ECONOMIC OVERVIEW

- After the Pacific Alliance’s CPI flood, we have a calmer week ahead where Colombian and Peruvian GDP, and the BCRP’s decision are the highlights (alongside Brazilian CPI) in the region.

- In today’s report, the teams in the region cover BanRep’s communications over the past week that point to no more easing in 2025, preview a strong Peruvian GDP reading that reinforces an on-hold BCRP stance, and take a closer look at the weakness in Mexico’s extraction, utilities, and construction sectors weighed by tight public finances.

- U.S. CPI, PPI, retail sales, U.K. GDP and employment, Japanese GDP, and the RBA’s decision are the main releases in the G10, while we all watch for a possible extension of the U.S.-China trade truce that is due to expire on Tuesday.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Colombia, Mexico and Peru.

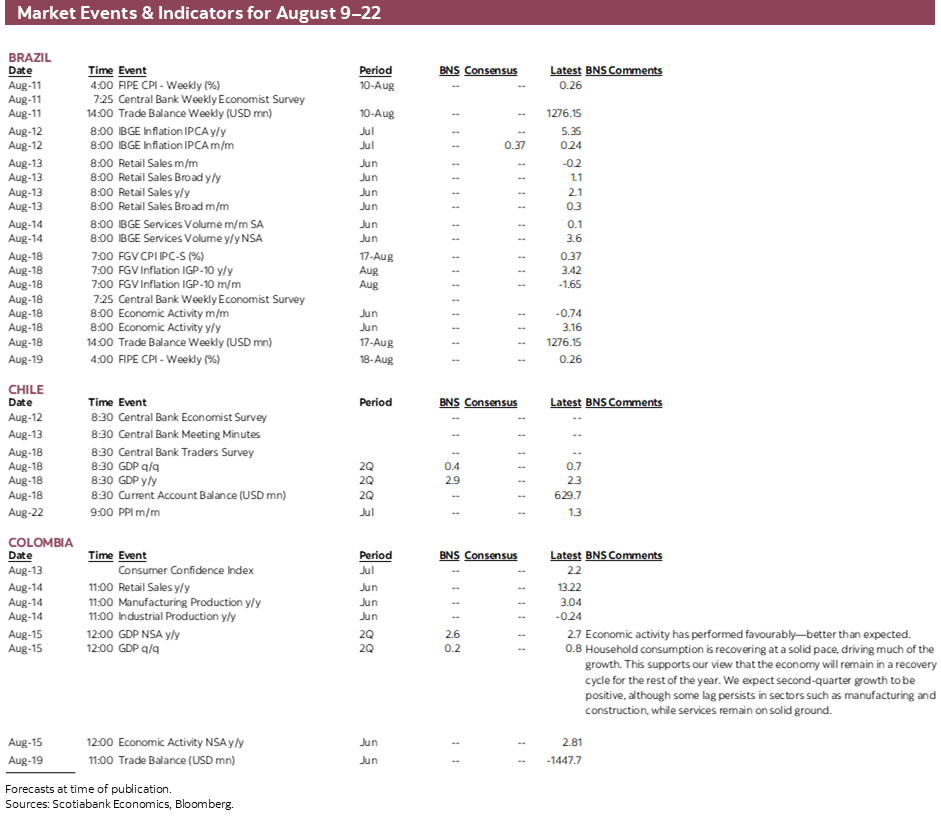

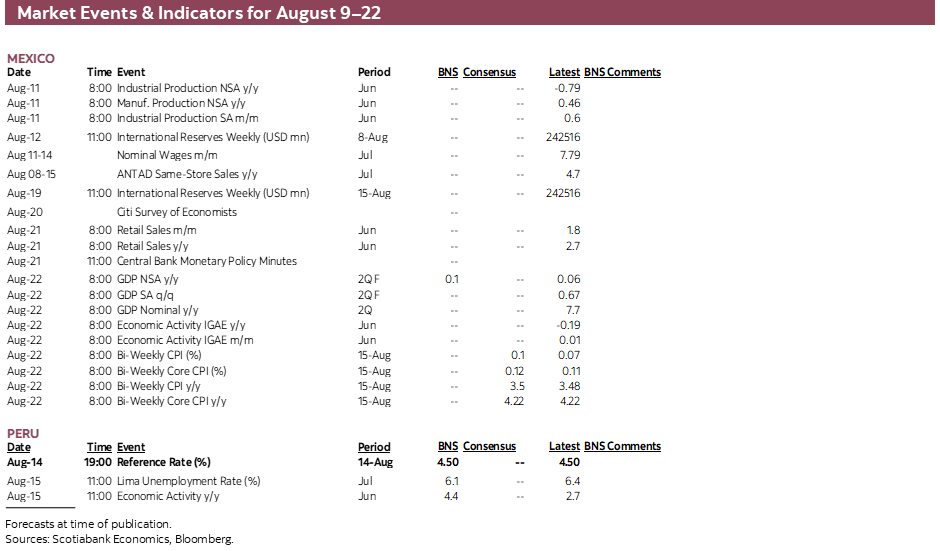

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period August 9–22 across the Pacific Alliance countries and Brazil.

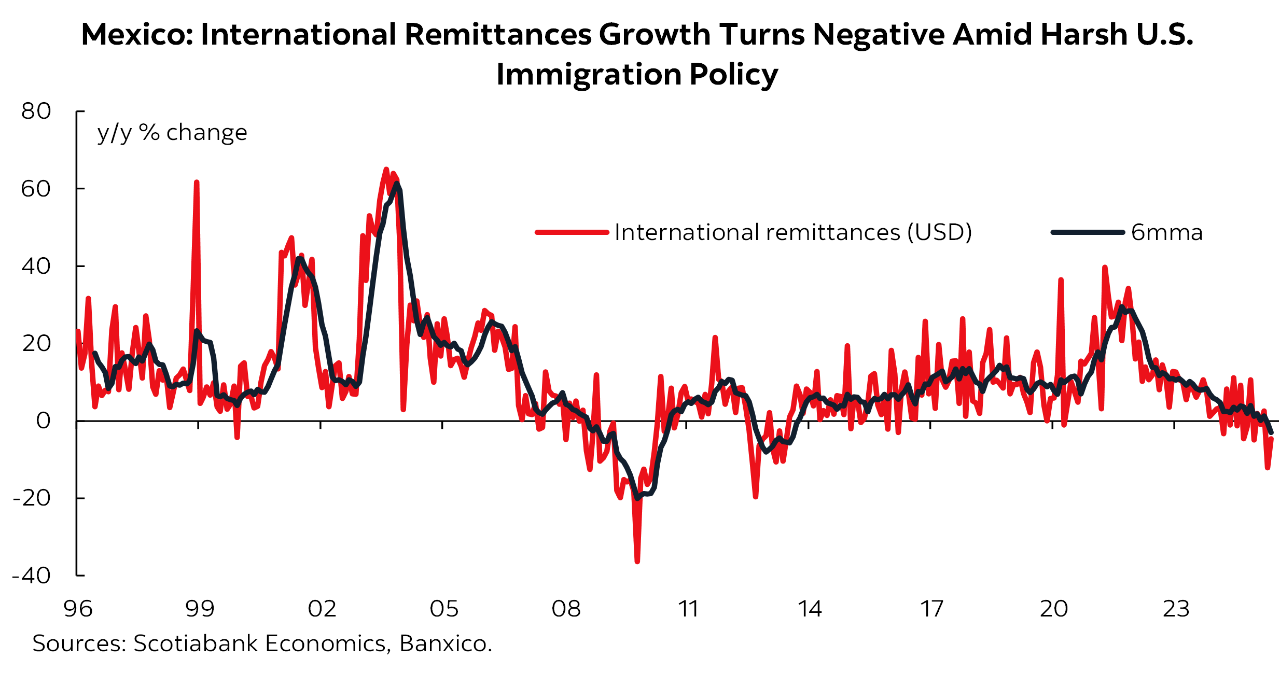

Chart of the Week*

*This chart is from Latam Insights: Mexico—Growth Challenged by Domestic and External (August 6, 2025).

ECONOMIC OVERVIEW: COLOMBIA AND PERU GDP, ANOTHER BCRP HOLD

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- After the CPI flood in the Pacific Alliance, we have a calmer week ahead where Colombian and Peruvian GDP, and the BCRP’s decision are the highlights (alongside Brazilian CPI) in the region.

- In today’s report, the teams in the region cover BanRep’s communications over the past week that point to no more easing in 2025, preview a strong Peruvian GDP reading that reinforces an on-hold BCRP stance, and take a closer look at the weakness in Mexico’s extraction, utilities, and construction sectors weighed by tight public finances.

- U.S. CPI, PPI, retail sales, U.K. GDP and employment, Japanese GDP, and the RBA’s decision are the main releases in the G10, while we all watch for a possible extension of the U.S.-China trade truce that is due to expire on Tuesday.

We have a calmer week ahead in Latam on the heels of regional CPI releases and central bank decisions, with major data and events mostly clustered over the second half of next week. Latam releases will be accompanied by a busy U.S. calendar (namely CPI and retail figures) and other key data out of the G10 (U.K. GDP and employment, and the RBA’s decision). Outside of the Pacific Alliance, Brazil publishes CPI data for the whole of July, though there’s little room for surprise with IPCA-15 figures at hand. Markets will also be on the lookout for a possible (likely) extension of the U.S.-China trade truce that expires on Tuesday, all while we get sporadic headlines on tariff negotiations and announcements as well proposals to halt the Russia-Ukraine war.

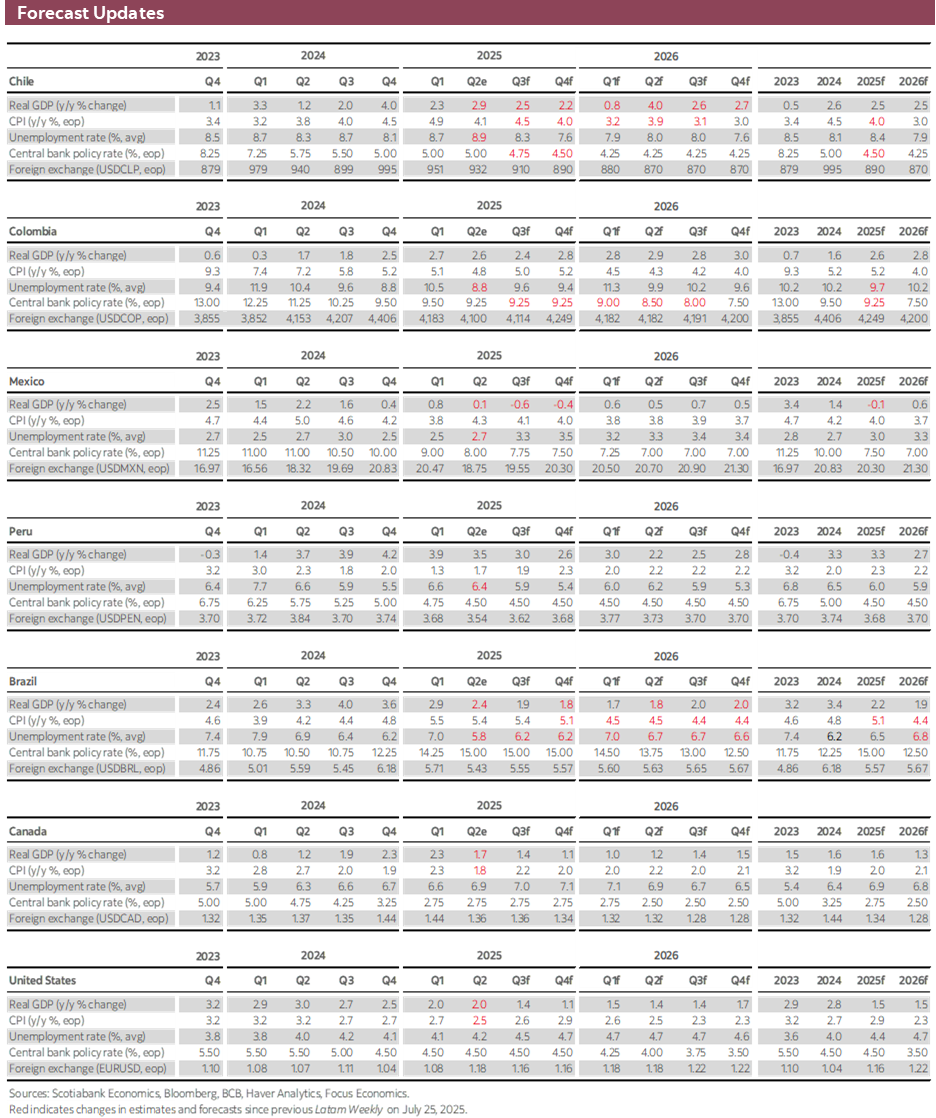

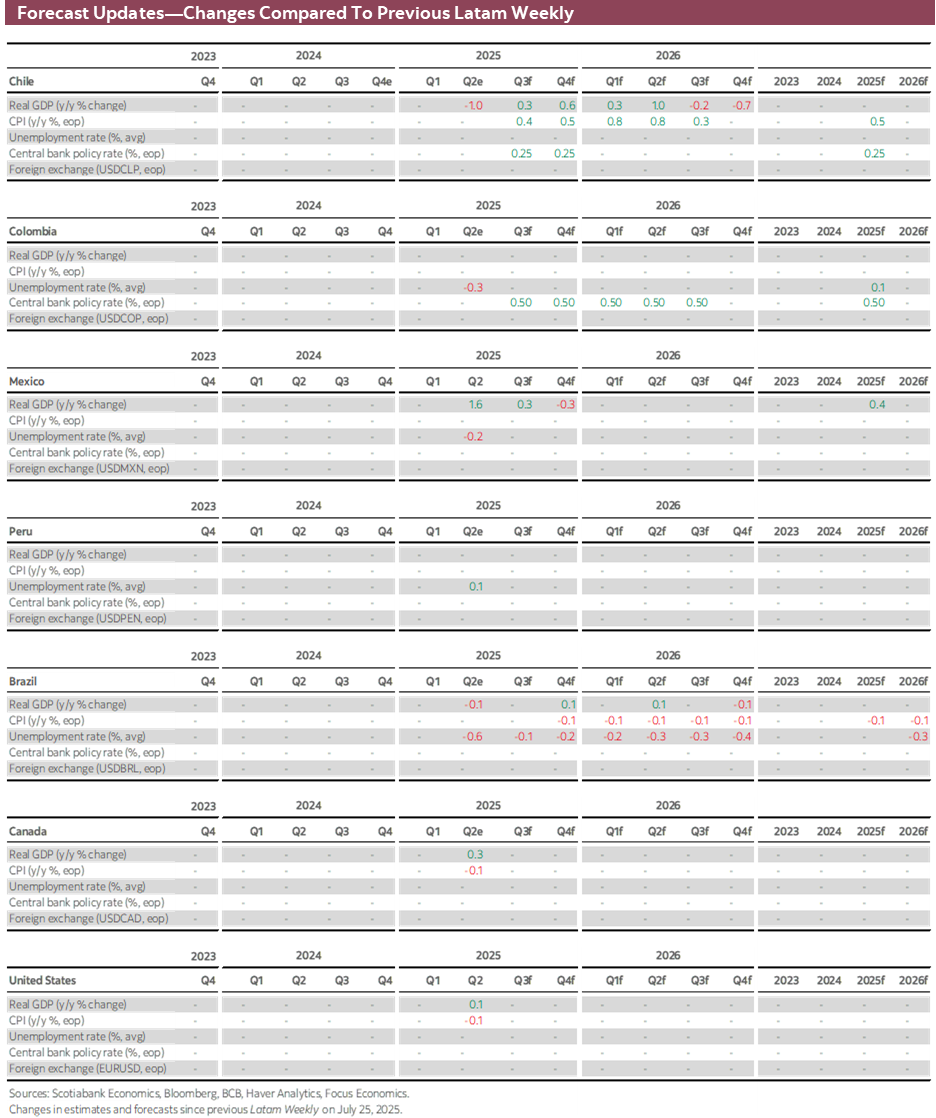

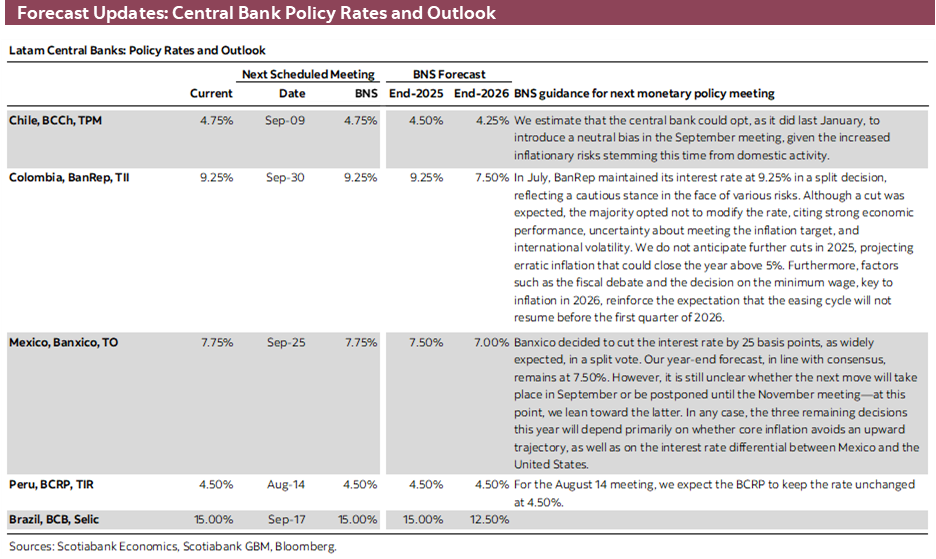

Colombia and Peru will release GDP data on Friday for June/2Q that are expected to show resilient growth in both countries that is, to differing degrees, a motivation for local central banks to keep policy settings unchanged. BanRep surprised last week with a rate hold that has virtually closed the door on easing through the remainder of 2025 (see here), with a solid economy seemingly giving them little reason to provide support.

In today’s note, the team in Colombia go over BanRep’s recent communications as the unexpected rate hold, hawkish projections, and meeting minutes show a clear division in the Board that leans towards continued restrictiveness for longer. Given elevated risks regarding the 2026 minimum wage hike, as well as political considerations, we now think that the central bank will not cut rates sooner than 1Q26.

Colombia’s economy is forecast to have expanded by 2.6% y/y in 2Q, practically in line with the 2.7% rise in 1Q, supported by solid household consumption that has acted as a pillar for economic momentum alongside robust job gains. We’ll look to refine this expectation on Thursday with June readings for retail sales and industrial production that come off respectively strong (13.2% y/y) and weak (-0.2%) prints in May, though the data are unlikely to shake the feeling that the economy is in a good spot in spite of high interest rates and political/fiscal risks and noise.

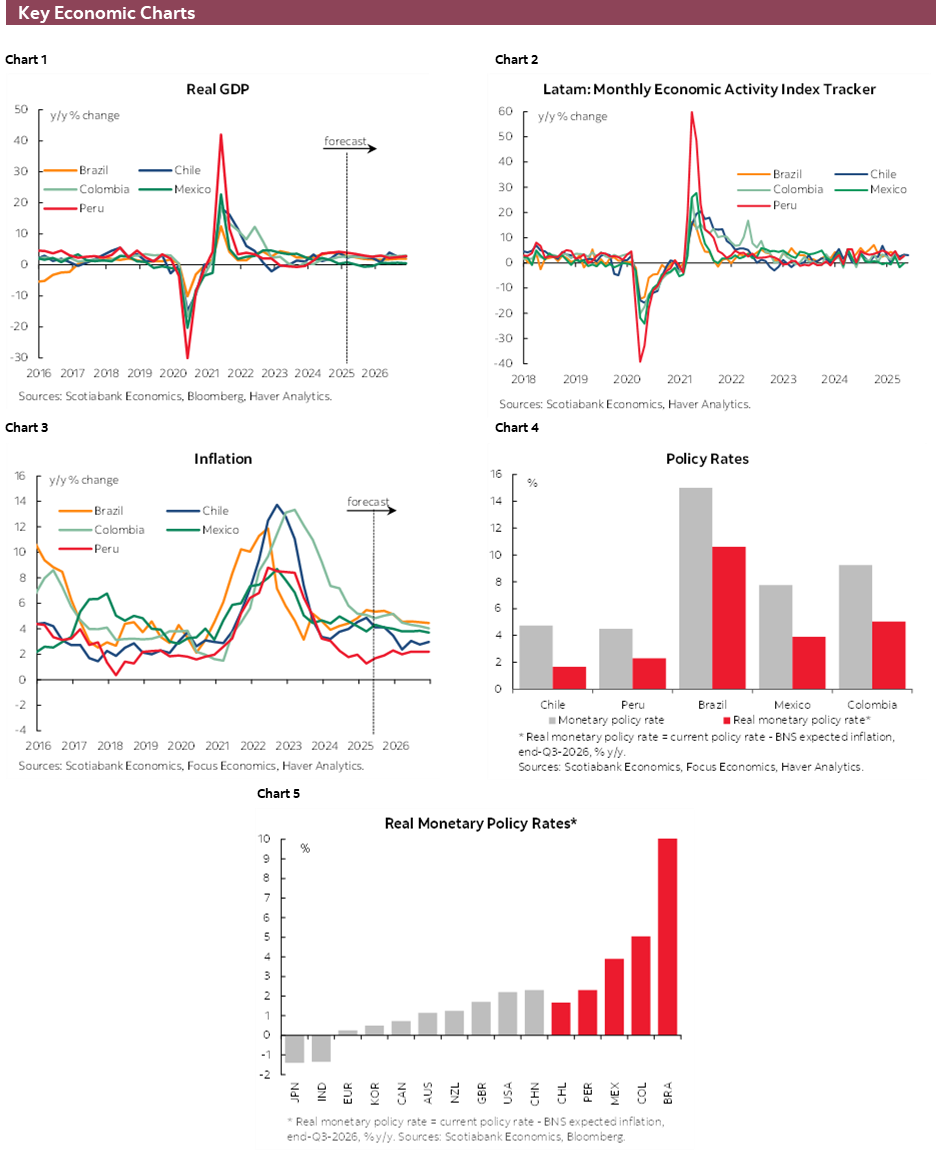

Peru’s June GDP release is the focus of our colleagues in Lima today. Industry-level data for fishing, mining, and construction activity point to a very strong reading of 4.4% y/y growth, up from relatively soft expansions in April (1.5%) and May (2.7%). The final month of the quarter is estimated to have patched over some of the factors that weighed earlier in 2Q, namely fishing and the extraction sector—both of which are not linked to domestic demand. Meanwhile, local economy indicators look firm and steadier than volatile/seasonal swings in these sectors (see our mid-July weekly).

On Thursday, the BCRP is due to announce a third consecutive rate hold as soft inflation (due to accelerate a touch in 2H) is offset by solid economic fundamentals to leave officials with little reason to cut (never write off a BCRP surprise, however). Macro conditions suggest the Peruvian economy is likely exceeding its growth potential, with no evident headwinds from tariff risks and seemingly completely desensitized to (the now usual) political noise—and not too concerned with next April’s elections. It’s steady as she goes at 4.50% over the forecast horizon to 2026.

There’s no macro data out of Chile next week (shortened by holidays on Friday), but we’ll pay close attention to the results of the BCCh’s economists survey out on Tuesday following the July inflation surprise. With last month’s 4.3% y/y CPI rise, a sustainable convergence to the 3% goal has been kicked down the road, teeing up an upward revision to economists’ forecasts and the central bank when it next updates its forecasts in September (with August CPI data also at hand).

In light of this, our economists have changed their call from a September rate cut to a hold, to only be followed by another reduction this year in 4Q, alongside a year-end CPI forecast of 4.0% (up from 3.5%). On Wednesday, the BCCh publishes the minutes to its as-expected 25bps cut in late-July, when it had highlighted already in its statement the upside surprises in core inflation and strong wages growth. The minutes may be stale considering the decision preceded the July CPI overshoot, but we’ll keep an eye on just how concerned officials were about the path for inflation and thus the likelihood of keeping rates unchanged for one or more meetings.

Mexico has little on tap aside from manufacturing and industrial production data out on Monday, which our economists in the country cover today. The team highlights the challenges that Mexico’s extraction, utilities, and construction sectors are facing, with their close link to the state’s limited fiscal space acting as a direct drag on their performance, weighing on the overall health of Mexico’s economy—which we discussed in detail in a special report published earlier this week.

PACIFIC ALLIANCE COUNTRY UPDATES

Colombia—Monetary Policy Perspective: No Room for Cuts in 2025. Analysis of BanRep’s Recent Communications

Jackeline Piraján, Head Economist, Colombia

+57.601.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Although the focus this year has largely been on fiscal policy, we wanted to pause and analyze the latest information from the central bank—specifically, the recent decision, meeting minutes, and the Monetary Policy Report. Our conclusion is that monetary policy faces significant constraints that limit the possibility of interest rate cuts in 2025. However, the decision-making process is influenced not only by economic factors but also by political considerations, particularly those related to fiscal policy and the potential increase in the minimum wage for 2026. These elements could delay the resumption of the easing cycle until at least the first half of 2026.

With that in mind, we divide the monetary policy discussion into two fronts: pure economic policy and political economy.

Economic Policy: The GDP vs Inflation Dilemma is No Longer a Huge Dilemma

In the Monetary Policy Report, BanRep’s staff presented a positive assessment of recent economic activity data. However, inflation and upside risks remain the main concerns. Against this backdrop, the staff emphasized that the monetary policy rate path consistent with inflation converging to the target is, on average, higher than the economics consensus. According to the July survey, economists project a year-end rate of 8.50% and 7.00% by December 2026.

Macro Picture:

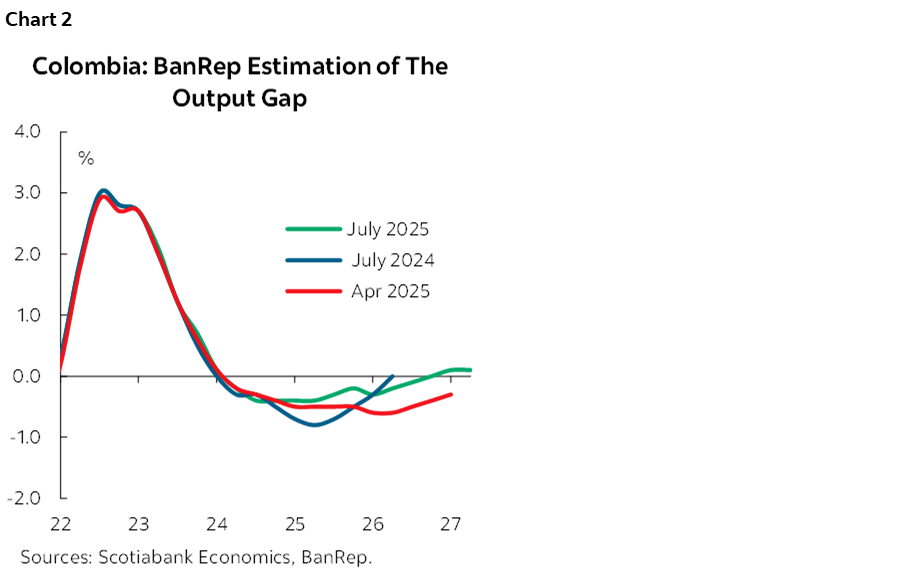

- Inflation: In the Monetary Policy Report, the central bank staff recognized that inflation has exceeded expectations in three of the four main analytical categories. Regarding core inflation, services have shown stronger-than-expected indexation effects due to rising labour costs. Goods-related inflation has also been elevated, driven by high international prices—though Scotiabank Colpatria Economics attributes this to statistical base effects. In non-core inflation, food prices have surpassed the central bank’s projections, while regulated prices—particularly electricity fees—have surprised to the downside. However, the slow pace of convergence towards the target range have pushed the staff to revise their projection for Dec-2025 to the upside to 4.7%, while for Dec-2026 it is expected at 3.2% (chart 1).

- Economic Activity: The central bank staff noted that GDP is outperforming expectations, supported by robust household consumption and specific investment areas. This strength appears sustainable over time. The labour market context reinforces this view, with strong job creation, ample vacancies, and high savings levels. In this context, BanRep projects economic growth of 2.7% in 2025 and 2.9% in 2026, which means the output gap will be closed in 2026 (chart 2).

- Investment Weakness: The sectors still lagging in investment recovery are not necessarily a monetary policy issue. According to Chief Economist Vargas, these sectors depend on government incentives and are affected by increased risk premiums stemming from fiscal concerns.

- International Context: The global trade environment and potential trade wars currently pose only moderate risks to the Colombian economy.

Political Economy: The Core of the Debate

Unfortunately, as the main source of uncertainty comes in this front, we anticipate that the better course of action for the central bank is to have a “wait and see” approach and keep interest rates on hold for the time being.

- Fiscal policy decisions towards higher deficits and an increasing debt to GDP burden. The Medium-Term Fiscal Framework 2025 (MTFF-2025) and the proposed 2026 Budget reveal the government’s limited willingness to reduce spending, while projecting overly optimistic revenue figures. This imbalance has led to credit rating downgrades by Moody’s and S&P and has undermined the credibility of Colombia’s fiscal framework. Notably, one board member who voted for a 25 bps cut argued that the negative fiscal news had limited market impact—a dynamic we believe was driven more by speculation than fundamentals.

- It is worth noting that since the July meeting, the central bank has become more cautious in commenting on fiscal policy, opting instead to discuss the consequences of high fiscal needs in a volatile financial market environment. According to the staff, this fiscal picture has two key implications for monetary policy:

1. It increases short-term volatility in economic activity, boosting domestic demand, but poses medium-term risks if the government (current or future) implements fiscal adjustments to reduce the deficit.

2. It raises the risk premium, leading to a higher neutral real interest rate. The staff has slightly revised the neutral rate estimate for 2026 from 3.0% to 3.1%. Vargas noted that this estimate includes international comparisons, which are increasingly relevant as investors perceive Colombia’s fiscal risk to be worse than that of peers like Brazil—despite Colombia’s current monetary policy stance being less contractionary.

- Minimum Wage Risk: The potential for a significant minimum wage increase in 2026 has created deep divisions within the board. Although wage hikes have contributed to inflation stickiness, Finance Minister Ávila and another board member who voted for a 50 bps cut remain skeptical of this effect. We think Minister Ávila’s strong views are a concern for the majority of the board, which now appears more cautious. The minimum wage increase is a non-trivial risk heading into 2026 and could further delay the convergence of inflation to the target—a concern that Ávila does not seem to prioritize. Meanwhile, President Petro has publicly signaled a substantial minimum wage increase in his final year in office.

- Scotiabank Colpatria projects year-end inflation slightly above 5%. Under this scenario, the minimum wage increase should not exceed 6.5%. However, if the government opts for a more aggressive hike, inflation may fail to return to the target range in 2026. The wage decision will be made at the end of the year (November/December), with its impact visible in January and February inflation data. This is the main reason we do not expect the central bank to consider a rate cut before March 2026 if the government exceeds the 6.5% threshold.

- The meeting minutes reveal that division within the board is not limited to the minimum wage debate. The two board members who voted for a 50 bps cut expressed disagreement with the reliance on unobservable variables such as potential GDP, the output gap, and the employment gap in guiding monetary policy. They also compared the current contractionary stance of the real interest rate with the average real rate between 2010 and 2023—likely overlooking key technical details, such as the fact that the real rate varies across the economic cycle and that Colombia has never faced the level of fiscal uncertainty it is currently experiencing.

- Interestingly, these two board members also advocated for lower interest rates to stimulate economic growth, viewing it as a solution to the fiscal equation. While this argument could hold some merit, Chief Economist Vargas clarified during the Monetary Policy Report press conference that the underperforming GDP components are those dependent on government-driven investment (e.g., infrastructure) and sectors requiring long-term financing. These sectors are now competing with the government for funding—a crowding-out effect—which is evident in areas such as housing construction and business credit. In any case, conversations between the staff and the board could be becoming more tense as the discrepancy in opinions are not only regarding the current situation, but also in the structure of the monetary policy framework.

All in all, we expect these divisions to persist in upcoming meetings. However, there are strong arguments suggesting that prudence will prevail. First, fiscal uncertainty is structural, and financing conditions remain highly volatile—both of which incentivize the central bank to maintain a contractionary stance. Second, political convictions are evident, and the minimum wage could become a key variable that materializes these convictions, posing a challenge to inflation convergence. Following this analysis, Scotiabank Colpatria has revised its interest rate outlook. We no longer expect rate cuts in 2025. The resumption of the easing cycle is now heavily dependent on a rational increase in the minimum wage. In the best case scenario, this could allow the board to consider rate cuts no earlier than March 2026. As noted by the staff in the Monetary Policy Report, the GDP vs. inflation dilemma is diminishing, and the inertia of the informal economy may support a continued contractionary monetary policy stance for some time.

Mexico—Weak Industrial Performance Reflects Fiscal and Sectoral Pressures

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

After several weeks marked by significant economic events and indicators, the upcoming week is expected to be quieter in terms of economic information. Among the few data releases, industrial production stands out, as its performance has shown signs of weakness—mainly due to sharp declines in the construction sector and stagnation in manufacturing.

Nevertheless, following recent government announcements regarding a restructuring plan for Pemex, it is relevant to analyze two other components of industrial production: mining and public utilities (generation and distribution of electricity, water, and gas).

During the January–May period, industrial production recorded an average annual decline of -1.4%. Within this result, mining posted a more pronounced drop of -8.8%, with oil extraction accumulating a -9.2% decrease. In terms of public finances, this has also had significant implications, as oil revenues from January to June—accounting for nearly 10% of total revenues so far this year—have seen a real annual reduction of -22%. Public utilities also declined, with a cumulative annual variation of -1.7%.

Although mining represents around 11% of total industrial production, it has been one of the deepest contracting sectors in recent years. In fact, it has posted consecutive annual declines since January 2024. Another sector that has significantly contributed to industrial weakness is construction, where uninterrupted declines began in January of this year. While its monthly drops have been less severe than those in mining, the collapse in infrastructure works stands out, with an average monthly decline of -25.27% so far this year.

Additionally, the public utilities sector—which includes the generation, transmission, distribution, and commercialization of electricity, as well as the supply of water and natural gas—has also shown weak performance, with a notable average annual decline in the first five months of the year.

However, this trend is unlikely to reverse in the short term, given the close ties of these sectors to the government and its limited fiscal space, a result of budget consolidation and efforts to clean up Pemex’s finances. Regarding the state oil company, although recent announcements—such as the PCAPS and the trust with Banobras—represent financial relief, their impact on the company’s operations will be limited.

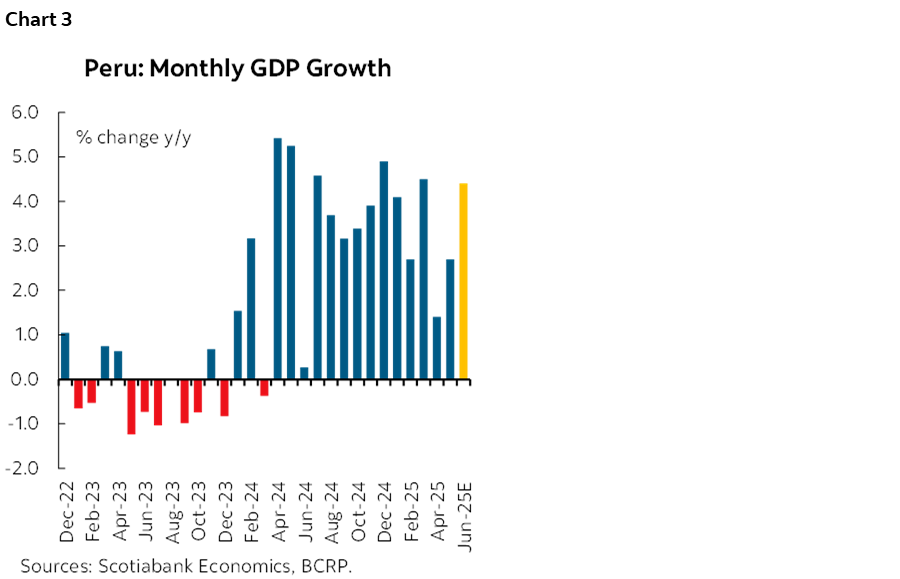

Peru—GDP Growth Would Accelerate in June, and Domestic Demand Remained Solid

Ricardo Avila, Senior Analyst

+51.1.211.6000 Ext. 16558 (Peru)

ricardo.avila@scotiabank.com.pe

June GDP will be published on Friday, August 15th. We expect 4.4% y/y growth. This is stronger than the 2.7% growth seen in May, and also better than the growth recorded in Q4 2024 (4.2%) and Q1 2025 (3.9%) (chart 3).

When one takes a closer look of the breakdown by sector, the message is optimistic. Three sectors are driving the projected 4.4% growth in June:

- Fishing: The actual figure has already been released, showing an increase of 33.7% y/y. This strong performance is attributed to a significant rise in anchovy catches during the month, which nearly doubled compared to June 2024.

- Agriculture: The actual data has also been published, indicating an 8.8% y/y growth. This was driven by a favourable base effect and increased output in the livestock subsector (poultry, cattle, and pigs).

- Construction: We estimate growth of 10% y/y, supported by robust public investment and a recovery in self-construction, as reflected in the sustained increase in local cement dispatches (5% y/y).

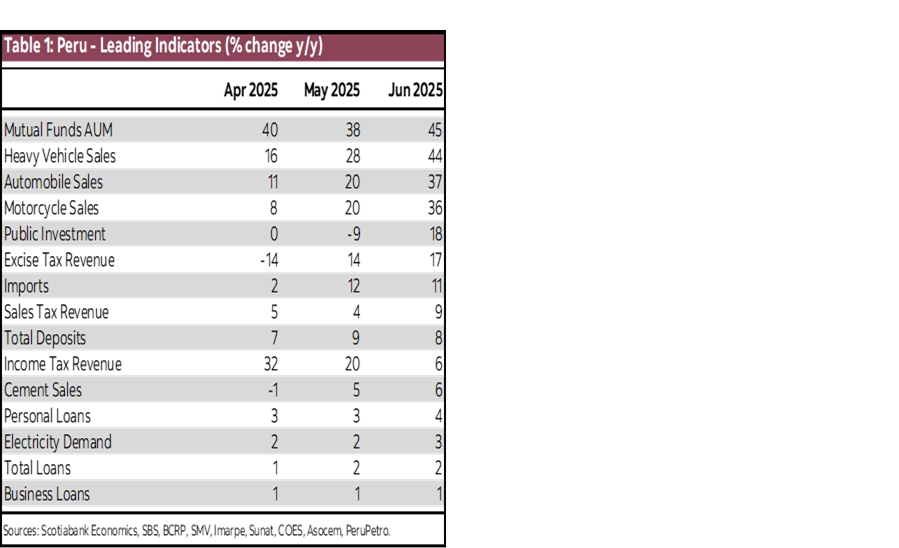

On the other hand, leading indicators (see table 1) also point to robust dynamics in June for sectors of the economy most closely tied to domestic demand, as they have shown improved performance compared to previous months.

Economic activity expectations improved in July. On August 7th, the Central Reserve Bank of Peru (BCRP) released its macroeconomic expectations report, highlighting that short-term (3-month) and medium-term (12-month) expectations not only remain in the optimistic range, but have also shown signs of recovery (chart 4).

In summary, GDP growth continues to exceed the estimated potential level. There is solid momentum in sectors linked to resources and domestic demand, and economic expectations convey a positive outlook. Therefore, despite inflation remaining low (1.7% over the past four months), we believe the BCRP is likely to keep its reference rate unchanged at 4.50% in its upcoming board meeting on Thursday, August 14th.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.