KEY CONCLUSIONS

- Mexico’s economy has evolved as we had broadly expected during the first half of the year, remaining on a weak growth path alongside a dearth of optimism due to important domestic and external headwinds.

- The local business economy remains sluggish, with a long-lasting hangover that started after the mid-2024 elections and subsequent flurry of constitutional reforms and continues to be underpinned by foreign risks such as U.S. tariffs and possible drags on Mexico from U.S. immigration policies and weaker growth stateside.

- In line with weak business sentiment, formal employment growth has now slowed to a crawl with practically no jobs gained over the past 12 months. Gross fixed investment has printed eight straight monthly negative results, with an average -6.8% in 2025 so far.

- On top of weaker economic prospects, Mexican inflation has also recently accelerated, thereby pumping the brakes on Banco de México’s (Banxico’s) dovish stance, with the central bank now nearing the end of its easing cycle.

- Banxico rate cuts have supported credit growth to around pre-pandemic levels (in real terms), though heightened uncertainty and the nearing end of rate cuts may limit further expansion.

Mexico’s economy has evolved as we had broadly expected during the first half of the year, remaining on a weak growth path alongside a dearth of optimism due to important domestic and external headwinds. The local business economy remains sluggish, with a long-lasting hangover that started after the mid-2024 elections and subsequent flurry of constitutional reforms and continues to be underpinned by foreign risks such as U.S. tariffs and possible drags on Mexico from U.S. immigration policies and weaker growth stateside.

The path for growth in Mexico remains highly dependent on the evolution of U.S. trade policy, which, as it stands currently, should at best leave gross domestic product (GDP) practically unchanged in 2025, to be followed by only muted growth in 2026. Our forecast for a small contraction in 2025 could be seen as a worst-case scenario (and among the most negative on the Street), as it considers stricter U.S. tariffs than those currently in place while we await firmer signals from the United States that these more “relaxed” duties will stay in place. Nevertheless, while Mexico may have avoided the worst of U.S. tariffs for now, direct and indirect impacts are significant.

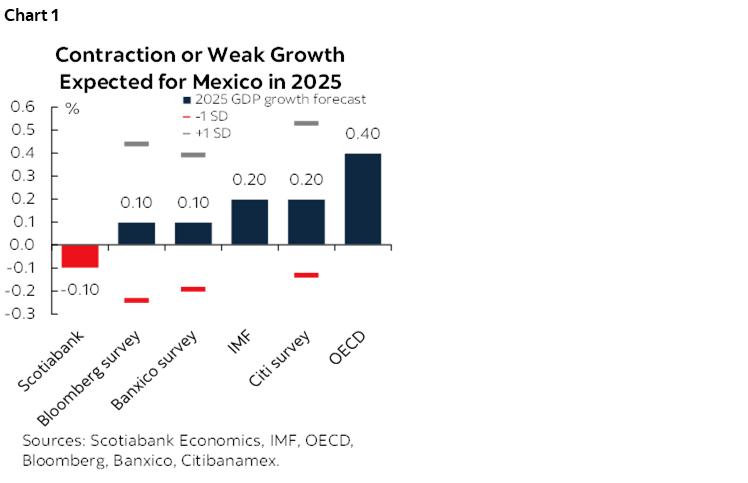

Mexico’s economy is widely expected to lag all countries in LatAm in 2025, with its projected performance for the year at least ~2 percentage points (p.p.) weaker than major peers in the region (chart 1). Economist surveys and key multinational organizations alike forecast 2025 GDP growth to be practically non-existent, with the bulk of estimates ranging from -0.3% to +0.5%. The variability in these estimates is mainly due to differing assumptions for the final level of tariffs imposed on Mexican goods and the intensity of their impact. Our -0.1% call is a slight outlier, as it still assumes high tariffs while we await greater clarity. The International Monetary Fund’s (IMF’s) recent reassessment to 0.3% in its July update from -0.2% in its April report also reflects shifting tariff goalposts. The IMF’s spring outlook incorporated a 25%–30% U.S. global tariff rate compared with its summer report where 15%–20% was assumed.

Our and others’ projections for Mexico’s economy in 2025 fall well short of the 2.2%–3.3% GDP projections for Brazil, Chile, Colombia, and Peru by our local Economics teams (chart 2). While the Mexican economy may improve in 2026, it will continue to underperform peers, reflecting ongoing structural weakness in investment and hiring in the country, as well as a greater direct impact from U.S. tariffs on exports and ongoing business uncertainty (with United States-Mexico-Canada Agreement [USMCA] renegotiation in 2026 also being a large unknown on the horizon).

GROWTH TO DATE IS UNDERWHELMING, AND HEADWINDS OUTNUMBER TAILWINDS

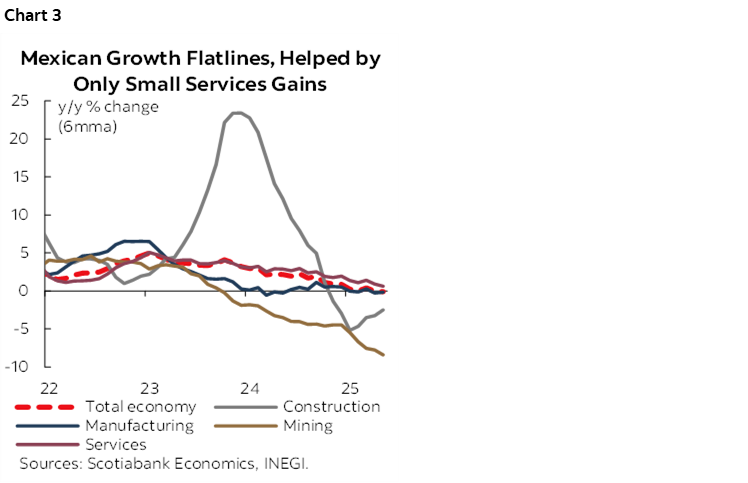

Per industry data as at May 2025, Mexican GDP has shown no growth when compared with the same period in 2025. Year-to-date, ongoing contractions in the extraction and construction sectors have now been joined by a small pullback in manufacturing, while services sector growth has slowed to a crawl (chart 3). Leap-year and Easter-timing effects have complicated the interpretation of activity data in the country, but the trend remains one of underwhelming momentum with no clear triggers for an acceleration in activity and more headwinds than tailwinds.

In Q1/25, Mexico’s economy managed an only 0.2% quarter-over-quarter (q/q) expansion as contractions in household consumption and investment were only partially offset by a large decline in imports and a modest rise in exports. We do not yet have an expenditure breakdown of Q2/25 GDP numbers, but those for the three main activity sectors show that the economy grew by 0.7% q/q, with greater momentum in secondary sectors (mining, utilities, construction and manufacturing) and tertiary sectors (services) against a decline in volatile primary activity (agricultural). As mentioned above, although trade-related kinks and calendar effects muddle readings of these data, Mexico’s 0.3% q/q average pace of growth in 1H/25 is underwhelming.

Growth, or the lack thereof, for the balance of the year will likely reflect a mix of muted household demand alongside softness in manufacturing—as some tariff front-running flips and is followed by weak external orders—and scaled-back investment due to elevated uncertainty.

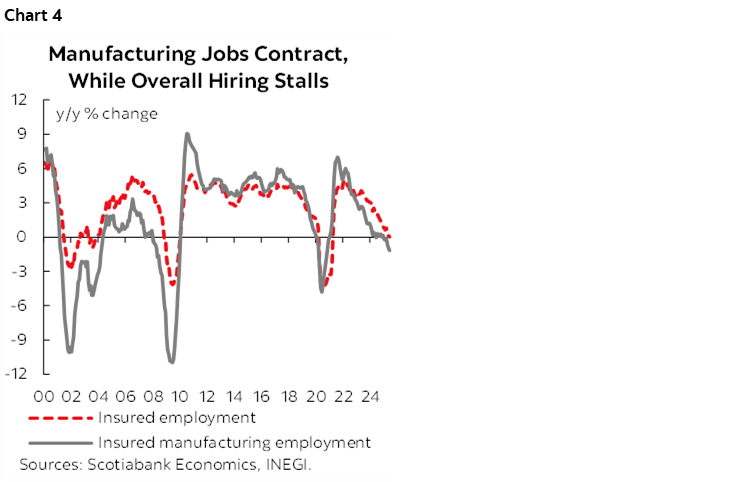

From a domestic standpoint, household consumption should remain subdued with hiring appetite having evidently soured, worsening a decelerating trend that began in mid-2023 (when insured employment was expanding by nearly 4%) through today (no growth year over year [y/y] as at June 2025). Continued declines in (1) construction and mining headcounts and (2) energy headcounts are no surprise given the end of former President Andrés Manuel López Obrador’s (AMLO’s) mega infrastructure projects and Pemex’s workforce reduction, respectively.

However, after holding flat through most of 2024, job losses in the manufacturing sector point to tariff-related pessimism among manufacturers (chart 4, more on this below), including the expectation of limited opportunities for expansion in the near term. Employment in services-oriented sectors remains positive, though muted (and liable to remain so) amid sluggish economic and aggregate income growth. Per data for insured employment going back to 1994, Mexico has never experienced zero or negative jobs growth—as at present—outside of recessionary periods.

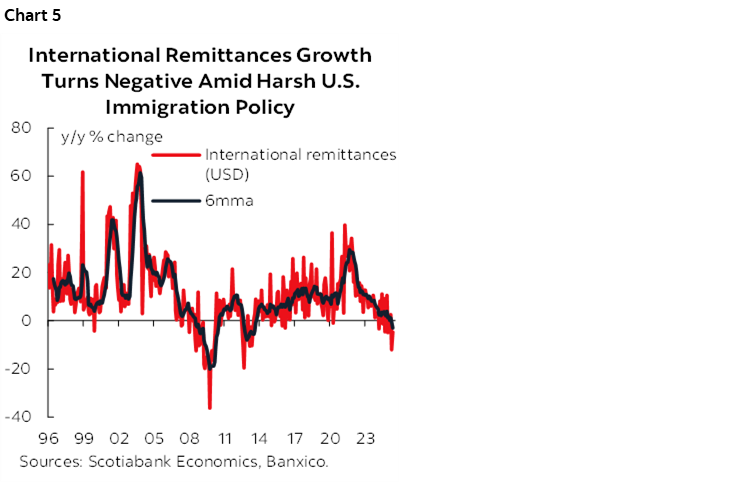

Remittance flows to Mexico are an important source of income for households in the country, but recent data show that strict U.S. immigration policy has stopped this growth in its tracks… and possibly reversed it (chart 5). From January 2020 to December 2023, international remittances averaged ~15% y/y growth, with full-year 2023 growth of 7.6% followed already by a significant deceleration to 2.3% in 2024. Now, through the first five months of the year, remittances are contracting at an average pace of 2.7% y/y. On a relatively positive note, the recently passed One Big Beautiful Bill Act in U.S. Congress imposed only a 1% tax on cash remittances sent by non-U.S. citizens, which should have a negligible impact on aggregate flows. However, that is but small comfort for the negative outlook for remittances, where fear of deportation may be keeping undocumented Mexican immigrants in the United States from working, while U.S. southern border apprehensions falling to their lowest level on record (going back to 2011) also point to the dwindling numbers of new entrants—the source of new remittance senders.

In tandem with softening consumption growth, private and public investment in Mexico is due to fall in 2025, with the former weighed down by domestic and external uncertainties and the latter coming off a period of strong growth under AMLO that is now being limited by tight public finances.

Gross fixed investment in Mexico contracted by nearly 7% y/y in the first third of 2025 (chart 6), with public expenditures declining 20%+, continuing the negative trend since mid-2024, but also accompanied by a 5% drop in private investment (mainly due to a sharp contraction in machinery spending) that had managed to stay in positive territory through most of 2024. The government forecasts public investment will likely represent 2%–3% of GDP, which is arguably below the level required to maintain the existing capital stock, let alone catch up with important bottlenecks in key sectors such as power, where spare generation capacity sits near a 40-year low—a factor that can constrain possible opportunities for private investment.

Heightened tariff uncertainty and softer growth in North America mean there is little appetite on both sides of the border to invest in expanding capacity. Idiosyncratic factors such as uncertainty from constitutional reforms, worsening security conditions for businesses, and a lack of investment in public services (e.g., water supply, electricity generation) remain negatives for domestic investment over the short to long term. Meanwhile, Mexico’s cash-strapped government (more on this below) does not have the financial latitude for large public works, with knock-on effects in the construction and construction equipment sectors.

Public spending will not be a catalyst for growth this year—quite the opposite. As mentioned in our team’s note on 2026 macroeconomic pre-criteria, the Mexican government is planning significant public spending cuts this year (a 3.0% decline in real terms) aimed at reducing the fiscal deficit to 4.0% after it reached a historic high of 5.7% in 2024 (partly due to it being an election year). While it is not yet a major concern, investors are paying attention to potential changes to Mexico’s sovereign credit rating outlook. Moody’s has assigned Mexico a Baa2 rating with a negative outlook. A key element on this front could be the government’s long-term plan for Pemex (likely presented around Q3). Although we do not currently expect important revisions, any developments to the plan in the second half of the year and compliance with the Ministry of Finance will be in the spotlight for rating agencies and investors.

Public finances remain a question, with the government’s adjustments focused on cutting investment in an economy that is already struggling with serious bottlenecks in infrastructure, such as power and water. The recent surge in tax collection despite a flat economy can be partly explained by efficiency gains, but it could also be linked to very high batting averages in fiscal litigation, which could have adverse side effects down the line. For now, the outlook for the country’s credit ratings, particularly Moody’s negative outlook, could depend on meeting fiscal targets and the soon-to-be-announced plans to restructure Pemex.

TARIFFS ARE A NEGATIVE, BUT CURRENT LEVELS WOULD BE MANAGEABLE ON AGGREGATE

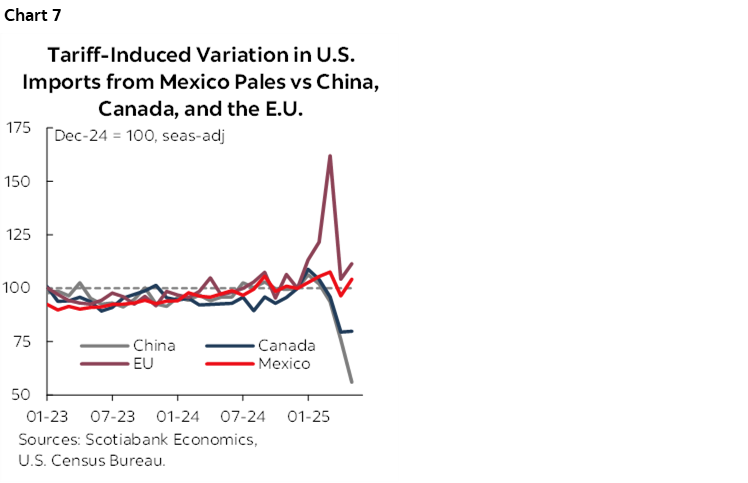

While ever-shifting tariff goalposts and announcements have made it difficult to evaluate the current level of tariffs on Mexican exports to the United States, the country’s effective tariff rate on all goods is relatively manageable for the performance of the external sector—were it to hold. The White House often advertises that Mexico “pays” a 25% tariff on its shipments to the country with specific duties on certain items (namely, steel, aluminum, and vehicles), but USMCA-compliant or secondary auto parts exemptions go a long way to lowering the duty rate that is effectively in force. In the year ended May 2025, U.S. imports from Mexico have also increased by 6.5% y/y, pointing to some modest, though not explosive, tariff front-running (chart 7). A relatively small 1.1% q/q rise in exports of goods and services in Q1, combined with a large 4.3% q/q drop in imports to reduce the drag of net trade on real GDP during the quarter, offset declines in household consumption and investment, resulting in a muted 0.2% q/q expansion in output to start the year.

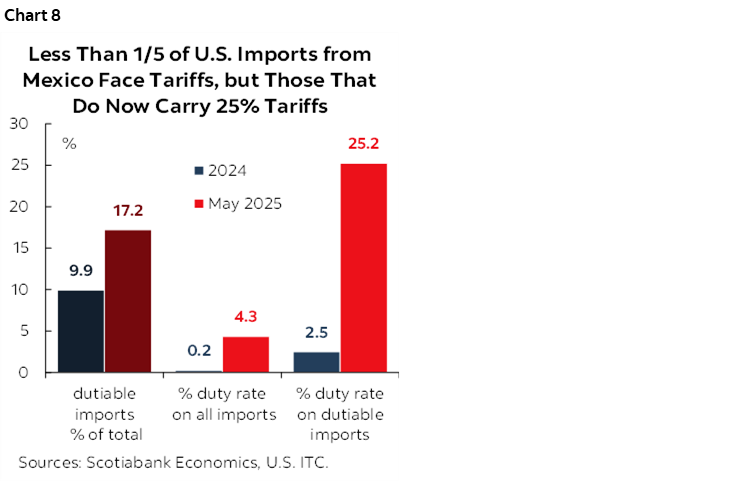

U.S. International Trade Commission (ITC) data show that across all U.S. imports from Mexico, buyers were levied an effective customs duty rate of 4.3% as at May 2025 (chart 8), representing an increase of about 4 p.p. from its level through 2024. Mexican officials—namely, Economy Minister Marcelo Ebrard—have stated that 85%–90% of all Mexican exports to the United States are compliant with USMCA and thus enjoy duty-free advantages. This would be the case even if an important share of U.S. imports from Mexico generally do or do not claim this benefit given zero or minuscule most-favoured-nation tariff rates. The U.S. ITC’s data seems to roughly align with these figures, as only 17% of imports from Mexico were subject to duties in May, up from around 10% in 2024 (under low rates).

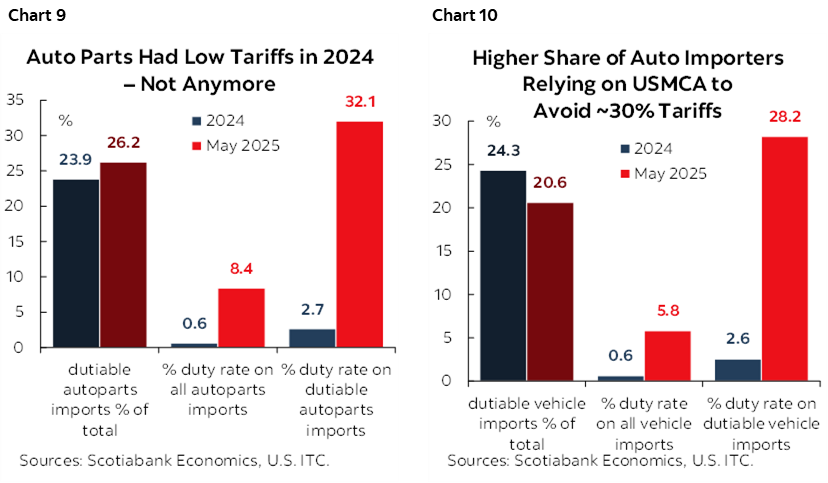

If the United States’ effective tariff rate remained at 5%, Mexico would have avoided feared 25%+ tariffs on all northbound exports. However, a narrower look at the data shows that there are important sectors hurting from these levies and facing heightened uncertainty over future tariff rates (charts 9 and 10). As such, Mexican manufacturers are highly unlikely to expand capacity, whether it is via higher headcounts or increased investment spending (on top of elevated borrowing rates). As at May 2025, U.S. data showed that an overall 4.3% duty was collected on its imports from Mexico, with the share of goods that were subject to duties rising from about a tenth in 2024 to under a fifth that month. That said, while that 10th faced only a 2.5% tariff rate on aggregate, the current 15%–20% of dutiable goods now face an effective tariff rate of 25%. Even though the overall impact would seem limited, there are important divergences across various exporting sectors.

While the United States’ recent announcement of a potential 5 p.p. hike to Mexico’s tariff rate (to 30%) was withdrawn at the last minute, it was still a step in the wrong direction for trade relations between the two countries, although the tariff increase itself was perhaps not the most impactful news. Based on imports data, the hike may amount to an increase of only a few decimal points in the overall effective tariff rate, with a greater impact on a subset of goods not eligible for duty-free treatment or tariff “discounts.”

The latest move has, however, turned around what seemed to be a slow path toward trade reconciliation, now lifting the odds that the United States moves ahead with tariffs on secondary auto parts (currently exempt) or narrows/ends preferential treatment for USMCA-compliant goods or the United States–sourced value of vehicles and key parts. Copper is a minor share of Mexico’s exports to the United States, but high tariffs on the metal would result in additional weakness in the U.S. manufacturing sector, which drags on Mexico’s. The tariff hike was also soon followed by a 17% levy on Mexican tomatoes and the suspension of a long-standing bilateral treaty that set a minimum on their export price. Although tomatoes may represent just under 1% of all U.S. imports from Mexico (2024 data), the end to the agreement highlights that little is safe from sudden U.S. trade actions. Put another way, what’s next?

BANXICO HAS NEARED THE END OF ITS CUTTING CYCLE

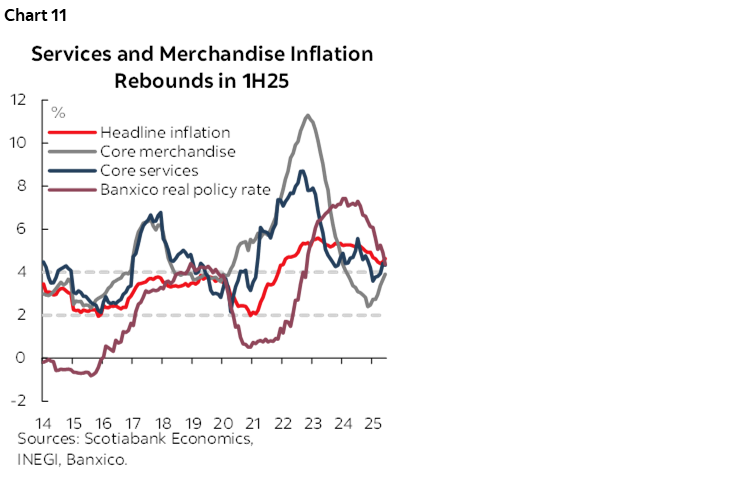

In spite of weaker economic prospects, Mexican inflation has also recently accelerated (chart 11), pumping the brakes on Banxico’s dovish stance—and in turn limiting the support that lower rates could have provided for economic activity. From reaching a cycle low of 3.6% in January, inflation has picked up to 4.3% as at June, quickening across all main components of the basket except for transportation thanks to lower gasoline prices. Of note, core merchandise inflation has sped up from 2.4% in November 2024 to near 4% as at the latest reading, with producers and importers likely affected by tariffs and still-strong wages and material costs. Core services inflation has slowed since the start of the year, though mainly on the back of slowing housing prices.

Inflation developments over the past few months have resulted in a reassessment of expectations among economists that has motivated greater caution among Banxico board members. While early 2025 data prompted economists to slightly trim their forecasts for end-2025 headline inflation to 3.7%, figures that have since followed have pushed the median estimate to 4.0% as at June. Economists also expect only a marginal slowing of inflation next year, with the median eyeing a year-end rate of 3.74%. At Scotiabank Economics, we also project inflation will close 2025 and 2026 at 4.0% and 3.7%, respectively.

While Banxico delivered a half-point cut at its June decision, the split vote and increased worries about upside inflation risks suggest that officials may soon consider a rate hold. Markets are pencilling in an 80% chance of a 25 bp rate cut at the August announcement that could be the last reduction of the cycle, leaving the overnight rate at 7.75% (at least temporarily).

We think Banxico still has two more cuts left in the chamber this year, followed by an additional 50 bp in 2026, for a terminal rate forecast of 7.00% that is in line with economists polled by Banxico. However, we are keeping a close eye on U.S. Federal Reserve guidance as well as developments on the tariff front. Mexico’s precarious fiscal situation has also possibly translated into a higher risk premium for local rates, resulting in a higher long-term neutral rate versus pre-pandemic, thus capping Banxico’s capacity to deliver much more in terms of additional cuts.

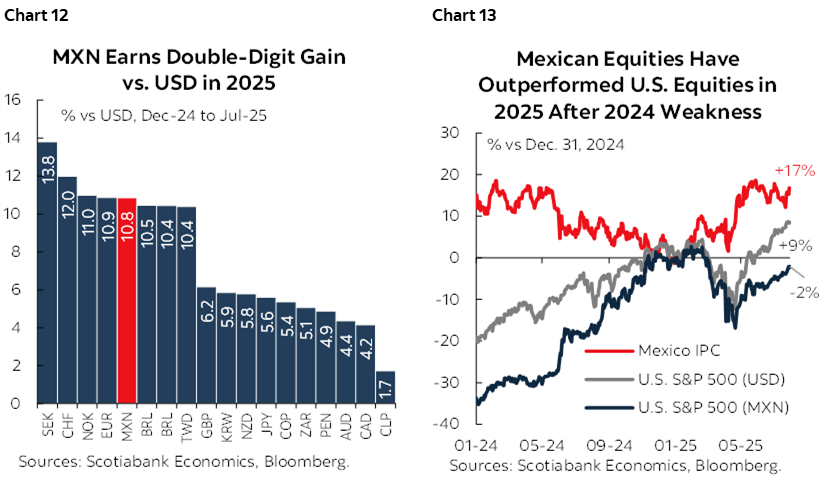

The performance of the Mexican peso (MXN) has been a welcome offset to domestic price pressures and Banxico’s assessment of risks (chart 12), appreciating by 10%+ year-to-date (leading Latam foreign exchange for the year) despite external risks. Regardless of the 2 p.p. narrowing of the Mexico-U.S. policy rate differential this year to 350 bp, the attractive return that short-term Mexican debt (or even deposits) offers has helped a greater share of domestic funds parked at home. Mexican stock markets have also enjoyed a ~17% gain for the year in MXN terms (chart 13), about double the gains in the S&P 500 in USD terms (and well beyond its ~2% drop in MXN terms).

Credit growth in Mexico remains healthy, with commercial bank lending to the private nonfinancial sector up by 13% y/y as at May 2025 against a slower growth rate in credit to households of 10%, where weak soft trends in borrowing for housing (+6.5% y/y in May) mixed with stronger consumer loans. Nonperforming loans (NPLs) at Mexican banks are also holding at historical levels, with a ~3% NPL ratio for consumer credit and under 1.5% for commercial lending. Risks to the financial system seem relatively limited overall, but relations with the United States and concerns about the trajectory of Mexican public debt remain on the radar.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.