ECONOMIC OVERVIEW

- Mexico and Brazil are in focus next week in Latam, with both countries releasing mid-month inflation data and facing an uncertain tariff outlook after sudden announcements by the White House in recent days.

- Mexico will also publish economic activity data that are expected to show only a muted recovery to growth in May, as covered by our local team in today’s Weekly. Economists in Citi’s survey will likely leave their estimates for rates, growth, and inflation little changed in next week’s results.

- Global PMIs, the results of Japan’s Upper House election on the 20th, the ECB’s likely rate hold, and Canadian retail sales are the highlight for global markets who will also have to follow Powell dismissal risks and unpredictable (though now usual) tariff announcements.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Mexico and Peru.

MARKET EVENTS & INDICATORS

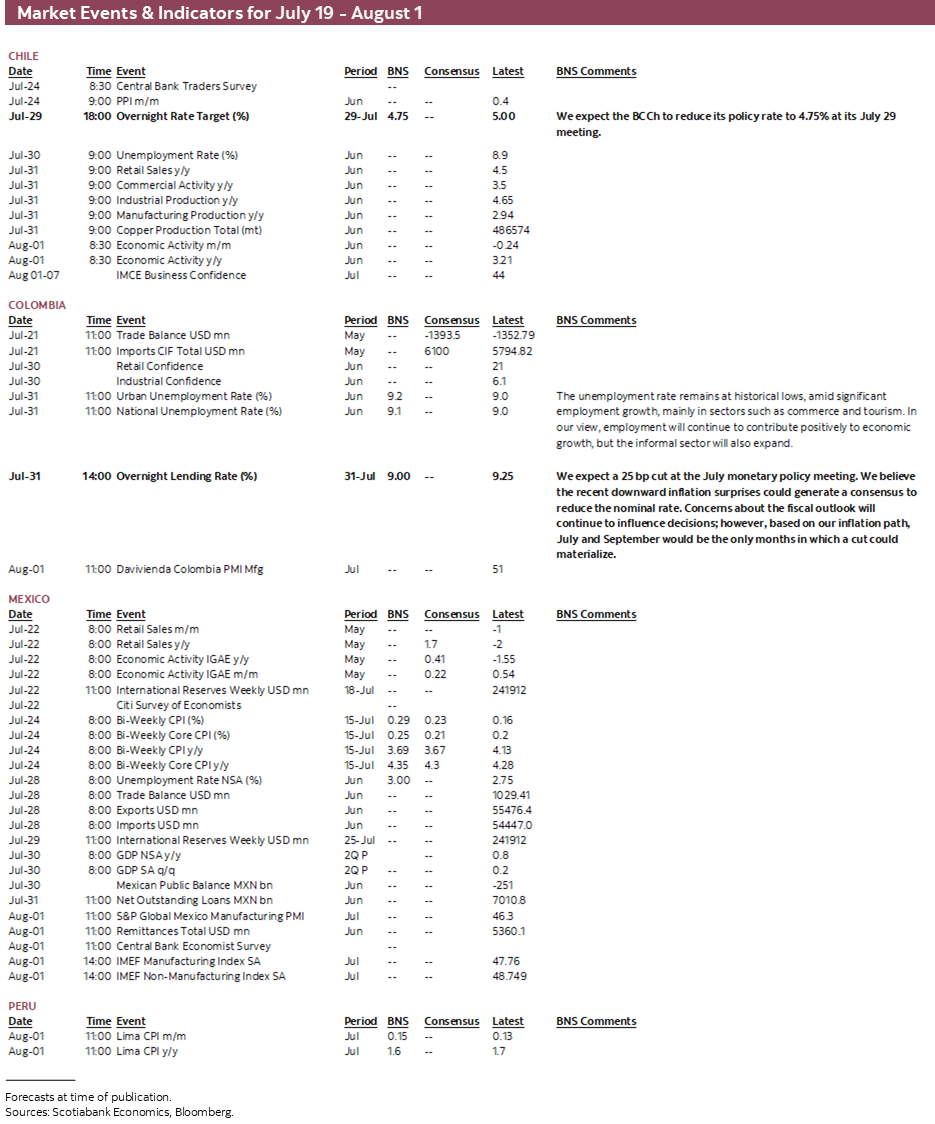

- A comprehensive risk calendar with selected highlights for the period July 19–August 1 across the Pacific Alliance countries and Brazil.

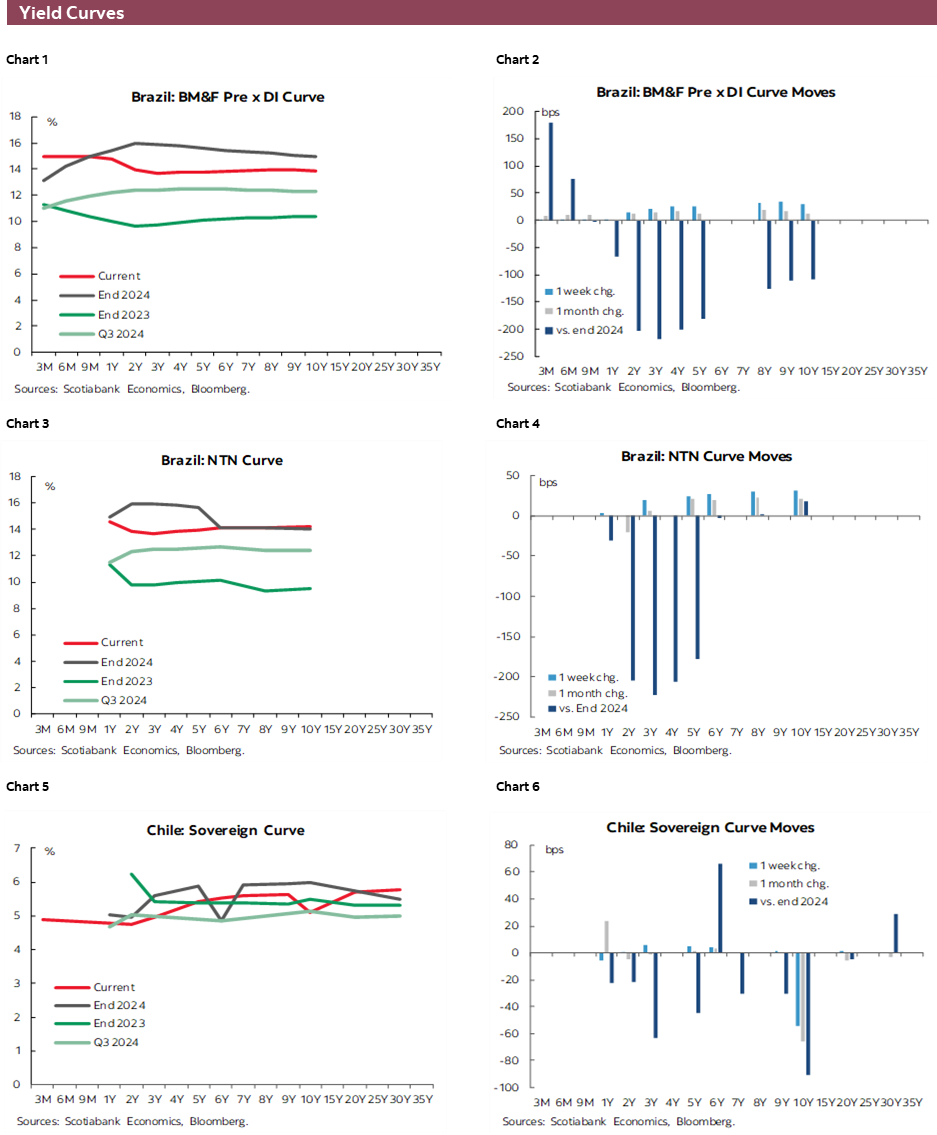

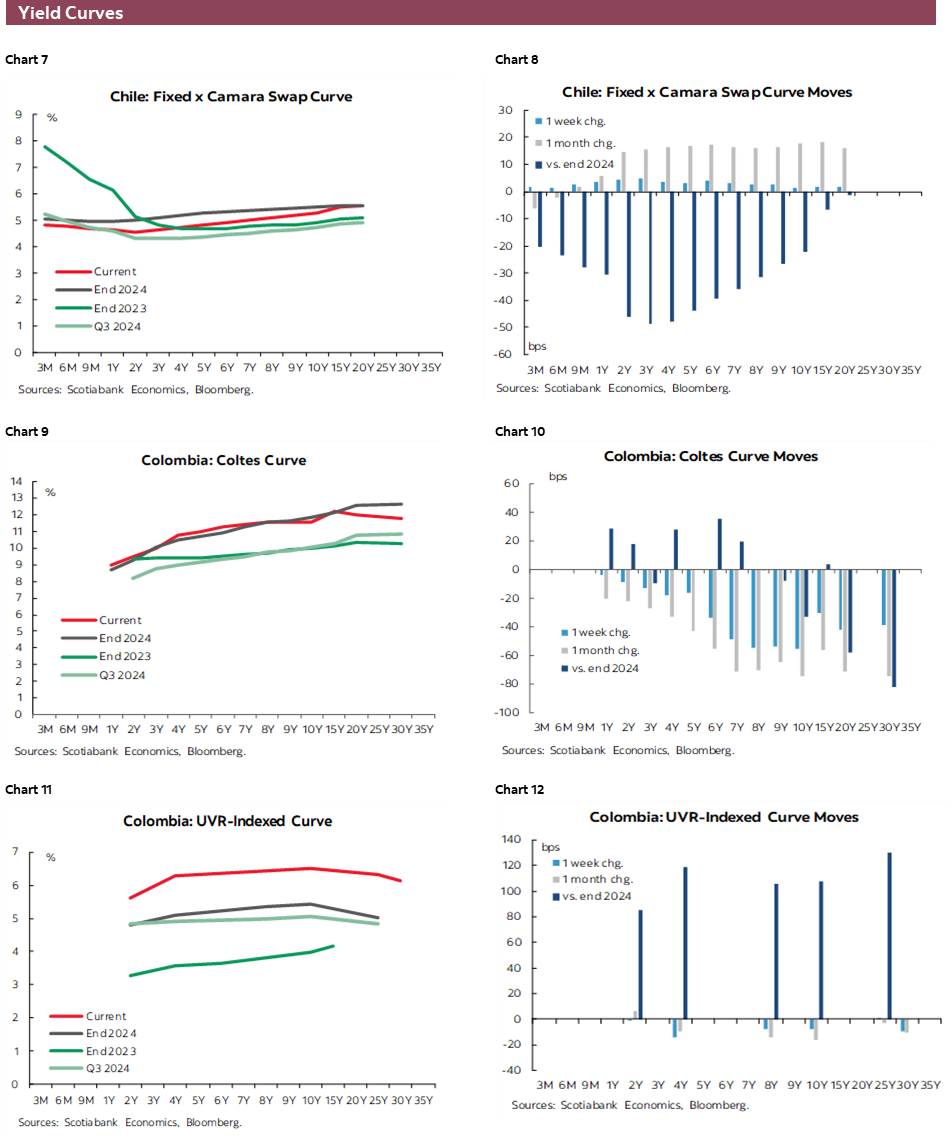

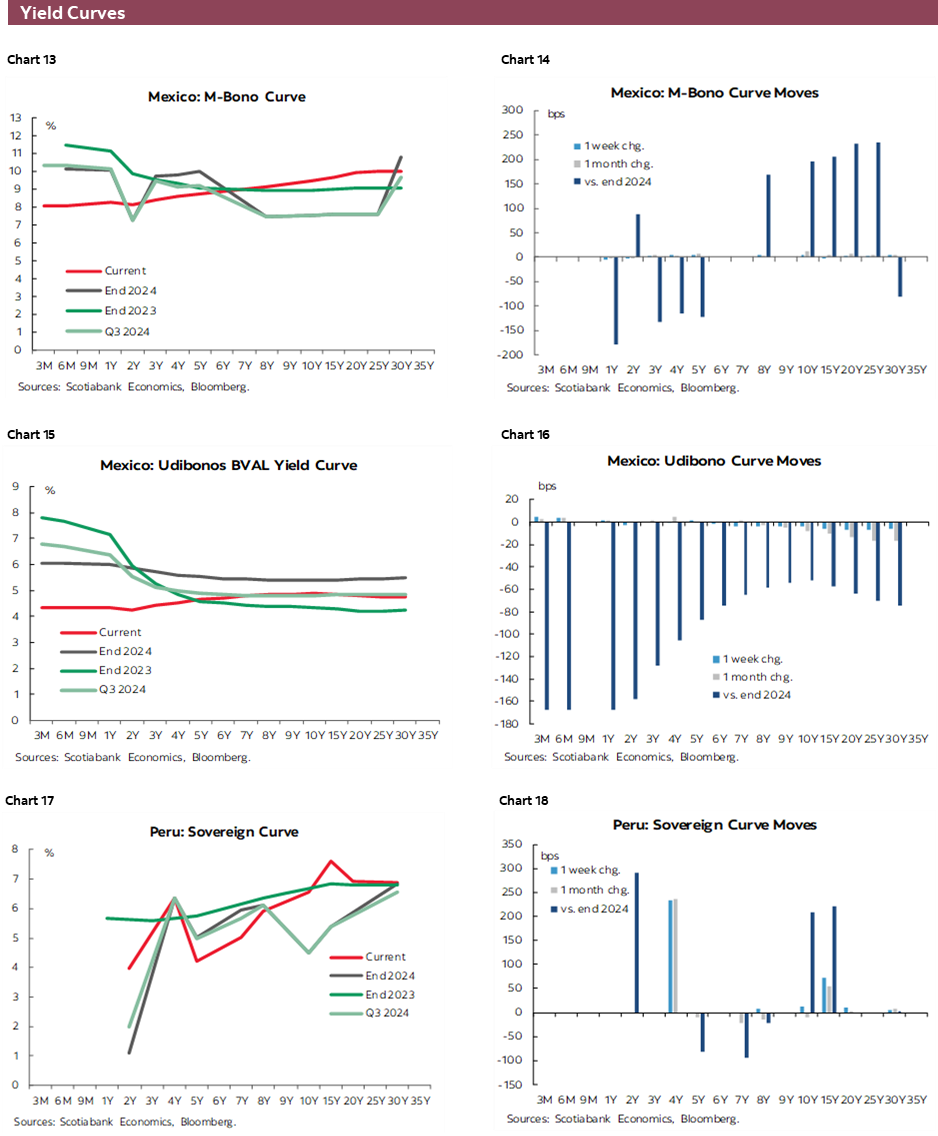

Chart of the Week

ECONOMIC OVERVIEW: MEXICO AND BRAZIL IN FOCUS

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Mexico and Brazil are in focus next week in Latam, with both countries releasing mid-month inflation data and facing an uncertain tariff outlook after sudden announcements by the White House in recent days.

- Mexico will also publish economic activity data that are expected to show only a muted recovery to growth in May, as covered by our local team in today’s Weekly. Economists in Citi’s survey will likely leave their estimates for rates, growth, and inflation little changed in next week’s results.

- Global PMIs, the results of Japan’s Upper House election on the 20th, the ECB’s likely rate hold, and Canadian retail sales are the highlight for global markets who will also have to follow Powell dismissal risks and unpredictable (though now usual) tariff announcements.

And so we head into another week of what will happen to U.S. tariffs and how these may be impacting the global economies. Announcements in recent days/weeks by U.S. President Trump of threatened 30% tariffs on Mexico (and 17% on Mexican tomatoes), 35% on Canada, and 50% on Brazil, as well as a multitude of new tariff rates on key countries, have seemingly done little to materially dent broad market sentiment.

Fears that Trump is considering firing Fed Chairman Powell have also been taken in stride by traders who lifted the S&P 500 to a fresh record high on Friday. That was all before reports on a 10–15% tariffs floor of imports from the E.U. emerged to dent gains to close the week. Still, markets seem fairly unfazed. The next two weeks will determine whether this optimism or resilience is warranted, where each passing day of not backing down from planned August 1st tariff hikes is likely to build anxiety in markets.

While global markets will follow what is decided on E.U. tariff rates, markets in Mexico and Brazil will pay close attention to their own duties. The U.S.’s decision to slap an additional 5ppts on its 25% tariff on non-USMCA compliant Mexican goods came somewhat out of nowhere as trade relations between both countries seemed steady and Mexico falls outside of the reciprocal tariff group of countries that awaited news in early-July.

A tariff hike to 30% would only amount to a few decimal points increase to the 4.3% effective duty rate that Mexican exports faced to the U.S. in May 2025 if all current exemptions hold on August 1st. But the move was another unexpected shifting of the goalposts by the White House that has again cast doubt on the sustainability of trade agreements made with the U.S. The 17% tariff imposed on Mexican tomatoes effective immediately, breaking a decades-long pact that regulates their price in exchange for duty free treatment, rubbed salt in the wound.

Brazil is also facing a huge 50% tariff next month that the U.S. has loosely based on the White House’s opinion on the treatment of former Pres Jair Bolsonaro rather than on protectionist reasons to boost the U.S. economy. The former Brazilian president was ordered to wear an ankle bracelet on Friday—on claims of obstruction of justice and him being a flight risk—ahead of an impending court date over accusations of attempting a coup in 2023. Bolsonaro’s trial has clearly caught the eye of President Trump, risking actions by the U.S. against the Brazilian economy. Lula’s highly-fractured relationship with Trump would suggest that these tariffs will come into force.

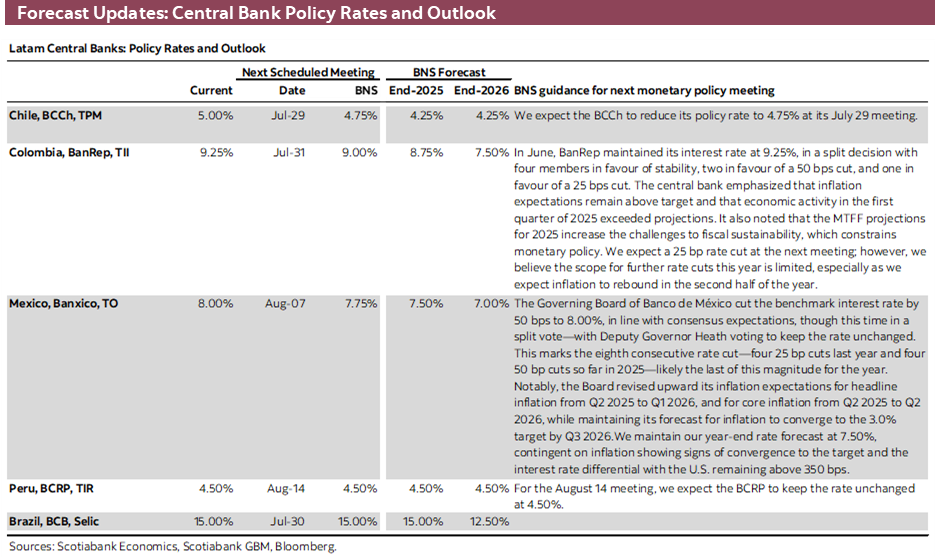

Next week’s main Latam data releases also come from Mexico and Brazil. Both countries will publish mid-July inflation which is expected to hold little changed in the latter yet decelerate in the former. Brazil’s IPCA-15 is forecast to remain at 5.3% in July for a fifth consecutive month above 5%, but with the winter months likely marking the high in inflation before marginally over the second half of 2025. The data are unlikely to do much to alter expectations for the BCB who is expected to hold steady until cuts in early-2026. Developments on the tariffs front and what that may do for the BRL or sentiment around Brazilian debt likely stand as the main risks to monitor for the BCB outlook.

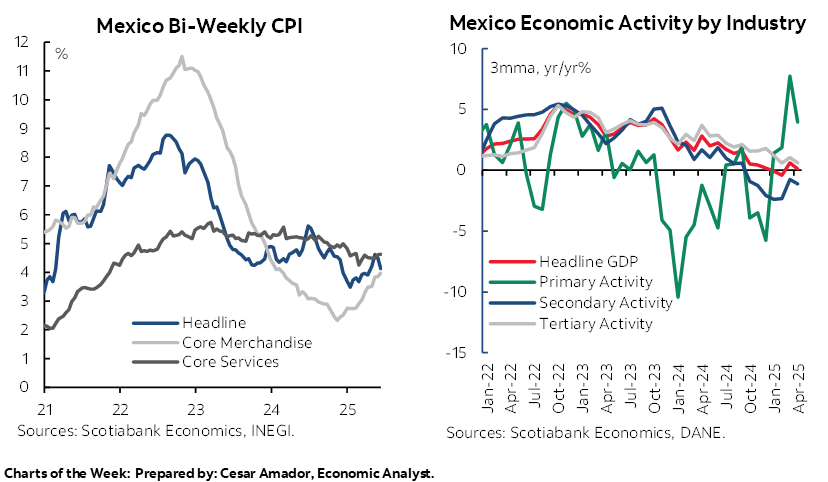

In today’s report, the team in Mexico previews next week’s data releases, starting on Tuesday with economic activity and retail sales figures, and the latest results to Citi’s survey of economists, followed on Thursday by H1-Jul CPI data. Mexico’s economy is estimated to have slightly rebounded in May after a contraction in April, but economic activity remains deeply muted with sub-1% growth expected for the month. After a few months of trending higher, inflation is seen slowing by about 0.5ppts in headline terms to near the mid-3s area thanks to base effects although core inflation is projected to sit practically unchanged around 4.3%—thus keeping Banxico alert. On that note, economists will likely leave their outlook for monetary policy rates steady, with a 7.50% median estimate for year-end (like us).

Chile, Colombia, and Peru calendars are fairly bare of major data or releases as Chilean PPI and the BCCh’s traders survey, and Colombian trade balance are unlikely to shake markets. Peru’s schedule is empty, but the team in the country provides an update on recent economic trends and risks in today’s Weekly. Briefly, “the main feature appears to be simple stability”. Outside of economic releases, Chile is hosting on Monday a high-level Democracy Forever summit with leaders from Colombia, Brazil, Uruguay, and Spain. Generally, these gatherings tend to offer little of note, but the recent experience of the BRICS summit that attracted the wrath of Donald Trump presents the risk that a poorly-received communique could result in tariff threats by the U.S. leader.

Outside of the Latam region, Thursday will be packed with global PMIs, the ECB’s rate decision, and Canadian retail sales data. The PMIs will give us the freshest look into how the tariffs rollercoaster continues to influence output, hiring, and prices decisions around the globe with economists expecting steady or marginally higher readings for the major economies. The ECB is expected to hold rates unchanged for the first time in a year, having delivered a cumulative 200bps in cuts since June 2024 and nearing the end of its easing cycle, to take a breather and evaluate the effects of easing to date as well as risks to growth. Friday offers U.K. retail sales and Tokyo CPI data, but Japanese markets will take their cue from the results of Upper House elections this Sunday (the 20th) with decent odds that the Ishiba ruling coalition loses its majority in the chamber (note that Japanese markets are closed on Monday).

PACIFIC ALLIANCE COUNTRY UPDATES

Mexico—Slight Recovery in Weak Economic Activity, With Mixed H1-Jul CPI Data

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Next week will be key in terms of economic indicators, as they will help assess the momentum of the economy and its potential contribution to easing inflationary pressures in the short term.

On Tuesday, retail sales data for May will be released. These figures are expected to show some resilience despite job losses in the formal labour market, or they may deepen the negative trend observed in April (-2.0% y/y). In that month, the sectors that contributed most to the decline were motor vehicles, auto parts, fuel, and lubricants (-5.5% y/y), as well as groceries, food, beverages, ice, and tobacco (-4.3% y/y). It is worth noting that light vehicle sales in May fell -2.0% y/y, an improvement from the -9.9% contraction in April, which could suggest a moderation in the decline of consumption.

The Global Indicator of Economic Activity (IGAE) for May will also be published on Tuesday. An annual rebound of 0.41% is expected, following a -1.55% drop in April. In seasonally adjusted terms, the INEGI’s Timely Indicator of Economic Activity (IOAE) estimates a 1.0% annual increase in May, driven mainly by the services sector (+1.6%), while industrial activity is expected to remain in negative territory (-0.4%).

Additionally, Citi’s survey of expectations will be released on Tuesday. It will be important to monitor any adjustments in inflation forecasts for 2024 and 2025, particularly in light of persistent pressures in the core component. Despite this, we do not anticipate a change in Banxico’s next move, which is expected to be a 25 basis point rate cut to 7.75% in the August monetary policy decision. In this context, it is likely that survey respondents will maintain their forecast for Banxico’s terminal rate in 2025 at 7.50%. It will also be relevant to track whether downward revisions to the expected exchange rate continue and whether analysts adjust their growth outlook for the remainder of the year.

Finally, on Thursday, inflation data for the first half of July will be released—a key figure to assess whether inflationary pressures are beginning to ease. Market consensus anticipates a decline in annual headline inflation, from 4.13% in the second half of June to 3.67%, partly explained by a base effect, as the same period in 2024 came in at 5.61%, its highest lecture during that year. However, core inflation is expected to edge up slightly, from 4.28% to 4.30%, which could maintain some pressure on Banxico’s Governing Board regarding the pace of coming interest rate cuts.

Peru’s Steady State

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

Wherever you look, whether it’s GDP growth, inflation, interest rates, the exchange rate, fiscal and external accounts, and even, to an extent, politics, the main feature appears to be simple stability.

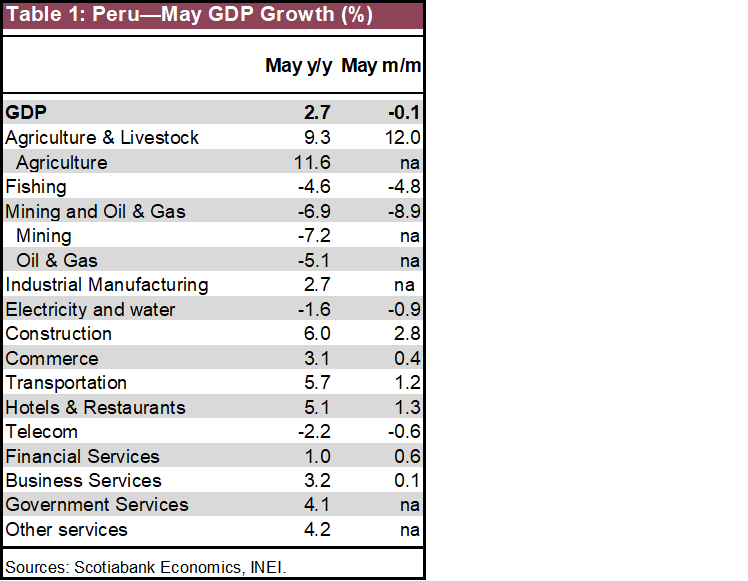

GDP growth gave us a bit of a scare in April and May, with low growth for both months. And yet, in both months, sectors linked to domestic demand have continued performing well, at around 3.5% (table 1).

Of the four sectors with negative YoY growth in May, three were resource sectors not linked to domestic demand (mining, oil & gas and fishing), while the fourth, telecom, has been struggling for some time. The 7.2% YoY decline in mining was mainly the result of a temporary closure of the Shougang iron ore mine, which later reopened in June. This closure was also probably largely behind the 1.6% YoY decline in electricity. The outlier was agriculture GDP, up a huge 11.6%, YoY. This was no doubt largely due to shifts in the harvest schedule, but is also linked to a simply good year, including agroindustrial exports to the U.S. (chart 1).

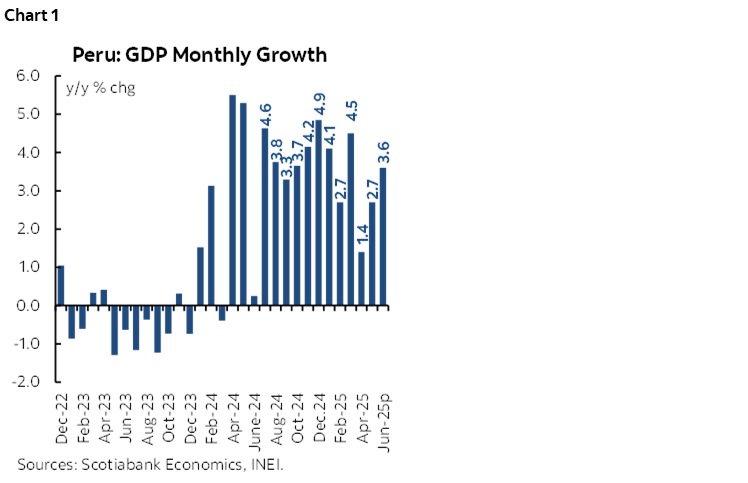

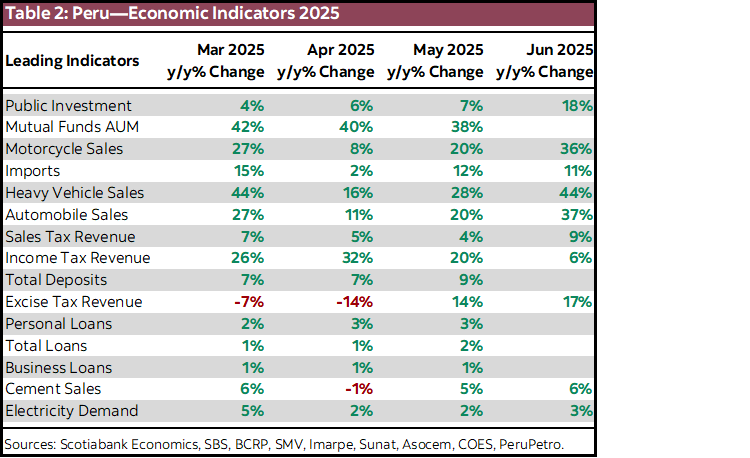

So, should we worry about the slowdown in GDP growth. Well, the lower than expected figures for April–May do make it a bit more difficult to reach our full-year forecast of 3.3% GDP growth. But, at the same time, the fact that domestic demand continues to grow just as well as we had been expecting is encouraging. Barring extraordinary events going forward, our 3.3% forecast continues to be in the cards. Furthermore, leading indicators for June appear healthy, and surpass handily the numbers for April and May (table 2). In fact, a number of the indicators are aligned with levels of growth seen in March, when GDP growth reached 4.5%. We’re not that optimistic, however, and expect 3.6% GDP growth for June.

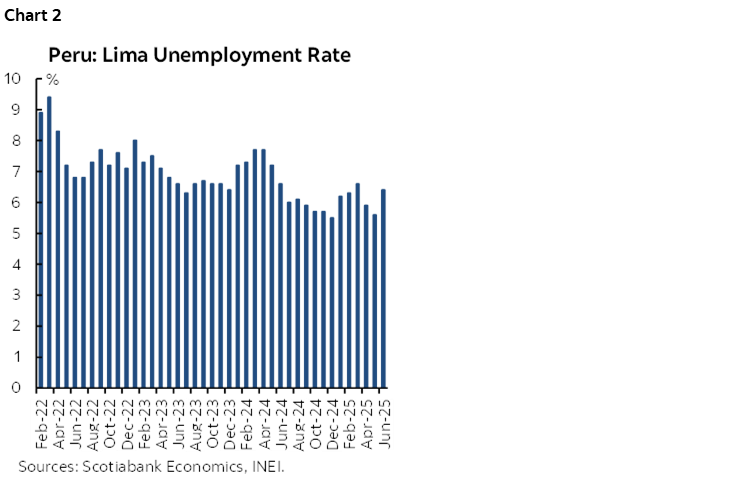

The dynamics of the labour market continue to be robust, although the momentum is slowing. Lima unemployment in June continues to be lower than for June in previous years, but overall the unemployment rate no longer seems to be declining since December 2024 (chart 2).

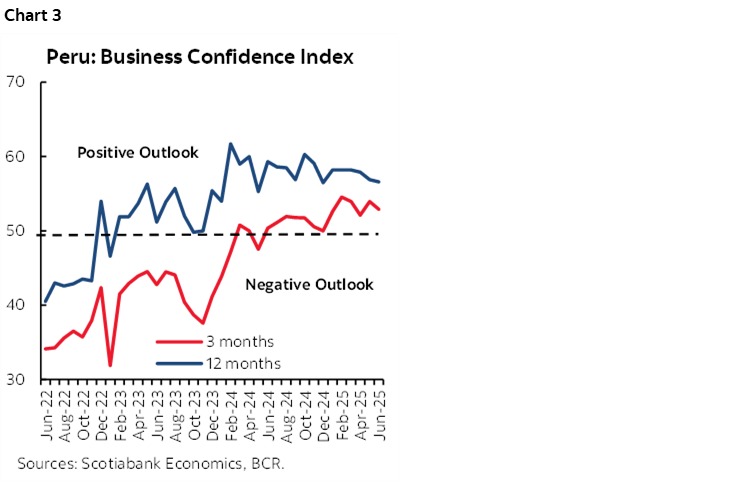

There is little evidence of either Trump’s tariffs or local politics having an overt impact on economic variables in Peru at this point in time. If one looks at the business confidence index, an argument could be made that it is slowly starting to decline (chart 3). We are, after all, less than nine months away from Presidential and Congressional elections in April 2026. Noise surrounding the elections is starting to increase. August 2nd is the deadline for the 42 political parties registered to be able to participate in the elections to join together through alliances and joint candidacies.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |