FORECAST UPDATES

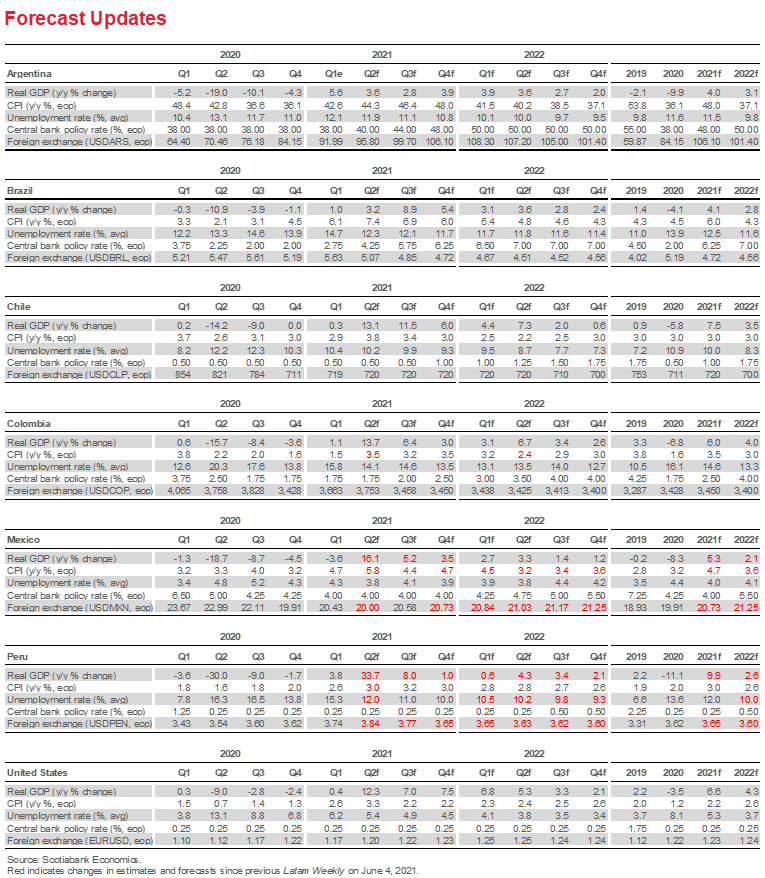

- What the bounce back gives, base effects take away. Faster growth and higher inflation readings have led to forecast revisions in Mexico and Peru. But higher y/y numbers this year (raising the base) result in modest downward revisions for 2022.

ECONOMIC OVERVIEW

- The Fed’s hawkish dot plots raises the spectre of less favourable global financial conditions.

- Latam central bankers will need to connect the dots, in terms of where global rates are going, and mind output gaps as inflation rises.

- Rising rates put a premium on sound public finances and stable policy frameworks.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico, and Peru.

MARKET EVENTS & INDICATORS

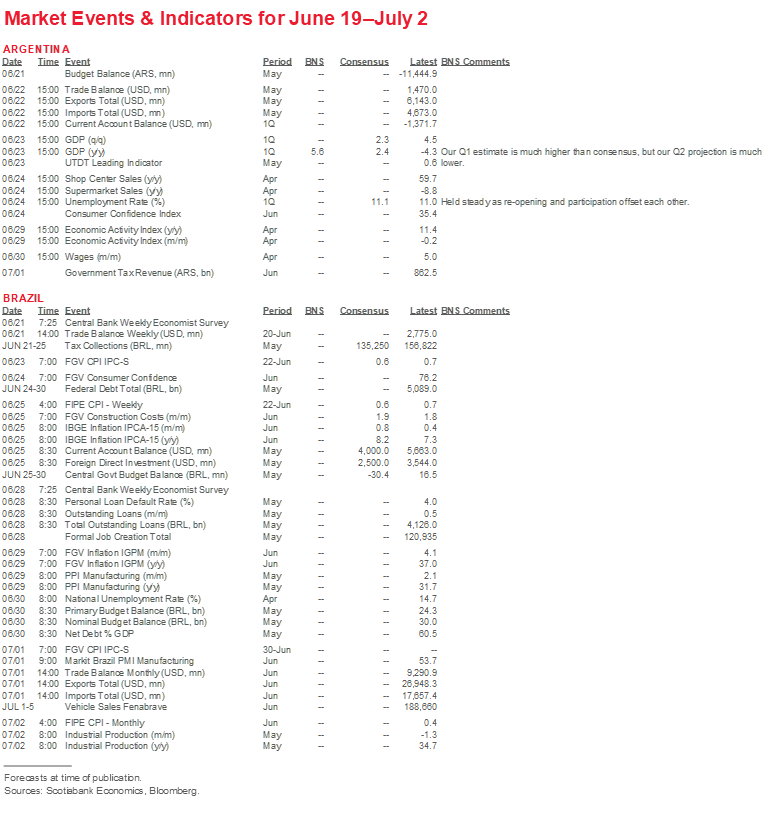

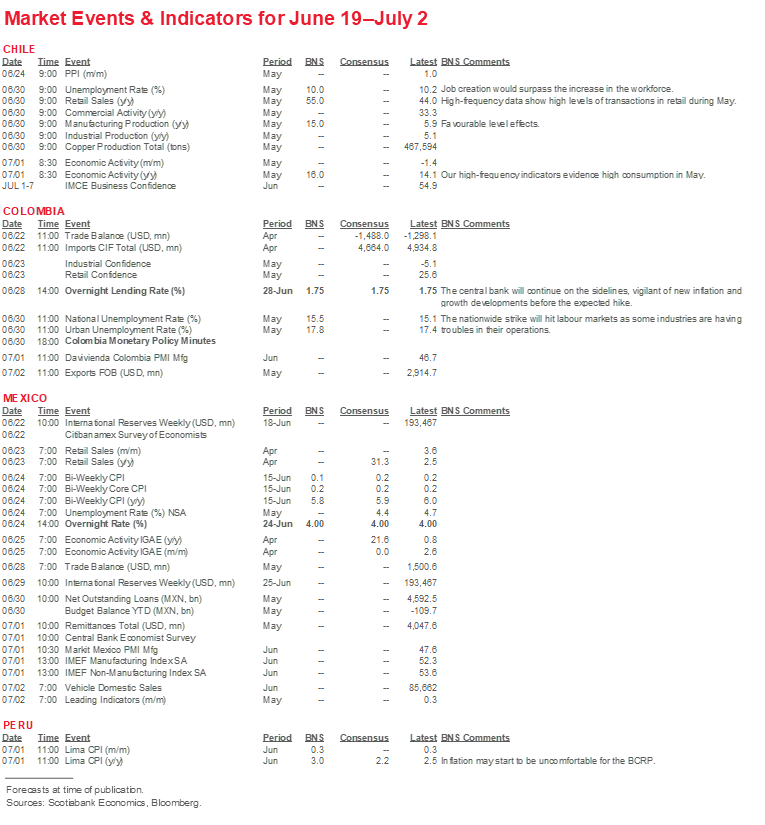

- A comprehensive risk calendar with selected highlights for the period June 19–July 2 across the Pacific Alliance countries, plus their regional neighbours Argentina and Brazil.

Economic Overview: Connect the Dots, Mind the Gap

James Haley, Special Advisor

416.607.0058

Scotiabank Economics

jim.haley@scotiabank.com

- A hawkish Fed dot plot chart creates a more challenging policy environment.

- Central banks will have to parse what the dots mean in terms of future rates, and monitor output gaps that are closing as their economies rebound.

- Less favourable global financial conditions put a premium on sound public finances and stable policy frameworks.

CENTRAL BANKING IN A (SLIGHTLY LESS) ZERO RATE WORLD

Global financial markets were surprised by the Fed’s hawkish dot plot chart showing the median expectation of Fed governors now with two rate hikes in 2022, which was published at the conclusion of the June 16, 2021 meeting of the Fed Board of Governors. US Treasuries and equities sold off on the news, with European and Asian markets following close behind. Not surprisingly, Latam financial markets broadly mirrored global trends.

The Fed’s announcement is certain to focus minds on central banks’ policy responses in coming weeks. As noted in the May 21, 2021 Latam Weekly, signs that G10 central banks were preparing to taper—or at least talk about tapering—asset purchases in the face of rising inflation were already raising expectations that emerging market central banks would have to accelerate their normalization process.

In calibrating future policy moves, Latam central banks will have to “connect the dots,” discerning how Fed governors’ beliefs regarding the path of US rates are likely to play out in terms of global interest rates.

And central banks will need to “mind the gaps.” That is, monitor the pace at which their economic recoveries close output gaps (the difference between potential output and the actual level of GDP)—a key determinant of inflationary pressures.

Monitoring the path of recovery on month-to-month basis is complicated, however, by year-over-year base effects and clouded by uncertainty with respect to ongoing effects of the pandemic. In Chile, for example, the re-imposition of a lockdown in Santiago underscores the need to contain COVID-19, though high vaccine rates, mobility passes and a population that has adjusted to life under lockdowns are expected to limit the impact on a robust rebound in activity. The pandemic has also led to supply bottlenecks, disrupting production and generating price prices. These effects should be relatively short-lived. Possible “scarring” effects on the economy, resulting from the destruction of idiosyncratic relationships in the supply chain and firm-specific human capital investments, may be more persistent. Central banks will have to asses the extent to which the pandemic has reduced potential GDP going forward. Our team in Colombia estimates that the pandemic will shave 1 percentage point of growth off potential GDP over the next five years.

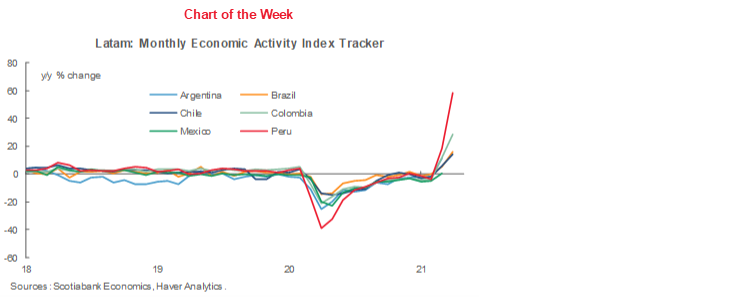

Gauging the impact of local currency depreciation and exchange rate pass-through effects on inflation will be an important element of “minding the gap.” In this respect, the prospect of higher global rates and stronger US dollar warrants close monitoring, especially against the backdrop of exchange depreciation earlier in the year (chart 1). Higher import prices and possible local currency depreciation are clearly on central banks’ radar screens.

The prospect that US rates could move higher at a more aggressive pace than previously expected could have spillover effects in foreign exchange markets. The Fed seems attuned to such concerns in that, in releasing its minutes and dot plot charts, it announced it would extend to end-2021 US dollar liquidity swap agreements it has with nine central banks, including the Banco Central do Brasil and the Banco de México. These agreements, which were initially extended in the global financial crisis, and resurrected in March 2020 as the pandemic swept across the globe, are intended to promote orderly conditions in US dollar funding markets by providing liquidity backstops and their extension could signal the Fed’s commitment to minimize potential spillover effects from monetary normalization. At the same time, Chile, Colombia, Mexico and Peru all have access to the IMF’s Flexible Credit Line (FCL), a precautionary credit facility for which qualified members are pre-approved. Colombia drew down about USD 5.4 billion of its roughly USD 17.5 billion facility in December 2020. Other Pacific Alliance members have not utilized their FCLs.

In addition to the Fed’s dot plot surprise, financial markets in the region have also had a heavy electoral calendar to process. In Mexico, markets responded positively to the mid-term elections, June 6, which reduced President AMLO’s supermajority in congress to a simple majority, possibly viewing the outcome as consistent with stable policy frameworks. In Peru, market reaction to the recent presidential election was subdued compared to the volatility in the run-up to June 6, as markets there proved more sensitive to the pre-election polls than to the event itself. However, the Pen depreciated sharply, which our team in Lima regards as particularly noteworthy considering the sharp increase this year in metal prices, which would have normally led to appreciation. The Lima stock market also sold off, dropping nearly 14% following the elections (chart 2), while fixed income markets were less volatile this week in unusually low trading levels.

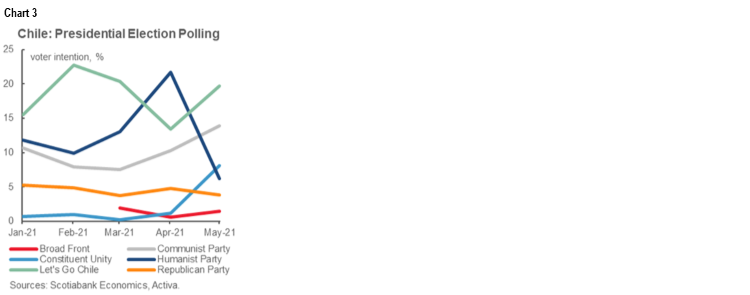

Chile’s presidential elections are next up on the electoral calendar, with coalition primaries scheduled for July 18. While it is too early to determine how the field will take shape post-primaries, polls suggest that candidates from the centre-right Chile Vamos (Let’s Go Chile) coalition rank highest in voter intention, followed by candidates from Chile’s communist party (chart 3). However, given that 16% of voters remain undecided, and it is unclear that voters of a specific candidate eliminated from the race will shift to another candidate from the same coalition, these results should be viewed with consideration caution.

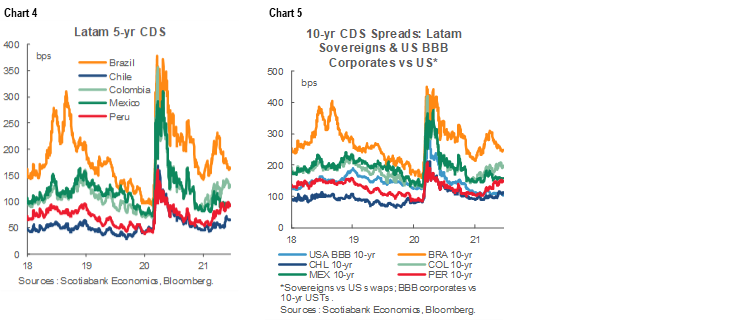

The possibility that less favourable global financial conditions are on the horizon underscores the importance of sound public finances and stable policy frameworks. Across the region, credit default swaps (chart 4) and 10-year CDS spreads (chart 5), which spiked at the outset of the pandemic, trended down over the course of 2020. Since early 2021, however, these indicators have risen in most Pacific Alliance countries, with increases in Colombia and Peru are especially pronounced. The increases on Peruvian assets likely reflect uncertainty in advance of the presidential elections and the subsequent vote tally. Similarly, widespread social protests in Colombia related to rising poverty and inequality may have eroded investor confidence.

In Peru, formal verification of the vote count and the formation of the cabinet could reassure investors if President-elect Castillo continues to moderate his policy pronouncements. In Colombia, meanwhile, an agreement by protest leaders to end the protests that have disrupted supply chains and affected production should assuage concerns.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—BCCh Signals an Early Start of the Normalization Process and Updates

Jorge Selaive, Chief Economist, Chile

56.2.2619.5435 (Chile)

jorge.selaive@scotiabank.cl

Carlos Muñoz, Senior Economist

56.2.2619.6848 (Chile)

carlos.munoz@scotiabank.cl

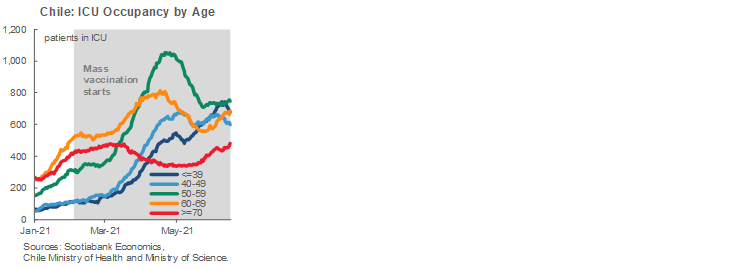

Amidst a rise in new cases and hospitalizations related to COVID-19 (first chart), authorities announced on Thursday, June 10, that the whole Gran Santiago area would return to strict lockdown starting on Saturday, June 12, for an indefinite period. While there are some indications of reduced mobility, we expect the impact on economic activity will be limited since people have adjusted to the “new normal” of life under lockdown. The impact on activity is also likely to be limited by a free mobility pass for fully vaccinated individuals (now almost 50% of Chile’s population). However, this pass does not affect certain services, such as restaurants, cafés and department stores, among others, which will not be open to the public.

On June 8, the central bank of Chile (BCCh) held its monthly monetary policy meeting, deciding again to hold the benchmark rate at 0.5%. This more hawkish stance affirms our view that the first hike will indeed occur in October 2021. On Wednesday June 9, the BCCh released its Quarterly Monetary Policy Report, whose main takeaway is the economy’s remarkable performance so far this year despite a decline in activity in March and April, which reflects a softer-than-anticipated impact of quarantines. In view of this solid performance, along with a much larger fiscal impulse and favourable external conditions, the BCCh has raised its range of forecasted GDP growth to 8.5%–9.5% y/y from 6.0–7.0% y/y in March.

In May, the Consumer Price Index increased 0.3% m/m (3.6% y/y), slightly above our forecast of 0.2% m/m, and below forward contracts (0.37% m/m). This outcome was driven by a higher core inflation, both in goods and services, as well as an increase in fuel prices.

In the political arena, the centre-left Unidad Constituyente (Constituent Unity) alliance was the big winner in elections for regional governors on Sunday, June 13. Combined with its first-round victories, the Constituent Unity bloc now controls 10 out of 16 regions—among them the Metropolitan Region of Santiago—making it the bloc with the broadest geographical strength. The election results suggest that moderate left-wing parties are positioned to gain votes in the November presidential election in which they will likely face a communist party candidate and two other candidates from the right-wing parties.

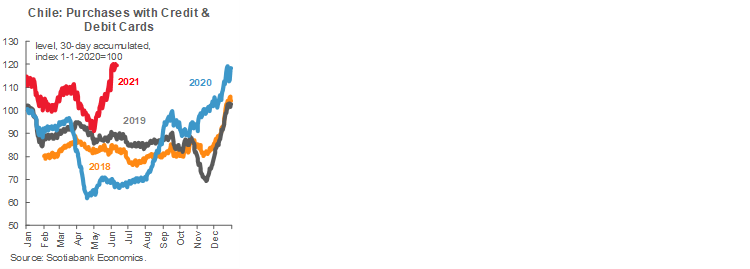

Our high-frequency indicators point to a new surge in purchases with credit and debit cards, evidence that the abundant liquidity coming from fiscal aid and the withdrawal of pension assets is fueling household consumption (second chart). This would confirm a solid recovery of private consumption during May, suggesting a high year-over-year expansion for the May monthly GDP.

In the fortnight ahead, on June 23, the BCCh will release the June Monetary Policy Meeting Minutes, which will provide more details on the discussion led by the Board regarding the decision to hold the policy rate at its technical minimum of 0.5%. We maintain our view that the first hike of 25 bps will occur in October 2021, with subsequent increases bringing the rate to 1.75% by December 2022.

On June 30, INE, the national statistical agency, will publish the performance of industrial production and retail sales for May. INE will also release the unemployment rate for the moving quarter ended in May, which we expect will remain around 10%, as job creation has slightly surpassed the increase in the workforce. The following day (July 1) the BCCh will publish the IMACEC (the monthly index of economic activity) for May, which we anticipate will expand by 15–16% y/y.

Colombia—Fiscal Announcements: A Balance Between Fiscal Responsibility and Social Policy

Sergio Olarte, Head Economist, Colombia

57.1.745.6300 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Jackeline Piraján, Economist

57.1.745.6300 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Along with other emerging market economies, Colombia faces a challenging situation requiring careful and clever management. The COVID-19 shock produced the deepest recession ever recorded in Colombia, with 2.5 million people falling into poverty and almost 2 million unemployed (10% of the labour force). By our calculations, COVID-19 has knocked off at least 1 ppt of annual growth from potential GDP for each of the next five years. The resulting negative effects on fiscal revenues from slower growth, together with rising demands for higher social expenditures to help Colombia recover from the pandemic, constrain fiscal policy going forward.

In addition, short-run prospects for the post-COVID-19 recovery are framed by widespread social discontent that is fueled by the increase poverty and unemployment. Protests add to fiscal policy challenges and have led to sporadic disruptions to production, putting pressure on prices and complicating monetary policy.

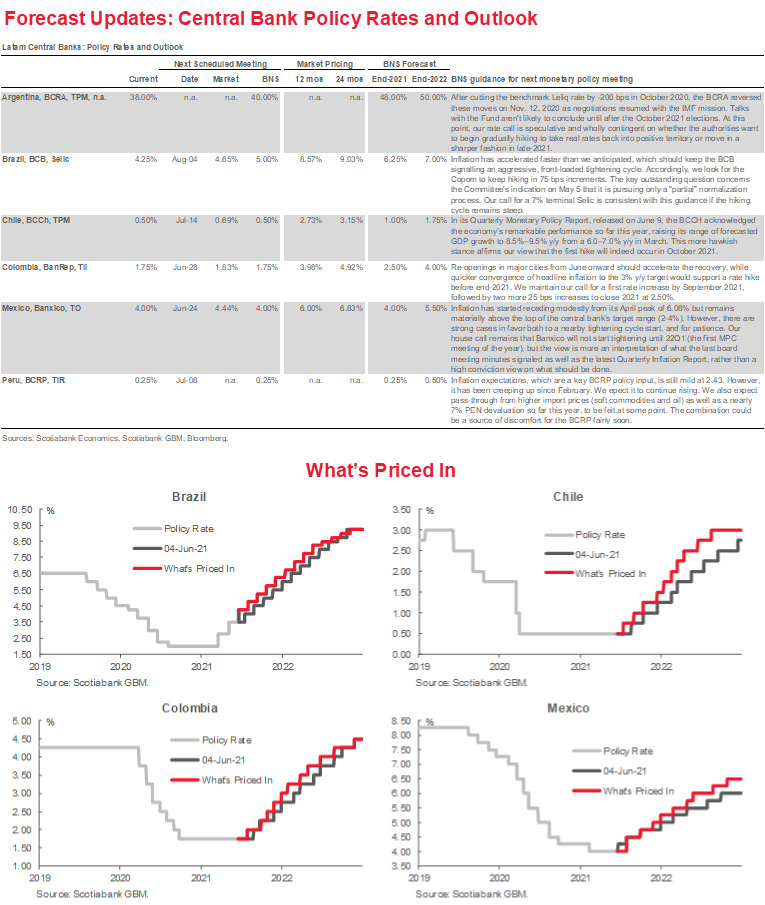

The convergence of these factors has led to a heavily indebted government (close to 65% of GDP) and an inflation rate slightly above target that will prompt BanRep to hike rates. We expect a 25 bp rate increase in the policy rate in September, followed by two more hikes before year-end.

To address the policy challenges posed by this conjuncture, on June 15, 2021 the Ministry of Finance (MoF) published its Medium-Term Fiscal Framework (MTFF) to signal the government’s commitment to fiscal responsibility and send a message to the general population that countercyclical policies will continue. Balancing these goals entails risks, but, overall, we think the MTFF strikes a good balance, at least on paper. To successfully implement the MTFF, the government will have to address two competing constraints.

On the one hand, the MTFF confirms that social expenditure and aid for the poorest will continue this year and next (at a fiscal cost of around 4 ppts of GDP per year). This support is intended to continue the assistance provided to more than 4 million employees and more than 3 million households in the pandemic and strengthen the health system. Together, these measures should reduce the social discontent of the general population.

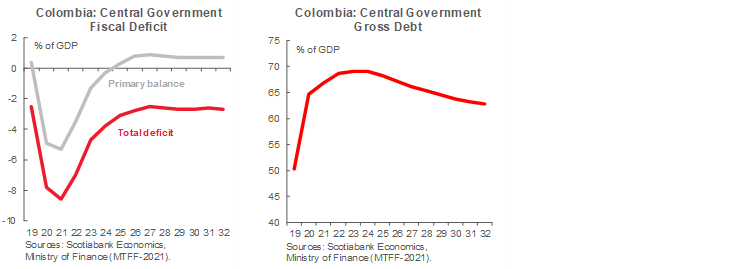

On the other hand, the cost of this commitment is that this year’s fiscal deficit will be the highest in history (8.6% of GDP, first chart). Moreover, the planned reduction in the deficit in 2022, although significant, will not be enough to stabilize the debt/GDP ratio. In fact, next year’s projected fiscal deficit of 7% of GDP would increase the debt/GDP to 68.6% (second chart). And given that Colombia is about to enter the presidential and congressional campaign season, even more pressure can be expected to be put on social programs that the public views are never enough, further fueling concerns about fiscal sustainability.

To finesse these constraints, the MTFF identifies two proposals designed to retain market and credit rating agency confidence in Colombian public finances in the face of rising social expenditures and a debt-to-GDP ratio that only starts to decline in 2024. The government intends to:

1. present a tax reform to congress in 2021 that would raise1.4% of GDP in revenues by increasing taxes on the wealthiest individuals and corporations in a gradual, two-step process; and

2. adopt a fiscal rule in 2022 that puts a ceiling on the debt/GDP ratio while subtracting from the structural allowed deficit calculation non-observable variables, such as potential growth, to reduce uncertainty on the future path of fiscal accounts.

In laying out these proposals, the MTFF noted that Colombia will need additional tax reforms to consolidate sustainability and stressed that the proposed new fiscal rule represents a significant change, amplifying the message that the government is committed to a fiscally responsible policy framework aimed at assuaging investor and rating agency concerns.

Two questions that arise after reading MTFF are: Will the proposals it outlines quell social unrest? And will the MTFF be enough to calm markets and placate international rating agencies? On the first question, while higher social expenditure and tax increases on the wealthiest would not eliminate social discontent, they could help de-escalate protests and curtail violence. Meanwhile, vaccine campaigns will concentrate on solving the COVID-19 shock that accounts for the increase in poverty and greater inequality. On the second question, we expect markets to react positively to the MTFF since it balances political reality while committing to fiscal sustainability. Having said that, we continue to believe that the probability of Fitch downgrading Colombia to junk grade this year is higher than 60%. In our view, however, markets have already priced in a downgrade and Colombian assets will continue moving in tandem with international risk appetite.

Mexico—Banxico’s Tough Dilemma: Communication Signals a Patient Approach, but Prudence Could Win Out

Eduardo Suárez, VP, Latin America Economics

52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

With the June 6 elections out of the way, market focus now turns back to the economic recovery and the Banxico policy debate. Inflation has started to recede from its April peak of 6.08% but remains materially above the top of the central bank’s target range of 2%–4% (first chart). However, strong cases can be made both for a near-term start to the tightening cycle and for patience.

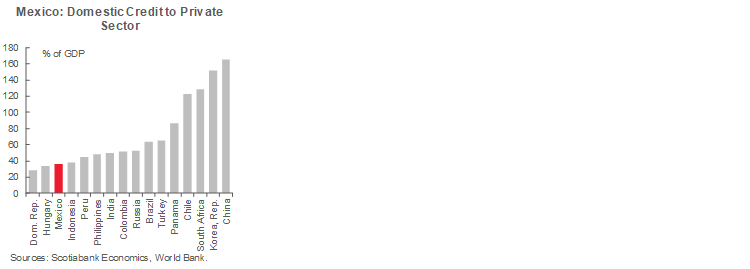

The risk that the near 6% y/y inflation (5.99% y/y in the latest bi-weekly print), which is currently driven by commodity price shocks and supply chain disruptions, will gain momentum militates for early action. Because monetary policy transmission channels are relatively shallow, with low domestic credit to the private sector, at 36.6% of GDP (second chart), and debt has a relatively long maturity, it would be unwise for Banxico to fall behind inflation.

The case for patience stems from Banxico’s recently revised forecasts (from the Quarterly Inflation Report), which have inflation converging to 3% by June 2022, well within the policy horizon, and the fact that the Governing Board has argued that recent price shocks reflect factors that monetary policy is not well suited to deal with: 1) global commodity prices (Mexico is a price taker), and 2) supply chain disruptions that are leading to shortages which in turn are driving price increases.

On balance, we think that Banxico will not start tightening until Q1-2022 (the first MPC meeting of the year), but this view is more an interpretation of what the last board meeting minutes signaled and our reading of the latest Quarterly Inflation Report, rather than a high conviction view on what should be done.

Our own view is that an earlier start of the tightening cycle would be the prudent course for Banxico, particularly since we see two additional emerging risks even as current inflation shocks fade. First, a rebound in the economy this year will likely give companies the opportunity to rebuild balance sheets and restore profit margins squeezed by recent cost pressures, which include the almost 40% cumulative minimum wage increases of the past 2 years, the elimination of the outsourcing regime, as well as energy price shocks. Second, we expect a very strong rebound in service sector activity leading to price pressures, combining with base effects that will boost y/y inflation rates towards the end of the year.

A further consideration is that, with the BCB’s Selic policy rate now higher than Banxico’s target range, MXN seems to be underperforming BRL, with possible effects on competitiveness. A weakening trend in the currency could be one more factor pushing Banxico to tighten earlier than anticipated.

On the growth side, the recovery remains fragile, largely owing to parts shortages that have led to manufacturing supply chain disruptions. However, we anticipate that as H2-2021 plays out, the recovery will broaden, with the services sector benefiting from re-openings in tourism and entertainment-related services—currently the economy’s weakest links, but which look poised for a very strong second half of the year. In fact, last week the improving outlook for the services sector—led us to revise our 2021 GDP forecast from 4.9% to 5.3% y/y.

Peru—Post-Elections Blues

Guillermo Arbe, Head of Economic Research

51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

Mario Guerrero, Deputy Head of Economic Research

51.1.211.6000 Ext. 16557 (Peru)

mario.guerrero@scotiabank.com.pe

After a week of uncertainty, protests, mutual accusations of attempted fraud, and nervous waiting for authorities to validate votes, a certain sense of calm—or perhaps exhaustion would be the better term—has descended upon the country.

Election authorities finalized the vote count on June 15, with Pedro Castillo holding a 44,000 vote lead over Keiko Fujimori. However, requests from the parties of both candidates for the annulment of votes, which may take a few days yet, still need to be resolved. While the formal vote tally is in, the narrow lead that Castillo held throughout the counting and validation process has weighed on public opinion and the markets. Once a winner is declared officially, the next piece of information needed to assess the profile and likely policy direction of the new government is the names of the cabinet members. The deadline for this milestone is the July 28 inauguration, although the names of key cabinet members are typically announced much earlier.

Market reaction to the elections was relatively subdued compared to the volatility in the run-up to June 6, as markets proved more sensitive to the pre-election polls than to the event itself. However, the PEN/USD exchange rate shot up 5.8% from 3.77 at its close on Friday June 4 to open at 3.99 on June 8. It has since fluctuated in a 3.85–3.95 range. This represents a loss of approximately 6.5% in the value of the PEN year-to-date. This depreciation is particularly noteworthy considering the sharp increase this year in metal prices. If not for political developments, the PEN would likely have appreciated rather than depreciated this year. The Lima stock market also sold off, dropping nearly 14% following the elections, although a relatively mild, albeit abrupt, drop in global metal prices no doubt contributed to the sell off. Fixed income markets were less volatile this week in unusually low trading levels.

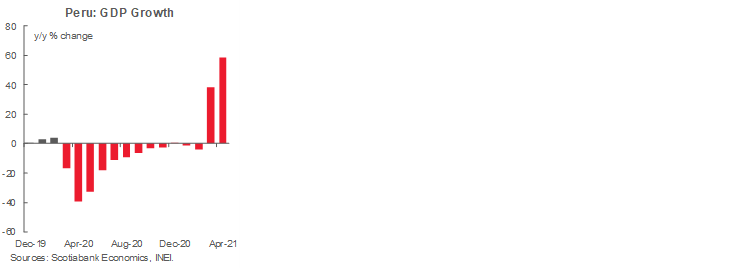

In about six weeks Peru will have a new president and Congress. The new authorities will be handed an economy that is improving nicely, with GDP growth in April of 58.5% y/y (first chart). As impressive as this result may seem, it largely reflects a rebound from an economy in severe lockdown in April 2020. To put the figure in perspective, April 2021 GDP was 3.5% lower than pre-COVID-19 April 2019.

Strong GDP growth likely continued in May, albeit not as high as in April. One indicator is electricity demand, which was up 35.6% y/y in May, versus 42.3% y/y in April (second chart).

Overall, the GDP growth trend supports the view that the rebound in production is faster and more significant than initially envisioned (second chart). However, such high growth figures obscure the impact that political—and policy—uncertainty may be having on growth, and which would otherwise be more evident. The make up of the next cabinet will provide a better sense of the new government’s policy direction.

The incoming government will also inherit an improving COVID-19 situation. Hospitalizations are 30% off their highs, and over 16% of the population has received at least one vaccination dose.

In addition, the next government will benefit from high metal prices, which should provide more fiscal space. The 12-month rolling fiscal deficit fell to 6.7% of GDP in May, declining for a third consecutive month from a high of 9.0% in February. Fiscal accounts give a positive picture, overall. While the government is spending strongly to stimulate the economy, revenue is improving enough to slowly close the fiscal gap.

Inflation came in at 2.45% for May and has remained rather stable in the 2.4% to 2.7% range so far throughout 2021. However, inflation expectations have begun creeping up, rising by 32 basis points since February. The figure now stands at 2.43%, which is not worrisome in itself, but does result in a negative real reference rate of -2.18%. We are monitoring inflation for signs of pass-through from high soft-commodity and oil import prices and the depreciation of the PEN.

We believe that some pass-through effects will eventually materialize, driving inflation expectations higher, and if so the BCRP may need to evaluate whether to raise its rate sooner rather than later. For now, we maintain our call for a rate hike in mid-2022.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | carlos.munoz@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.