- Outlook remains constrained by the ongoing and expected impacts of U.S. trade and economic policies.

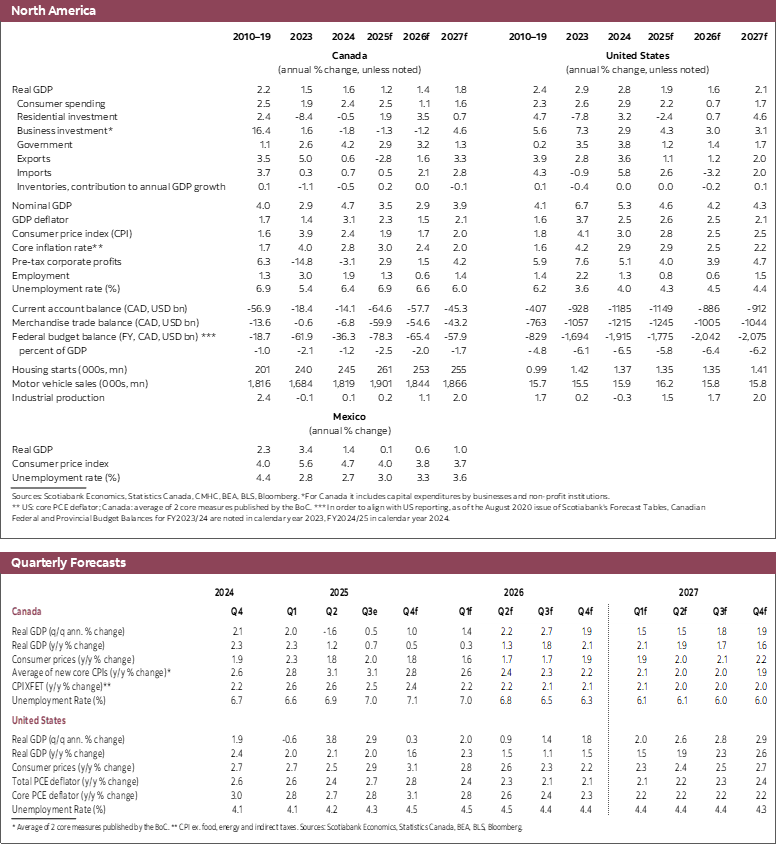

- Weak growth expected in Canada and the U.S. next year. In Canada, the damage from trade policies and lower immigration is weakening potential growth, acting as a limit on growth in the near-term.

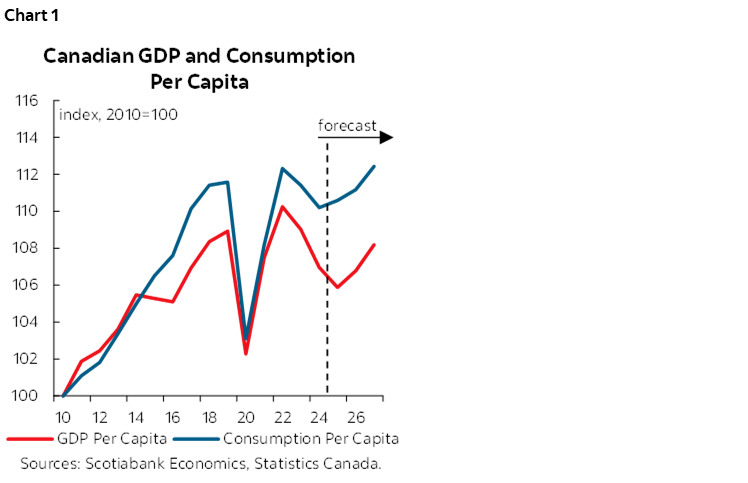

- Despite tepid growth, GDP and consumption per capita are expected to rise going forward given weak expected population growth.

- The Bank of Canada is done cutting rates with the next move expected to be an increase in the policy rate in the second half of 2026.

- The Federal Reserve is expected to cut its policy rate by another 100 basis points through the first half of next year.

The outlook remains challenged owing to the ongoing impacts of U.S. trade policies and associated uncertainty. In the U.S. there is mounting evidence that the goods economy is struggling, while in Canada, the economy is struggling to adapt to the evolving trade situation. Major uncertainties remain with respect to the way forward. These include the way forward on U.S. trade policy, the performance of the U.S. industrial sector, the path for inflation, the evolution of equity markets, and the impact of Budget 2025 in Canada. Weighing what we know at present, it seems likely that growth in Canada will improve modestly next year owing to fiscal support, while growth in the U.S. will slow given the impact of President Trump’s policies on non-tech sectors.

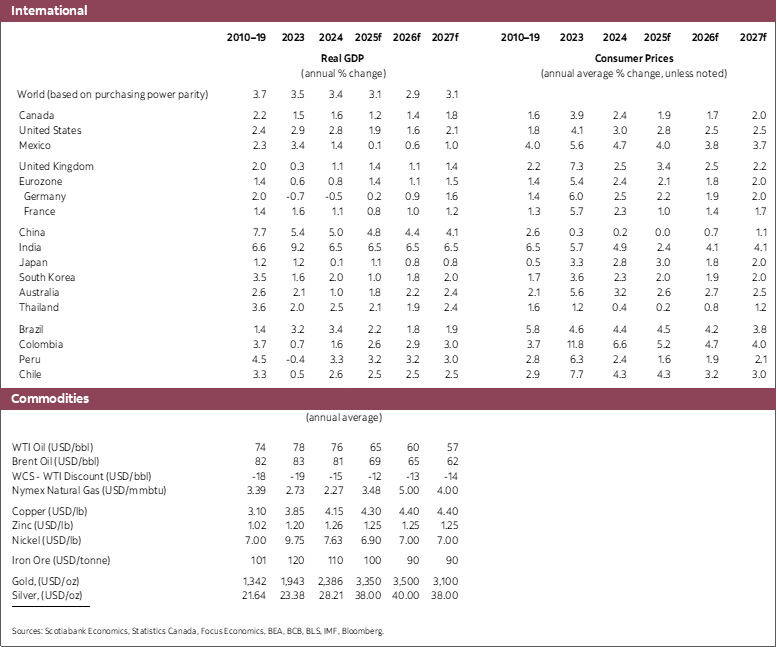

The U.S. economy continues to demonstrate surprising strength given the trade-related and associated policy uncertainty. Much of that resilience comes from booming tech investment and sharply stronger equity markets, which have reflected a keen appetite for AI companies and strong earnings growth in a broad range of sectors. That support has to date compensated for marked weakness in the goods economy as seen in declines in manufacturing activity and employment, a sharp rise in layoffs in October and deteriorating consumer sentiment. This dynamic on the goods side of the economy, along with evident labour market weakness, suggests that growth in the U.S. will weaken from the 1.9% expected this year to 1.6% next year.

That headline growth profile reflects some of these dynamics. Consumption growth will approach stall speed, slowing from 2.2% in 2025 to a mere 0.7% in 2026. Business investment will slow modestly from 4.3% to 3.0% next year as we expect some moderation in tech spending. We expect some draw down in inventories given pre-tariff stocking in 2025 and slowing consumption growth. Importantly, we expect a sharp reduction in imports next year, going from a rise of 2.6% this year to a decline of 3.2% in 2026 reflecting weakness in domestic demand and the impact of tariffs. Headline GDP growth would be much weaker were it not for that import performance.

Inflation is expected to remain in the 2.5% range in the first half of 2026 despite slowing growth. This largely reflects the lagged impacts of tariffs on prices along with continued upward pressure on core services prices. We expect that the Federal Reserve will largely look through these price pressures, arguing that they are more likely to be one-off shocks related to tariffs rather than indicative of broader price pressures. There is also clearly immense political pressure on the Federal Reserve to be more aggressive in pursuing rate cuts. We reflect some of these concerns in our expectations for the Federal Reserve as we forecast a terminal Federal Funds target rate of 3.0% by the 2026Q2. Our modelling suggests an optimal policy rate of 3.5% given our growth and inflation views but we build in an extra 50 basis points of easing relative to our modelling work to account for the Federal Reserve’s more dovish stance.

That outlook is of course subject to significant uncertainties including but not limited to:

- How will fiscal policy impact the outlook? Our forecast has long incorporated the tax cuts and tariffs implemented earlier this year, but we do not reflect President Trump’s statement that the government would give $2,000 tariff rebate cheques to middle-class and low-income households. Transfers at these levels would have a significant impact on growth and inflation, with likely consequences on the policy rate and the yield curve.

- How will households respond to rising health care insurance premiums resulting from the elimination of the Affordable Care Act enhanced tax credits? Studies estimate this could double the monthly premiums paid by some households. We do not account for these specifically in our outlook for weak consumption growth but we will be watching closely for signs of spending weakness that may result from that.

- It remains to be seen how supply chains are being reworked in light of the tariffs. The unprecedented nature of the trade shock has made it challenging for businesses (and economists) to identify with certainty how U.S. and global businesses will adapt, including very importantly on the extent to which higher costs will be passed on to end-users. We continue to expect sticky inflation in the U.S. and judge that risks to inflation remain skewed to higher inflation.

- Uncertainty is falling but it remains elevated given trade policies. While there is some clarity on the way forward for this, President Trump continues to muddy the waters on the way forward noting once in a while that tariffs with some countries may change going forward. There is a risk that uncertainty rises in coming months if the Supreme Court rules against the IEEPA tariffs. It is likely that the Administration would react aggressively to such a ruling as it seeks to find alternative ways of tariffing goods. There are a few options for doing this, but the uncertainty of how and when alternative tariffing statutes will be used would act as a further dampener on business investment.

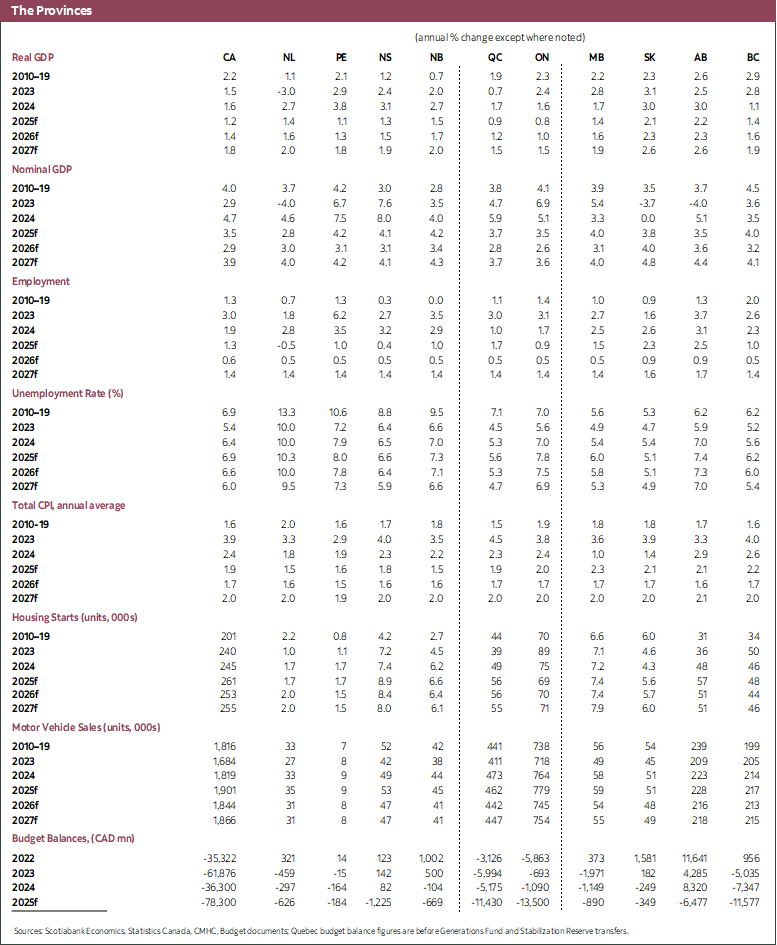

The Canadian outlook is of course impacted by developments in the U.S. and the risks to that economy. In contrast to the U.S. however, our forecast assumes that Canadian economic growth improves in 2026 relative to 2025. This is admittedly not a very high bar, as growth would go from 1.2% this year to 1.4% next year owing to the damaging impacts of tariffs and related uncertainty. That modest acceleration comes from what we believe to be more effective policy support in Canada relative to the U.S.

It is abundantly clear that Canadian governments are deploying a set of policy tools designed to strengthen the outlook over the medium-term as the country adapts to a new trading relation with the U.S. and focuses on raising investment. This, in our view, is in sharp contrast to the evolving policy environment in the U.S.

The 2025 Federal Budget did not contain major surprises on the amount of fiscal support for the economy next year in relation to our assumptions. We have nevertheless adjusted our forecast to reflect two critical changes. Immigration policy seems to target a lower rate of population growth going forward than we had assumed. We now assume population growth of 0.5% in 2026 and 2027. This accounts for the majority of our revision to GDP growth as it has the effect of lowering growth in demand and supply over those years, by lowering our estimated rate of growth in potential output. We partially offset this impact through higher investment and lower import growth.

On investment, the new measures revealed in the Budget do not appear to be game changers relative to our expectations. It is clear however, that the governments (both provincial and federal) are moving aggressively to identify transformational investment projects. Some of those were known pre-budget but more are expected shortly. We expect non-residential investment to rise starting in early 2026 but weak momentum towards end-2025 and early 2026 mean that investment will likely fall in 2026 despite policy support. Investment should strengthen more robustly in 2027 given the nature of infrastructure projects but there are clear risks of under-execution on these projects and consequently on private sector investment.

Finance Minister Champagne and PM Carney both expect additional investment of $1 trillion over the next 5 years as a result of their policies. Investment growth would be significantly stronger were even a fraction of this to occur in 2026 or 2027. For reference, total annual investment is about $500 billion. Assuming for the sake of exposition that policies do generate an extra trillion in investment and that this is spread equally over 5 years, this would represent an increase of about $200 billion over current levels of investment. We of course hope this occurs but will refrain from including these impacts in our forecast until we see tangible evidence that investment is tracking in that direction.

Buy Canada policies are likely to dampen the import response of rising investment relative to history. We have held back import growth modestly to reflect this. This provides a bit less drag from imports onto GDP relative to our pre-budget view.

Despite this relatively tepid outlook, the net impact of these revisions is to generate a very welcome increase in GDP and consumption per capita (chart 1) and reverse some of the erosion in standards of living observed in recent quarters.

Zooming into more recent months, the economy continues to send conflicting signals. Evidence of economic damage is clear in many communities with unemployment rates in trade-impacted areas substantially higher than elsewhere in the country. Pain is also mounting rapidly in the forestry sector owing to the punitive U.S. tariffs on softwood lumber. That being said, there appear to be signs of vigor in the labour market. Over 120k jobs were created in the last two months and the unemployment rate fell in October while the participation rate ticked up. Auto sales have risen sharply over the last three months. On balance it appears as if the economy may grow by around 0.5% in 2025Q3 and expect a modest acceleration to 1% in 2025Q4.

Growth at these rates suggests the economy will grow below potential in the second half of this year. Our estimate of the output gap is relatively unchanged compared to our last forecast given changes to the population outlook. The persistence of excess supply should continue to put downward pressure on inflation despite underlying inflation that remains stubbornly in the upper half of the Bank of Canada’s target range of 1–3% for inflation. Weak productivity, strong wage growth, rising input costs and the potential for rising U.S. import prices reflecting the impact of tariffs on U.S. goods all point to upside risks to inflation despite growing excess supply. We continue to believe inflation will moderate going forward as weak demand exerts downward pressure on inflation, but this is not a particularly high confidence call.

We think inflation risks are serious enough that the Bank of Canada is done cutting interest rates. We consider the most recent cuts to be insurance against weaker outcomes given the uncertainties being faced. That insurance is not likely be required later next year. As a result, we expect Governor Macklem and his colleagues will raise the policy rate by half a percentage point in the second half of 2026, reversing the most recent cuts. It may well be that an earlier reversal of those cuts is required if the economy responds more forcefully to the Government’s transformation agenda than we have currently imbedded into our forecast. Recall that the Bank of Canada only expects 1.1% growth in real GDP next year. The bar to exceed that does not seem particularly high.

Even though uncertainty has fallen in recent months, the Canadian outlook will remain under a cloud of uncertainty until the tariff situation is finally settled. We may well see some scaling back of tariffs on steel and aluminium in coming months given what seemed to be progress on that front prior to President Trump walking away from those negotiations. Relief in that space could provide a significant boost in sentiment to Canadians (along with significant tariff relief for impacted American importers). The review of CUSMA may also act as a source of uncertainty. It is entirely unclear what, if any, demands the U.S. may have in that review. We take comfort from the fact that the vast majority of goods shipped to the U.S. under CUSMA remain tariff free. We interpret this, perhaps optimistically, as a recognition of the importance of the trade deal to U.S. economic interests. If that interpretation is correct, we are hopeful that only minor tweaks will be negotiated in the review, as was largely the case when NAFTA was renegotiated into the CUSMA. That hope will likely be strained by a to-be-expected ramping up of caustic language by Trump Administration officials with respect to Canada as the review unfolds. This is a hallmark of President Trump’s negotiating strategy.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.