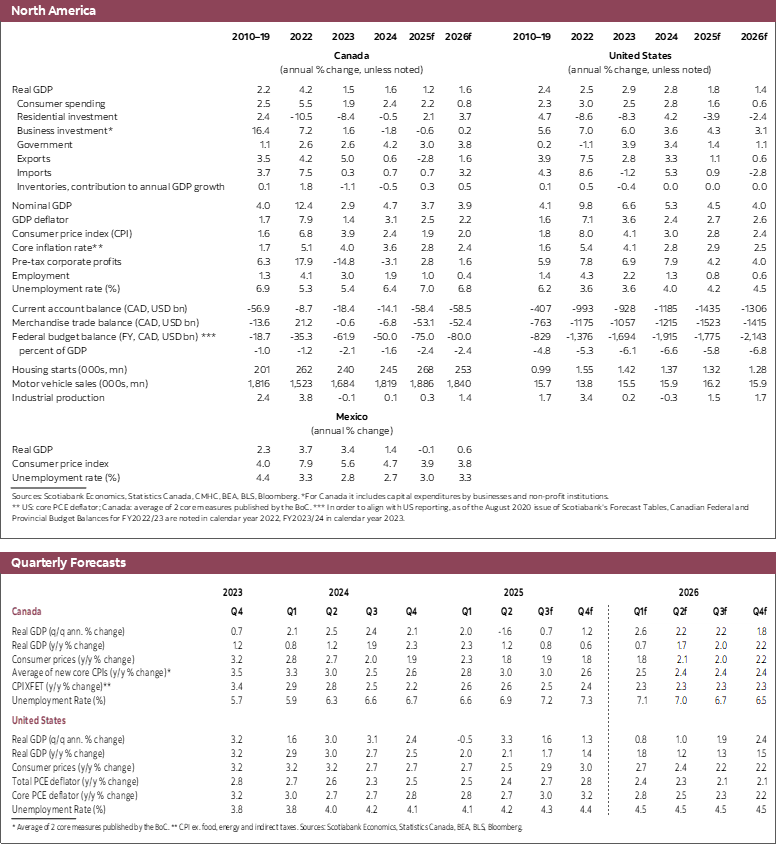

- The conflict between weak growth and high inflation is on full display. The Bank of Canada and Federal Reserve should be cutting interest rates based on the growth outlook, but the strength of inflation suggests otherwise.

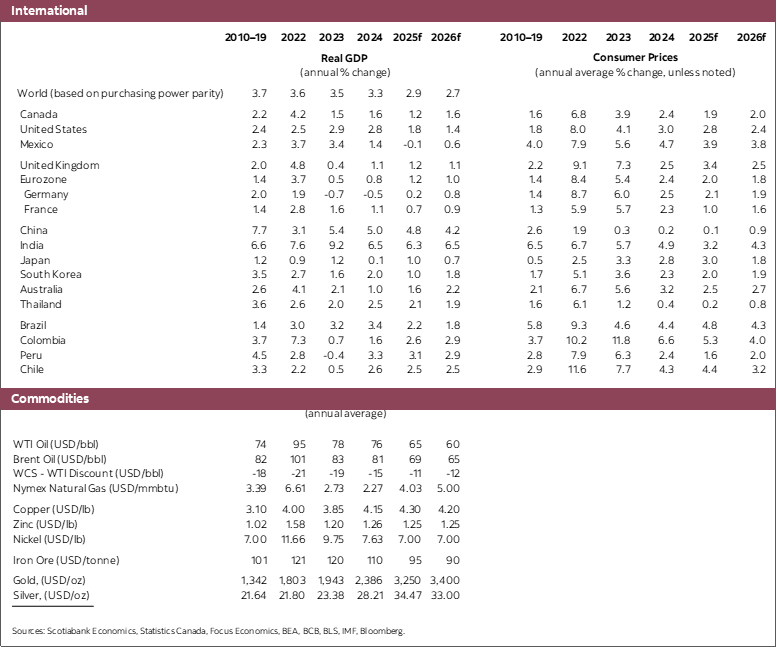

- We expect U.S. growth to moderate from 1.8% this year to 1.4% next year, and Canadian growth to accelerate from 1.2% this year to 1.6% as fiscal policy acts to boost our growth potential.

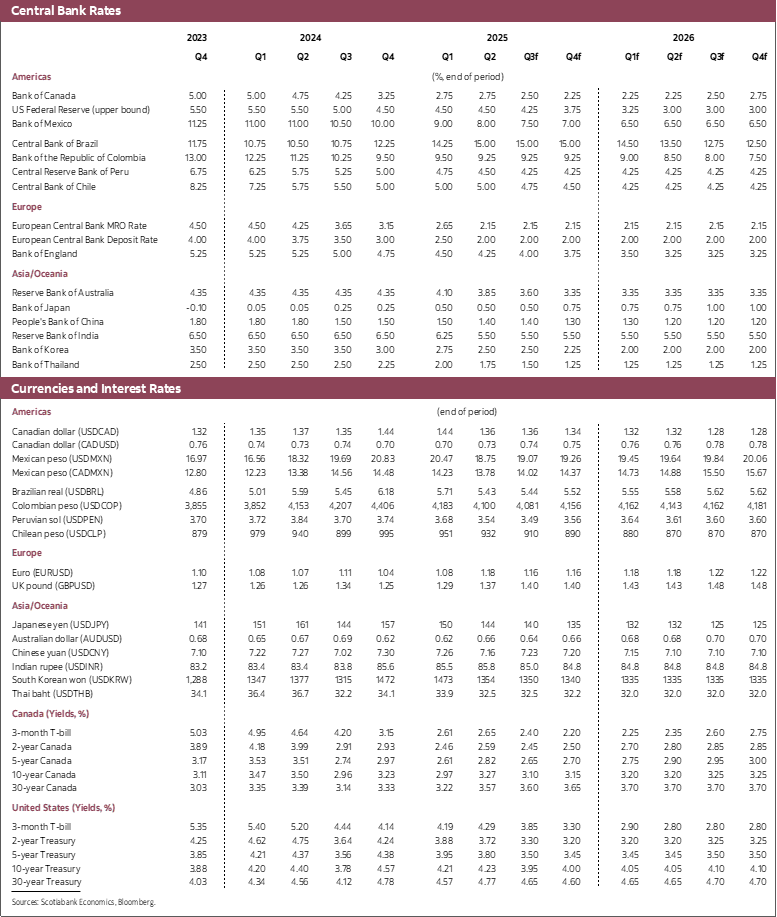

- Though inflation remains high, central banks seem inclined to treat the strength in inflation as transitory, as was the original thinking during the pandemic. Combined with below-potential growth in the U.S. and Canada, we believe the Bank of Canada will cut by 25 basis points at each of the next two meetings as a form of insurance against weaker growth and inflation. We expect those cuts to be reversed in the second half of 2026 as we believe inflation will prove to be more persistent than currently believed by the Bank of Canada. We now think the Fed will cut by 25 basis points at each of the next 6 meetings.

- Political pressure on the Fed could lead to more cuts than we currently foresee and lead to challenging developments if that were to occur.

Central banks are increasingly being confronted with the conflicting impact of President Trump’s policies on inflation and growth. The growth impacts are becoming clear in a broad range of countries, most notably seen in U.S. and Canadian labour markets. Inflation remains problematic, with core measures of inflation near 3%, well away from target in both countries. Despite this tension, we believe the Federal Reserve and Bank of Canada will be cutting policy rates in coming meetings. There is very little doubt in our mind that the growth outcomes for this year and next would have already warranted rate cuts were it not for the behaviour of inflation.

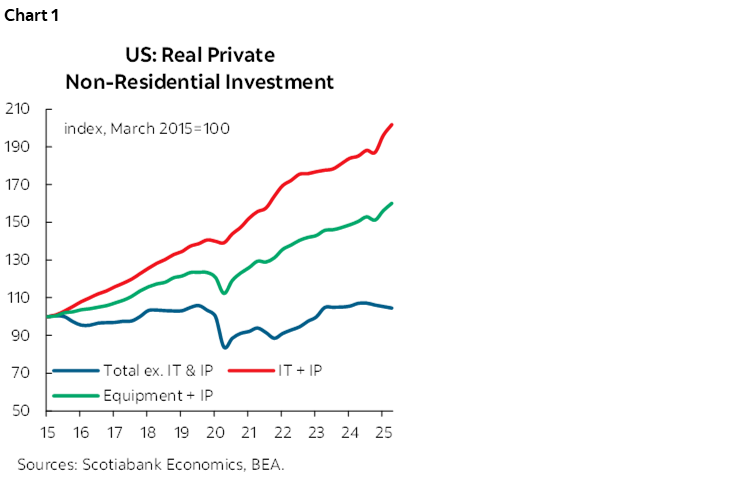

We see this more clearly in the U.S, the originator of the trade tensions roiling the global economy. Recent revisions to job creation numbers show a significantly softer labour market than earlier revealed by published data. While on first blush that may seem surprising, the performance of the U.S. so far this year, in which growth has been stronger than expected, looking beneath the surface on GDP data suggests underlying weakness. The U.S. is benefitting from an extraordinary surge in investment in information technology and intellectual property, which is masking broader weakness in investment (chart 1) and struggles in U.S. manufacturing activity. We continue to think a recession will be avoided but expect growth to slow from 1.8% this year to 1.4% next year. These are weak numbers however and are well below potential growth suggesting the economy will transition from excess demand to excess supply in 2026. The hope is that this opening of spare capacity will put downward pressure on inflation, allowing the Fed to lower its policy rate.

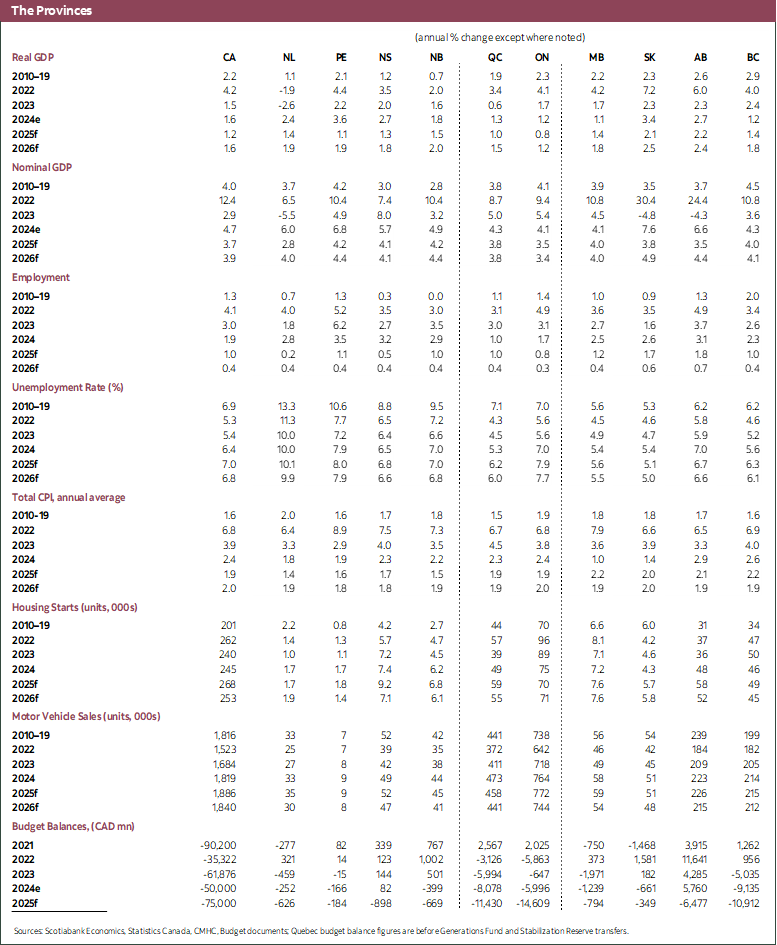

The Canadian economy is somewhat weaker than the U.S. owing in part to weaker business investment, which has been more impacted than the U.S. so far this year by concerns about the impact of U.S. tariffs, even if those tariffs are significantly lower than feared in the early months of the year. It has been clear for some time that worries about the tariffs have impacted spending decisions by firms and households in Canada. Moreover, there is some evidence that the impact of tariffs is being felt more rapidly than we had assumed. We had expected that the damage from tariffs would build over time, but the drop in GDP in Q2 in sectors most impacted by tariffs suggest that the impact of trade policies hit earlier than expected.

Those worries around the trade disturbance seem to have abated in recent months despite our view that the impact has been felt more rapidly than we thought was going to be the case. This is either the result of some relief that tariffs have generally been lower than feared (with the notable exception of those sectors subject to high tariffs), Canadians slowly getting accustomed to the disruptive nature of U.S. policy announcements, and some early signs that the transformation agenda being developed jointly between the federal government and provinces will eventually set the country on a better path. This improvement in sentiment is likely behind the resumption of activity in existing home sales in recent months. There are signs that last year’s interest rate cuts are working to boost, ever so modestly, the rate-sensitive parts of the economy.

There is no denying however that the employment numbers of the last two months have been concerning. Over one hundred thousand jobs have been lost. Employment is typically a lagging indicator and that showing may reflect the drop in GDP experienced in the second quarter, but the decline does seem large, and it is cause for worry. We currently believe Canadian GDP will rise by 0.7% in the third quarter, but the possibility of a technical recession (two quarters of falling GDP) cannot be excluded.

We expect a meaningful improvement in growth next year owing to the combined impact of more stimulative fiscal policy as governments move on the transformation agenda, and the impact of tariffs and associated uncertainty fade. The upcoming October budget will help inform our views on this impact, but it does seem clear that the economy will receive some fiscal support next year and beyond. On net, we expect Canadian growth to rise from an expected 1.2% this year to 1.6% next year.

The outlook for monetary policy depends critically on how inflation evolves. Core measures of inflation are around 3% in Canada and the U.S. This is not an outcome that would lead central banks to cut policy rates. The tension between inflation and growth is evident. The growth outlook would point to lower interest rates while the inflation outcomes suggest otherwise. Balancing these tensions is challenging given the unprecedented nature of these policy actions. Key to striking the right balance is the extent to which inflation pressures will prove to be transitory or not. It seems clear that the Fed and Bank of Canada want to believe these pressures will be temporary for the time being. That is a reasonable, but risky, position to take. If all goes well, tariffs should have a one-off impact on price levels. Given the breadth of tariffs applied in the U.S., their staggered sequencing, and the threat of even more tariffs going forward there is a real risk that tariffs lead to a broader and more sustained rise in inflation. We see these concerns clearly in consumer measures of inflation expectations on both sides of the border. Moreover, the experience of the pandemic, where central banks assessed the surge in inflation to be temporary when the surge proved to be persistent suggests a high degree of caution should be placed on views that inflation will only temporarily be impacted by trade policy developments. Further, there is evidence in the U.S. and Canada that much of the rise in inflation thus far reflects broader inflationary pressures than those resulting from trade policy frictions.

In the U.S., there is an added consideration of political pressure on the Fed which can only increase the odds of lower interest rates. Recall that President Trump has said numerous times that the U.S. policy rate should be cut by 200–300 basis points. Shifts in Fed board composition and the selection of a new Chair in May next year clearly raise the possibility that the Fed will, at best, prioritize arguments of a temporary inflation hit, and at worse, indicate great comfort with elevated levels of inflation in the implementation of monetary policy.

Given that the Fed has an explicit dual mandate, it has some flexibility to cut given employment developments, particularly if it assumes that the tariff impact will be temporary on inflation. For this reason, we now think the Fed will cut by 25 basis points at each of the next six meetings. We expect a series of small cuts over larger cuts owing to the evident risks that inflation remains a challenge. Shifts in Board composition could lead to greater cuts than that, but we assume that Fed voting members will remain committed to the inflation control aspect of their mandate. If that were to slip, then we could see lower rates than where we currently expect them to land (3.0%). That would come with a host of troubling consequences however, which are not incorporated in this forecast.

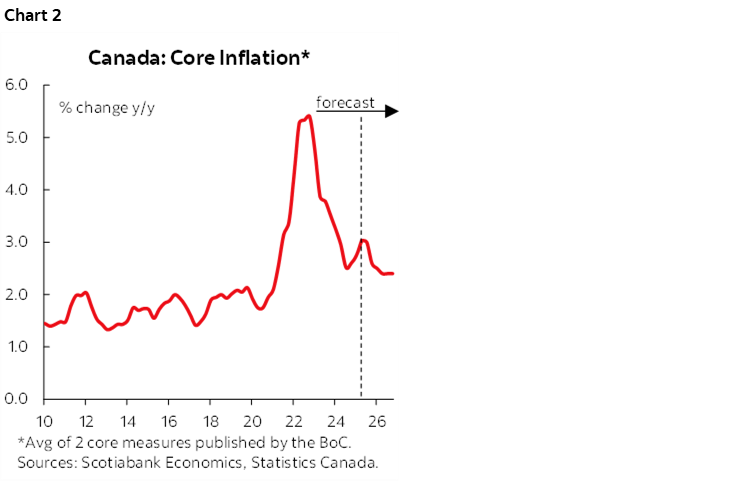

In Canada, the balance of risks is more straightforward given the single mandate of inflation control. We remain concerned that inflation is likely to be more persistent than assumed by the Bank of Canada but there is clearly a chance that inflation slows going forward. The economy is in excess supply and that excess capacity will grow in 2026. That should put downward pressure on inflation and underpins our view that inflation will moderate slowly going forward (chart 2). Our work suggests that monetary policy is reasonably well calibrated at the moment, but one cut could be justified. However, a single cut would be excessive fine-tuning, with only very modest impacts on growth and inflation going forward. If the BoC cuts on September 17th, as we currently expect, we think they would follow that up with another cut in October to generate a bit more of a monetary impulse.

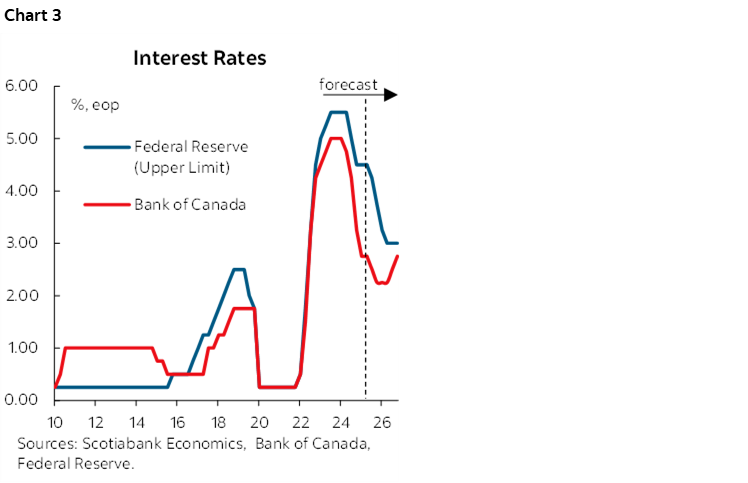

We are inclined to think of these cuts as insurance. The sharp decline in employment gives the BoC the option to make a couple of cuts at the next two meetings as a form of insurance against weaker growth and inflation outcomes. However, because we still believe inflation pressures will be more persistent than the BoC, we expect that these rate cuts will be reversed in the second half of 2026 to ensure that inflation converges sustainably to the 2% inflation target (chart 3).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.