ECONOMIC OVERVIEW

- Chilean and Mexican holidays keep things light in Latam next week, with economic activity data out of Brazil, Colombia, and Peru and the BCB’s likely rate hold standing as the regional highlights, overshadowed by the Fed’s likely rate cut on Wednesday that will draw the market’s attention (with BoJ, BoC, and BoE decisions also due).

- In today’s report, the teams in Mexico, Chile, and Peru discuss their latest expectations for their domestic economies, with more easing expected from Banxico, some differences in opinion with the BCCh, and some small GDP tweaks against a stronger PEN view, in that order. Our colleagues in Colombia go over the flurry of fiscal and financing developments of recent weeks.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico and Peru.

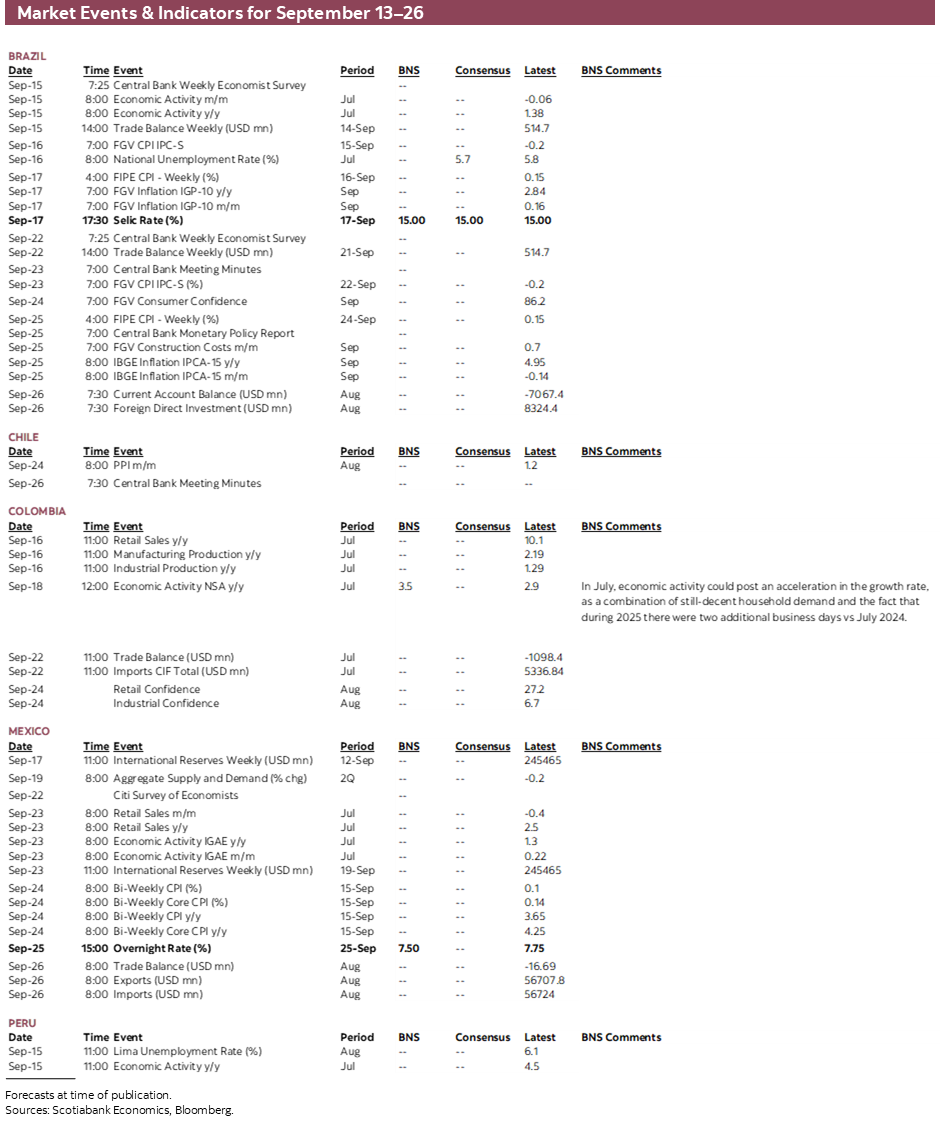

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period September 13–26 across the Pacific Alliance countries and Brazil.

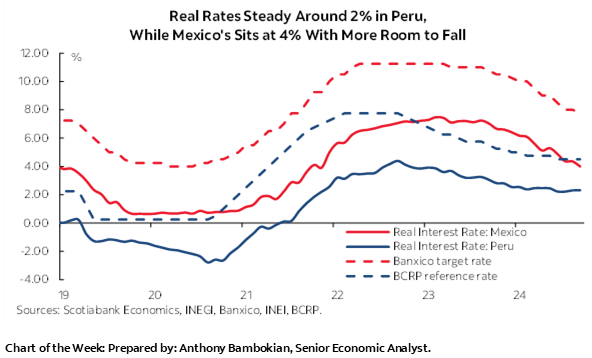

Chart of the Week

ECONOMIC OVERVIEW: FORECAST REVISIONS AHEAD OF G10 RATE DECISIONS

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Chilean and Mexican holidays keep things light in Latam next week, with economic activity data out of Brazil, Colombia, and Peru and the BCB’s likely rate hold standing as the regional highlights, overshadowed by the Fed’s likely rate cut on Wednesday that will draw the market’s attention (with BoJ, BoC, and BoE decisions also due).

- In today’s report, the teams in Mexico, Chile, and Peru discuss their latest expectations for their domestic economies, with more easing expected from Banxico, some differences in opinion with the BCCh, and some small GDP tweaks against a stronger PEN view, in that order. Our colleagues in Colombia go over the flurry of fiscal and financing developments of recent weeks.

Holidays and relatively empty data calendars await in Latam next week, with global markets laser focused on the Fed’s rate decision next Wednesday to drive broad trading sentiment. Economic activity data for July out of Brazil, Colombia, and Peru are the data highlights in the region, joined by the BCB’s midweek announcement of a likely hold, in contrast to bare schedules in Mexico and Chile, whose markets are closed on Tuesday and Thursday/Friday, respectively, due to national holidays.

Like the Fed, the BoC is expected to roll out a 25bps rate cut on Wednesday after Tuesday’s CPI release, but the BoE and BoJ are seen leaving policy rates steady at their Thursday and Friday announcements. With few doubts over what cuts or holds central banks (the BCB included) will deliver next week, attention will fall on guidance meetings over the balance of 2025 and early-2026 (particularly from the Fed). The U.K. and Japan also release national CPI data next week, with other key ex-Latam releases including Chinese retail sales and industrial production, U.K. and Australian employment, and U.S., Canadian, and U.K. retail figures.

This week, Scotiabank Economics updated its projections for the globe’s major economies, focusing their attention on the conflict that central banks may be facing between weak growth and high inflation, with the team now expecting considerable near-term easing from the Fed and some additional cuts by the BoC.

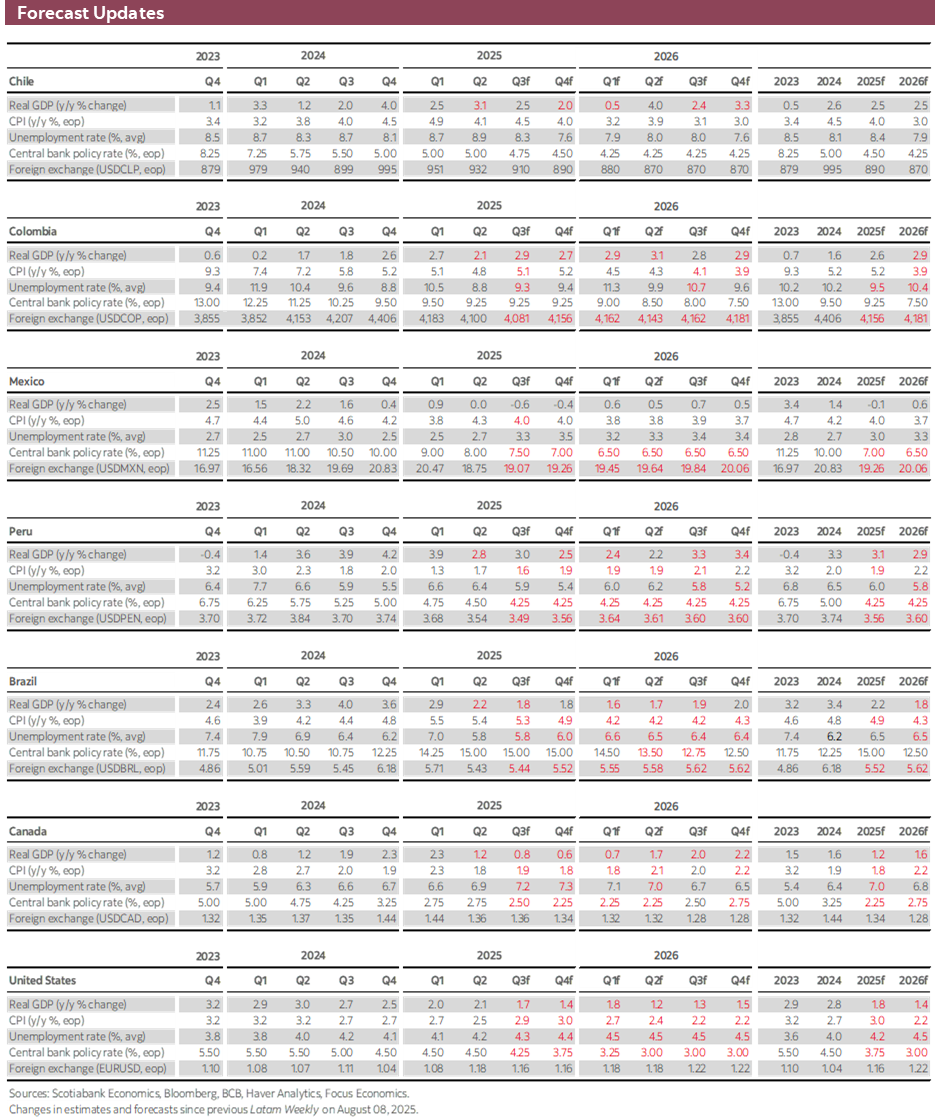

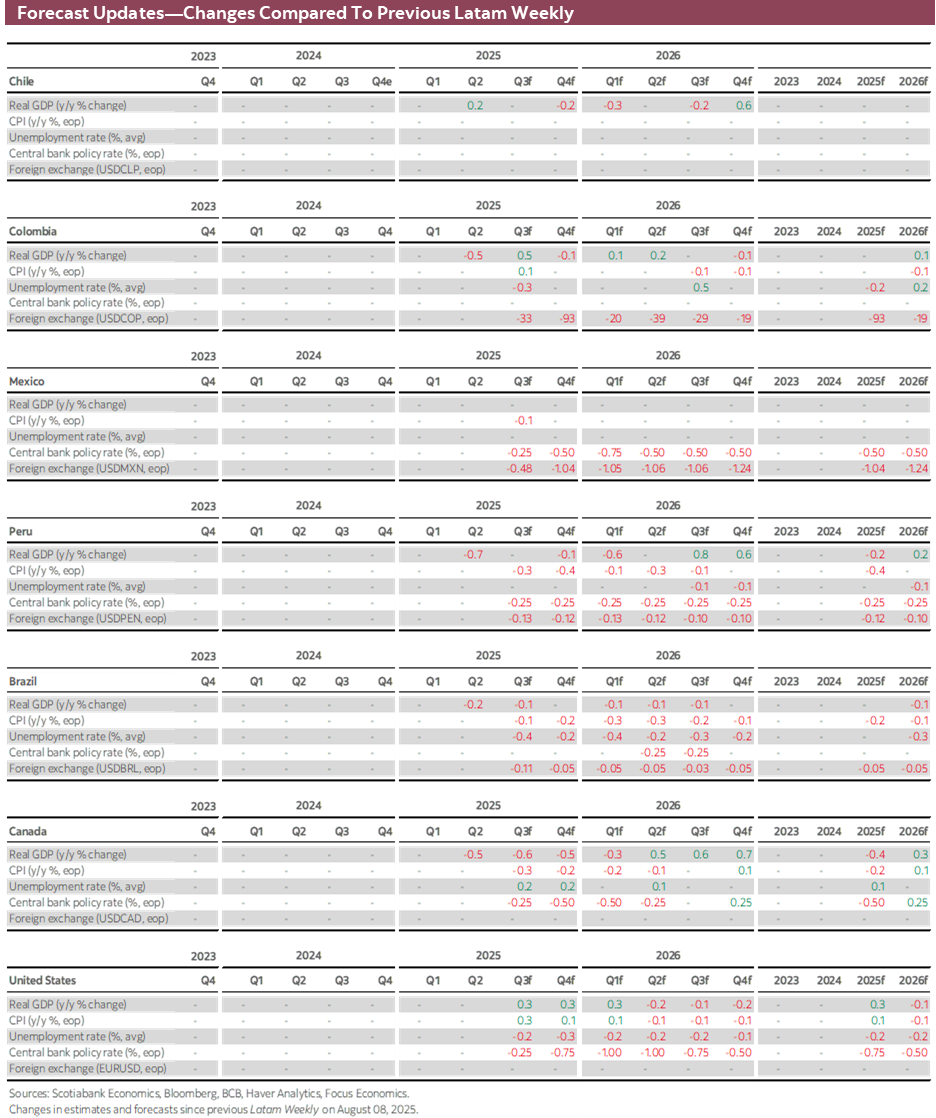

Our economists in Latam have also made some small adjustments to their projections for their respective economies when compared to early-August forecasts. Outside of Peru (more on this below), GDP growth forecasts for the Pacific Alliance were left practically unchanged with Mexico still estimated to marginally contract in 2025 while Colombia and Chile record ~2.5% expansions this year—although the former picks up speed next year while the latter holds.

In today’s report, the team in Lima discuss their updated projections, which include a lower forecast for 2025 GDP growth from 3.3% to a still solid 3.1%. The drivers of this change are not too worrisome, however, as a temporary iron ore mine closure and other exports hiccups resulted in a softer Q2 than expected. A small scaling back in fiscal expenditures to comply with the fiscal rule is also a tiny drag versus their previous baseline. The outcome for 2026 is a bit trickier as much may depend on the lead-up to and result of the April elections, but growth is still seen around ~3% in spite of electoral uncertainty. For now, we don’t anticipate additional BCRP rate cuts, while our economists have made significant revisions to their PEN exchange rate forecasts owing to strong fundamentals.

From Chile, we compare our expectations to the latest views of the BCCh presented in this week’s Monetary Policy Report. We are generally aligned with the central bank in its expectations for inflation at end-2025 at 4.0% though we think the 3% target will be reached somewhat sooner than officials anticipate. On the other hand, we think the BCCh’s outlook for consumption growth is a bit too rosy given challenging labour market conditions. The latter may reflect structural adjustments related to rising labour costs—of the kind on which policy rates are of little influence.

A flurry of fiscal and financing developments have taken the spotlight in Colombia in recent weeks, as covered by our local economists in today’s Weekly. Discussions over the 2026 Budget are ongoing between the government and Congress, with next year’s fiscal plan due to be finalized next week. The government is banking on a series of tax initiatives to lift revenues, though we believe they may be overestimating the success of these measures in Congress—as suggested by FinMin Avila already floating concessions on Friday. The team also go over the multitude of bond repurchases, EUR debt issuance and the chance of additional issuance in international markets in coming weeks. At home, bond exchanges and modifications to auction sizes have also been rolled out.

Finally, with a closer view to next week’s events (the Fed), the team in Mexico discuss their new Banxico forecast that now shows the local central bank cutting by an additional 75bps by end-2025 to close the year at 7.00%. The forecast change from 7.50% end-2025 policy rate predicted this time last month owes to a large degree to the important shift in Fed expectations in recent weeks as a result of underwhelming U.S. data (particularly on the employment front), with our Fed call changing from no cuts in 2025 to three cuts over the same amount of remaining meetings this year to 3.75%. We’ll see whether next week’s Fed decision confirms our expectation, but U.S. policy aside, Mexico’s central bank seemingly remains on a steady policy easing path with multiple cuts in store this year.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—We Expect Another Policy Rate Cut, Just Two Days After the Presidential Runoff

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

Key Takeaways From the Monetary Policy Report vs. Scotiabank’s View:

- Investment is projected to grow by 5.5% in 2025 and 4.3% in 2026 (table 1). After several Monetary Policy Reports (IPoMs) in which the central bank showed limited conviction about the mining investment boom, it now acknowledges that both recent and expected investment materialization, along with the sharp increase in capital goods imports, warranted a revision. At Scotiabank, we have been expecting total investment to expand by 6.0% in 2025 and 3.5% in 2026. It is worth noting that a large share of mining investment is aimed at maintaining rather than expanding mining production levels, unlike the early-2000s mining boom.

- Consumption is projected to expand by 3.0% in 2025, a figure we currently see as difficult to achieve given the ongoing weakness in the labour market, which still needs a few more quarters before showing meaningful improvement. We maintain our forecast of 2.5% consumption growth for this year.

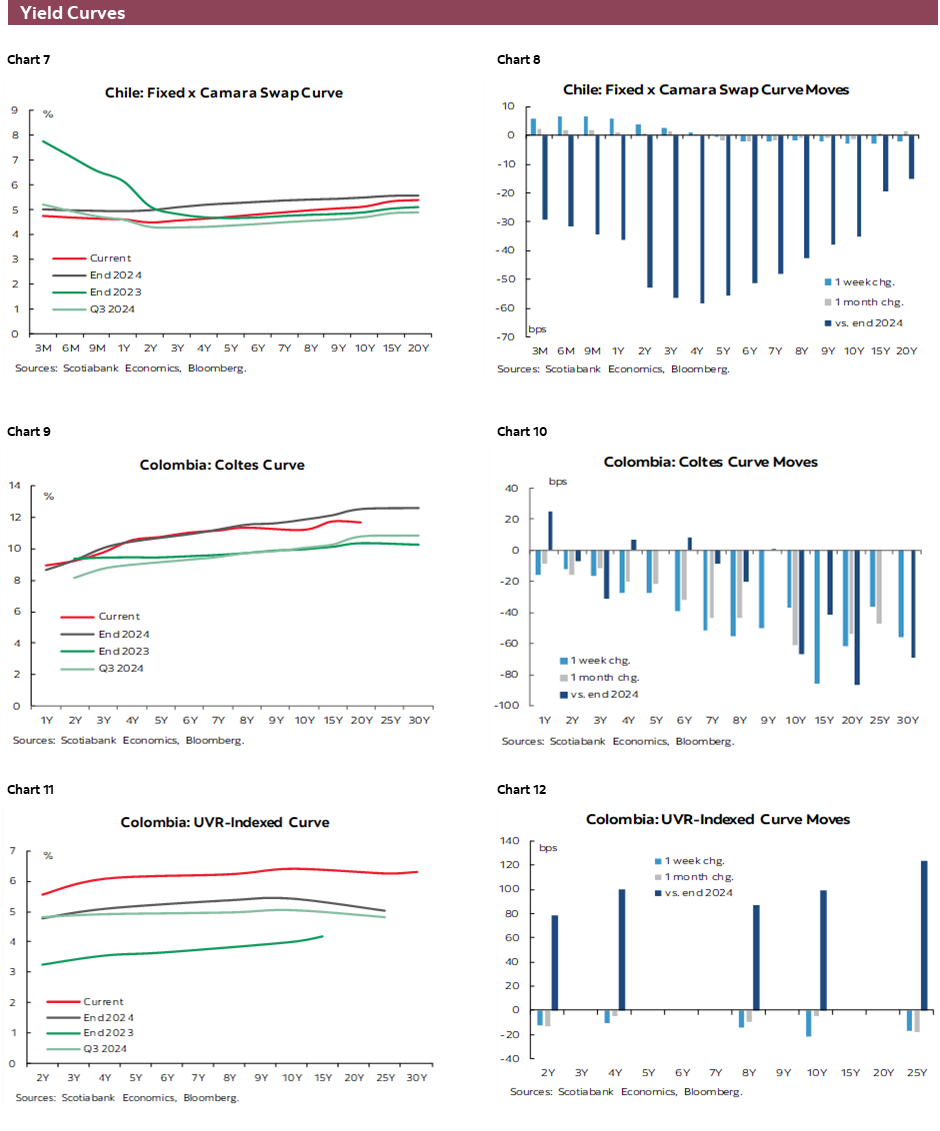

- Real Exchange Rate (RER) is expected to appreciate. After a peculiar depreciation forecast in the June IPoM, the central bank now anticipates real appreciation over the projection horizon. At Scotiabank, we expect the exchange rate to end 2025 at CLP 890, consistent with a RER around 101 (base 1986=100), supported by: (1) strong copper prices ending 2025 at USD 4.5/lb or higher; (2) local monetary policy in a “cautious stance”, widening the rate differential with the Fed, which the BCCh pencils in will cut 100bps over the next four quarters; (3) a favourable political environment, with a new congressional composition facilitating administrative and legal reforms from the start of the next administration in March 2026; and (4) a renewed carry-trade dynamic in favour of the peso, potentially breaking the psychological barrier that marked the beginning of FX reserve accumulation. We expect the peso’s appreciation to accelerate after the first-round presidential election in mid-November, when a new congressional makeup will also be known.

- Inflation is projected at 4.0% at end-2025, converging to 3.0% by Q3-26. We agree with the 4.0% forecast for this year, though we see the convergence to 3.0% happening slightly earlier than the central bank. Moreover, we anticipate a September CPI print significantly above the forward-implied projection in markets (0.38%), in line with the IPoM’s 0.55% m/m forecast. This would be driven by a notable rebound in clothing and footwear (especially men’s), seasonal increases in food, some transport services, and a modest rise in gasoline prices. The core CPI (ex-volatiles) projection for September is 0.62% m/m, reflecting elevated inflation in both goods and services—precisely those upside surprises acknowledged by the central bank in its September statement.

- Short-term activity remains volatile, particularly ahead of the first-round presidential election. August GDP is expected to come in around 2.0% y/y, while September GDP—to be released two weeks before the election—is projected at 4.0% y/y, in line with our base case.

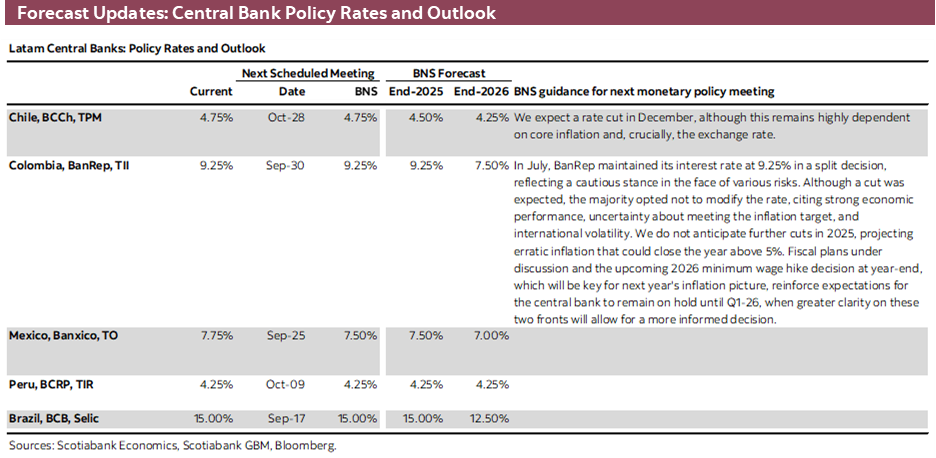

- The policy rate path reflected in the IPoM’s rate corridor includes a cut at the December meeting (to 4.50%) and another in July 2026 (to 4.25%). Although the December meeting is scheduled for the 16th, daily rate data suggest the corridor assumes a 25bps cut at that meeting, followed by another in July 2026. This implies a delayed convergence of the policy rate to its neutral level, which would not be reached before 2027. However, we expect the central bank to revise its estimate of the neutral rate in the December IPoM, likely to a range of 3.75%–4.75%.

- The IPoM assumes real public spending growth of 1.2% in 2026, consistent with the Q2 Public Finance Report and planned expenditures. Were the Budget Law due on September 30th to include a higher public spending growth figure in relation to the central bank’s baseline scenario, it would have upside implications for the BCCh’s projected policy path.

- The labour market is being affected by accelerated structural adjustments due to rising labour costs. A new IPoM box highlights the negative impact of the minimum wage hike, which has led many firms to fast-track efficiency and transformation processes. The report includes useful quantifications of the negative impact on total employment. From a monetary policy perspective, this aligns with our view that labour market weakness should not be interpreted as a traditional employment gap where monetary policy plays a central role. The cyclical component of labour market weakness attributable to tight monetary policy appears limited. Therefore, it should not weigh as heavily as the activity gap or core inflation in guiding future policy rate decisions.

Colombia—Fiscal and Financing Recap

Jackeline Piraján, Head Economist, Colombia

+57.601.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Valentina Guio, Senior Economist

+57.601.745.6300 Ext. 9166 (Colombia)

daniela.guio@scotiabank.com

It is once again a good time to take stock of Colombia’s fiscal matters, as recent weeks have brought some developments in both the above-the-line and below-the-line accounts.

ABOVE-THE-LINE ACCOUNTS: The government is currently discussing the 2026 Budget proposal with Congress. The first stage of negotiations has a deadline of September 15th, by which Congress must decide on the total budget amount. The government has proposed a COP 557 trillion budget for the General Government, which specifically regarding the Central Government increases the spending assumption compared to what was presented in the Medium-Term Fiscal Framework (MTFF) in mid-June. In this context, primary spending for the Central Government is expected to rise by COP 18.2 trillion (~1% of GDP) versus the MTFF-2026, based on assumptions of higher tax revenues and lower interest payments. As a result, the estimated primary deficit for the Central Government has increased from 2% of GDP in the MTFF-2026 projection to 2.4% in the current budget proposal.

The technical staff at the Ministry of Finance has stated that, despite the deterioration in the primary deficit, there is a commitment to maintain the total fiscal deficit projection stable at 6.2% of GDP. This deficit target depends on raising additional fiscal revenues through a Financing Law (Tax Reform), which aims to collect the equivalent of 1.4% of GDP from new sources. The tax reform was released on September 1st and includes reasonable initiatives, although they may be challenging to pass. Even if some measures are approved, we do not expect the additional fiscal revenue to be as strong as the government projects. The most recent news regarding the budget is the government floating that it’s open to reducing its tax revenues estimate by COP 10 tn, with a corresponding COP 10 tn reduction to its proposed budget (at COP 547 tn instead of 557 tn), though this has not been formalized as of writing.

In parallel, we are currently in the personal income tax filing season. However, the government’s cash balances in its BanRep account are not increasing as usual this year, which is something to monitor closely—especially considering that the government typically experiences significant payment outflows at the end of the year.

BELOW-THE-LINE ACCOUNTS: There have been several movements that deserve to be outlined:

Operations in International Markets:

A. On August 11th, Colombia announced the repurchase of USD 2.96 billion in global bonds maturing in 2042, 2045, 2049, 2051, and 2061, which were trading at a discount. According to the Ministry of Finance (MoF), this operation was carried out using foreign and local currency cash buffers.

B. On Wednesday, September 10th, there was an issuance of EUR 4.1 billion in bonds maturing in 2028, 2032, and 2036, with coupons of 3.75%, 5.00%, and 5.625%, respectively. These two operations suggest a re-expression of floating debt. According to the MoF, part of the proceeds will be used to cover budgetary needs, while another portion will be allocated to liability management operations.

C. During the first week of September, six international banks purchased USD 5.4 billion in global bonds to hedge a Total Return Swap (TRS) structure with Colombia. The potential structure could involve these banks paying Colombia a portion of the return on this basket of assets, while Colombia has yet to disclose the payment terms it will set with the banks.

D. A couple of weeks ago, the MoF convened the Comisión Interparlamentaria de Crédito Público to request authorization to issue USD 7.5 billion in international markets. The Commission has not yet approved the transaction. It was reconvened for a second vote on September 1st, and if no decision is made within 30 days, the government will interpret this as a negative but non-binding opinion and may proceed with the issuance. Therefore, potential new debt supply could emerge in the coming weeks, once the commission’s debate period expires.

Operations in the Domestic Market:

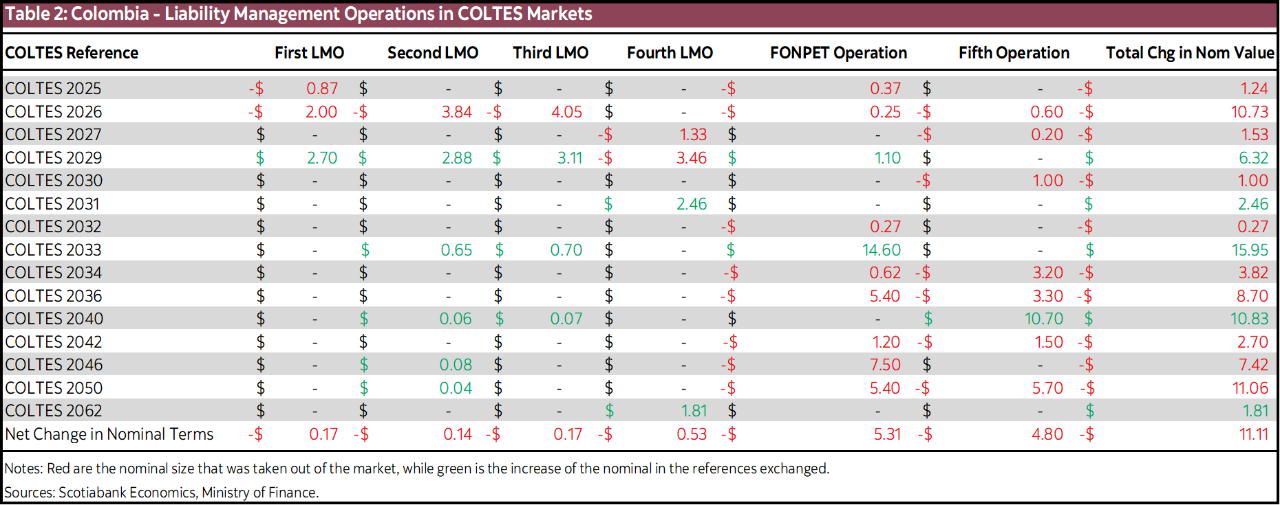

A. The MoF carried out five liability management operations aimed at exchanging discounted bonds for bonds closer to par. The changes in outstanding debt resulting from these operations are summarized in table 2:

B. Movements in MoF portfolios: The Ministry of Finance (MoF) reported COLTES purchases, accumulating a portfolio of COP 14 trillion by the end of July. In August, they sold COP 2 trillion.

C. On Friday, September 5th, and Monday, September 8th, there were some after-market movements in the FX and bond markets suggesting the possible structuring of a collateralized loan (this information has not yet been confirmed). The hypothesis is that fresh TCO bonds were issued for COP 26 trillion (1.4% of GDP), which, together with a basket of COLTES (estimated at COP 14 trillion/0.8% of GDP), now form the collateral for a loan. It is still unclear whether the loan will be fully disbursed in the local market. This structure is expected to mature in less than one year. The market is still awaiting any official disclosure from the MoF, as the potential size of the operation is COP 40 trillion (~2.2% of GDP).

D. Auction sizes have changed, but we expect an extended calendar. The MoF decided to reduce the nominal auction size to COP 800 billion biweekly (previously COP 1 trillion), COP 400 billion biweekly in UVRs (previously COP 700 billion), and COP 900 billion weekly in TCOs. This sustained debt supply aims to meet the COP 58 trillion auction target and also to pre-finance part of the 2026 budget, for which the initial auction target is COP 65 trillion. In previous year’s, the regular auctions calendar ends around October, however in 2025 we expect a extended period depending on the MoF.

All in all, the most significant movements involve structures maturing in less than one year. In the meantime, we will continue monitoring any disclosures regarding recent operations, as for now, we only have clues based on visible market movements.

Mexico—Shifting Fed Views Shift Banxico Outlook

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Next week, global markets—including Mexican participants—will be closely watching the Federal Reserve’s policy decision, which is expected to shape the trajectory of interest rates worldwide. Besides the rate announcement, the Fed will release updated macroeconomic projections and its expected path for the federal funds rate, offering clearer signals on the direction of monetary policy.

This decision comes amid elevated uncertainty. Until recently, markets lacked clarity on the Fed’s stance, largely due to the ambiguous effects of tariff policies promoted by the Trump administration—particularly on prices and the labour market.

However, two recent developments have significantly shifted expectations: the release of July’s nonfarm payrolls, which came in below forecasts, and sharp downward revisions to previous months’ data. Additionally, Jerome Powell’s speech at Jackson Hole explicitly opened the door to a potential rate-cutting cycle.

As a result, and with inflationary pressures easing due to tariffs, markets are now pricing in at least two rate cuts this year.

In Mexico, this shift has also impacted expectations for Banxico’s policy rate trajectory for the remainder of 2025 and into 2026. Until recently, analysts considered the central bank was nearing the end of its easing cycle. However, the prospect of a more flexible Fed has created room for Banxico to continue lowering rates in tandem, helping preserve the interest rate differential and support financial stability throughout the cycle.

Notably, this shift is occurring despite persistent inflationary pressures at home, particularly in core inflation. If Banxico continues cutting rates, it could move toward a neutral monetary stance, even as market inflation expectations remain anchored around 4%. That said, we recognize an upward inflation risk balance, which could deteriorate in the coming months due to new tariff measures, greater persistence in core components, or a rebound in agricultural prices.

In line with this outlook, we have adjusted our forecasts for Banxico’s policy rate, projecting a rate of 7.00% for end-2025 and 6.50% for end-2026.

Peru—Stability As Far as The Eye Can See… Or Until the April 2026 Elections Anyway

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

We have made a number of changes to our 2025 and 2026 forecasts. Some are tweaks, and some are more significant. However, none of the modifications change the central message of a country showing moderate growth, robust macroeconomic balances, and general price stability.

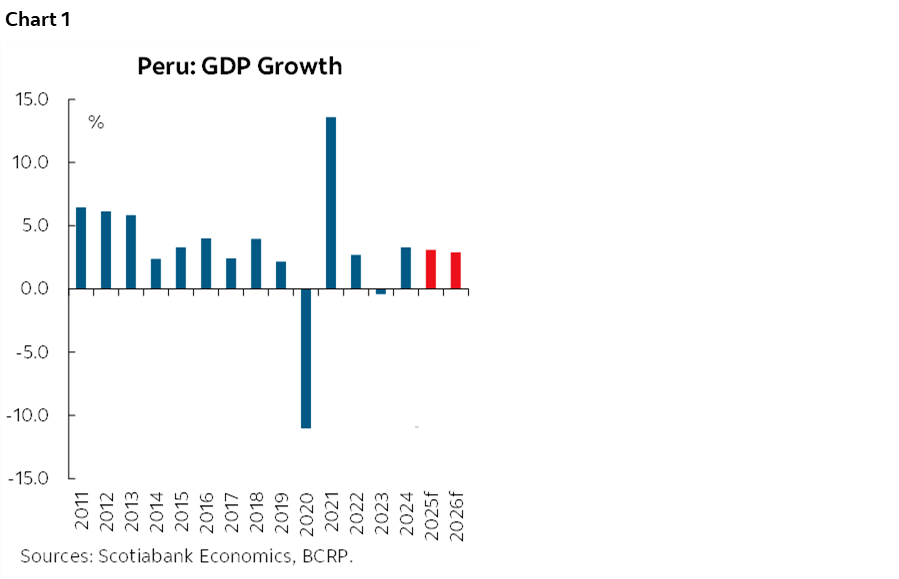

Let’s start with GDP. We are lowering our GDP forecast for 2025 from 3.3% to 3.1% (chart 1). There are two reasons for this. The first is the adjustment we need to make as GDP growth in Q2 came lower than we had anticipated, at 2.8%, YoY, rather than 3.5%. The relatively good news is that this lower reading was linked to extraordinary circumstances, rather than a weakening economy. In Q2, Peru’s largest iron mine, Shougang, was closed down temporarily for technical reasons (the impact of the closure will also spill into Q3). As a result of this, and other minor issues with copper production, export volume fell 0.6%. At the same time, Peru experienced a sharp increase in imports (12.7% in the quarter in volume). The latter is not necessarily a bad thing, as capital goods imports rose equally sharply in Q2. The increase in capital goods imports goes in hand with the 9.0% YoY growth in private investment, which is healthy.

The second reason for our mild downward GDP adjustment is more forward looking. In a bid to reduce the fiscal deficit so as to comply with the fiscal rule of 2.2% of GDP fiscal deficit for 2025, and 1.8% for 2026, the Minister of Finance, Raúl Perez-Reyes, announced the government’s intention to reduce public expenditure growth going forward. We see complying with the 2.2% rule for 2025 as something that is within reach, given that the deficit stood at 2.4% in July, although the main factor behind improving fiscal accounts is strong fiscal revenue growth, rather than lower spending growth (chart 2).

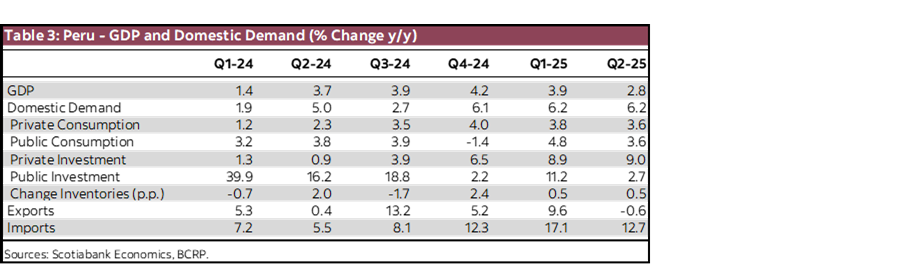

The reality of GDP growth is that the economy is growing in a moderate and sustainable fashion, and this growth is increasing, driven by private investment and domestic demand. Note that domestic demand has increased by just over 6% for three consecutive quarters now. Thus, our modest forecast adjustment is not indicative of underlying weakness, but, rather, of temporary issues as well as a transition in the drivers of growth from the public sector to the private sector (table 3).

For 2026, we have tweaked our forecast up from 2.8% to 2.9%. The forecast increase would have been greater if not, once again, for the explicit intention of the government to limit spending growth. This intention is reflected in the 2026 budget, in which the government is targeting a spending increase of only 2.2%. The slack will be compensated by greater private sector spending, with private consumption rising 2.6%, and private investment rising 3.5%. These are not bad figures, considering that 2026 is an election year. We do not presume an elections outcome, but, rather make the simple assumption that economic management and political turbulence under the new administration will not be better, but also not worse, than it has been over the past decade. This assumption will be tested by the election results. If a government that hurts investor confidence is elected, private investment is likely to suffer. However, if a business-friendly government is chosen, together with a reasonable Congress, then, with the metal prices environment that currently exists, private investment could potentially increase dramatically. The reality is likely to be somewhere in between.

Monetary Policy and Inflation Forecasts

We recently changed our inflation forecasts for 2025 from 2.3% to 1.9%, and maintained inflation expectations at 2.2% for 2026 (see here). At the same time, we lowered our terminal reference rate forecast to 4.25%. Is it possible for the reference rate to be reduced further, to, say, 4.0%? Yes, it is possible. However, for this to happen, inflation expectations would likely need to fall below 2%, which is something that has only happened once over the last twenty years, during COVID in 2020. Inflation expectations become very sticky to the downside when it reaches 2%.

The other option would be for the BCRP to reduce its neutral rate definition from 2.0% currently to something lower. This is not impossible, as there has been a period in which the neutral rate was considered to be 1.50%. But, this scenario would need to materialize first for us to consider it in our forecasts.

Exchange Rate

Finally, our most significant change, perhaps, has to do with the PEN. We are lowering our 2025 year-end PEN FX forecast from 3.68 to 3.56. The change is all the more significant as four months ago our forecast was 3.78. For 2026, our new year-end forecast is 3.60, down from 3.70.

A note of caution, however. Although we needed to revise our outdated forecasts without delay, we are aware that we are doing so before the Fed decision on September 17th, 2025, which could conceivably lead to the need for a new revision.

For the moment, everything seems to be going favourably for the PEN (charts 3 and 4). Metal prices are high, Peru has a record trade balance, offshore inflows into PEN assets are favourable, and the USD is weak. One could construe a scenario which warrants more favourable forecast. However, there are elections on the horizon, and typically the FX rate is affected to some extent the closer we come to the elections.

Plus, PEN fundamentals have been almost too good, and good scenarios don’t last forever. It’s hard to conceive terms of trade continuing to improve in 2026 as they did in 2025. Peru’s import prices are at levels that seem unsustainably low. The wind behind high precious metal prices could slacken next year. And the world is starting to show signs of slowing, which is never good for Peru export prices.

Finally, there is the BCRP. Peru’s central bank has stayed uncharacteristically sidelined during much of the recent PEN appreciation period. It is not clear when the BCRP will begin to draw the line regarding the PEN trend, but precedent over the past 20 years suggests it may be soon.

In a nutshell, then, a strong PEN is helping to reduce inflation. Low inflation is helping wages to rise in real terms. Higher wages are supporting consumption and housing demand, which in turn, together with stable interest rates, is conducive to private investment growth. This virtuous cycle is reliant, ultimately, on metal prices remaining high. As long as they do so, Peru’s situation of moderate growth with robust macro accounts and general price stability, should be sustainable.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.