy Meeting on March 29, the central bank is likely to significantly increase the benchmark rate, with a possible hike of between 100 and 150 basis points once again under consideration. Market expectations also include new hikes in the benchmark rate for following meetings, above the upper part of the central bank’s December corridor (chart 1).

On Friday, February 4, the Ministry of Finance (MoF) released its Public Finance quarterly report, corresponding to the fourth quarter of 2021. A key change relative to the last report was the upward revision in the GDP forecast for 2022, which increased from 2.5% in September to 3.5%. Scotiabank Economics also projects GDP growth of 3.5% this year.

Regarding the fiscal figures, the MoF is projecting a structural fiscal deficit of 2.8% of GDP for 2022 (compared to 3.9% of GDP in the September projection) and an increase in public debt from 37.5% of GDP to 38.6%. In addition, the MoF announced the injection of USD 4 bn to the Economic and Social Stabilization Fund (FEES) in January, which closed 2021 with USD 2.5 bn and with the injection now totals USD 6.5 bn.

On Tuesday, February 15, the Constitutional Assembly began discussion and voting on the first set of proposals coming from the seven thematic commissions established to make recommendations to be included in the new constitution bill. On Tuesday, February 15, the floor of the Assembly voted, in general, on the proposals from the Justice Systems Commission, passing 14 of 16 proposed principles, including legal pluralism, which in practice would allow indigenous communities to create their own conflict resolution systems. On Wednesday, February 16, the Assembly voted, in general, on principles for the new constitution proposed by the State Form Commission, including among others a regional, multinational and intercultural State, the creation of autonomous regions, and autonomous indigenous territories. The Assembly is also scheduled to vote on the proposals of both Commissions, on an article-by-article basis. Each proposal needs a two-thirds majority in the Assembly (103 votes) for approval. The final results of this process are unknown at the time the Latam Weekly is published. However, if an initiative is rejected, it will go back to the original Commission to be discussed, modified, and voted in the floor of the Assembly in a second round. This process will extend to April 28, at which point the Assembly will have the final draft of a new constitution. After that, a Commission of Harmonization will ensure the consistency and coherence of the approved norms.

In the fortnight ahead, on March 1, the central bank will release the January monthly economic activity index (IMACEC), for which we expect an expansion between 11.5% and 12.5% y/y.

Colombia—Good Fundamentals Behind the Political Noise

Sergio Olarte, Head Economist, Colombia

+57.1.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Jackeline Piraján, Economist

+57.1.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

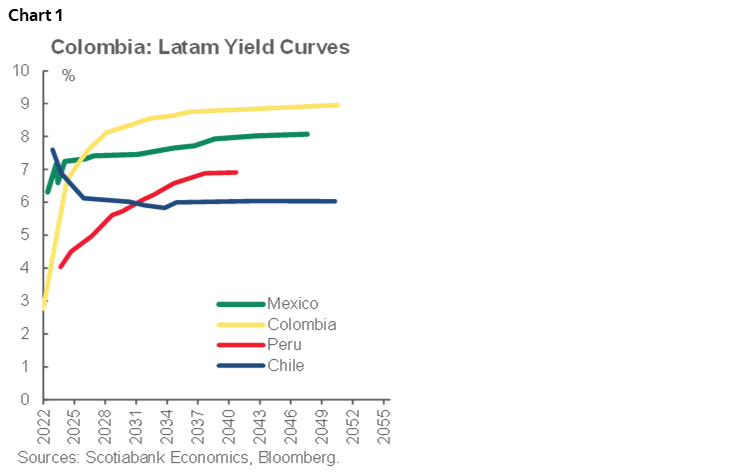

The COVID-19 crisis not only produced the most significant economic contraction in Colombia in the last 100 years but also revealed how vulnerable and weak the fiscal accounts were. In fact, despite the severity of the 2020 recession, in which growth fell 7%, the countercyclical expenditure of the government was only 3% of GDP. In contrast, Colombia’s peers provided expenditure support of more than 12% of GDP. Meanwhile, markets and international rating agencies downgraded Colombia’s assets to non-investment grade. As a result, the COLTES curve deteriorated on average by 280 bps in 2021—40 bps more than Peru’s yield curve and 80 bps more than Mexico’s, while the COP depreciated 8% more than the currencies of these peers (chart 1). However, in the aftermath of the crisis, Colombia has been able to recover at a faster pace and with apparently more stability than its regional peers, given the resilience of private demand, which has brought higher tax collections that drove public debt as a share of GDP three percentage points lower than projected in 2021.

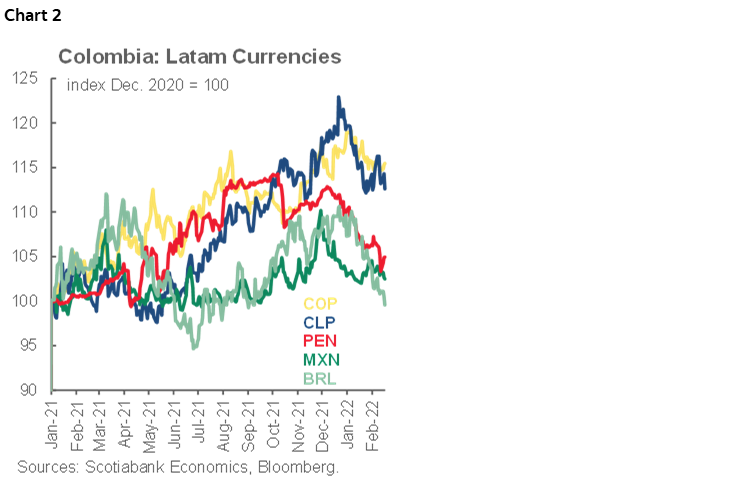

Unfortunately, this good news in terms of growth and the fiscal accounts has not yet been incorporated in asset prices and expectations regarding the medium-term outlook. The yield curve continues discounting a weak fiscal scenario, while the COP is one of the worst-performing currencies in the region (chart 2). While the new more hawkish tone from the Federal Reserve and other developed central banks affects asset pricing, along with geopolitical issues between Russia and Ukraine, those effects should hit markets across the peers and not only Colombia. So why have Colombian assets fared worse than peers in the past couple of months? We think that the upcoming electoral season may be to blame.

In this respect, the next president must introduce fiscal and labour reforms to consolidate the recent good news in terms of financial accounts and economic activity. But there is still considerable uncertainty regarding the possibility and willingness of the new president to implement a fiscal reform that would make current expenditures more flexible, increase tax collection by at least 1.5 ppts of GDP, and enhance the flexibility of the labour market to increase the formal sector and raise productivity. Currently, the informal sector accounts for more than 50% of the economy, while productivity has declined for the last five years.

We think markets are unlikely to incorporate economic and financial good news into Colombian asset pricing until the elections are behind us. Moreover, volatility will continue at least until the first round of the presidential election (May 29). That said, markets will likely come to realize that, while the Colombian congress has no majority, close to 80% of the congress members are market-friendly, which will ensure the status-quo prevails and Colombia will continue to re-pay debts and welcome FDI and portfolio investment to the country. In addition, monetary policy tightening will be at its final stages with y/y inflation on a gradual converging path to the target range. Therefore, though we anticipate volatile and challenging market conditions in H1-2022, we think H2-2022 will bring calm to the markets, once we know congress and presidential winners, have a better idea of how high international and domestic interest rates are likely to go, and a clearer idea of the possible labour and fiscal reform that the next president will try to pass before congress.

Mexico—The Latest Employment Quarterly Survey Shows a Re-Composition in the Labour Market

Luisa Valle, Deputy Head Economist

+52.55.5123.0000 Ext. 36760 (Mexico)

lvallef@scotiabank.com.mx

Miguel Saldaña, Analyst

+52.55.5123.0000 Ext. 36760 (Mexico)

msaldanab@scotiabank.com.mx

As of the last quarter of 2021, the labour market has recovered after the onset of the pandemic in the beginning of 2020. Although the unemployment rate is higher (3.7% Q4-2021 versus 3.4% Q1-2020), this is explained by an increase in the working age population that has not been matched by the rise in the economically active population (EAP) or the employed population. In percentage terms, the population over 15 years of age (working age) increased 3.5% while the EAP increased 3.06% (participation rate 59.7%) and the employed population increased only 2.82%.

By economic activity, employment expanded in practically all sectors, except for transportation, communications, mail and storage; miscellaneous services, and government and international organizations (-0.71%, -0.25% and -10.03%, respectively). It is worth noting that, despite the effects of the pandemic on contact-intensive activities, the percentage of people employed in the tertiary sector increased from 60.9% to 62.4%, with larger rises recorded for professional services, commerce and social services.

By gender, the economically active population grew by 2.87% for women, while that of men grew by 3.19%. With a higher population growth, women continue to work less than men, which is reflected in a lower participation rate (45% women versus 76% men) in 2021 Q4. Women also worked fewer hours (38.4 hours per week, while men worked 45.5 hours. In addition, the unemployment rate is higher for women (3.8%) than for men (3.6%). Women account for more than 70% of the population working in the tertiary sector, the sector most affected by the pandemic, which is one of the reasons why the recovery in the labour market has been better for men than for women. Meanwhile, the proportion of women working in informal jobs (54.8%), which typically pay less and are subject to poorer working conditions, is higher than that of men (49.1%).

In the aftermath of the pandemic, there has been a re-composition in the labour market, which led women to gain participation in mostly male-dominated sectors. As of the first quarter of 2020, women’s participation in the primary sector was 11.8%; by the fourth quarter of 2021, participation increased to 14.2%. And in transportation and communications, women’s participation increased from 12.53% to 14.06%.

In conclusion, although the labour market has maintained a good pace of job creation since the first shutdown, this pace has not been enough to return to a pre-pandemic unemployment rate. In addition, labour market conditions for women are still far from closing the labour gap.

Peru—A Truce of Sorts

Guillermo Arbe, Head Economist, Peru

51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

After weeks of exchanging threats of impeachment and accusations of planning coups, leaders of the Executive and Congress called for a ceasefire on February 16. María Alva, who presides over Congress, denied allegations that the opposition had been meeting to impeach the president, and decided to calm the political waters by expressing a willingness to work with the Executive to “see what we can do together for Peru”. Two hours later, the Head of the Cabinet, Aníbal Torres, stated that he agreed with Alva, and even apologized to Congress if any of his “expressions” had exacerbated tensions between the two. Hopefully, neither of the two had their fingers crossed at the time that they made their statements.

Given the levels of polarization in the country, and the different mindsets that prevail in the two branches of government, one can wonder about the duration of the truce. But, for the time being at least, the intentions of the two parties are believable, in part because both sides know that neither has the power to close the other down.

Given the truce, it has become more likely, but not certain that the Torres Cabinet will receive the vote of confidence on March 8, when the Cabinet is scheduled to appear before Congress. What is more intriguing is whether the Executive and Congress are capable of forging a working relationship going forward. This would require a significant change in behaviour, and a large quota of goodwill, on the part of both branches of government.

It seems much longer, but the Torres Cabinet has only been in place for ten days now (since February 8), and a lot of questions remain regarding its composition. Minister Torres himself seems to have been appointed mainly because in his prior position as Minister of Justice he had become the most vocal and loyal defender of the Castillo Regime. Other Cabinet designations seem to have been made with an eye on appeasing enough parties in Congress to ensure that the Cabinet will get the confidence votes. President Castillo seems to have been especially keen on appeasing Perú Libre, four members of which now hold Cabinet positions. This represents a shift away from the more moderate leftist group, Juntos por el Perú, in favour of the more radical leftist party.

Significantly, the Ministry of Finance remains in capable hands. Oscar Graham, who initially replaced Pedro Francke during the ephemeral four-day Héctor Valer Cabinet, is well known at the Ministry of Finance, where he spent twelve years, mostly as General Manager of Financial Markets and Private Pension Funds. He is even better known at the BCRP, where he has worked in various positions for a total of 29 years. His 40 years of combined experience at the central bank and Ministry of Finance is a strong CV and portend that the Ministry of Finance will continue to provide policy reliability and continuity.

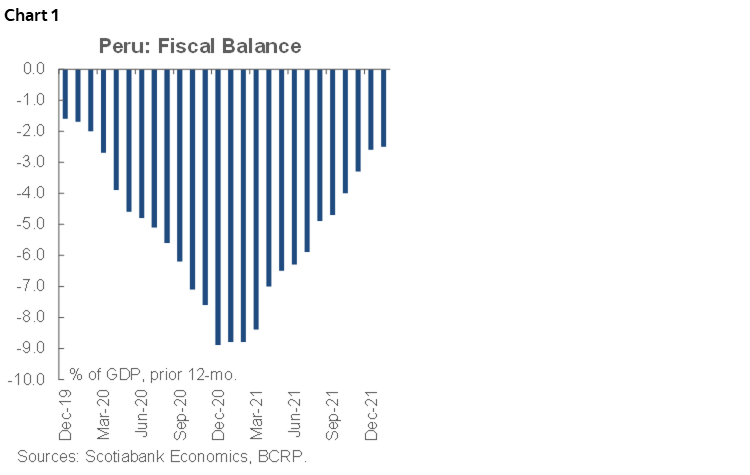

Since his designation, Minister Graham has met with the BCRP and the Banking Superintendent for policy coordination. In early statements to the press, Minister Graham has stressed that fiscal accounts will be prudently managed, building on the decline in the budget deficit over the course of 2021 (chart 1), and that the MEF is working on new fiscal rules for 2023–2026 to be sent to Congress in March, probably meaning a return to the pre-COVID-19 fiscal deficit rule of 1% of GDP.

Minister Graham has also stated his intention to encourage public investment, including modifying the regulations for the Territorial Development Fund (Fondo Invierte para el Desarrollo Territorial, FIDT) to improve the efficiency in its use by regional and local governments.

With Minister Graham now at the helm, the Ministry of Economy and Finance (MEF) also vetoed a Congressional Bill awarding a nearly unpayable PEN 42 bn to past participants in the defunct FONAVI housing fund, and suggested paring down the plan to PEN 6.6 bn.

Though it is early in his tenure, we are waiting to see if Minister Graham will back his words that private investment needs to be promoted as the main driver of sustainable growth with policy. There are also several topics, many coming from the previous MEF administration, that Minister Graham has yet to address, including an investment schedule for new infrastructure projects, private pension fund reform, tax reform, increasing the minimum wage, and increasing the fiscal stabilization fund. In our view, he is less likely to pursue tax reform or a reform of the pension fund system than Pedro Francke was.

Minister Graham’s designation suggests that President Castillo is relying on properly managed economic institutions, even as Castillo uses non-economic portfolios to build political support. However, Minister Graham’s influence within the Cabinet and his relationship with Cabinet Head Aníbal Torres is not clear. Nor is it clear whether Minister Graham will have enough influence to ensure adequate investment by other ministries, in particular the ministries of Transportation, of Health, and of Education, which are key in terms of government infrastructure investment.

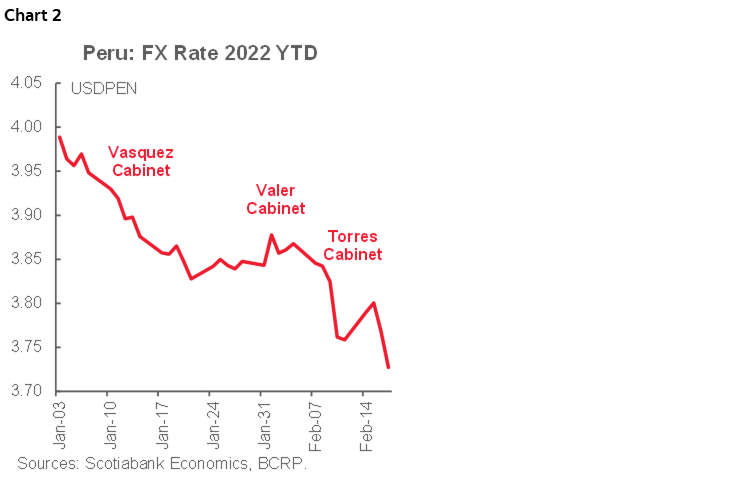

Markets have taken recent events in Peru quite well, considering the bout of instability early in the month. The FX rate appreciated from USDPEN 3.85 on February 7 to 3.72 on February 17, as inflows from mining companies converting USD revenues to PEN to pay taxes outweighed political concerns (chart 2).

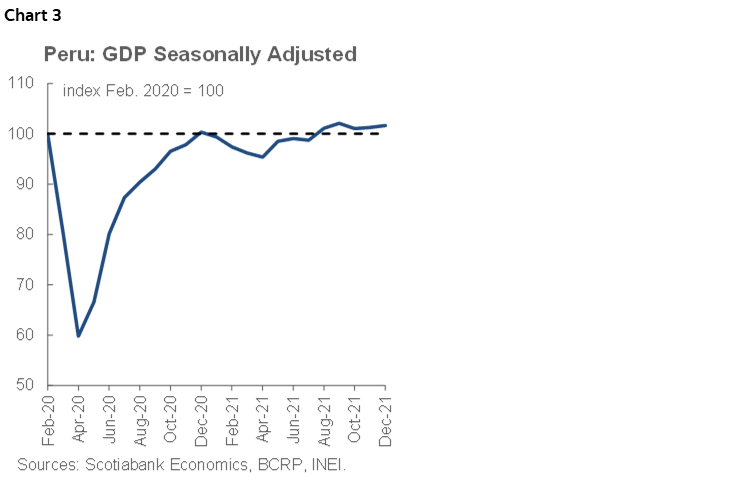

Macro indicators have been mixed. GDP growth for 2021 came in at 13.3%, as expected. Growth in December was up 0.4% m/m (GDP contracted in November), but only a weak 1.7% y/y, which is something we will probably have to get used to seeing in 2022. Nevertheless, output returned to pre-pandemic level earlier than initially expected (chart 3). The fiscal deficit (12-months aggregate) hovered around 2.5% of GDP in January, continuing a strong downward trend. There is good and bad in the number. On the good side, tax revenue rose a healthy 11% y/y. This should continue, as high metal prices persist. At the same time, public investment declined 19% y/y, the fourth consecutive month of decline, which suggests that high investment growth early in the Castillo Government was likely inertial, whereas current investment figures reflect the real government capability to invest. Thus, overall, in 2022 Peru continues to show a dual personality, mixing the good with the bad.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.