- Incoming data and fiscal policy announcements in the U.S. and Canada suggest growth will be modestly stronger than earlier anticipated.

- Both economies are still expected to grow below potential growth rates this year and next owing to U.S. trade policies and the associated uncertainty, but inflation pressures will limit central bank ability to respond to slower growth.

- We continue to hold to our long-standing view that both the Bank of Canada and Federal Reserve will remain on hold for the remainder of the year.

- Our forecast does not reflect recent trade pronouncements in the U.S. We will wait until policies actually take effect before reflecting those in our forecasts. There is simply too much uncertainty about the way forward on trade to build those into our forecasts at the moment.

There is lots of noise on the trade side that could have meaningful impacts on the global outlook. Time will tell how things settle, but we consider it premature to incorporate recent threats and announcements into our forecasts. As a case in point: some days President Trump says the letters he has sent are the final deals, other days he says they are open to negotiation. We are unlikely to have clarity on the tariff front until early August, and even then, things risk looking opaque. As is our long-standing practice, we will incorporate trade developments as they come into force. At present however, President Trump’s more recent trade threats seem like they would result in stronger downward revisions to growth and higher revisions to inflation in the U.S. relative to its trading partners.

For the time being, our forecast update reflects the impact of incoming data and fiscal policy announcements in Canada and the U.S. in particular. The net impact of these developments is an upward revision to the outlooks in both countries.

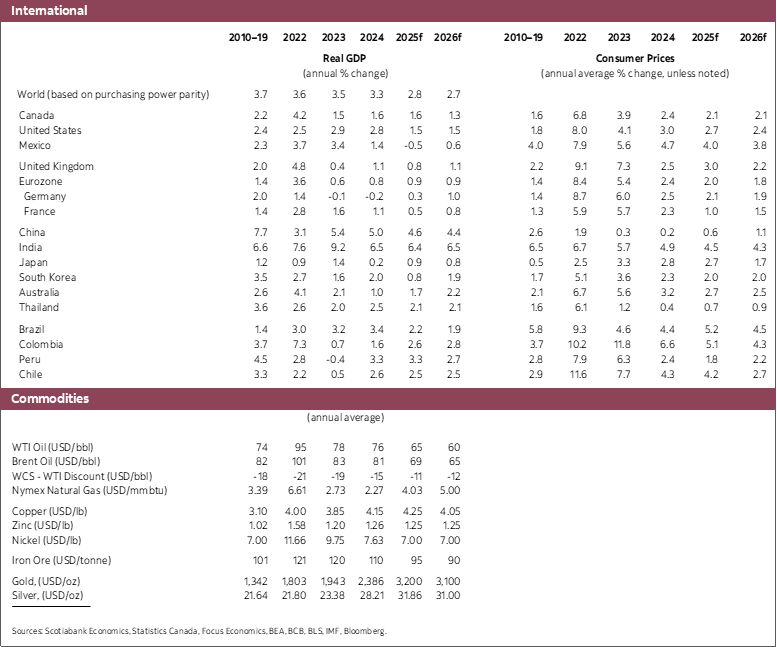

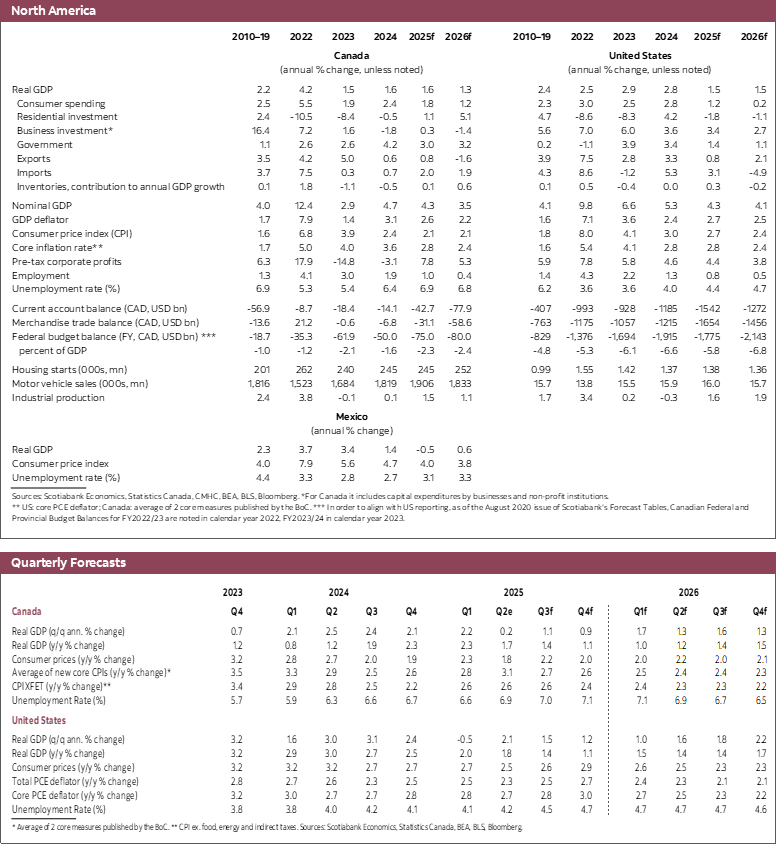

Growth in Canada appears to be on a better track than we had assumed in our last forecast. We had anticipated a one percent decline in real GDP in Q2, for instance, and our tracking now suggests something slightly above zero. We are seeing quite unexpected signs of a strengthening in the labour market, with 83k jobs created in June, and hours worked rising by 1.3% at annualized rates in the second quarter. Moreover, sales of existing homes have been rising for the last three months, suggesting a recovery in the housing market may be underway after significant weakness post U.S. election. Moreover, informal conversations with clients suggest a more optimistic view of the outlook relative to the last few months. This is not to say the economy is strong, it remains weak across a broad range of indicators, but on balance the economy is less weak than we had earlier assumed. Ongoing trade negotiations could of course affect the outlook, but it bears emphasizing that the most recent tariff threat of 35% tariffs on non-CUSMA eligible exports to the U.S. (from the current 25% rate) would cause reasonably minor additional aggregate economic impacts if enacted.

Against this context, underlying measures of inflation in Canada remain in the three percent range and risks continue to point to stronger, rather than weaker, inflation in coming months. This combination of stronger, but not strong, growth and resilient inflation confirms our long-standing view that the Bank of Canada would remain on hold for the remainder of the year. Indeed, market pricing is coming around to this view even though markets are still pricing in a chance of a cut by year-end.

The U.S. outlook continues to be subject to significant uncertainties. As noted above, we are not reflecting the impact of recent trade letters, but we do incorporate the impact of the One Big Beautiful Bill. This results in a more stimulative fiscal policy at the margin as our forecasts had never incorporated the phasing-out of the tax cuts implemented in the first Trump mandate. The fiscal law presents a number of challenges for the outlook: it complicates inflation management, it adds significantly to fiscal sustainability concerns, and it may well raise the sovereign risk premium for the U.S. This, in addition to the increasingly shrill calls for the removal of Federal Reserve Chair Powell point to heightened financial market uncertainty going forward, with virtually all signs pointing to higher borrowing costs. It may be the case that an early Powell dismissal could lead to lower policy rates this year if his replacement follows President Trump’s desire for the Federal Funds Rate to be cut by 300 basis points, but this would likely curtail demand for U.S. assets significantly, leading to higher longer-term yield spreads, a lower dollar, and potentially lower equity valuations. Time will tell how this evolves.

For the moment, the U.S. economy is weakening less rapidly and equity markets have been stronger than expected, as is the case in Canada. We have revised up our forecasts for growth modestly this year and next, with growth of around 1.5 per cent this year and next now expected. The outlook continues to reflect the negative impacts of tariffs and policy uncertainty, which, as noted above, could lead to downward revisions to growth once there is more clarity about the policy environment. Though this below potential growth will create excess supply in time that should put downward pressure on inflation, we continue to believe that upside risks to U.S. inflation dominate because of the tariff shock. We are starting to see signs of this in inflation data, and these effects will be even more apparent in coming months. While monetary policy should in theory look through one-off impacts on things like tariffs on inflation, the chaotic rollout of the U.S. trade agenda is creating serial tariff shocks that will be hard to distinguish from one-off impacts. Firms and households already have inflation expectations that are inconsistent with the Fed’s mandate. That risks rising further if inflation rises. As a result, we remain comfortable with our long-held view that the Federal Reserve will remain on hold for the remainder of the year but cut interest rates next year as the build-up in excess supply starts to put downward pressure on inflation. We would of course revise these views if Chair Powell were to vacate his position.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.